Real estate syndication — the pooling of capital from multiple investors to acquire properties that no single investor could access alone — is growing rapidly in the UK as individual buy-to-let becomes less viable for higher-rate taxpayers. Syndications allow investors to access commercial buildings, large residential blocks, and development sites at institutional scale while retaining more direct involvement than a REIT or fund provides. This guide explains the structures, the economics, and the due diligence required to participate safely.

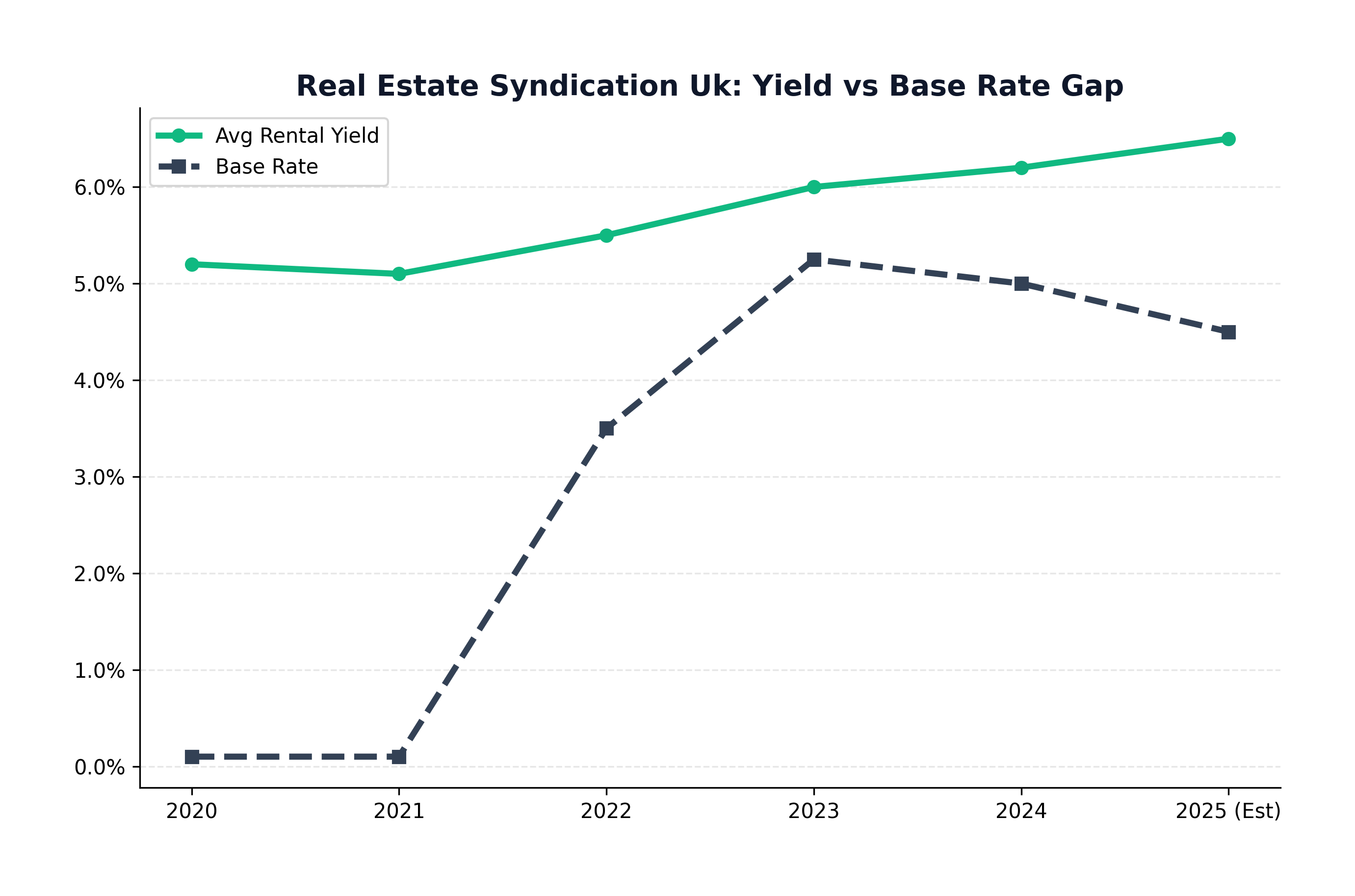

Figure: Yield vs Interest Rates

Figure: Yield vs Interest Rates

Syndication vs REITs: The Critical Distinctions

A Real Estate Investment Trust (REIT) is a listed company; you buy shares on the stock exchange and have no say over individual asset decisions. A syndication gives you direct (or near-direct) ownership of a specific asset or portfolio — typically structured as a share in a Limited Liability Partnership (LLP) or a Special Purpose Vehicle (SPV) limited company. This distinction matters for tax transparency, control, and alignment of interests.

In a well-structured syndication, the lead investor (the 'Sponsor' or 'General Partner') co-invests their own capital alongside passive investors (the 'Limited Partners' or syndicate members). This alignment of interests — the Sponsor losing money if the deal fails — is the most important structural safeguard. Minimum investment thresholds typically range from £25,000 to £100,000 per investor, limiting participation to those with sufficient capital to withstand illiquidity.

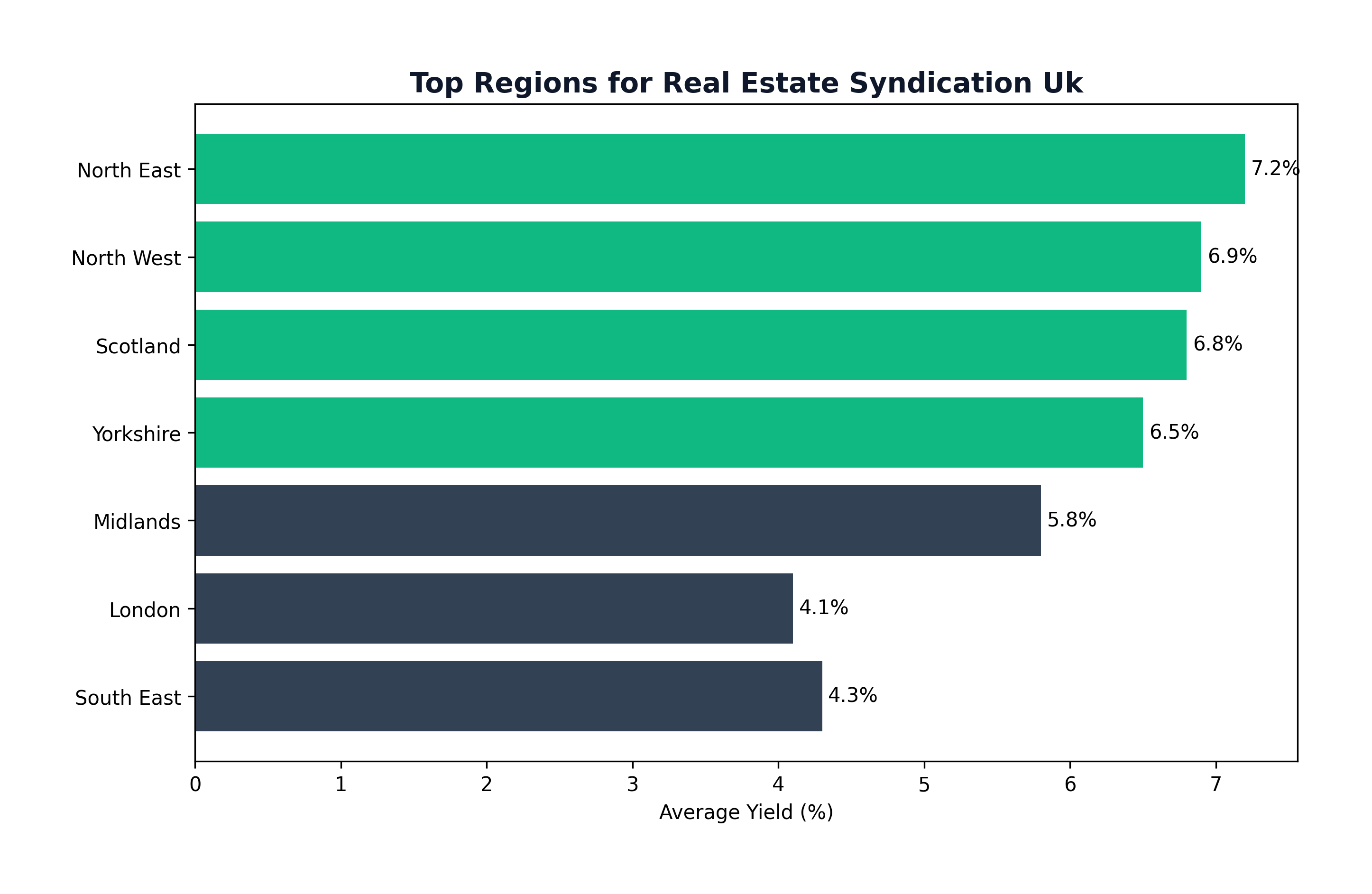

Figure: Regional Yield Heatmap

Figure: Regional Yield Heatmap

Legal Structures for UK Syndicates

LLP vs SPV (Limited Company)

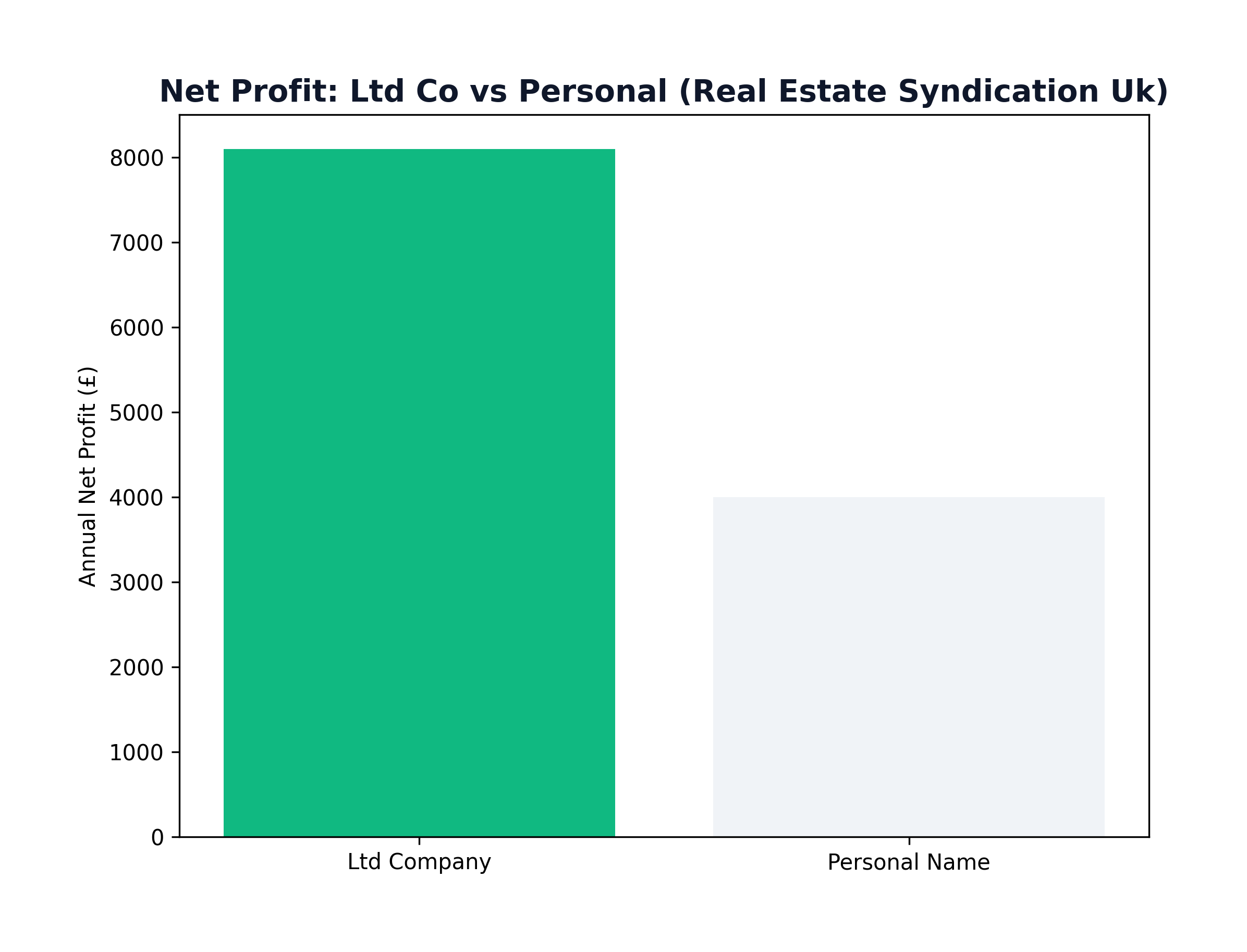

The Limited Liability Partnership structure offers tax transparency — investors are taxed as individuals on their proportionate share of profits, with capital gains flowing through at personal CGT rates. This can be advantageous for basic-rate taxpayers and those with existing capital loss carry-forwards. The SPV (limited company) structure means profits are taxed at corporation tax rate (25%) before distribution, but retained profits can be reinvested at a lower effective rate. Most UK syndicates now use SPV structures to allow easier mortgage financing, as lenders are more familiar with SPV lending.

A Deed of Trust or Shareholders' Agreement is the legal bedrock of any syndication. This document must specify: the profit waterfall (how returns are distributed), the Sponsor's fee entitlements, the voting rights of investors on major decisions (sale, refinancing), exit provisions if an investor needs to withdraw early, and the decision-making process if the Sponsor defaults. Cutting corners here is the leading cause of syndication disputes. Budget £3,000–£5,000 for a specialist property solicitor to draft these documents properly.

Figure: Tax Trap: Personal vs Ltd

Figure: Tax Trap: Personal vs Ltd

The Economics of Syndication

Returns in a syndication are typically expressed as a combination of cash-on-cash return (the annual dividend relative to capital invested) and Internal Rate of Return (IRR) — which accounts for the timing and magnitude of all cash flows including the final sale. A well-run UK commercial syndication should target a cash-on-cash return of 6–8% per annum during the hold period, with an IRR of 12–18% over a 3–7 year hold, depending on market conditions and leverage.

The 'performance promote' or 'carried interest' is the Sponsor's share of profits above the agreed hurdle rate (typically 8–10% preferred return to investors). This structure incentivises the Sponsor to maximise returns — they earn nothing from the promote until investors have received their preferred return in full. Understanding the waterfall mechanics before investing is non-negotiable.

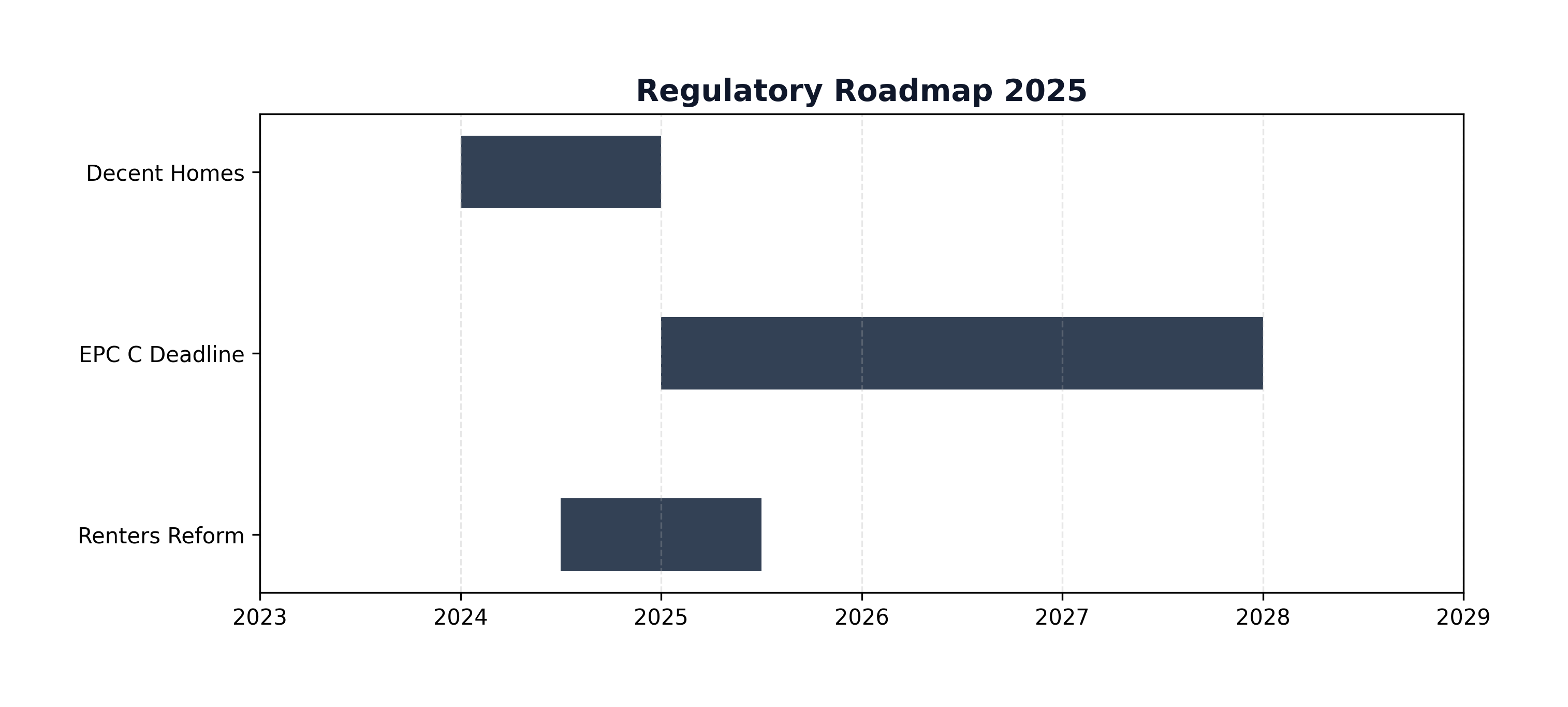

Figure: Regulatory Roadmap

Figure: Regulatory Roadmap

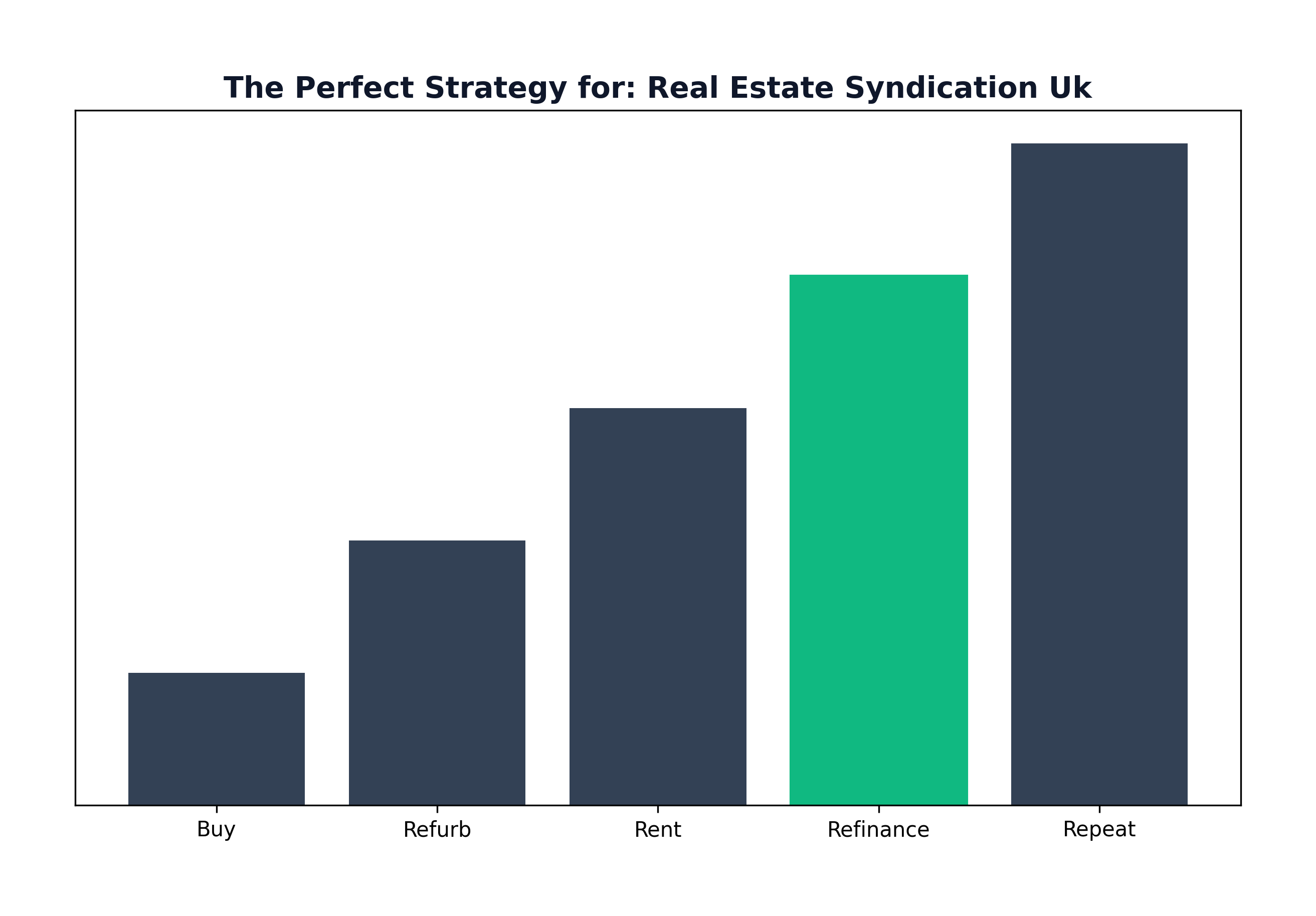

Joint Ventures: The Private Syndication

For investors with capital but without operational expertise, a Joint Venture (JV) with an experienced operator is the most common private syndication model. The classic structure is 'cash versus time' — one party provides the deposit capital, the other sources the deal, manages the refurbishment, places the tenant, and handles ongoing management. Profit is split by agreement, typically 50/50 or 60/40 in favour of the cash partner on the first deal.

Finding partners through Property Investor Network (PIN) meetings, Progressive Property events, or online forums (Property Hub forum) is legitimate and common. The legal protection of all JVs — regardless of how well you know the partner — is a Deed of Trust or JV Agreement prepared by a solicitor. Never proceed on a handshake. The most common JV failures occur when roles, responsibilities, and profit splits are assumed rather than documented.

Figure: Strategy Cycle

Figure: Strategy Cycle

Risk Analysis and Due Diligence

Illiquidity is the defining risk of syndication. Your capital is locked into the asset until the Sponsor decides to sell or refinance — typically 3–7 years. There is no secondary market for syndication stakes in the UK (unlike REITs, which trade daily). Investors must be comfortable that they will not need this capital during the hold period. Key-man risk — the dependency on a specific Sponsor to manage the asset — is significant. What happens if the Sponsor becomes ill, goes through a divorce, or simply underperforms? The legal documents should specify governance in these scenarios.

When diligencing a Sponsor, the minimum checklist should include: a verified track record of previous syndications with references from past investors (not testimonials on a website), audited financial statements for the proposed SPV or LLP, a third-party valuation of the target asset, a stress-tested financial model (not the optimistic base case), and evidence of the Sponsor's own co-investment. Red flags in Offering Memorandums include projected occupancy rates above 90% for serviced accommodation, IRR projections above 25% without detailed justification, and exit strategies dependent on market conditions that cannot be controlled.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →