Is property still a good investment?

If you read the headlines, you'd think the "Golden Age of Buy-to-Let" is over. Higher interest rates, the abolition of Section 24 tax relief, and new tenant rights have scared away many amateur landlords.

But here is the reality: Rents are up 8-10% year-on-year. Demand is at an all-time high because house building has stalled.

Property is not dead. The "amateur era" is dead. If you treat property like a hobby, you will lose money. If you treat it like a business, the returns in 2026 are still unbeatable.

This guide is your roadmap to doing it right.

1. The 2026 Investment Landscape

Before you buy, understand the new rules of the game:

- Interest Rates: No longer 1%. Plan for 4.5% - 5.5%. Your deal must stack up at 6% to be safe.

- The "Coverage Ratio": Lenders now require your rent to cover 145% of the mortgage payment (at a stress-tested rate of 5.5%). This means you need bigger deposits (25-30%).

- Tax: If you are a higher-rate taxpayer, owning property in your personal name is tax suicide. You pay tax on revenue, not profit.

2. The 7-Step Investment Roadmap

Step 1: Strategy First

Don't browse Rightmove yet. Decide what you want:

- Cashflow: I need £500/month extra income now. (Strategy: HMOs in the North).

- Growth: I have a lump sum and want it to double in 10 years. (Strategy: Single Lets in regeneration zones).

Step 2: Entity Structure (Crucial)

Sole Trader vs Limited Company (SPV)

- Sole Trader: Easier setup, but higher tax and no mortgage interest relief.

- Limited Company: Pay Corporation Tax (19-25%). Full mortgage interest relief.

- Verdict: For most new investors in 2026, buying via a Limited Company is the only viable option. Speak to an accountant first.

Step 3: Financial Stress Test

Can you survive a "perfect storm"?

- 3 months of void periods (no tenant).

- A £2,000 boiler repair.

- Interest rates hitting 6%. If these bankrupt you, do not buy.

Step 4: Sourcing (Finding the Deal)

Rightmove is the shop window. The best deals are found in the stock room.

- Direct to Vendor: Leaflet campaigns or letters to tired landlords.

- Auctions: Speed and certainty, but you must do due diligence before bidding.

- Relationship Building: Call estate agents weekly. Be the "reliable buyer" they call before listing on Rightmove.

Step 5: Due Diligence

Use the 10-2-5 Rule:

- View 10 properties.

- Offer on 2.

- Buy 1 that will profit for 5 years.

- Check: Flood risk, planning permission, crime rates, and comparable sold prices (not asking prices).

Step 6: Legals & Compliance

The Renters' Rights Bill is coming. You must be compliant:

- EPC C-Rating: Deadline 2030 (proposed). Don't buy an F-rated house unless you have the budget to fix it.

- EICR: Electrical safety every 5 years.

- Gas Safety: Annual.

Step 7: Management

Self-manage to save 12%? Or pay an agent?

- If you have a full-time job, pay the agent. Your time is worth more than £80/month.

- A bad tenant costs more than 10 years of management fees. Good referencing is non-negotiable.

3. Core Strategies Explained

Vanilla Buy-to-Let

- What: Buying a house/flat and renting it to one family.

- Pros: Low effort, easy to finance.

- Cons: Lower cashflow (typically £200-£300/month net).

HMOs (House in Multiple Occupation)

- What: Renting rooms individually to 3+ unrelated people.

- Pros: High cashflow (often double a single let).

- Cons: High regulation (licensing), high tenant turnover, higher utility bills (you usually pay bills).

BRR (Buy, Refurbish, Refinance)

- What: Buy a wreck, add value, refinance to pull your money out.

- Pros: You can recycle your deposit and buy multiple houses.

- Cons: High risk. If the valuation comes in low, your money is trapped.

4. The Tax Minefield (2026 Update)

- SDLT Surcharge: Investors pay a 5% surcharge on top of standard Stamp Duty rates (from April 2026). Factor this in!

- Capital Gains Tax: The annual exempt amount is now just £3,000. If you sell a house, you pay tax on almost all the profit.

- FHL Abolition: The tax perks for Furnished Holiday Lets (Airbnbs) are being scrapped in April 2026. Many Airbnb hosts are selling up—this could be a buying opportunity for long-term investors.

5. Conclusion

Property investment is a marathon, not a sprint. The days of "get rich quick" are gone. The days of "build sustainable wealth slowly" are here to stay.

Start small. Get educated. Treat it like a business.

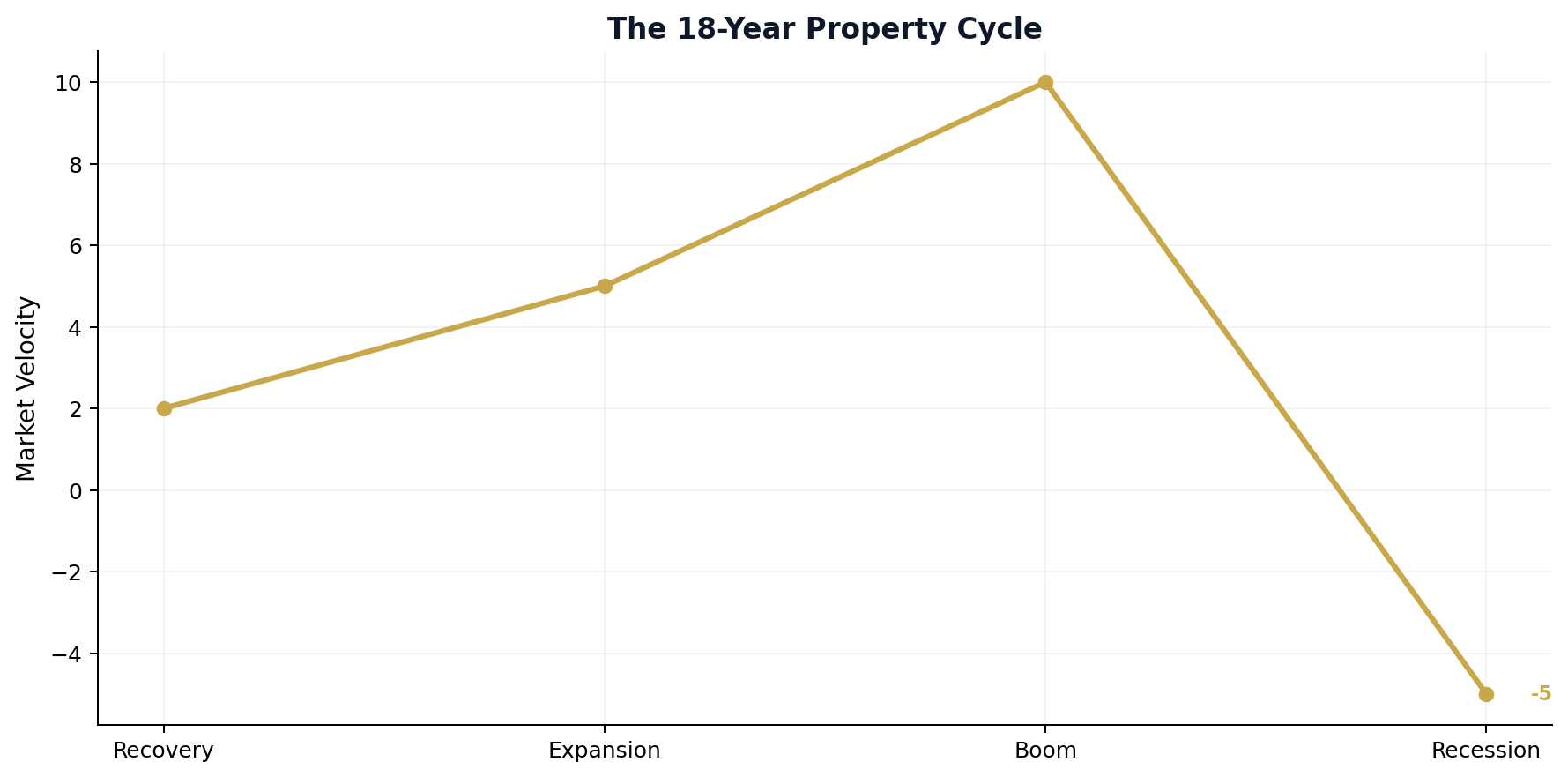

Figure: The 18-Year Property Cycle

Figure: The 18-Year Property Cycle

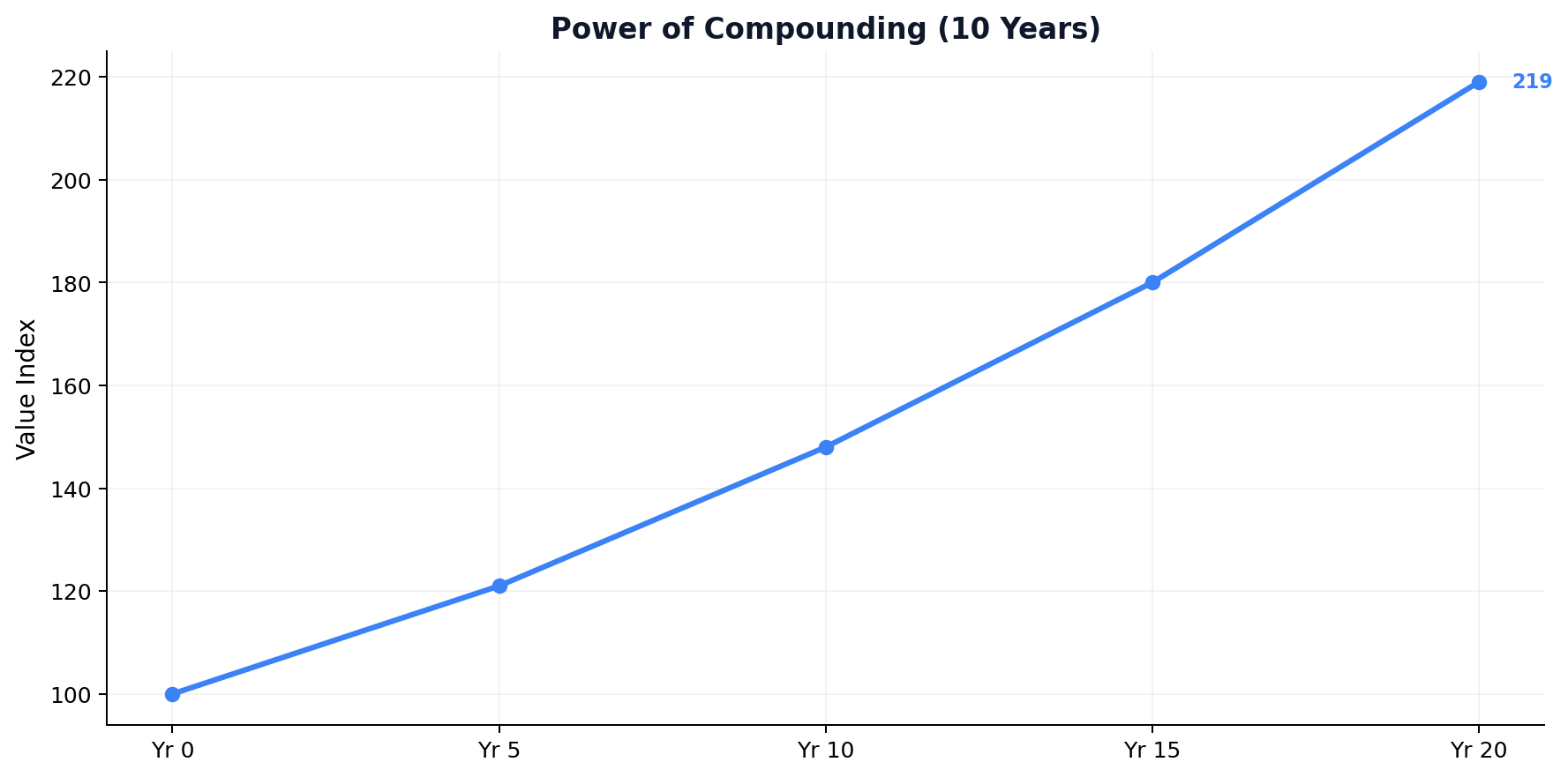

Figure: The Power of Compounding

Figure: The Power of Compounding

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →