The allure of purchasing a run-down property, injecting a moderate sum into renovations, and walking away with a hefty lump-sum profit is deeply ingrained in UK real estate culture. Television shows have spent decades making the "fix and flip" strategy look like the ultimate fast track to financial freedom. Yet, as we progress deeply into 2026, the question on many serious investors' minds is clear: is fix and flip property worth it today?

The short answer is yes – but the landscape has fundamentally shifted. Gone are the days when casual investors could rely on explosive double-digit house price inflation to mask budgeting errors or sluggish timelines. Today, the UK property flipping sector is characterised by one undeniable truth: profitability is mathematically manufactured, not incidentally achieved. It requires an almost clinical approach to sourcing, renovation management, and exit structuring.

This comprehensive guide breaks down the financial realities of property flipping in the UK today. We dive into evolving market trends, the fierce reality of holding costs, newly structured tax environments, and data-backed comparisons that illustrate exactly where the margins lie.

1. The Professionalisation of the Market

In 2026, the era of the "amateur flipper" is largely over. Several converging economic factors have forced a deep professionalisation of the fix and flip sector. Over the last four years, the market has seen increased costs of short-term financing, stringent legislative changes to energy efficiency standards, and a plateaued pricing paradigm where buyers are profoundly data-conscious and heavily reliant on detailed survey findings to dictate their offers.

Historically, if an investor overspent by £15,000 on a renovation, general market appreciation would often absorb that mistake. If you held a property for five months instead of three, the market might push its value up enough to cover the extra bridging loan interest. In 2026, those safety nets do not exist. Margins are painfully tight, and failing to adhere strictly to your initial budget directly erodes your net takeaway.

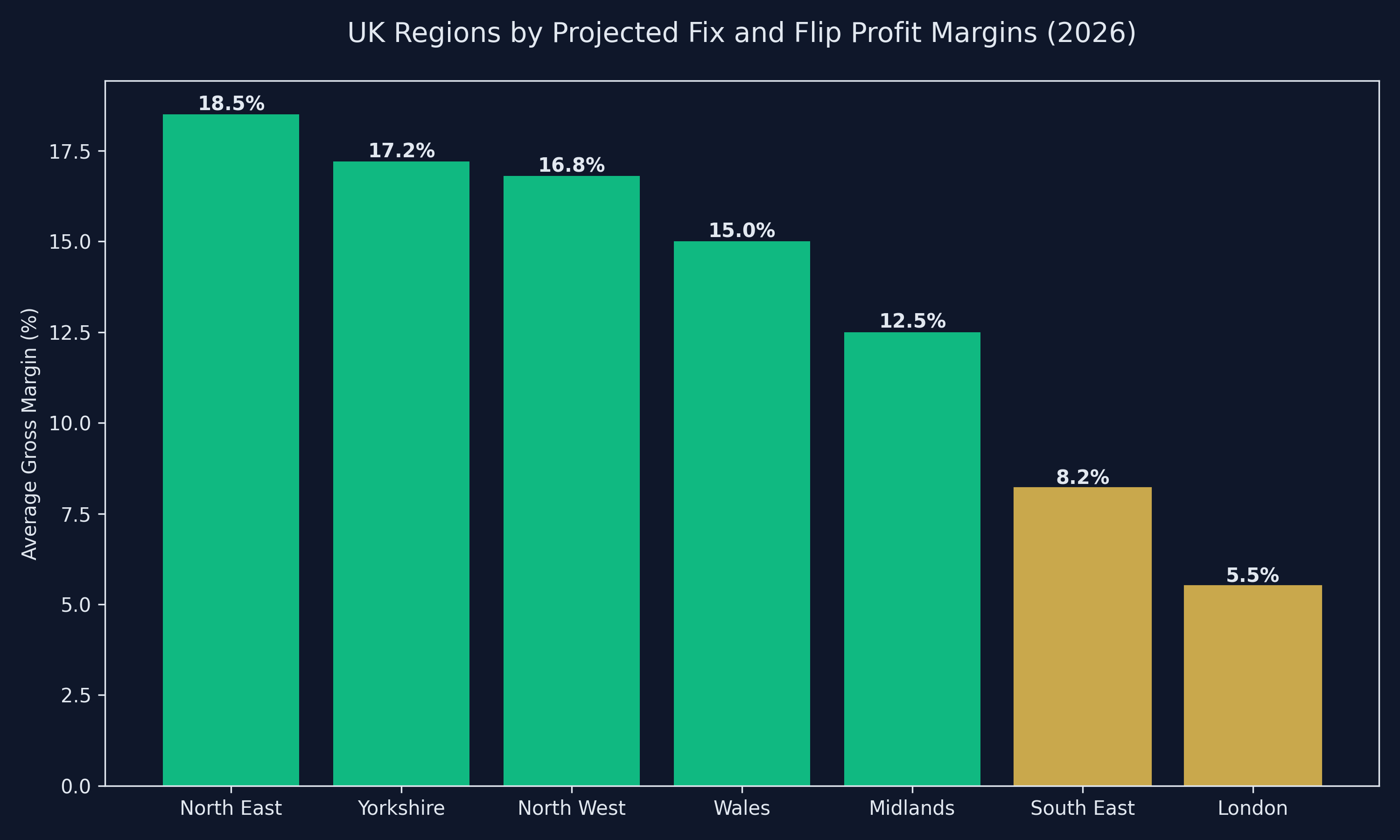

For those considering this strategy, UK property flip margins 2026 projections reveal that average gross margins have compressed from roughly 21% a decade ago to around 12-16% today, depending largely on geographic location. Professional flippers are countering this compression by relying on robust local networks of tradespeople to lower costs, aggressive negotiation tactics to secure under-market deals at the initial stage, and precise schedule management to keep construction periods incredibly lean.

[PLACEHOLDER_GRAPHIC_1]

2. North vs South: The Geographic Divide

One of the largest determinants of whether a fix and flip project is viable is geography. A stark contrast has emerged between the North and Midlands versus London and the South East. Historically, London was the epicenter of flipping due to astronomically high resale values. Today, it presents some of the most significant risks for speculative investors.

Why the shift? High Stamp Duty Land Tax (SDLT) burdens and immense capital requirements mean that flipping property in the South requires a level of financing that quickly destroys profit margins through vast interest payments. Furthermore, a ceiling of affordability has been hit in the South East, meaning "Done Up" resale prices simply aren't growing fast enough to justify the sheer cost of property acquisition and premium Southern labour rates.

Conversely, the North of England (particularly North West and Yorkshire) alongside regions in Wales and the Midlands offer much more forgiving entry prices. Here, an investor can acquire a standard semi-detached terraced house for under £140,000. When comparing a North vs South property flip, the sheer velocity of capital in the North allows investors to recycle their cash faster, executing multiple projects a year rather than tying up half a million pounds in a single, high-risk Southern asset.

[PLACEHOLDER_GRAPHIC_4]

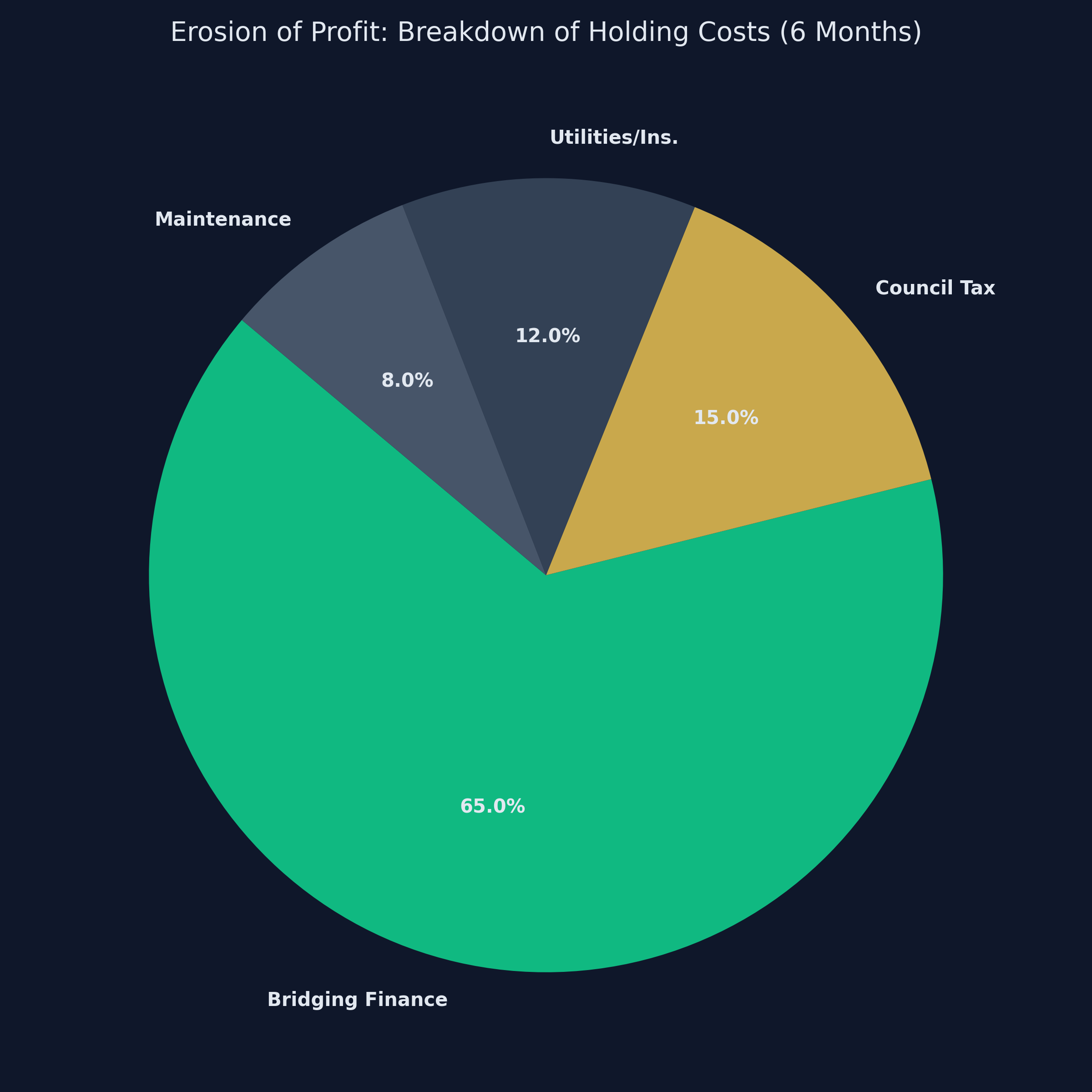

3. The Silent Margin Killer: Holding Costs

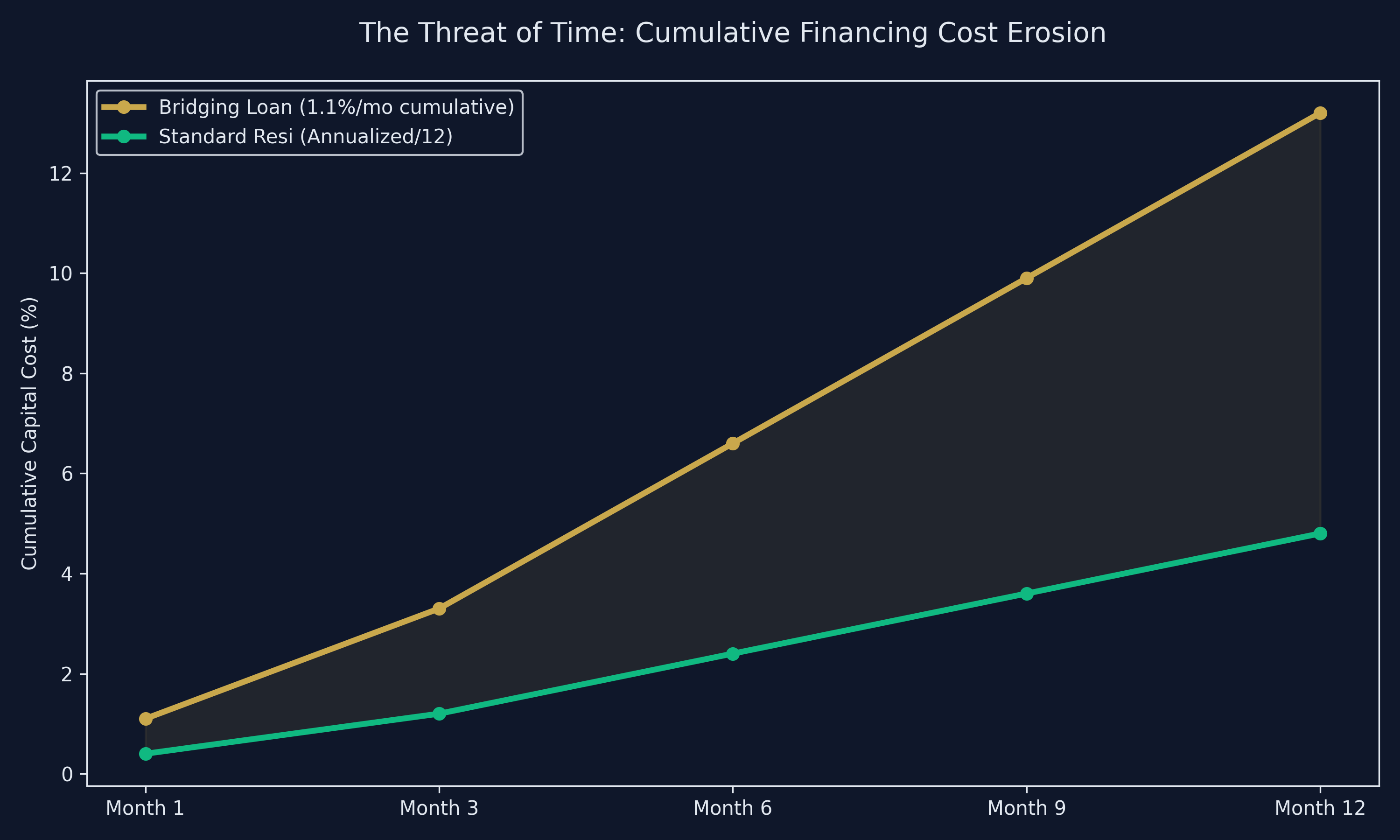

While investors tend to focus obsessively on their renovation material and labour costs, the most significant threat to a flip is often ignored until it is too late. Holding costs in property flipping are the ongoing financial obligations you incur simply by owning an empty property during the renovation and sales period.

Every single day you own the property, your potential profit shrinks. The largest culprit is short-term finance. Due to the un-mortgageable condition of many perfect flip properties (e.g. absent kitchens, severe structural defects), investors rely on bridging finance. These loans might charge between 0.8% and 1.5% per month. On a £200,000 borrowed amount, a 1% monthly rate equates to £2,000 leaking from your profit every 30 days.

- Bridging Interest: Accrues daily, capitalizing over time.

- Council Tax: Empty properties in many UK councils now face huge council tax premiums (up to 300% in some regions) specifically designed to penalise empty homes.

- Utilities and Insurance: Vacant property insurance is notably more expensive than standard landlord insurance, whilst standing charges on gas and electric keep ticking.

- Security: If a site is gutted, securing it against theft of raw materials (like copper pipes and boilers) adds direct costs.

Because the UK conveyancing system is notoriously slow, taking an average of 4 to 5 months to move from "offer accepted" to completion in 2026, those holding costs stretch out painfully long after the renovation tools have been packed away.

[PLACEHOLDER_GRAPHIC_2] [PLACEHOLDER_GRAPHIC_7]

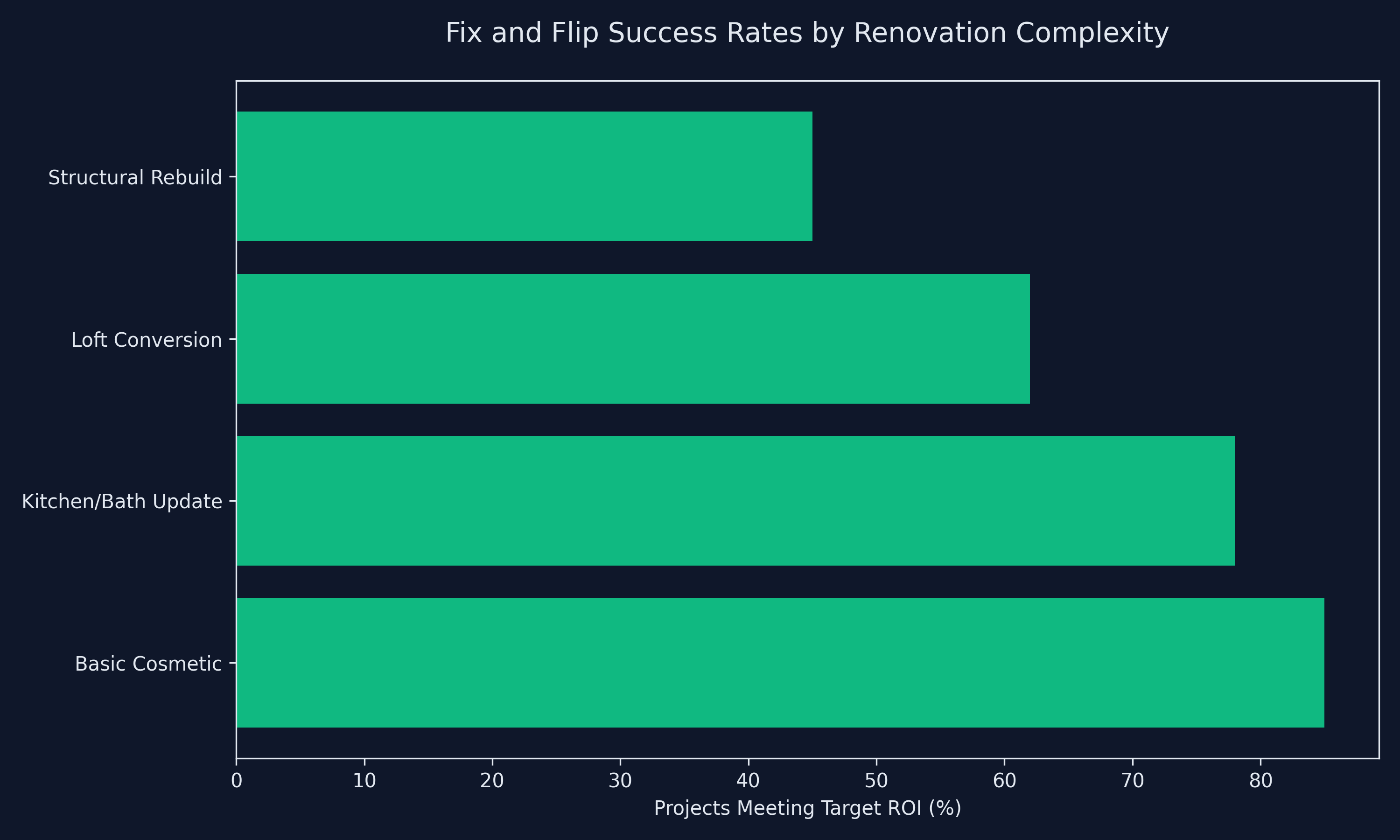

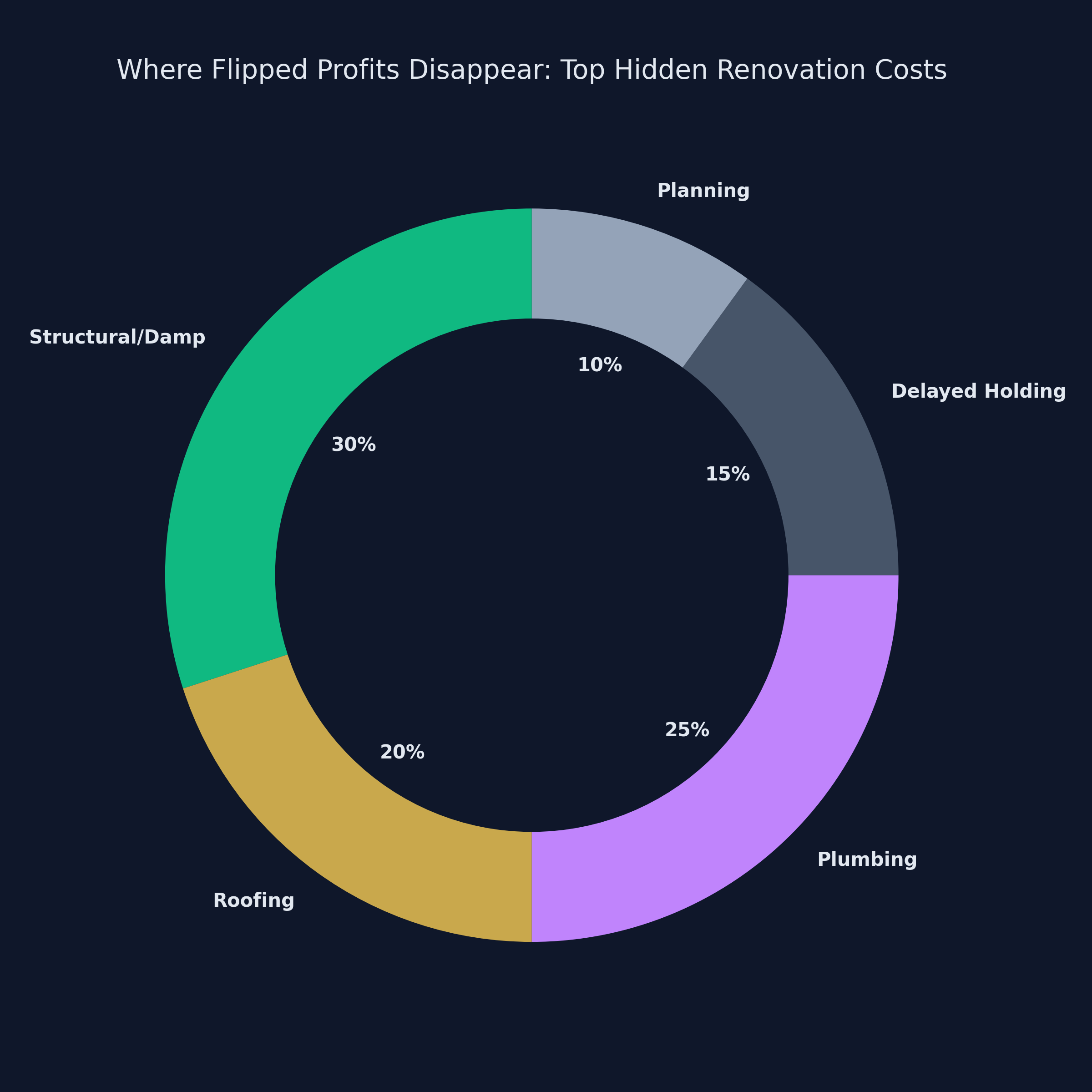

4. Structuring for Returns: Cosmetic vs. Structural Renovation

When an investor buys a property, they must decide immediately whether they are taking on a cosmetic refresh or a structural overhaul.

Cosmetic Flips: These are properties that are structurally sound but aesthetically exhausted. Think vintage 1970s carpets, wood-chip wallpaper, dated avocado bathroom suites, and overgrown gardens. The work involves peeling back the ugly layer, plastering, painting, fitting standard kitchens and bathrooms, and staging. These projects are mathematically safer. They are predictable, rely on standard trades, and can often be turned around in 6 to 8 weeks.

Structural Flips: These involve heavy lifting. We're talking underpinning, damp-proof courses, massive structural steelwork for open plan living, extensions, or loft conversions. While structural work can theoretically boost the end-value (After Repair Value or ARV) substantially more than cosmetic work, it inherently carries execution risk. You rely on heavily backlogged local planning councils for sign-off, you face volatile materials pricing for heavy construction, and the timeline can easily blow out from 3 months to 9 months due to unpredictable factors like uncovering severe dry rot or facing terrible winter weather.

Data clearly indicates that the highest volume of successful investors who consistently hit their target ROI are those running tight, predictable cosmetic upgrades over high-risk structural gambles.

[PLACEHOLDER_GRAPHIC_5] [PLACEHOLDER_GRAPHIC_9]

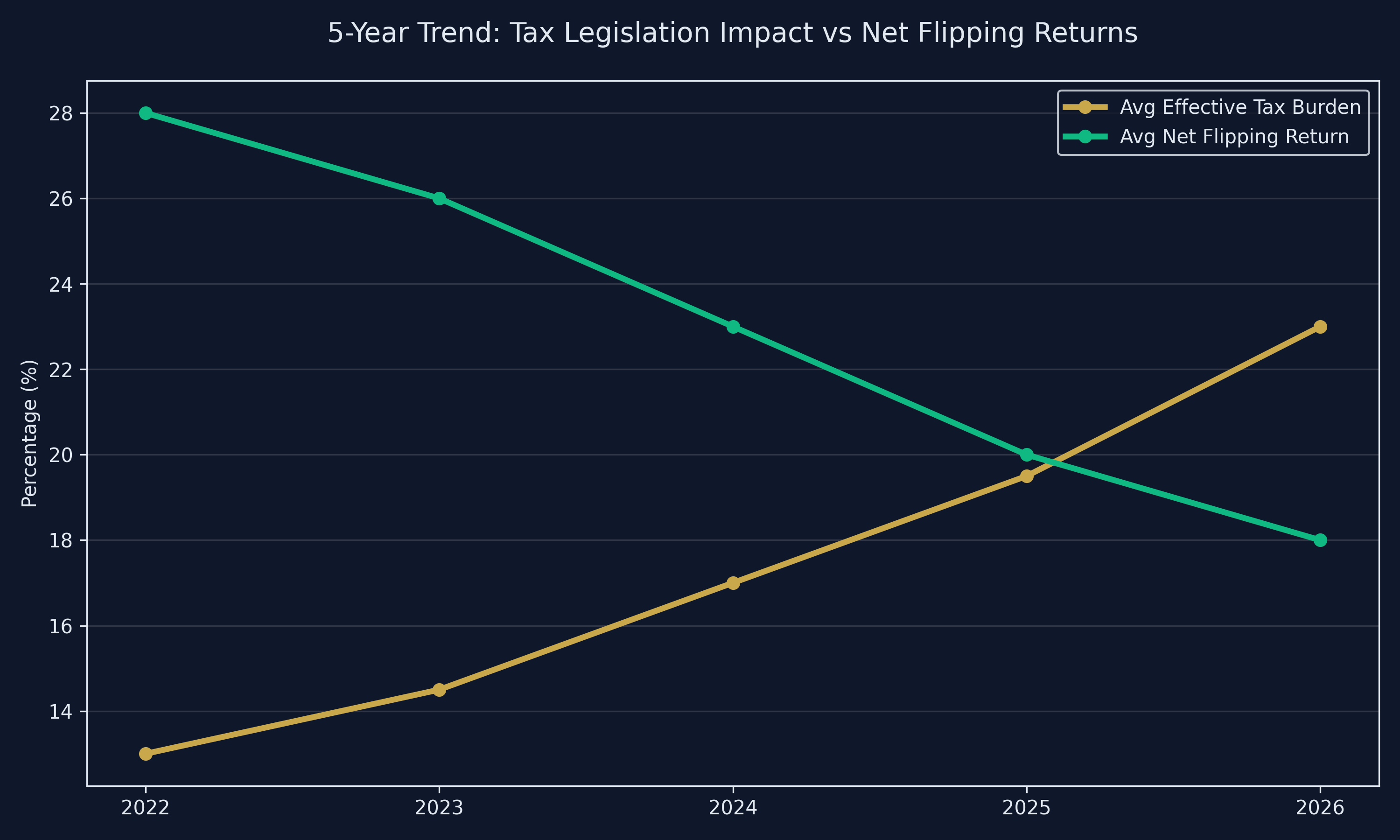

5. The Legislation Squeeze: Taxation and Energy Efficiency

Any article exploring whether a fix and flip property is worth it must heavily underline the new regulatory environment of 2026. The government has placed intense legislative pressure on the private housing sector.

A New Tax Environment

Recent fiscal policies have fundamentally altered the tax landscape. UK property tax changes 2026 directly assault the gross margins of a flip. Aside from standard Corporation Tax (if flipping within a Limited Company—which is currently the only viable method for professional investors), investors are battling strict Capital Gains Tax (CGT) reductions for individual investors and punishingly high non-residential Stamp Duty rates. HMRC has introduced tighter compliance metrics, removing leeway for delayed reporting.

[PLACEHOLDER_GRAPHIC_3]

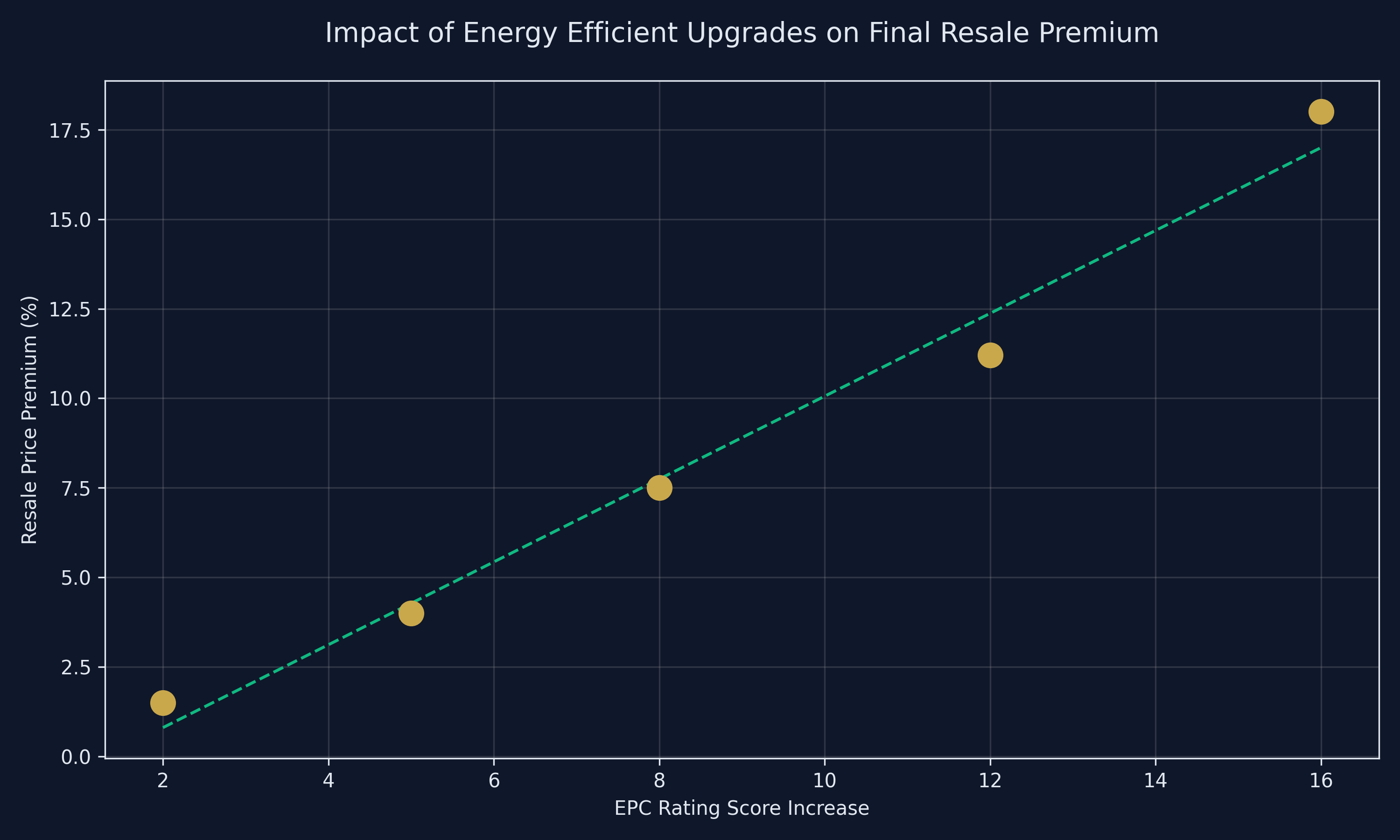

Energy Efficient Renewals

One of the most profound shifts in buyer psychology today is the paramount importance of utility efficiency. Due to chronically high energy baselines, modern UK buyers fiercely scrutinise a property's Energy Performance Certificate (EPC). If your freshly renovated flip boasts a massive open-plan kitchen but maintains an EPC rating of 'E' with old single glazing and zero loft insulation, it will stagnate on the market.

Implementing energy efficient renovations UK is no longer a "nice to have"; it is a foundational requirement to achieve your target ARV. Things like solar panel pre-wiring, modern efficient boiler systems, comprehensive draft-proofing, and air-source heat pump retrofits physically add to the resale premium of the house. Ignoring the energy efficiency aspect practically limits your buyer pool by 60%.

[PLACEHOLDER_GRAPHIC_6]

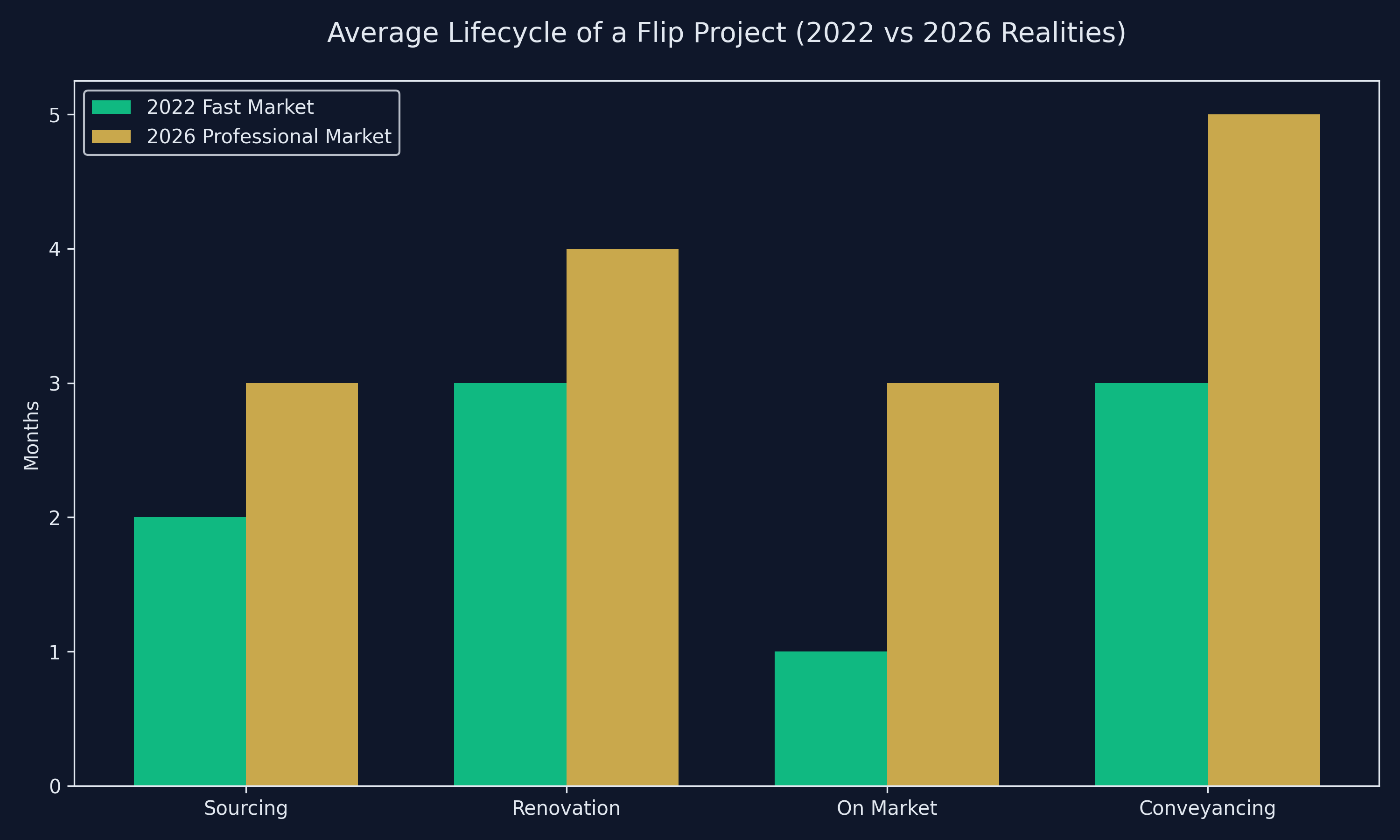

6. The Evolution of Time: Market Speed

In the "boom" years around the turn of the decade, property selling speed meant you could list a house on Monday, conduct a bidding war on Wednesday, and have an unconditional cash buyer by Friday.

The 2026 market lifecycle requires extreme patience. As mentioned, the time between finding a buyer and exchanging contracts has extended significantly due to mortgage lender caution, rigorous solicitor checks regarding new legislation (like the Building Safety Act implications), and a general sluggishness in the civil service local searches. If your financial model assumes you will have your cash out of the deal within 120 days of purchase, your model will fail. You must aggressively bake a 6 to 8-month timeline into your finance applications, drastically changing the ROI mathematics.

[PLACEHOLDER_GRAPHIC_8]

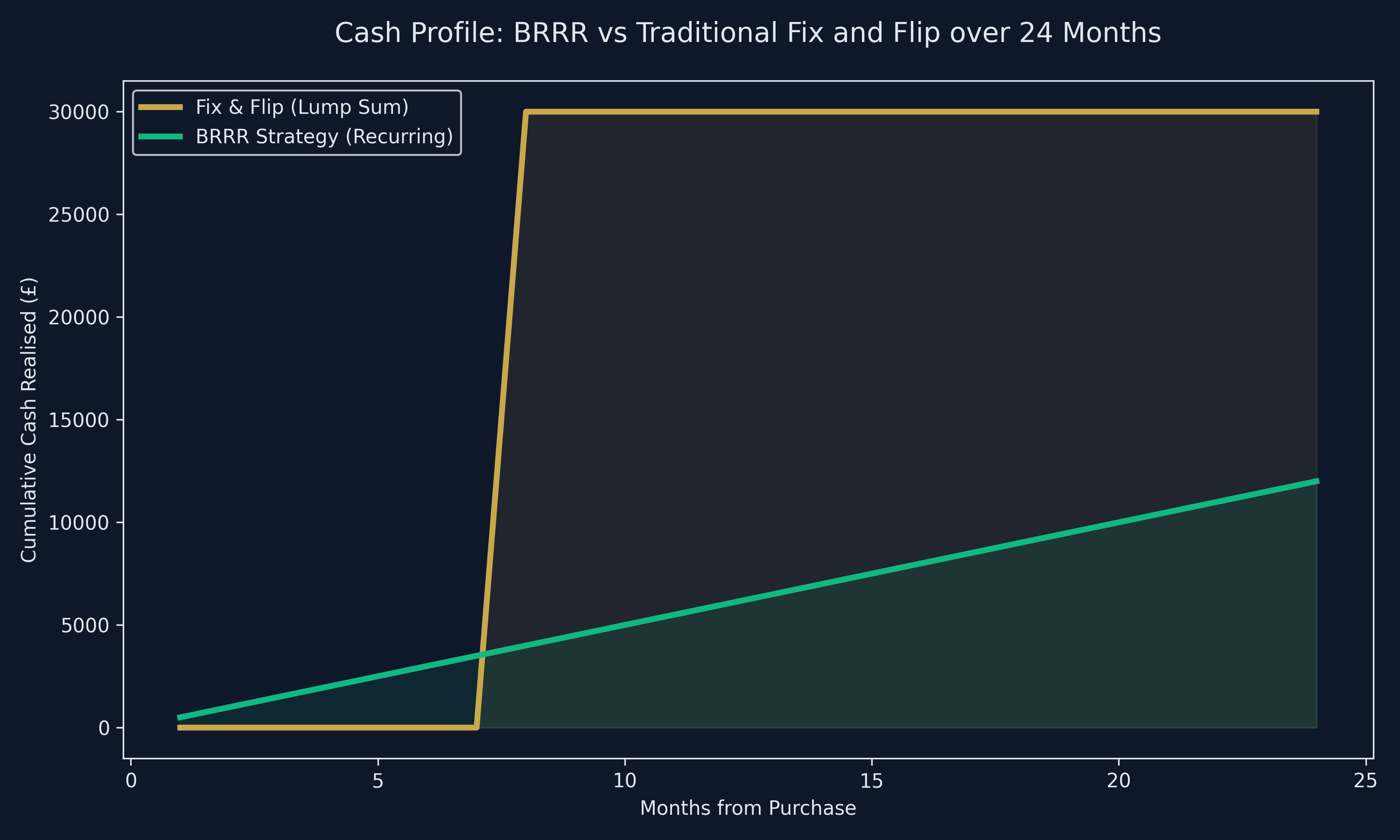

7. Strategic Alternatives: BRRR vs Fix and Flip

Given the execution risk and tight margins, countless former fix-and-flippers have transitioned to buy-and-hold strategies, specifically the BRRR (Buy, Refurbish, Refinance, Rent) model. Understanding the dichotomy between BRRR vs Fix and Flip UK is essential for deciding if flipping aligns with your goals.

Fix and Flip provides an active, lump-sum payout. It generates capital, not passive cash flow. You work intensely for six months, you pay your taxes, and you hopefully walk away with £25,000 in your pocket. But then you are back to square one, completely unemployed until you find your next deal. It is an active job, subject to heavy taxation, that happens to involve bricks and mortar.

The BRRR Strategy uses the exact same initial skill set: you find a rundown property, you buy it under market value, and you renovate it. However, instead of selling it to realize the gain, you refinance the property based on its newly elevated After Repair Value. By refinancing at the new ARV, you pull out your initial capital (and your renovation costs) to recycle into the next deal, while you retain the asset. The property is then rented out, providing monthly passive income and exposing you to long-term capital appreciation. While you don't get the £25,000 lump sum, you build a resilient, inflation-protected portfolio that spins off cash continuously.

[PLACEHOLDER_GRAPHIC_10]

The Verdict: Is It Worth It?

Is fix and flip property worth it? Yes. But only for a specific type of investor.

If you are a casual observer looking to make a quick buck by painting over some cracks and putting down laminate flooring on weekends, the current market structure—with its savage holding costs and tight lending constraints—will eat you alive. The margins of error are simply too thin.

However, if you operate as a data-led professional, treat your property flipping as a registered, systematic business, and have deep localized networks in the North or Midlands where entry points are viable, it remains one of the most powerful mechanisms for generating large tranches of capital. Success belongs to those who underwrite their deals with brutal conservatism, prioritizing aggressive completion timelines and energy-efficient, buyer-centric renovations over mere cosmetic glamour.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →