For decades, the standard blueprint for generating wealth in the UK was remarkably simple: save a deposit, take out an interest-only mortgage, buy a two-bedroom terrace, and let inflation and renters do the heavy lifting. The traditional Buy-to-Let (BTL) model forged a generation of millionaires.

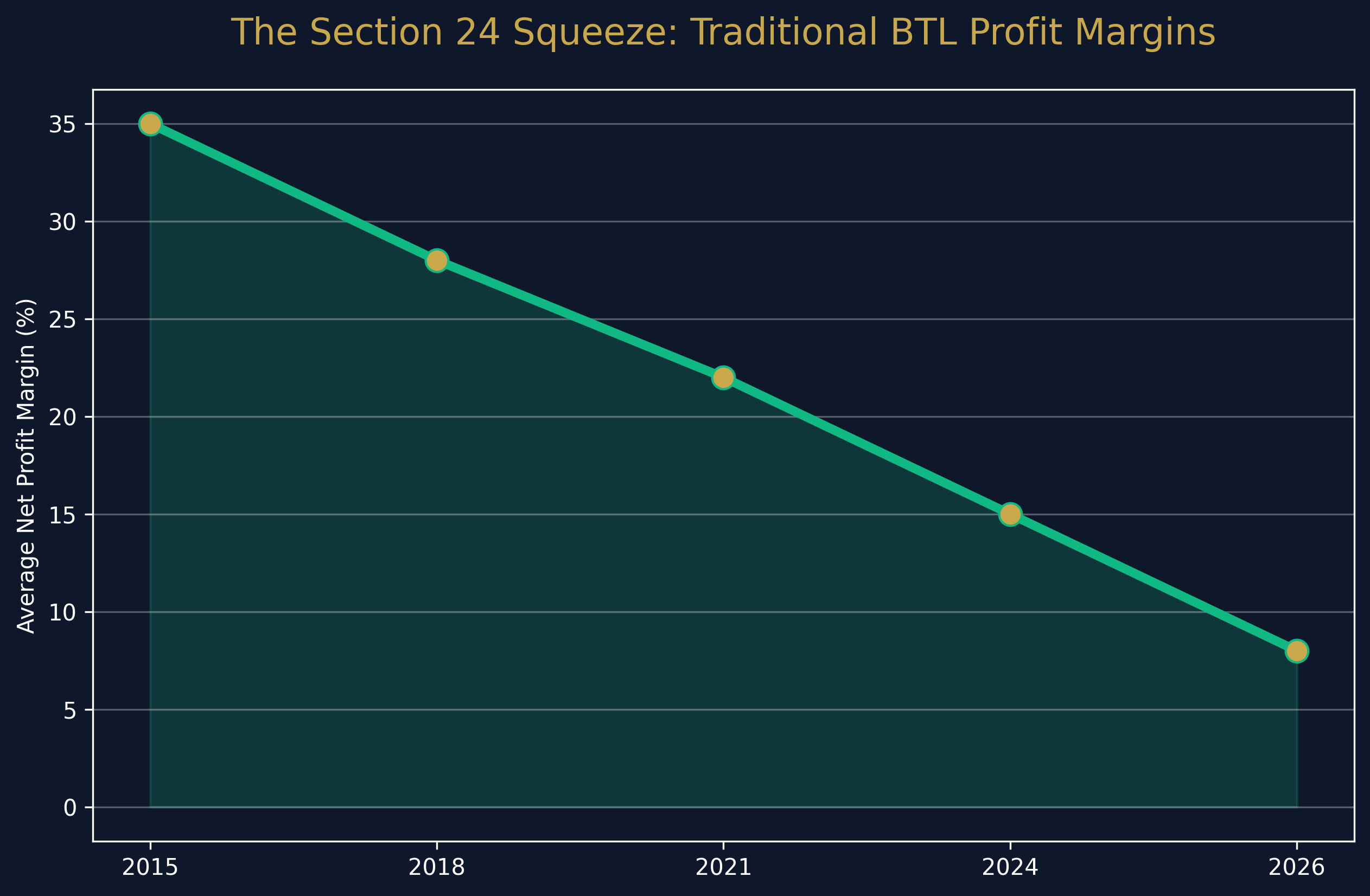

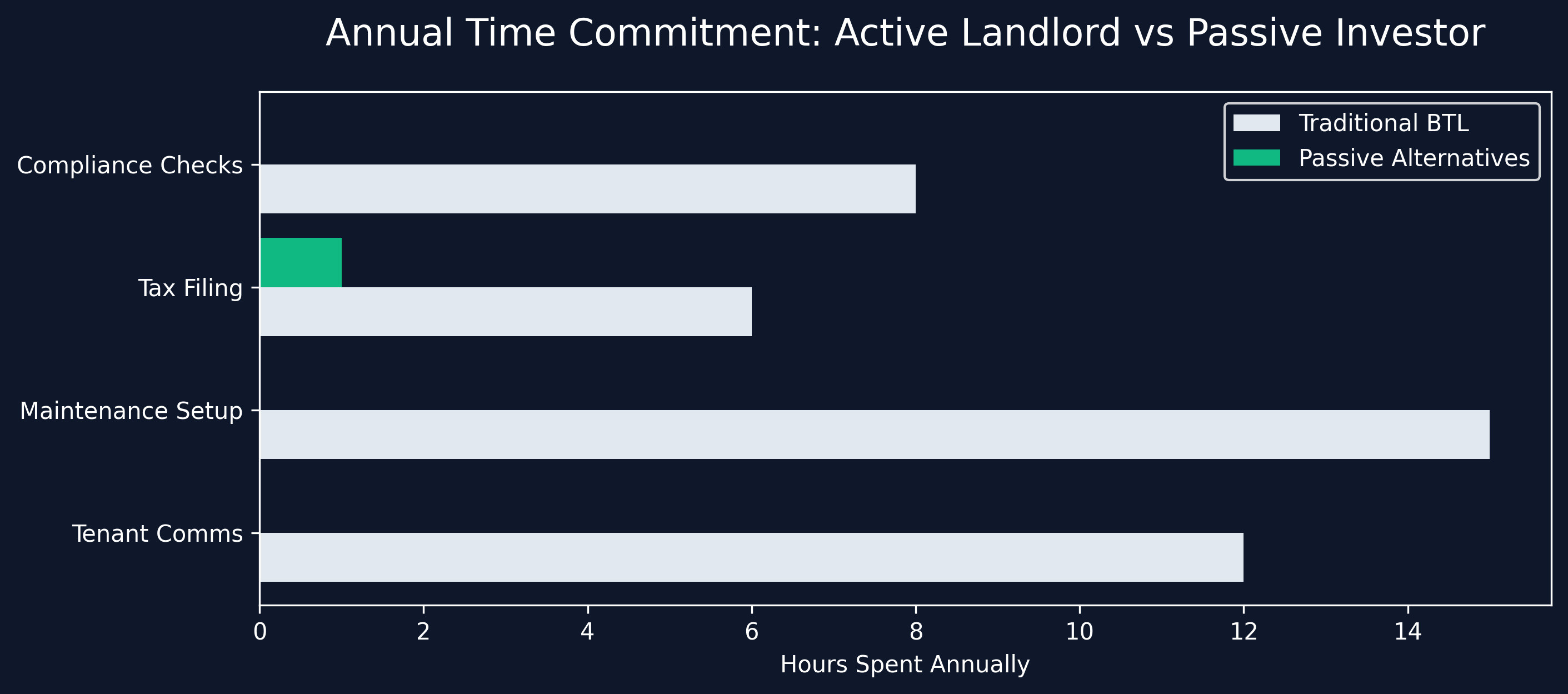

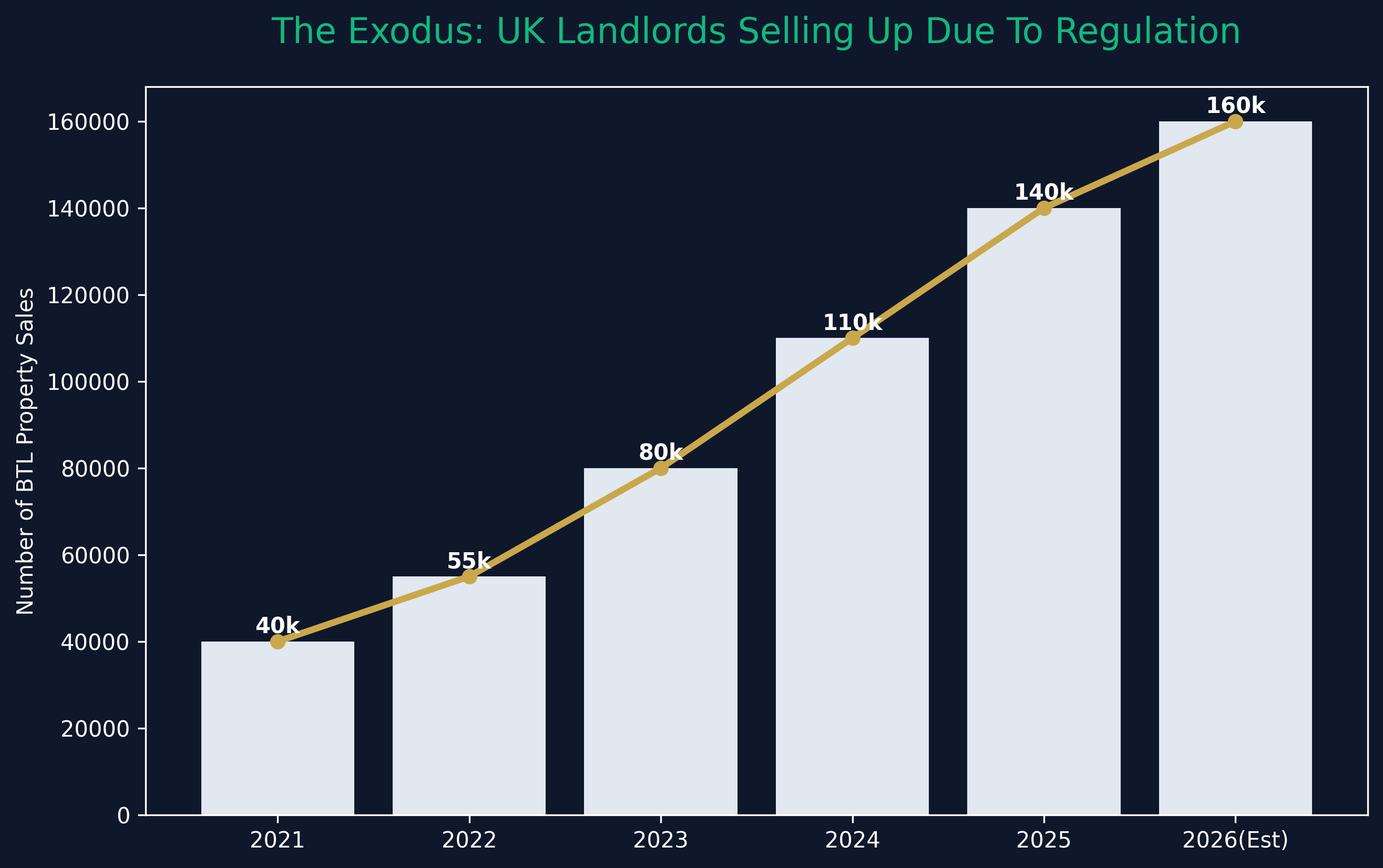

But as we navigate 2026, that blueprint is severely fractured. Between the punitive Section 24 mortgage interest relief restrictions, the impending enforcement of the Renters' Rights Bill (abolishing Section 21 "no-fault" evictions from May 2026), and strict new EPC rating mandates, the individual landlord model is facing an unprecedented structural reset.

Consequently, smart money is rotating. Investors are increasingly seeking a viable alternative to buy to let—strategies that offer exposure to the resilient UK property market without the crushing tax burden and intensive tenant management.

If you are tired of midnight boiler breakdowns and shrinking profit margins, this comprehensive guide ranks every major alternative investment to buy to let available today, from hands-off REITs to fixed-return property bonds.

Why the Stampede Toward Buy to Let Alternatives?

Before exploring the solutions, we must understand the catalyst driving the mass exodus toward buy to let alternatives.

- The Taxation Squeeze: Section 24 has neutralized the ability of higher-rate taxpayers to deduct mortgage interest from their rental income before calculating tax. Many individual landlords now find themselves taxed on their turnover rather than their profit, pushing some into negative cash flow.

- Regulatory Strangulation: The Renters' Rights Bill fundamentally alters the power dynamic between landlord and tenant. The inability to seamlessly regain possession of an asset via Section 21 has drastically increased the risk profile of single-family lets.

- Capital Expenditure: Upgrading older housing stock to meet the new, stringent Energy Performance Certificate (EPC) 'C' ratings is costing landlords tens of thousands of pounds in retrofitting.

For investors who hold property in personal names, the math simply no longer works. This has sparked immense interest in strategies that allow for property investment without mortgage reliance and personal tax exposure.

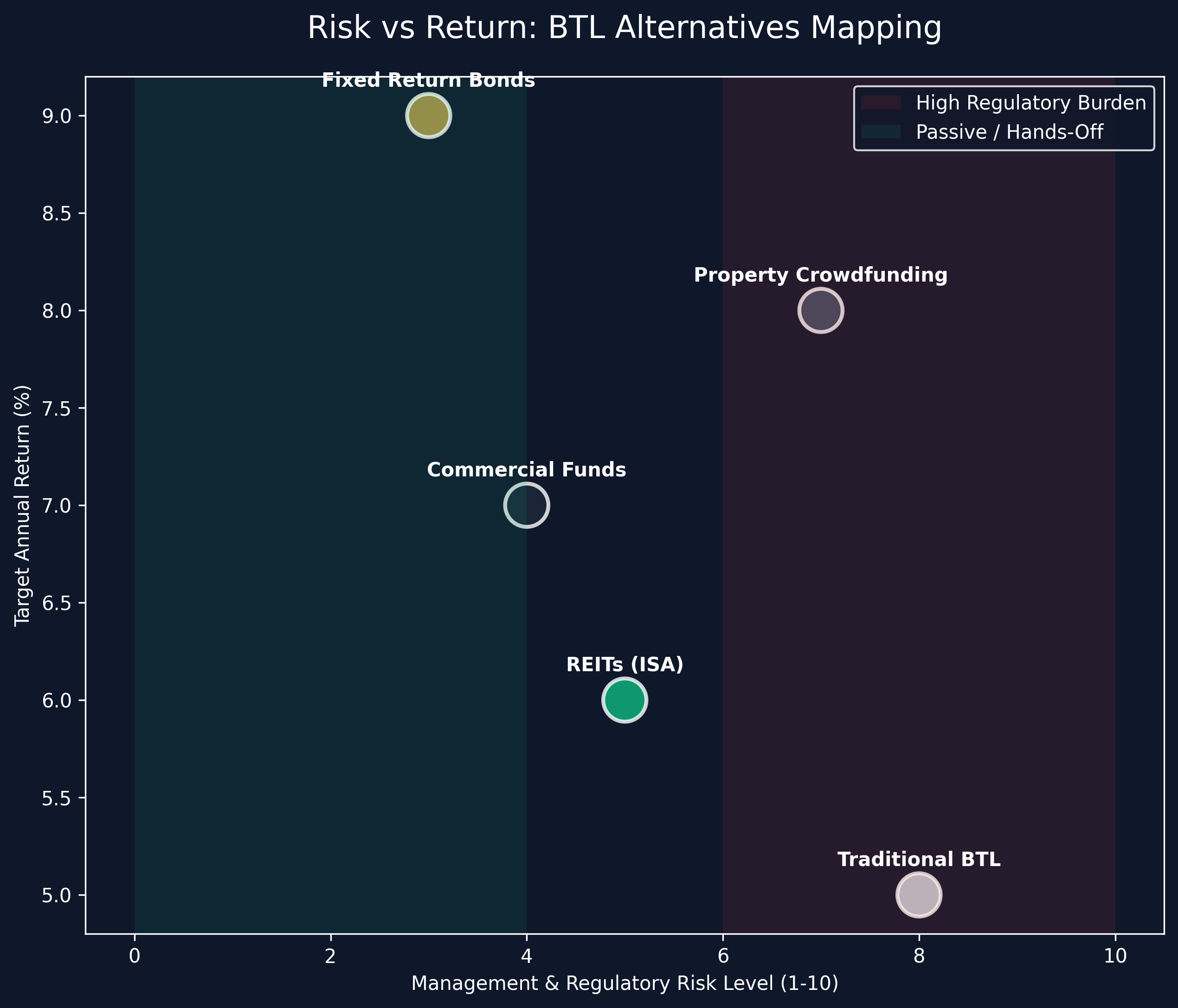

Alternative 1: Real Estate Investment Trusts (REITs)

If your primary goal is absolute passivity and high liquidity, Real Estate Investment Trusts (REITs) are the foremost alternative to buy to let.

A REIT is a company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs pool the capital of numerous investors. This makes it possible for individual investors to earn dividends from real estate investments without having to buy, manage, or finance any properties themselves.

The Mechanics

You buy shares in a REIT on major public stock exchanges (like the LSE). By law, UK REITs must distribute at least 90% of their tax-exempt property rental business income to shareholders as dividends.

Pros & Cons

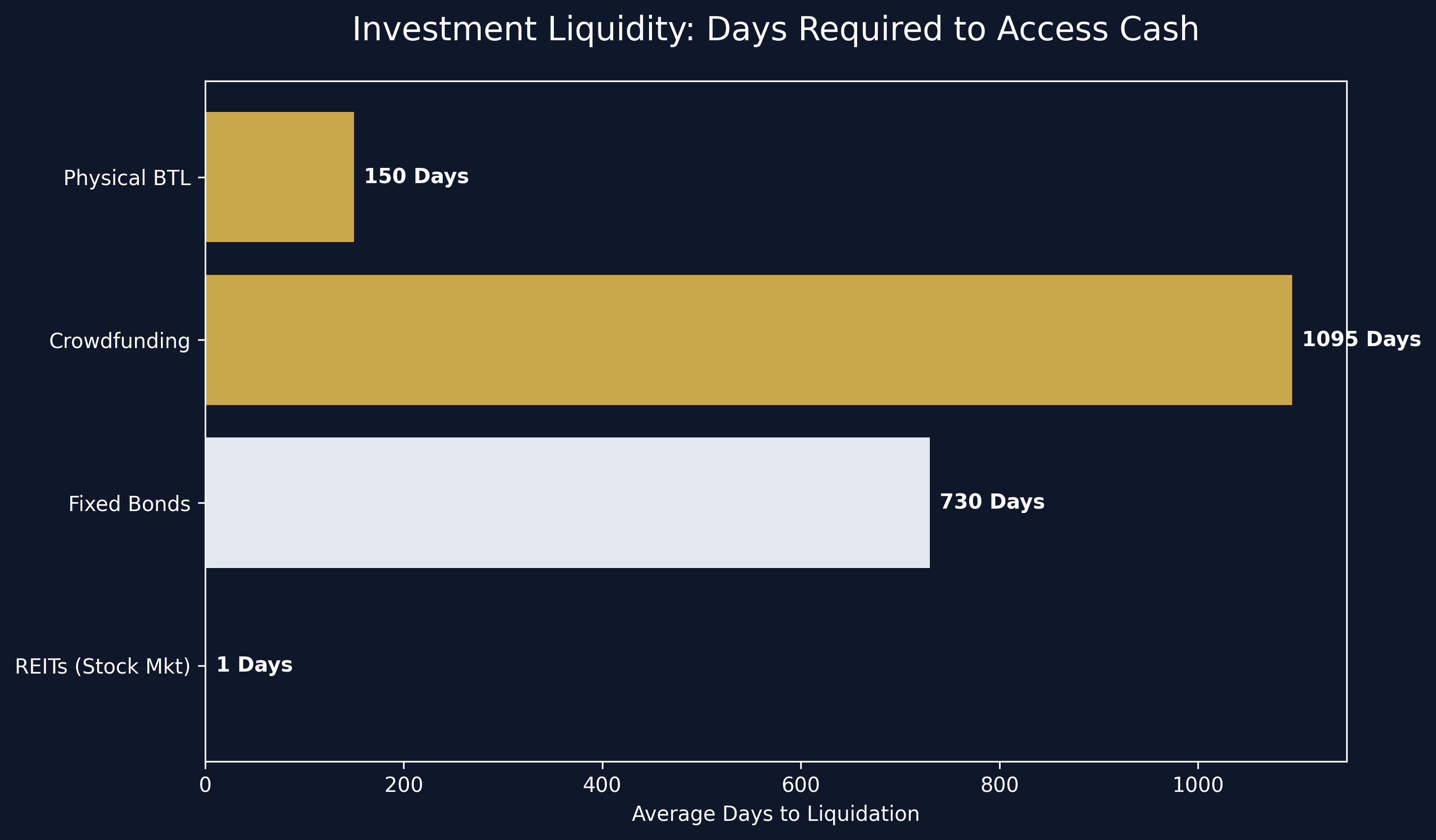

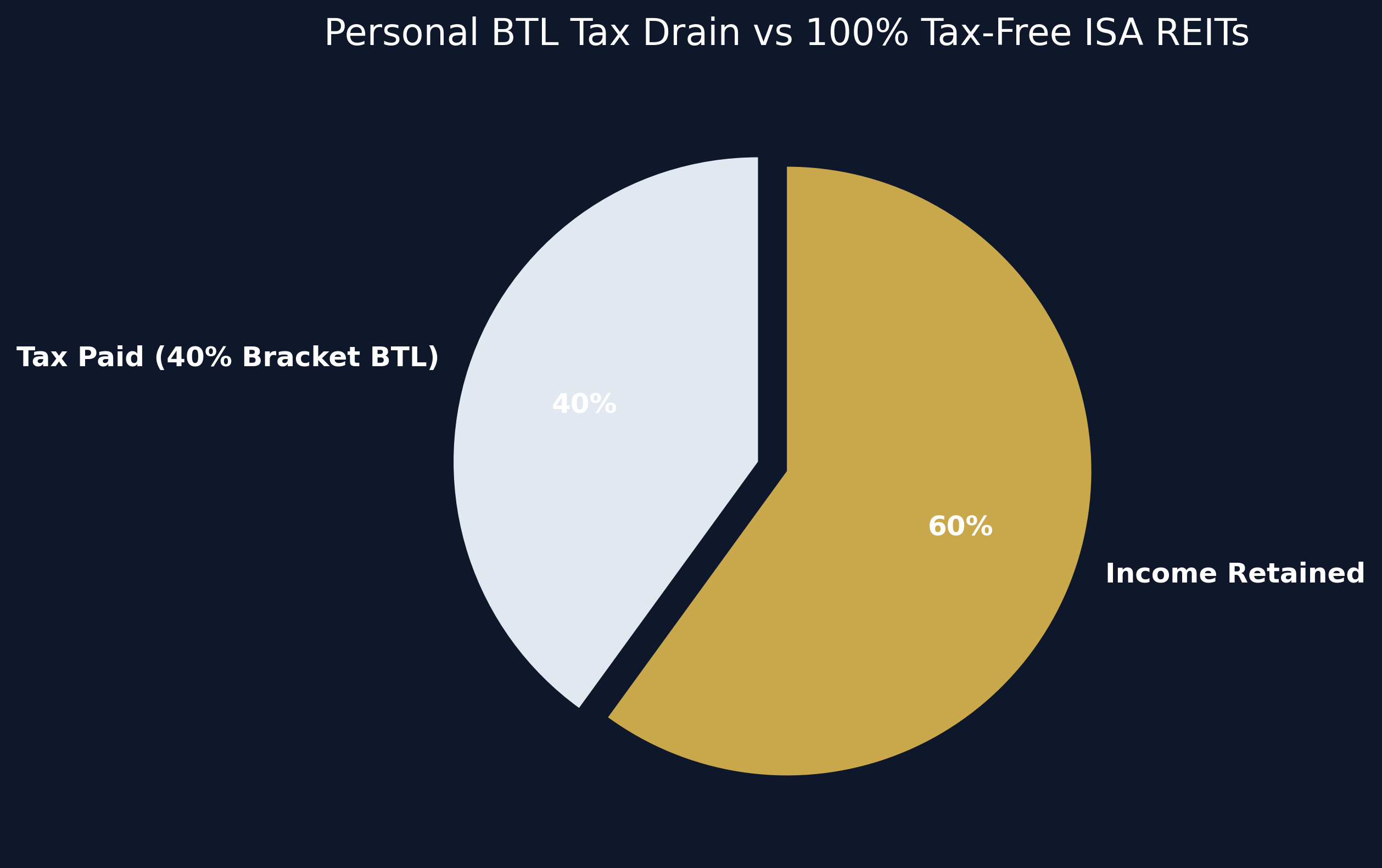

- Pros: Total hands-off investment. Incredible liquidity (you can sell shares in seconds). Can be held inside a Stocks & Shares ISA, rendering your dividends and capital growth completely tax-free.

- Cons: Returns are linked to the broader stock market, meaning you lose the insulation from market volatility that physical bricks-and-mortar usually provide. You also cannot leverage your investment with a mortgage.

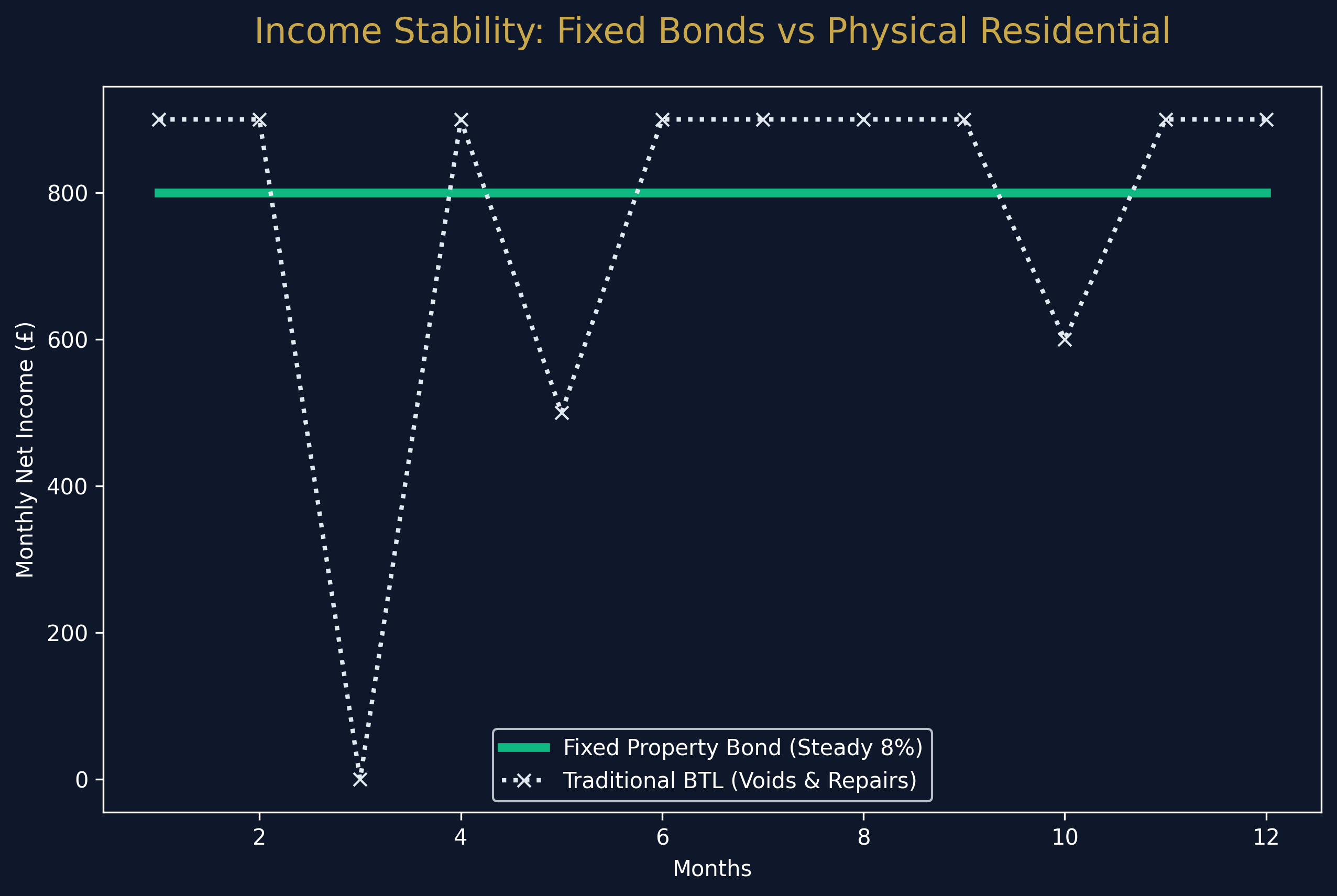

Alternative 2: Fixed-Return Property Bonds (Loan Notes)

For investors seeking predictability over the erratic nature of the open housing market, property bonds (or loan notes) have become a dominant alternative investment to buy to let in 2026.

Instead of buying a house, you effectively act as the bank. You lend your capital to an established property developer or sourcing company. In exchange for utilizing your capital to build or acquire assets, they contractually guarantee you a fixed interest rate (typically between 8% and 12% per annum) over a set term (usually 1 to 5 years).

Safety and Security

Because you are lending money to a corporate entity, your capital is usually secured by a first or second legal charge against the physical asset, providing a robust layer of protection. This is an excellent way to achieve a property investment without mortgage complications, entirely bypassing the volatile UK residential market.

Alternative 3: Property Crowdfunding

Crowdfunding platforms allow you to invest small amounts of capital (sometimes as little as £100) alongside hundreds of other investors to purchase a specific property or fund a development.

The platform handles everything from the acquisition and tenant management to the eventual sale. You receive a proportionate share of the monthly rental income and a share of the capital uplift when the asset is sold.

Pros & Cons

- Pros: Extremely low barrier to entry. Allows for rapid diversification across different regions and property types (e.g., investing £1,000 across ten different properties rather than £10,000 in one).

- Cons: Highly illiquid. You cannot easily pull your money out until the investment term ends or the property is sold. Fees charged by the platform can significantly eat into your net yield.

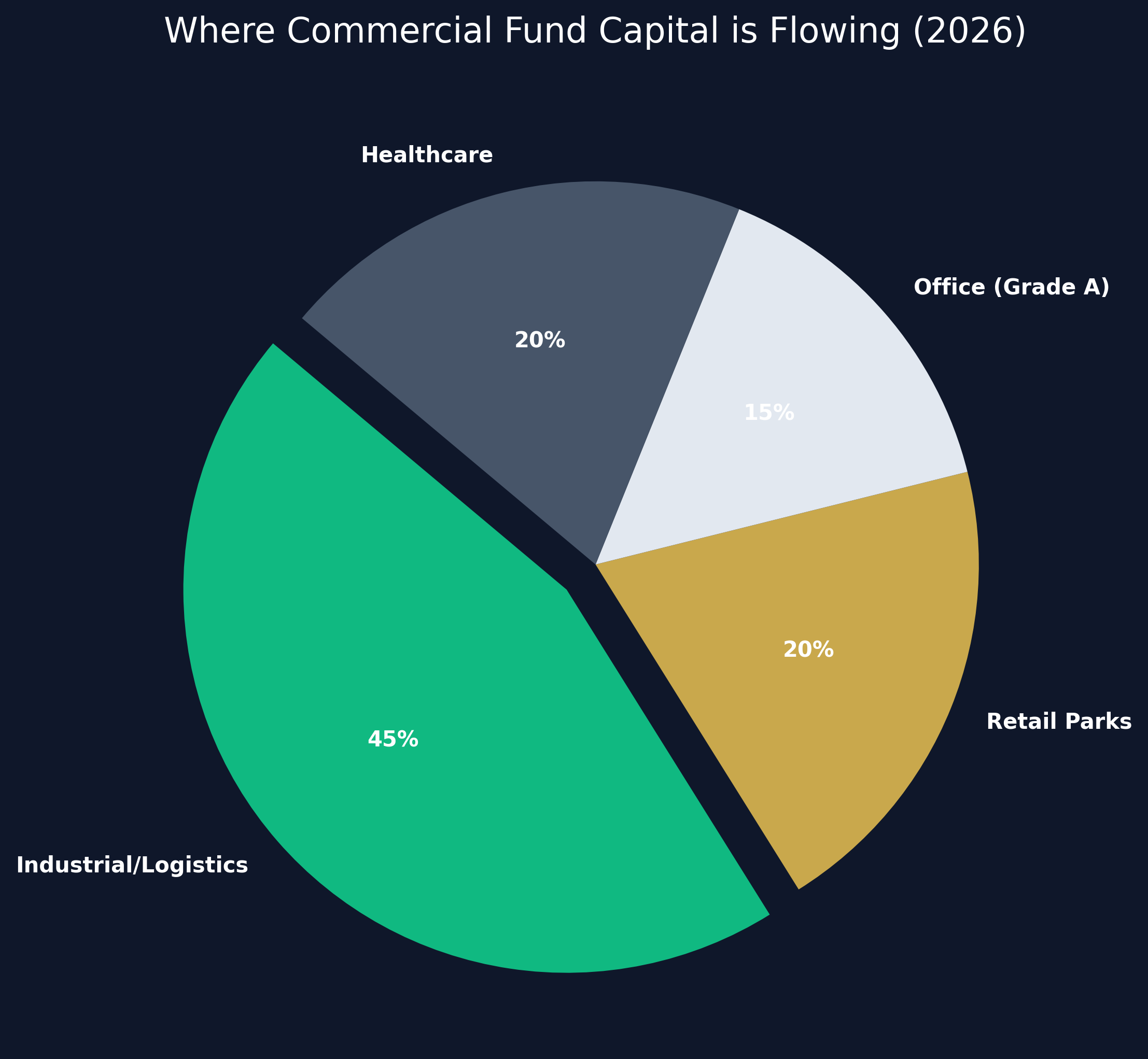

Alternative 4: Commercial Property Funds

Unlike residential BTL, commercial property (warehouses, office blocks, healthcare facilities, and retail units) generally offers longer lease terms (5 to 10+ years), upward-only rent reviews, and Fully Repairing and Insuring (FRI) leases where the tenant pays for the building's maintenance and insurance.

Unless you have millions in liquid capital, buying a logistics hub outright is impossible. Commercial Property Funds allow you to buy units in a massive portfolio managed by institutional fund managers. This grants you access to asset classes that are fundamentally insulated from the regulatory burdens crushing residential landlords.

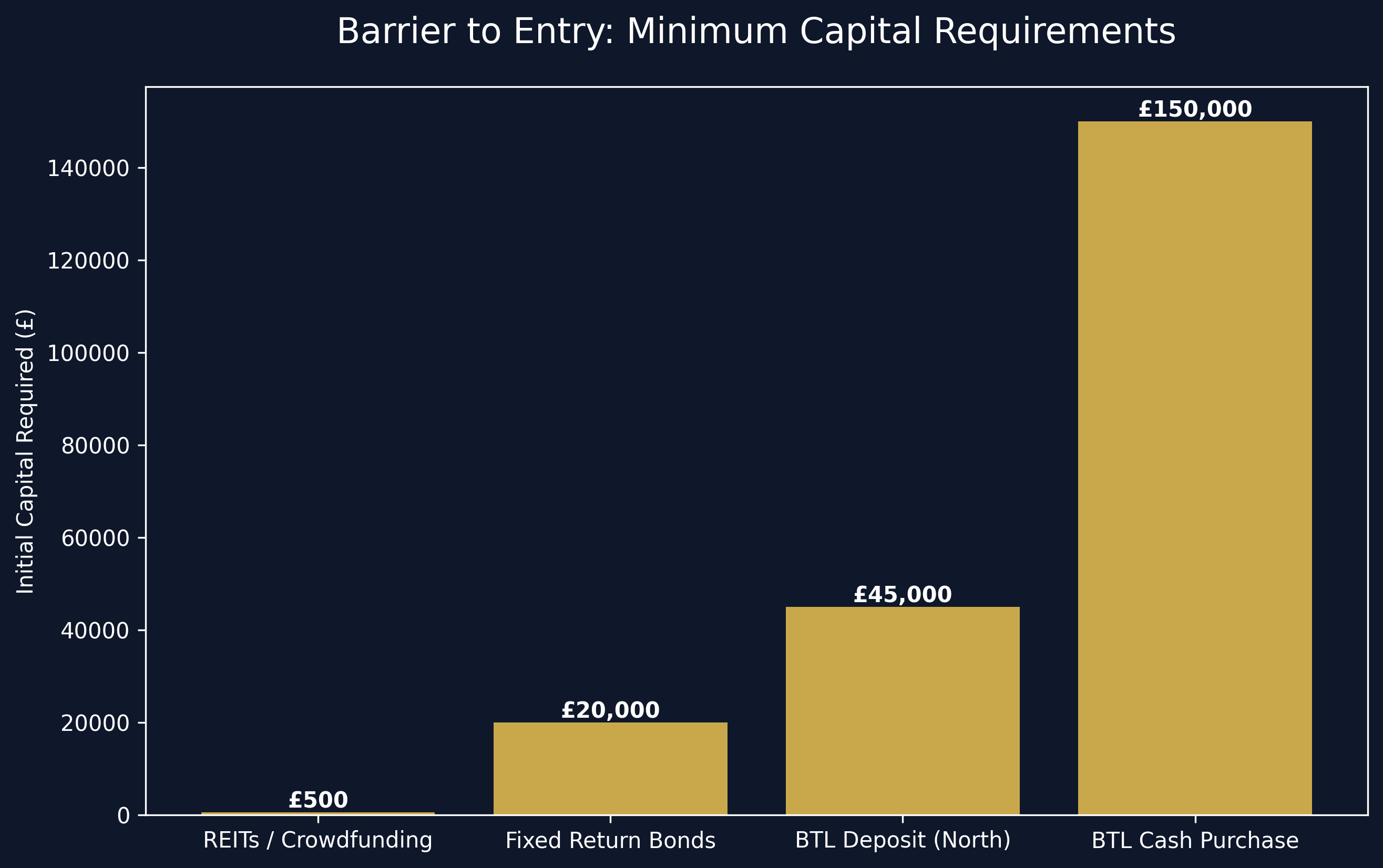

Exploring the Cash Market: Buy to Let Without Mortgage

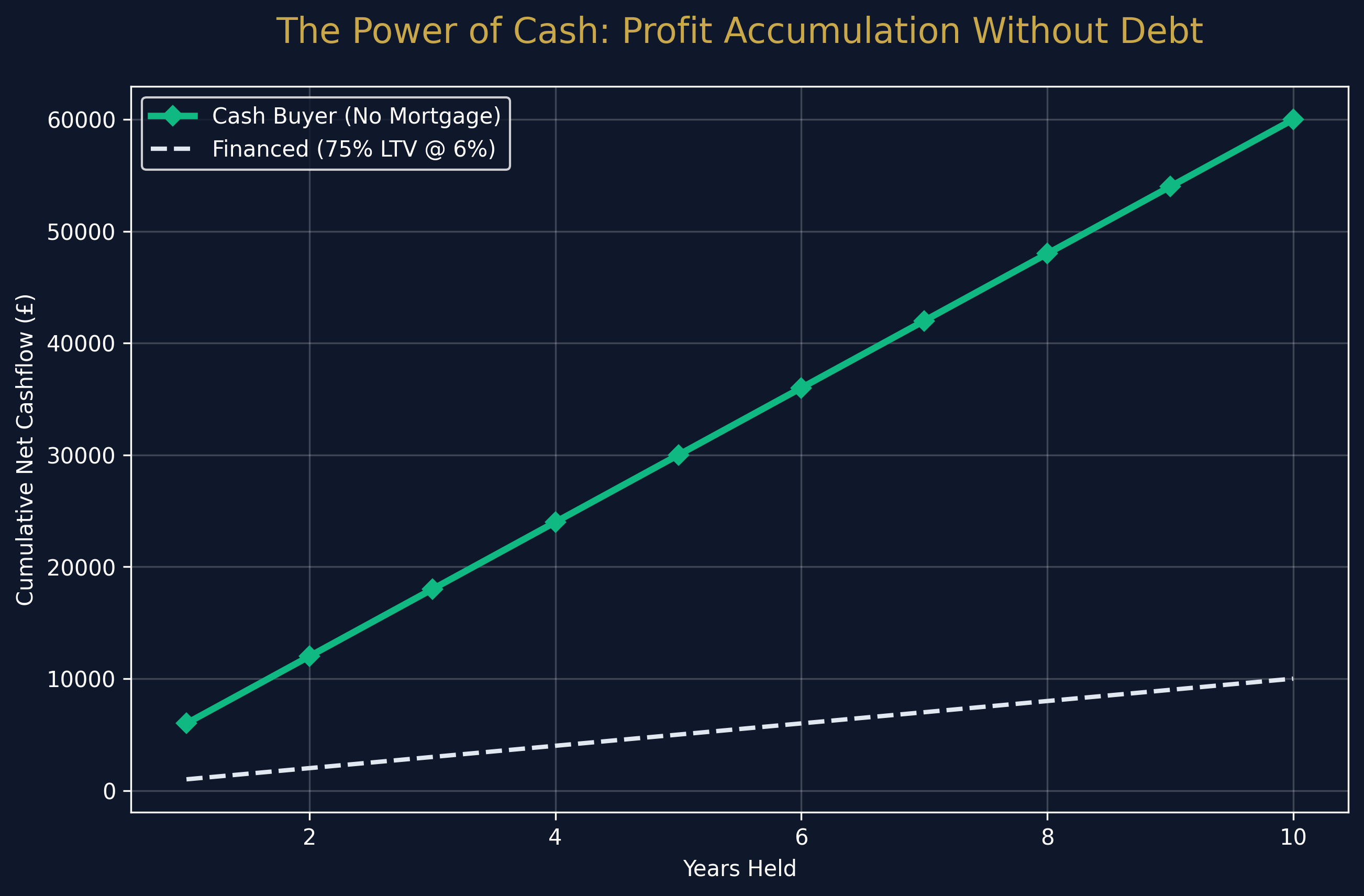

What if you still want to own physical, residential property, but you want to escape the high-interest rates and Section 24 taxes? The answer is executing a buy to let without mortgage.

If you have sufficient capital to buy the property outright—a buy to let no mortgage strategy—you instantly eliminate your largest monthly expense (interest payments) and entirely sidestep the Section 24 tax trap, as you have no finance costs being disallowed.

Why Buy in Cash?

Buying in cash allows you to negotiate aggressively, as sellers favor the speed and certainty of a cash buyer. A buy to let no mortgage strategy generates exceptional, stable monthly cash flow. If a £150,000 property rents for £900 a month, and you have no £500 mortgage payment eating into it, your net monthly income is formidable.

Buy to Let vs Normal Mortgage

A persistent point of confusion for new investors is the distinction of a buy to let vs normal mortgage. You absolutely cannot use a standard residential mortgage (which you use for your own home) to rent a property out. Doing so constitutes mortgage fraud.

BTL mortgages require much larger deposits (usually 25% minimum), carry higher interest rates, and are stress-tested based on the property's anticipated rental income rather than your personal salary. Because these specialized mortgages have become so expensive in 2026, many investors are choosing to either buy in cash or abandon physical property altogether for the alternatives listed above.

Conclusion: Evolving Beyond the Traditional Model

The era of the "amateur landlord" is over. As we plunge deeper into 2026, navigating the UK property market requires professionalization and strategic agility.

If you are exhausted by hostile regulations and shrinking margins, executing an alternative to buy to let is the most prudent financial pivot you can make. Whether you lean into the tax-free liquidity of a REIT held in an ISA, the absolute predictability of a fixed-return property bond, or the robust cash flow of a buy to let no mortgage cash purchase, there are myriad ways to capture the underlying strength of UK real estate without enduring the traditional landlord headaches.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →