Here's the thing: there are countless ways to park your money and beat inflation without losing sleep at night. The massive factor I discovered? I just needed to wait long enough to be right. While everyone has their own appetite for risk and liquidity, I found that patience usually leads to profitable returns.

Today I'm sharing my playbook for safe investments that have helped me preserve capital while still growing my wealth. Think of these as financial cheat codes for conservative investors who want stable returns without the roller coaster ride.

What Are Low-Risk Investments and Why They Matter

Low-risk investments are exactly what they sound like - financial vehicles designed for capital preservation with minimal chance of losing your principal. These safe investments prioritize protecting your money over chasing massive returns.

The suits on Wall Street might tell you that risk equals reward, but here's my take: sometimes boring is beautiful. When you've got a family to feed and bills to pay, keeping your money safe becomes priority number one.

These conservative portfolio options typically include government bonds, high-yield savings accounts, CDs, and blue-chip dividend stocks. They won't make you rich overnight, but they also won't leave you when the market crashes.

Think of low-risk investments as the financial equivalent of wearing a seatbelt. You might not need it most of the time, but when things go sideways, you'll be glad it's there.

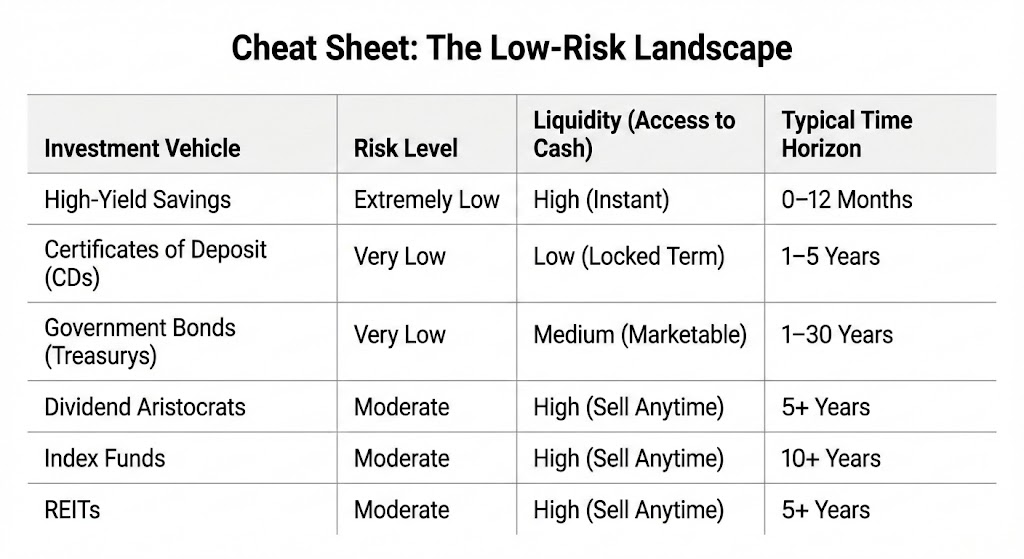

Types of Low-Risk Investments: Your Complete Arsenal

Not all safe investments are created equal. Here's your cheat sheet for the main categories that actually work:

Fixed-Income Securities: Government bonds, treasury securities, and investment-grade corporate bonds offer predictable returns. These are the workhorses of conservative investing.

Bank Products: High-yield savings accounts, CDs, and money market accounts provide FDIC insurance protection up to $250,000. Boring? Absolutely. Safe? You bet.

Dividend-Paying Stocks: Blue-chip companies with long dividend histories offer income plus potential growth. Think Coca-Cola, not some random crypto token.

Real Estate Investment Trusts (REITs): Professional-managed real estate without the headaches of being a landlord. I'll dive deeper into these later.

Index Funds: Diversified exposure to hundreds of stocks at once. Like buying a little piece of the entire economy instead of betting on individual companies.

The key is mixing and matching based on your timeline and comfort level. Diversification isn't just a fancy word - it's your insurance policy.

High-Yield Savings Accounts: The Foundation of Every Portfolio

Let's start with the most basic cheat code: high-yield savings accounts. These aren't your grandma's 0.01% savings accounts gathering dust at the local bank.

Today's best high-yield accounts offer 4-5% annual returns. That might not sound exciting, but it's guaranteed money with FDIC insurance. No market crashes, no sleepless nights, just steady growth.

Here's where I park my emergency fund and short-term money:

Online Banks: Marcus by Goldman Sachs, Ally Bank, and Capital One 360 consistently offer competitive rates. They can afford higher interest because they don't have physical branches.

Credit Unions: Often beat big banks on rates and fees. Worth checking if you qualify for membership.

The downside? Inflation can still eat into your purchasing power if rates don't keep up. But for money you need within 1-2 years, nothing beats the safety and liquidity.

My rule: Keep 6-12 months of expenses in high-yield savings. It's not glamorous, but it lets me sleep soundly knowing I'm covered if life throws a curveball.

Certificates of Deposit and Money Market Accounts: Locking in Returns

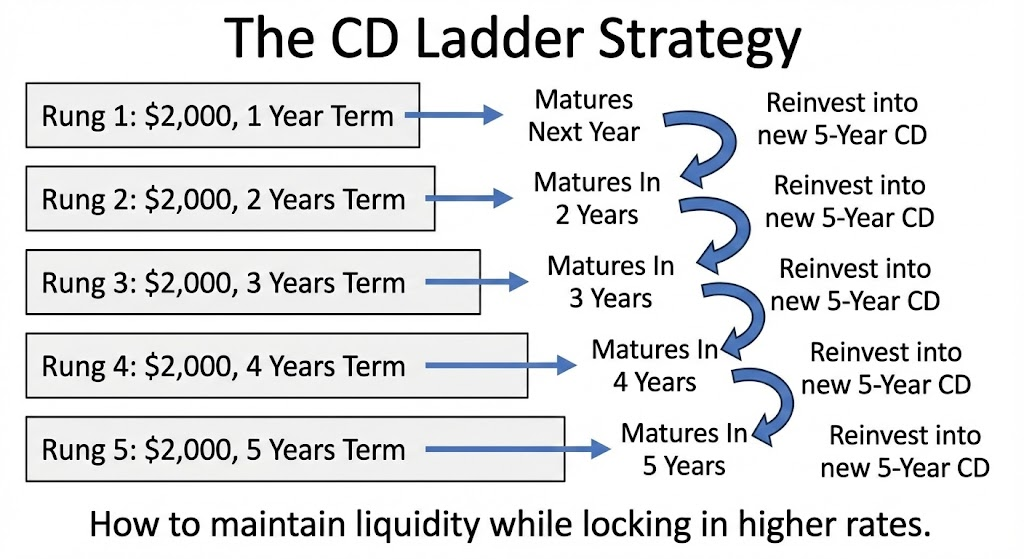

CDs are like making a deal with the bank: you promise not to touch your money for a specific period, and they promise a fixed return. It's a win-win for conservative investors.

Current CD rates range from 4-5% for terms between 6 months to 5 years. The longer you commit, the higher the rate typically goes.

CD Laddering Strategy: Instead of putting all your money in one CD, spread it across different maturity dates. This gives you regular access to funds while maximizing returns.

By the end of year 5, you have a CD maturing every single year, giving you access to cash annually while earning the higher long-term rates.

Money market accounts sit between savings and CDs. They offer higher rates than regular savings but may require minimum balances. Some even come with check-writing privileges.

The trade-off? Your money is locked up with CDs, and money markets might have transaction limits. But for stable returns and capital preservation, they're hard to beat.

I use CDs for money I won't need for 1-3 years, like a future house down payment or my kid's college fund starting money.

Government Bonds: Treasury Securities That Actually Pay

Government bonds are IOUs from Uncle Sam, and they're about as safe as investments get. The U.S. government has never defaulted on its debt, making treasury securities the gold standard for low-risk investing.

Treasury Bills (T-Bills): Short-term (4 weeks to 1 year) with lower yields but maximum liquidity.

Treasury Notes: Medium-term (2-10 years) offering higher yields than T-Bills.

Treasury Bonds: Long-term (20-30 years) with the highest yields but more interest rate sensitivity.

I Bonds: These inflation-protected securities adjust their returns based on the Consumer Price Index. Currently offering around 5%, they're like having an inflation cheat code.

You can buy treasury securities directly from the government at TreasuryDirect.gov, avoiding broker fees. The minimum investment is just $100, making them accessible to everyone.

The main risk? Interest rate changes can affect bond prices if you need to sell before maturity. But if you hold until maturity, you get your full principal back plus interest.

Blue-Chip Dividend Stocks: Income with Growth Potential

Here's where conservative investing gets interesting. Blue-chip dividend stocks offer the best of both worlds: steady income and potential capital appreciation.

These are companies that have been paying dividends for decades through good times and bad.

We're talking about household names like:

Johnson & Johnson: 60+ years of consecutive dividend increases

Coca-Cola: Over 50 years of dividend growth

The dividend aristocrats (S&P 500 companies with 25+ years of consecutive dividend increases) are particularly attractive for conservative portfolios.

My approach: Focus on companies with dividend yields between 2-4% and strong

fundamentals. Too high might signal trouble, too low might not provide enough income.

Dividend Reinvestment Plans (DRIPs): Many companies let you automatically reinvest dividends to buy more shares, often without fees. It's compound interest on autopilot.

The risk? Stock prices can still fluctuate, and dividends can be cut during tough times. But quality dividend stocks have historically been more stable than growth stocks.

Index Funds: The Ultimate Diversification Cheat Code

Index funds are my secret weapon for long-term wealth building. Instead of trying to pick winning stocks, you buy a tiny piece of hundreds or thousands of companies at once.

The S&P 500 index fund I mentioned earlier tracks America's 500 largest companies. When Apple represents 7% of the index, 7% of your investment goes to Apple stock. It's like owning a slice of the entire U.S. economy.

Total Stock Market Index Funds: Even broader diversification across small, medium, and large companies.

International Index Funds: Exposure to global markets beyond the U.S.

Bond Index Funds: Diversification across thousands of bonds instead of picking individual issues.

The beauty of index funds? They're self-cleansing. Companies get added and removed automatically based on market performance. You never have to worry about individual company failures.

Expense ratios are incredibly low - often 0.03-0.20% annually. That means more of your returns stay in your pocket instead of going to fund managers.

Real Estate Investment Trusts: Professional Property Management

REITs let you invest in real estate without becoming a landlord. These companies own income-producing properties like office buildings, apartments, shopping centers, and hospitals.

By law, REITs must distribute at least 90% of their taxable income as dividends to shareholders.

This makes them attractive for income-focused investors seeking stable returns.

Equity REITs: Own and operate real estate properties

Mortgage REITs: Provide financing for real estate purchases

Hybrid REITs: Combination of both strategies

REITs trade on stock exchanges like individual stocks, providing liquidity that physical real estate lacks. You can buy and sell shares instantly during market hours.

The downside? REITs are sensitive to interest rate changes and economic cycles. When rates rise, REIT prices often fall as investors chase higher yields elsewhere.

I allocate about 10-15% of my conservative portfolio to REITs for diversification and income generation. They've provided steady dividends even when my rental properties had vacancy issues.

Risk vs Return: Finding Your Sweet Spot

Here's the reality nobody talks about: there's no such thing as a completely risk-free investment. Even "safe" options carry some risk.

High-Yield Savings: Risk of inflation outpacing returns

CDs: Risk of missing out on higher rates if interest rates rise

Government Bonds: Risk of interest rate changes affecting prices

Dividend Stocks: Risk of stock price volatility and dividend cuts

REITs: Risk of real estate market downturns

The key is understanding these risks and building a portfolio that matches your timeline and comfort level.

My framework: Use the "sleep test." If an investment keeps you awake at night worrying, it's too risky for you regardless of potential returns.

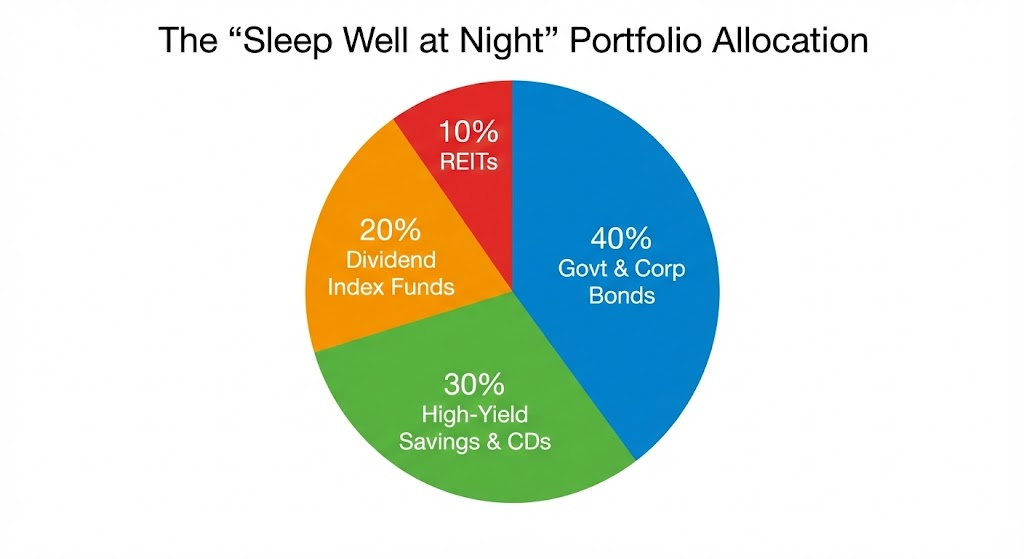

🥧 Chart: The "Sleep Well at Night" Portfolio

My personal conservative allocation example:

This provides stability, income, and modest growth potential while preserving capital.

How to Choose the Right Low-Risk Investment Option

Picking the right safe investments depends on three key factors: timeline, goals, and risk tolerance.

Timeline Questions:

Goal-Based Approach:

Risk Tolerance Reality Check:

Start conservative and gradually increase risk as you gain experience and confidence. There's no shame in prioritizing capital preservation over maximum returns.

My cheat code: Automate everything. Set up automatic transfers to different accounts based on your allocation. This removes emotion from the equation and ensures consistent investing.

Tax Implications: Keeping More of Your Returns

The suits forget to mention that taxes can eat into your investment returns. Here's what you need to know about the tax treatment of low-risk investments:

Taxable Accounts:

Tax-Advantaged Accounts:

Maximize contributions to 401(k)s, IRAs, and other retirement accounts first. These provide immediate tax benefits or tax-free growth.

Municipal Bonds: Interest is often tax-free at federal and sometimes state levels. Particularly attractive for high-income investors.

The takeaway? Consider the after-tax returns, not just the headline rates. A 4% tax-free municipal bond might beat a 5% taxable corporate bond depending on your tax bracket.

Inflation Protection: Your Money's Purchasing Power

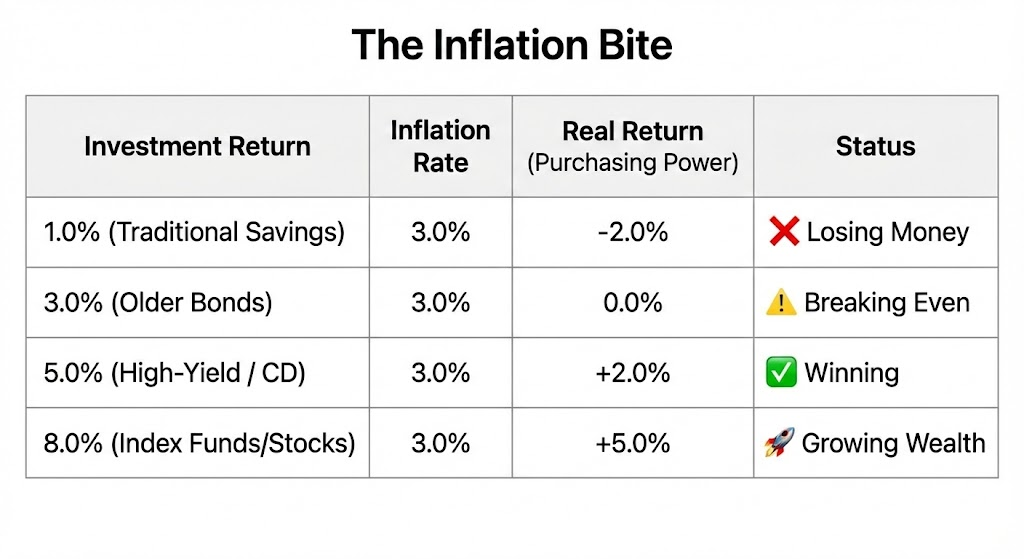

Here's the dirty secret about "safe" investments: inflation can silently erode your wealth even when your account balance grows.

If your money earns 3% annually but inflation runs at 4%, you're actually losing 1% of purchasing power each year. Your dollars buy less stuff despite having more of them.

Inflation-Protected Strategies:

I Bonds: Adjust returns based on inflation rates, providing direct protection.

TIPS (Treasury Inflation-Protected Securities): Principal adjusts upward with inflation, maintaining purchasing power.

Real Assets: REITs and dividend growth stocks often increase payouts during inflationary periods.

Short-Term Bonds: Ability to reinvest at higher rates as interest rates rise with inflation.

My approach: Keep some inflation protection in every portfolio, even conservative ones. It's insurance against the silent wealth killer.

Building Your Low-Risk Investment Portfolio

Here's my step-by-step cheat code for building a conservative portfolio that actually works:

Step 1: Emergency fund first. 6-12 months of expenses in high-yield savings. Non-negotiable.

Step 2: Max out any employer 401(k) match. It's free money with guaranteed returns.

Step 3: Determine your timeline for different financial goals.

Step 4: Allocate based on when you need the money:

Step 5: Automate everything. Set up automatic transfers and reinvestment.

Step 6: Review and rebalance annually, not daily. Frequent checking leads to emotional decisions.

Start small if you're nervous. Even $100 monthly into a diversified portfolio builds wealth over time through compound growth.

Your Path to Financial Security Through Low-Risk Investments

After four days in the hospital becoming a father, I realized something important: protecting your family's financial future doesn't require risky bets or market timing genius. Sometimes the boring approach wins.

Low-risk investments like high-yield savings accounts, government bonds, dividend stocks, and REITs provide the foundation for long-term wealth building. They might not make you rich overnight, but they won't keep you awake worrying about market crashes either.

The key is starting now, automating your approach, and staying consistent. Whether you choose treasury securities for maximum safety or dividend-focused index funds for growth potential, the most important step is taking action.

Remember: this isn't financial advice, just information that I found useful and hope serves you well. Please seek professional advice and make decisions based on your own financial situation.

Your future self will thank you for prioritizing capital preservation and stable returns over get-rich-quick schemes. Sometimes the best cheat code is patience combined with smart, conservative investing.

📚 Related Reading

- Buy dirt

- How I save nearly £2,000 a Year on Groceries for a Family of 4

- How to Improve Company Cash Flow: 4 Proven Ways

- Hobbies That Make Money: Real "Cheat Codes" for Turning Your Passion Into Profit

- How Environment Affects Business Success

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →