In the world of wealth creation, real estate remains one of the most reliable vehicles available. However, entering the market blindly, without a precise understanding of the numbers, is a guaranteed path to poor performance. If you are assessing property investment returns uk in 2026, you cannot rely on outdated assumptions from a decade ago.

Between fluctuating bank base rates, shifting regional affordability, and evolving tax structures, measuring your true return on investment for property requires precision. Whether you are aiming for a solid 6% or chasing elusive 12 property returns uk (12% yields), this comprehensive guide decodes the mathematics of property investing.

We will explore exactly what is yield in property, how to calculate your true ROI, and where to find the best property investment returns uk in the current market cycle.

The Foundation: Understanding Yield

Before you sign a mortgage or transfer a deposit, you must master the terminology. The most common metric thrown around by agents and investors alike is "yield." But what does yield mean in property exactly?

Property Investment Yields Explained

At its most basic level, yield in property investment is a measurement of the annual income generated by an asset, expressed as a percentage of its value. It tells you how hard your money is working on a month-to-month basis, independent of whether the house price is going up or down.

When someone asks, "what does rental yield mean?", they are usually asking for the Gross Yield calculation:

- Gross Yield = (Annual Rental Income ÷ Property Price) x 100

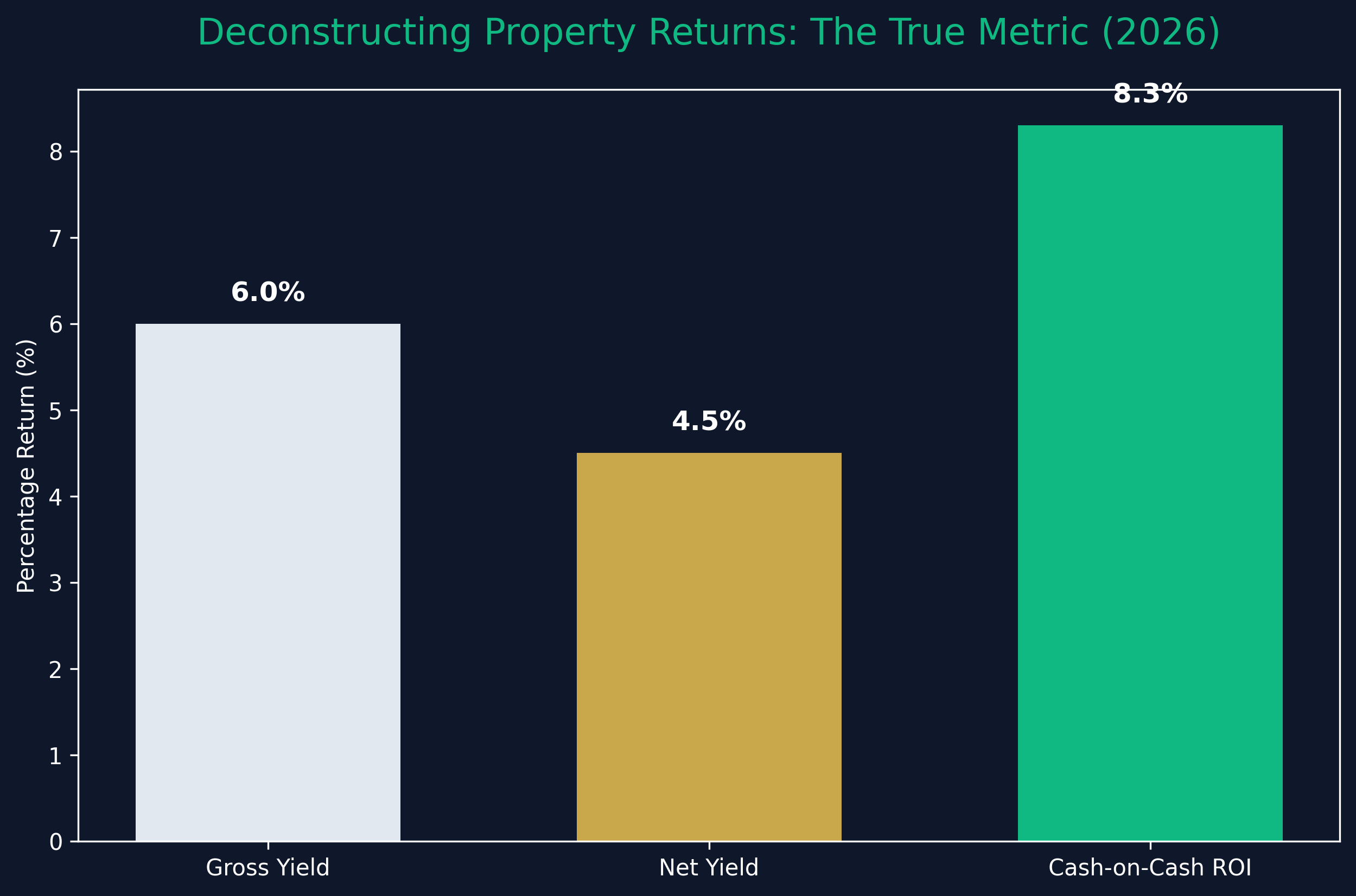

For example, if you buy a house for £200,000 and the tenants pay £1,000 a month (£12,000 a year), your gross property rental yield is 6%.

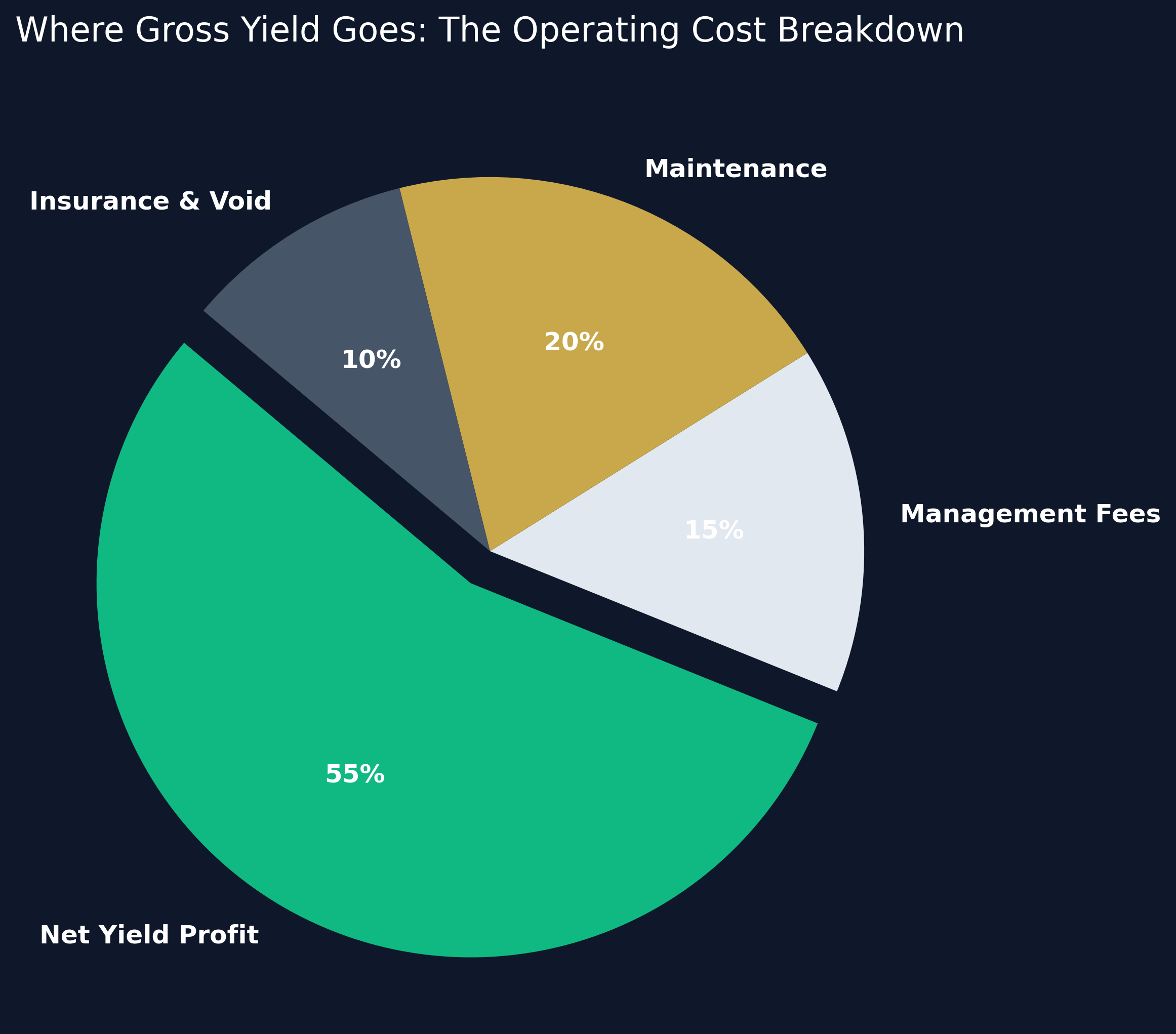

Gross vs. Net Yield

While gross property yield is useful for quickly comparing properties on Rightmove, it is incomplete. It ignores the reality of operating an asset.

Net yield provides a much clearer picture of your actual residential property investment returns.

- Net Yield = ((Annual Rental Income - Annual Operating Costs) ÷ Property Price) x 100

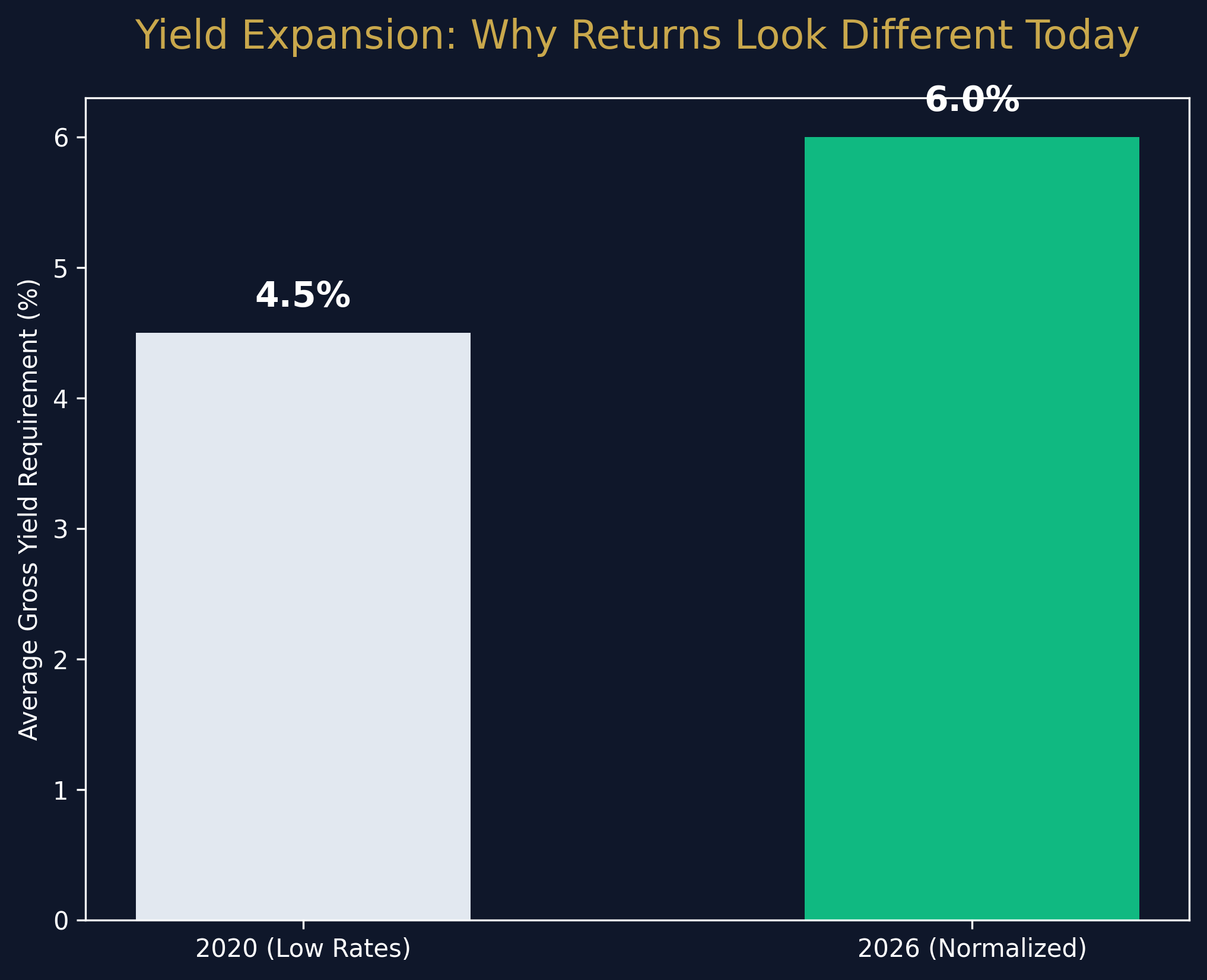

Operating costs include management fees (usually 10-12%), landlord insurance, maintenance reserves, ground rent, service charges, and void periods. If your £12,000 gross income is reduced by £3,000 in annual expenses, your net yield drops to 4.5%.

ROI vs. Yield: Know the Difference

A critical mistake novice investors make is confusing yield with ROI. While real estate investment yield looks at the income generated relative to the property's total purchase price, your return on investment for property (ROI) measures your profit relative to the actual cash you invested.

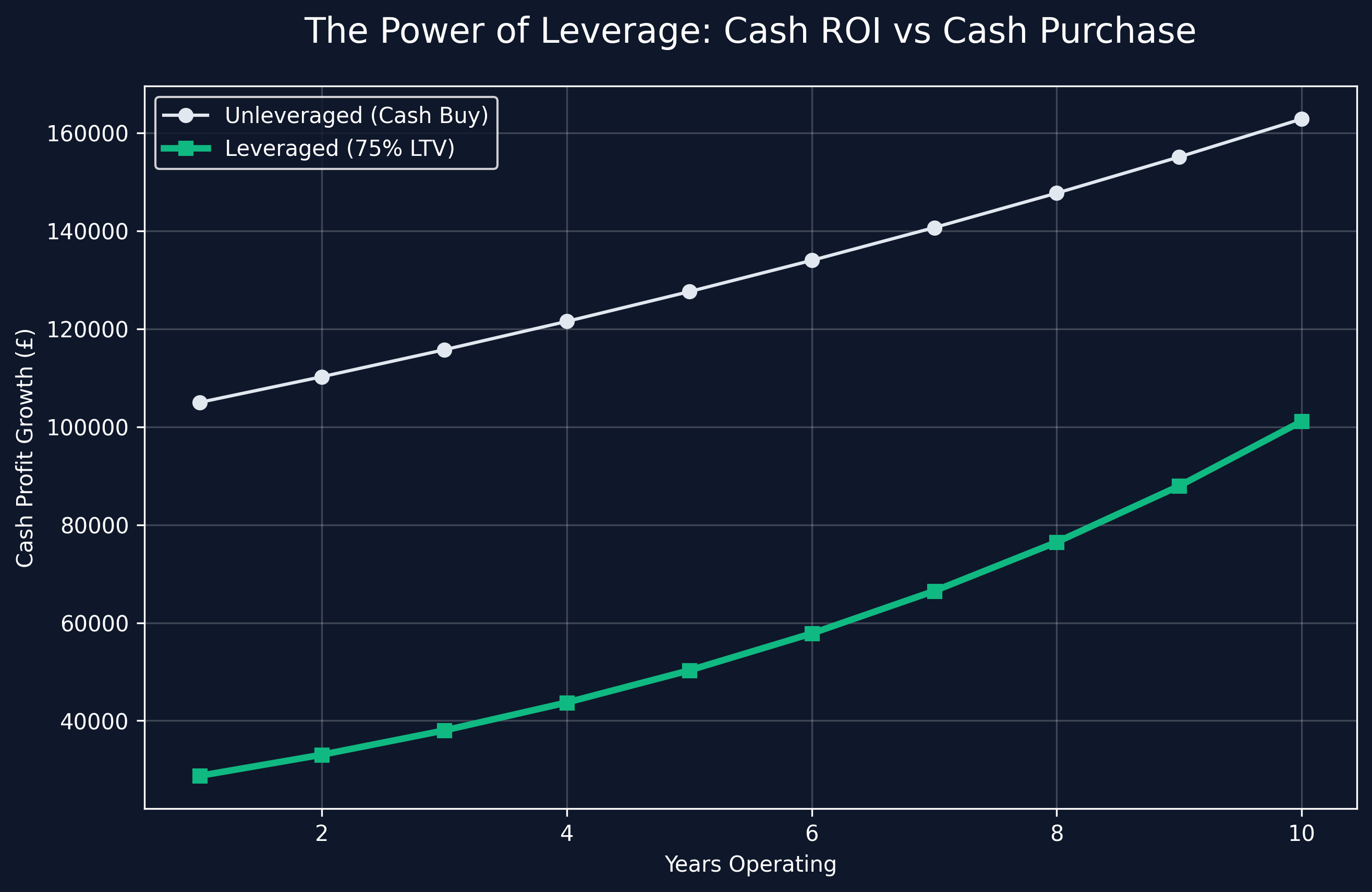

Because property is almost always bought using leverage (a mortgage), your cash invested is usually just a 25% deposit plus buying costs (Stamp Duty, legal fees).

Calculating True ROI

Imagine you buy a £200,000 property.

- You use a 75% LTV mortgage (£150,000) and put down a £50,000 deposit.

- Your buying costs (Stamp Duty, solicitors, surveys) total £10,000.

- Total cash invested: £60,000.

If your property generates £12,000 in gross rent, and your operating costs plus your mortgage interest total £7,000, your annual net profit is £5,000.

ROI = (Annual Net Profit ÷ Total Cash Invested) x 100 In this scenario, (£5,000 ÷ £60,000) x 100 = 8.3% ROI.

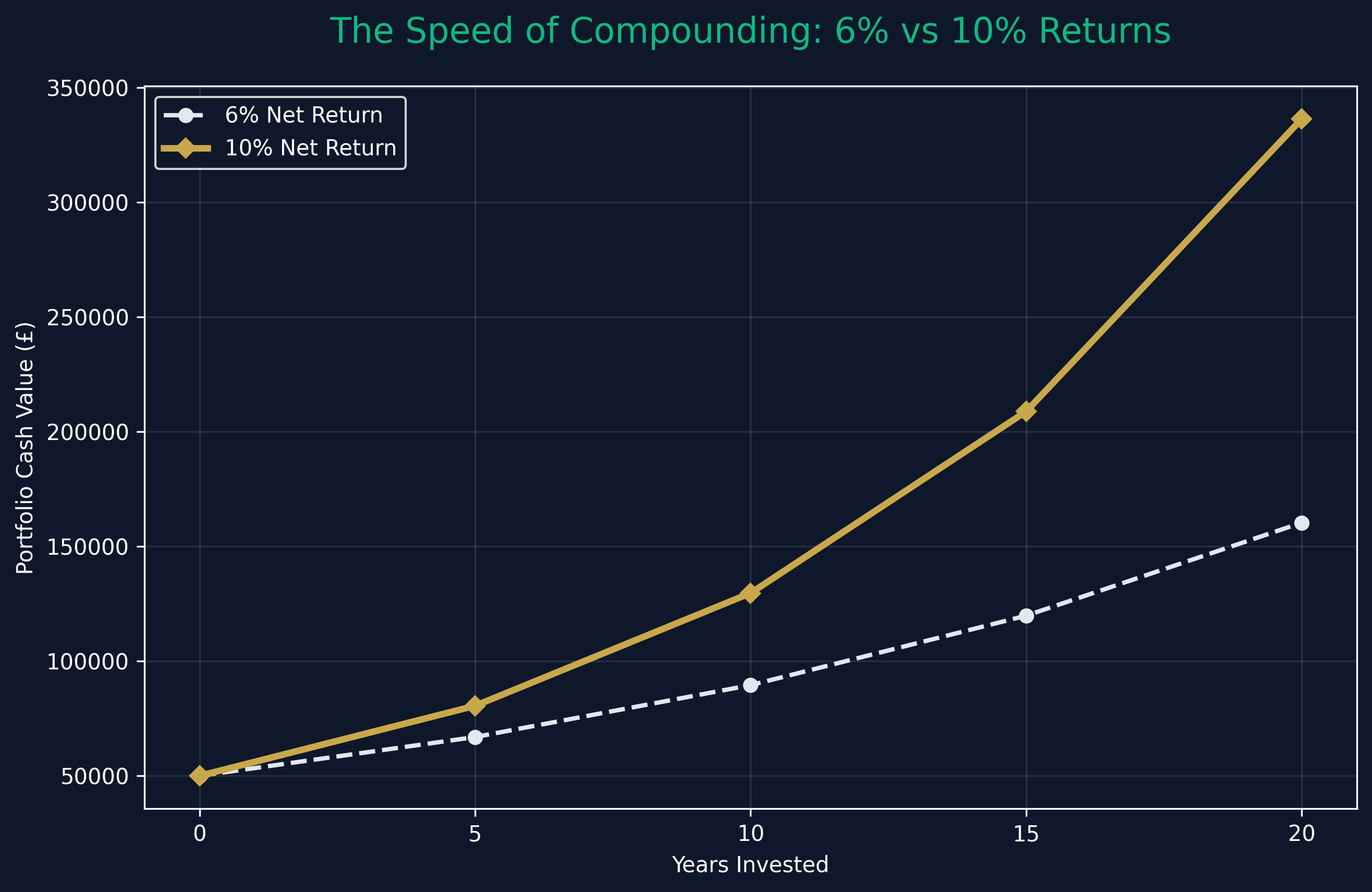

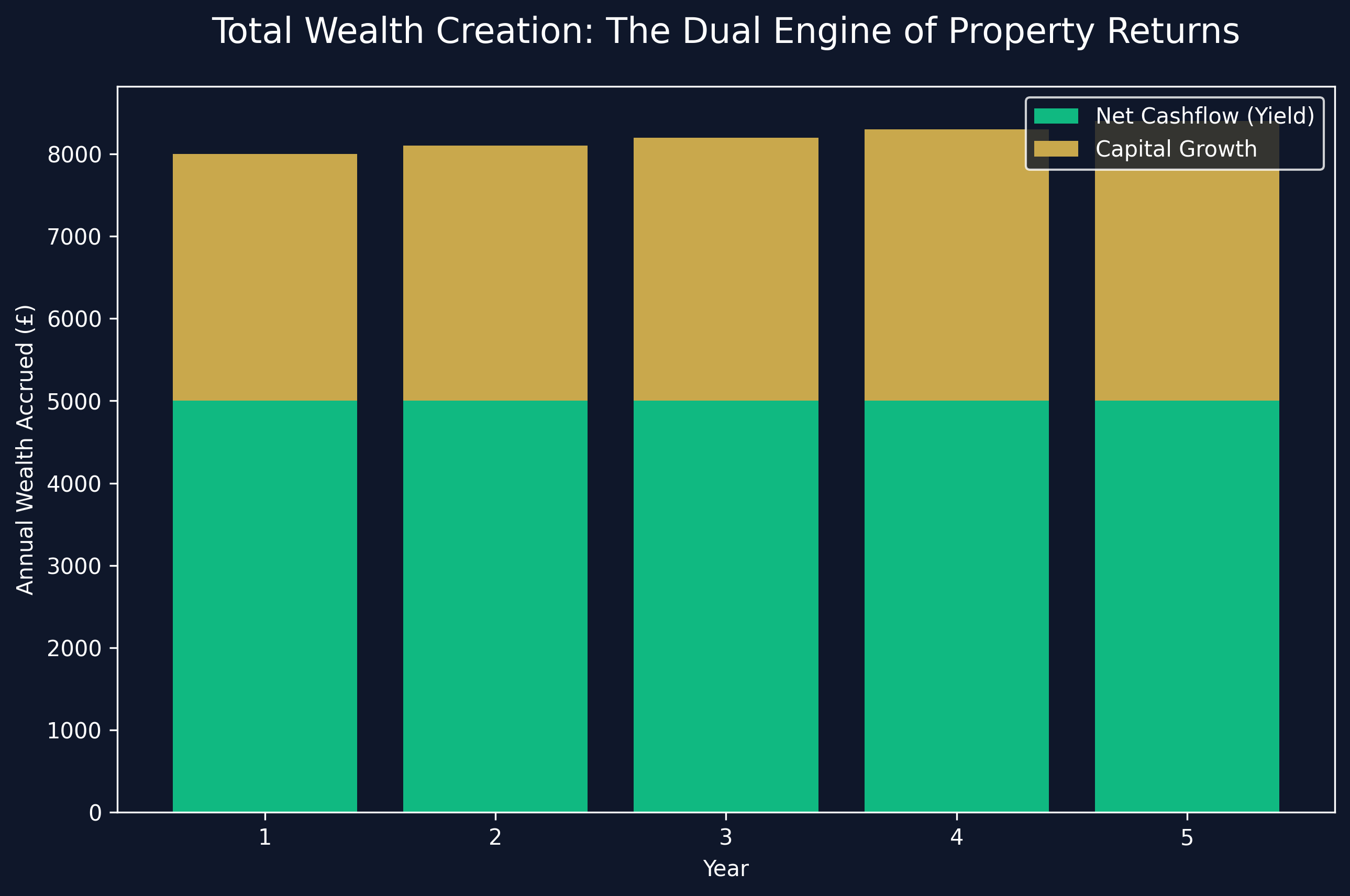

Notice how a 6% gross yield transformed into an 8.3% ROI? This is the power of leverage. If the property also appreciates in value by 3% that year (£6,000), your total wealth creation is £11,000 on a £60,000 investment—an exceptional 18.3% total return.

The 2026 Landscape: Average Returns

What should you expect right now? The average return on property investment across the UK shifted as we entered 2026, stabilizing after a period of high inflation.

According to major industry forecasts (including Savills, Rightmove, and JLL), the national picture looks like this:

- House Price Growth: Expected to be modest but steady, sitting between 2.0% and 3.5% annually.

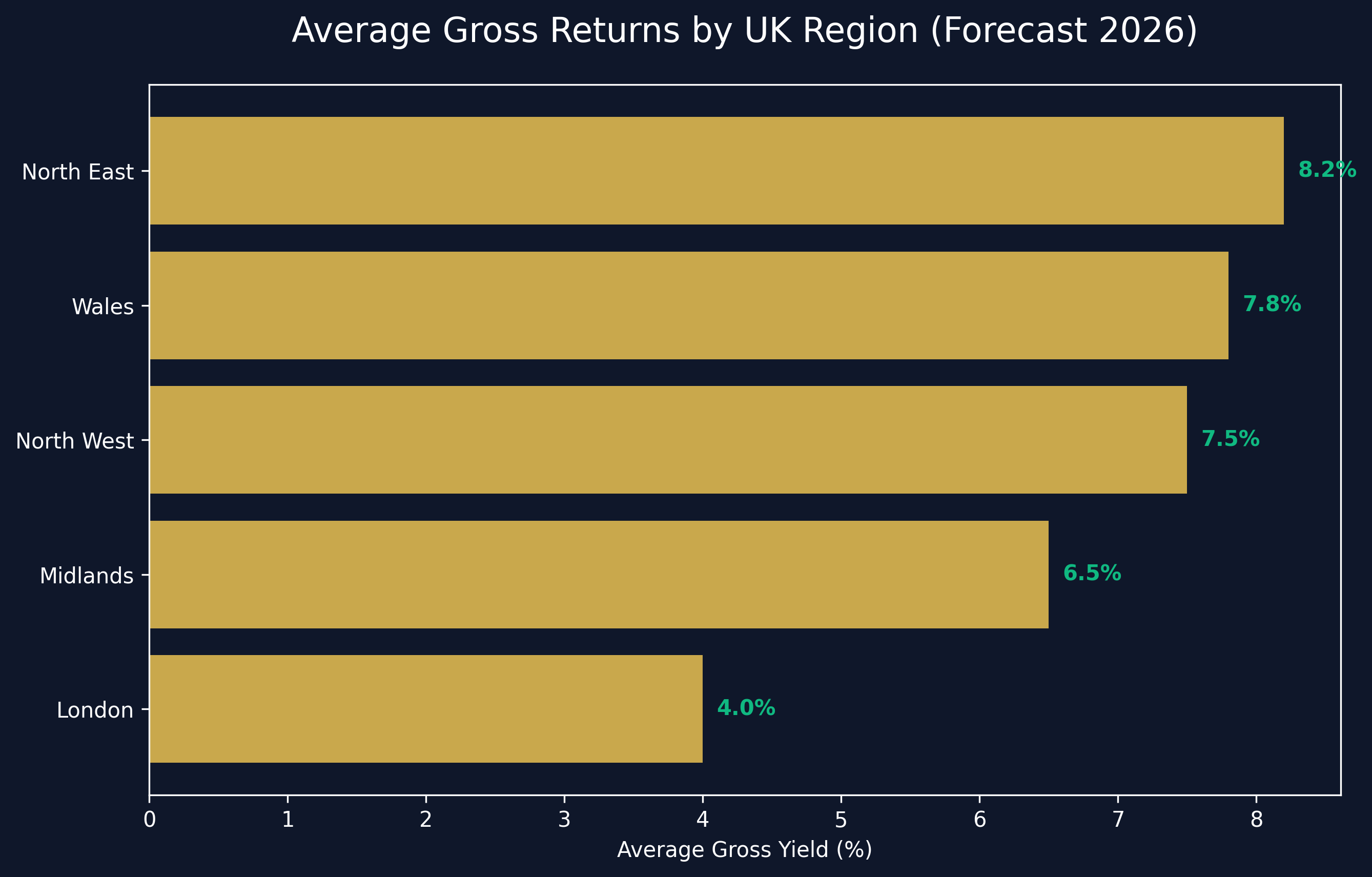

- Rental Yields: The national average gross yield is hovering around 5.9%. However, this is heavily skewed by London's high property prices and low yields (often 3-4%).

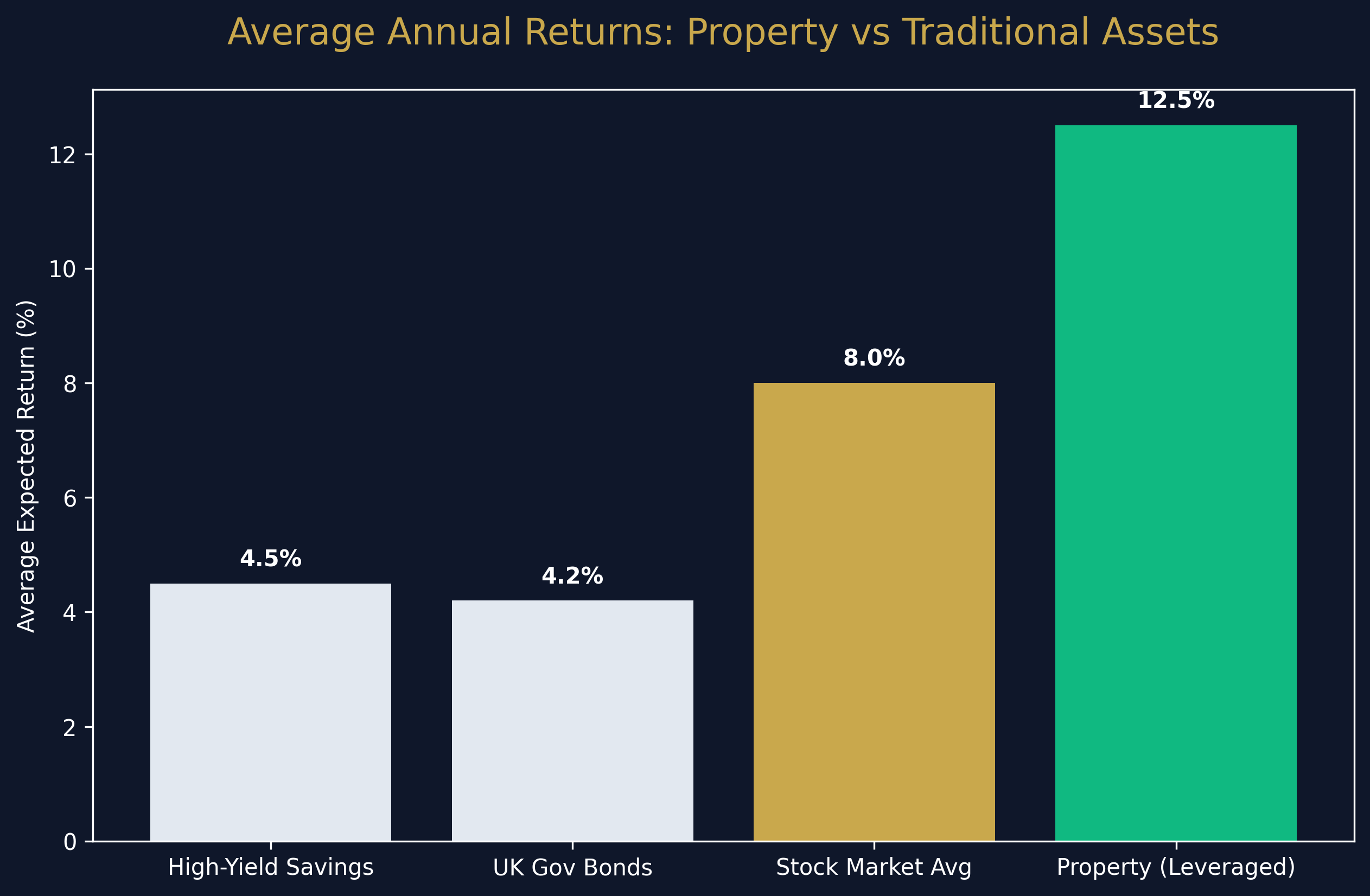

When you combine a 5.9% yield with a 3% capital growth rate, the average return on property investment (unleveraged) sits around 8.9% annually. When leveraged with a standard mortgage, top investors are seeing double-digit overall returns.

Where to Find the Best Returns

If you want the best property investment returns uk, you must look beyond the national averages. The smart money in 2026 is flowing distinctly away from the South East and toward specific high-growth regions.

High-Yield Northern Corridors

Cities like Hull, Liverpool, Bradford, and Sunderland are currently dominating the yield tables. Because property prices in these areas remain incredibly accessible (often under £130,000), but rental demand is fierce due to economic regeneration, gross yields of 8% to 10% are standard.

Targeting 12% Property Returns UK

Achieving double-digit returns on single-let residential properties is increasingly difficult. If you are strictly targeting 12 property returns uk, you must pivot your strategy towards specialist asset classes:

- HMOs (Houses in Multiple Occupation): Renting out by the room drastically increases rental income, frequently pushing gross yields past 12% in Northern university towns.

- Commercial Property: Industrial and logistics assets, or well-placed high street retail targeting essential services, can deliver very high yields, often on fully repairing and insuring (FRI) leases where the tenant covers maintenance.

- Holiday Lets / Serviced Accommodation: Short-term rentals on platforms like Airbnb generate significantly higher nightly rates than long-term ASTs, though this involves higher management intensity and regulatory risks.

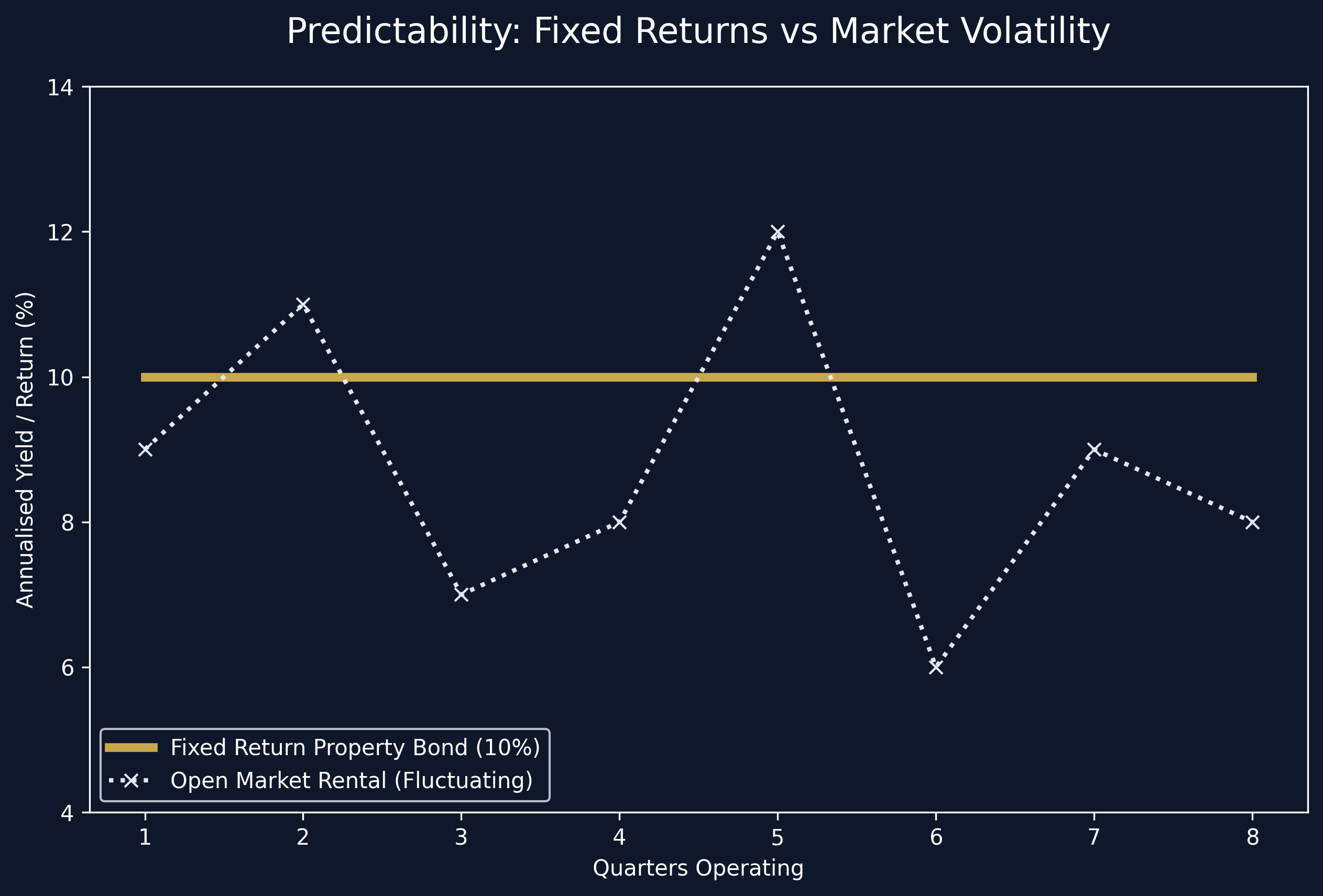

The Appeal of Fixed Return Property Investment

Not every investor wants to deal with the volatility of the open market, void periods, or boiler breakdowns. For those seeking absolute predictability, the fixed return property investment model is surging in popularity.

In these structures—often facilitated via property bonds, loan notes, or hands-off syndicates (SPVs)—you act as the bank. You lend your capital to an experienced property developer or sourcing company for a fixed term (usually 1 to 5 years). In exchange, they contractually guarantee you a set interest rate, completely independent of whatever the rental market does.

Currently, a strong fixed return property investment might offer 8% to 10% per annum, paid quarterly. Your capital is usually secured against the property asset via a first or second legal charge. It is the ultimate hands-off play for time-poor professionals.

Conclusion

Analyzing property investment returns uk requires you to look far past the asking price. By mastering the distinction between gross yield, net yield, and ROI, and by targeting high-performance areas in the North and Midlands, you can architect a portfolio that vastly outpaces inflation and traditional savings accounts.

Whether you opt for the aggressive cashflow of a Northern HMO, the steady capital appreciation of a suburban family let, or the hands-off predictability of a fixed-return bond, the mathematics of UK real estate in 2026 remain undeniably compelling.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →