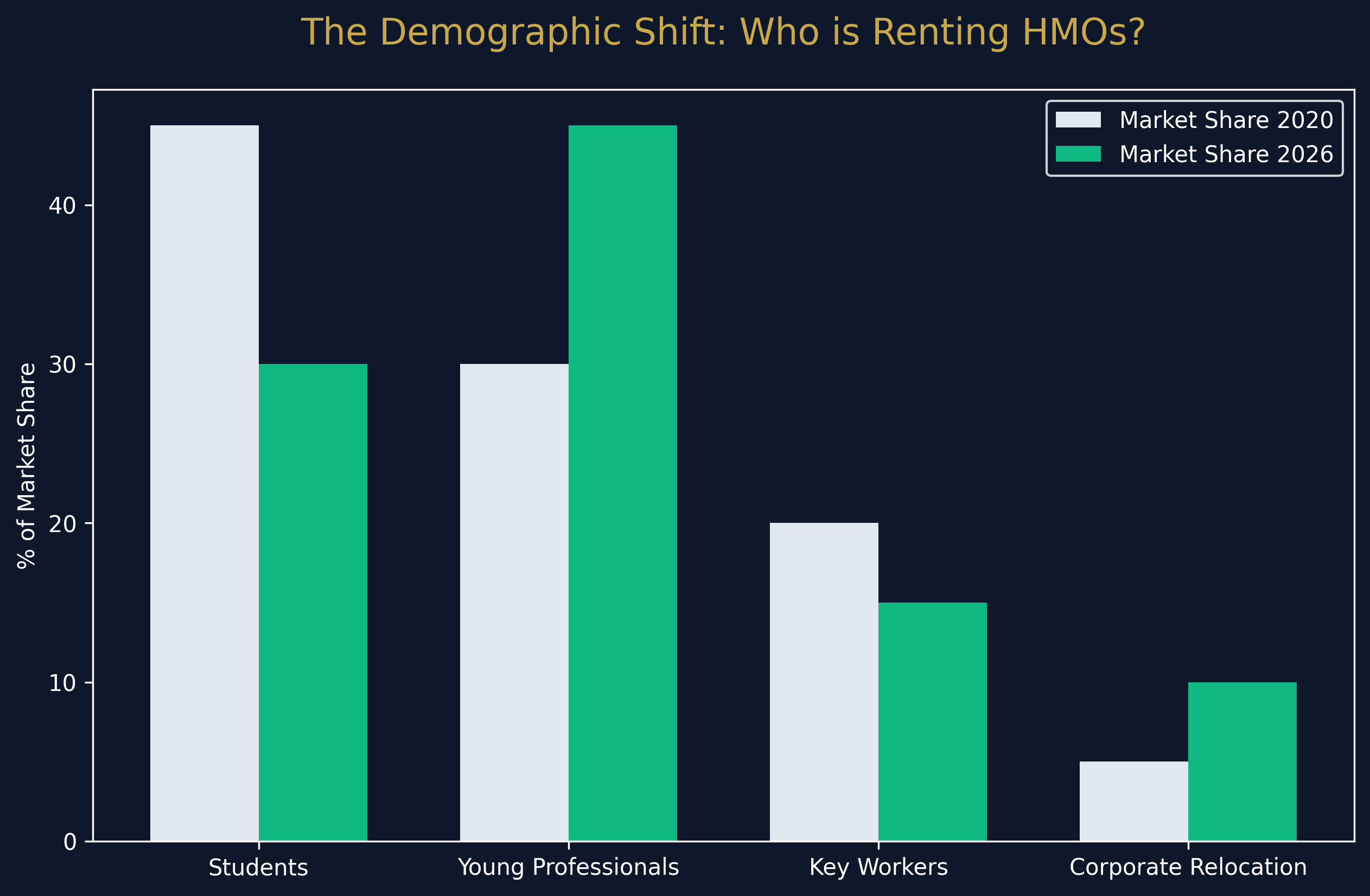

The UK Houses in Multiple Occupation (HMO) market in 2026 is arguably the most dynamic, heavily regulated, and potentially lucrative segment of residential property investment. As we move deeper into a landscape defined by stringent energy efficiency standards, the sweeping changes of the Renters' Rights Act, and an unyielding supply-demand imbalance, the "amateur landlord" era is officially over.

To succeed in 2026, investors must adopt institutional-grade strategies, prioritising scale, geographic arbitrage, and premium tenant experiences. This comprehensive guide outlines the definitive HMO strategies required to generate superior, risk-adjusted yields in the current market.

The Changing HMO Landscape in 2026

Before deploying capital, it is critical to understand the macroeconomic and regulatory forces shaping the 2026 HMO sector. The traditional model of converting a standard 3-bedroom semi-detached house into a 4-bedroom "mini-HMO" and managing it passively is largely obsolete.

The Regulatory Squeeze

Two major regulatory shifts are dictating HMO strategy in 2026:

- The Renters' Rights Act 2026: The abolition of Assured Shorthold Tenancies (ASTs) in favour of rolling periodic tenancies, coupled with the end of Section 21 "no-fault" evictions, means landlords must rely heavily on rigorous tenant referencing and retain tenants through exceptional service and property quality. Void periods are a more significant risk as tenants can leave with just two months' notice from day one.

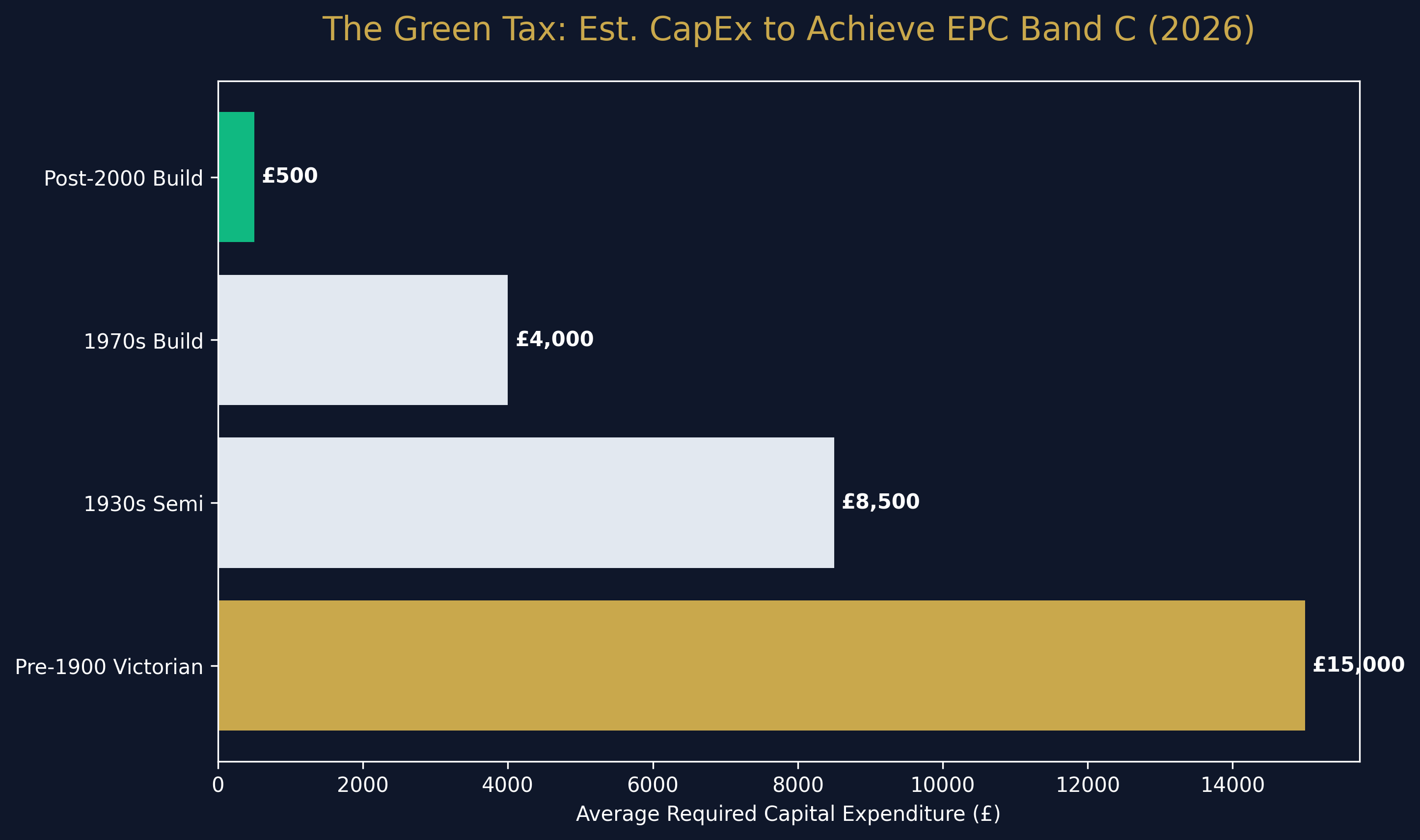

- EPC Rating 'C' Mandate: The requirement for all rental properties to achieve a minimum Energy Performance Certificate (EPC) of Band C is a hard deadline. Older, poorly insulated Victorian terraces—historically the staple for HMO conversions—now require substantial capital expenditure (CapEx) to meet these standards.

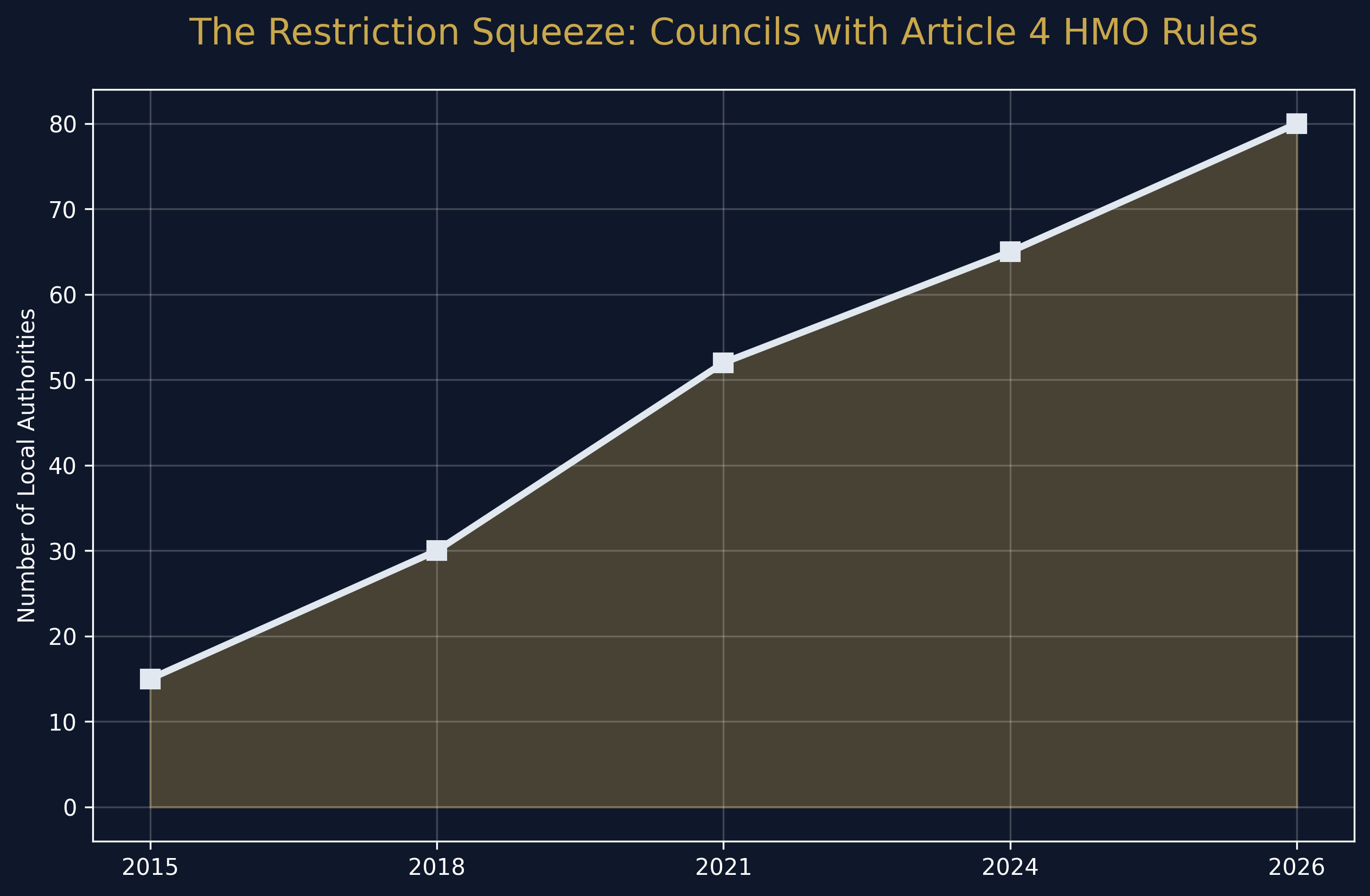

The Rise of Article 4 Directions

Local authorities are aggressively deploying Article 4 directions to curb the proliferation of small HMOs to preserve "family housing". This removes the permitted development right to convert a Use Class C3 (dwellinghouse) to a C4 (HMO for 3-6 people). Consequently, acquiring existing, licensed HMOs or purchasing commercial buildings for conversion are becoming more attractive, albeit capital-intensive, routes.

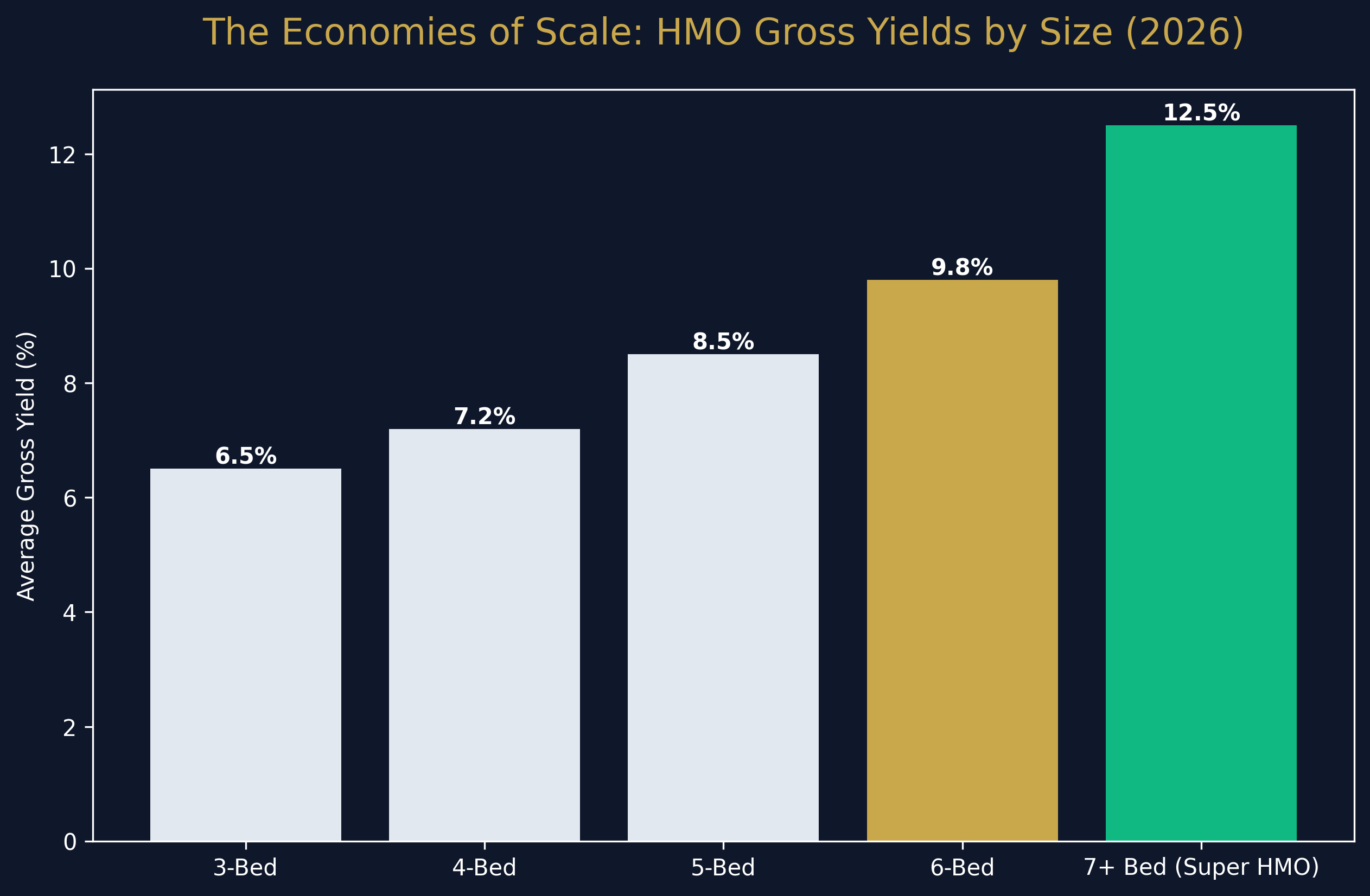

Strategy 1: The "Super HMO" and Economies of Scale

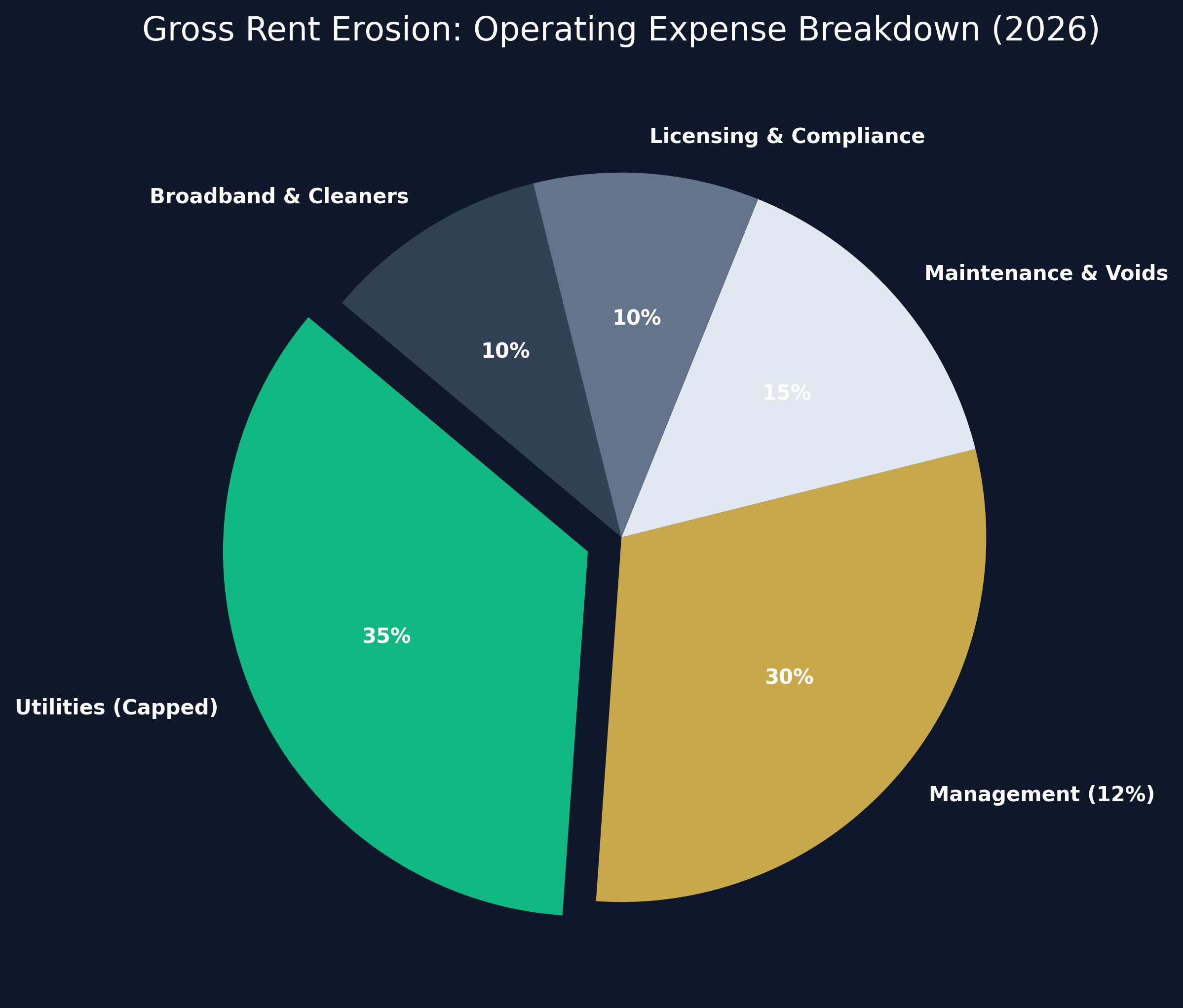

In an environment of rising operational costs (utilities, management fees, compliance certification), small 4-bed HMOs suffer from squeezed margins. The defining strategy for 2026 is the "Super HMO" – properties with 7+ to 15+ bedrooms.

Why Scale Wins

- Fixed Cost Dilution: The cost of an HMO license, fire alarm panel servicing, broadband, and communal cleaning are relatively fixed. Spreading these costs over 8 rooms rather than 4 drastically improves the net operating income (NOI).

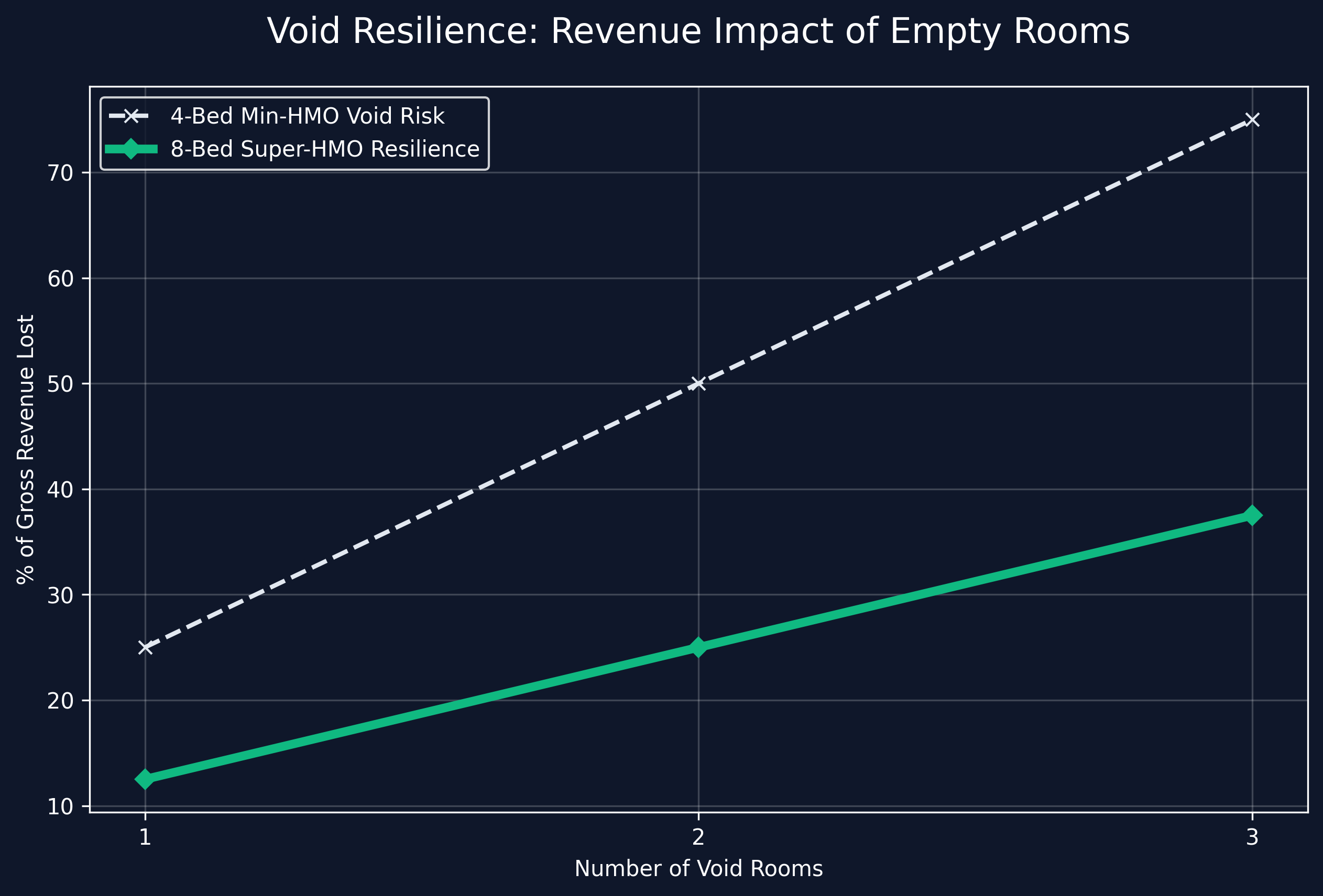

- Void Mitigation: In a 4-bed HMO, a single void room represents a 25% drop in gross revenue. In an 8-bed HMO, one void is only a 12.5% reduction. Larger properties offer inherent cash flow stability.

- Commercial Valuation (Yield-Based): Properties with 7 or more tenants (Sui Generis planning class) are typically valued on a commercial basis, as a multiple of their rental profit, rather than purely on bricks-and-mortar comparables. This allows investors to force appreciation through operational efficiency and rent increases.

Implementation

Look for large, detached properties, former guest houses, or small commercial premises (e.g., outdated office space under Class E to residential permitted development rights) that offer the square footage to accommodate 8+ en-suite rooms and generous communal living areas.

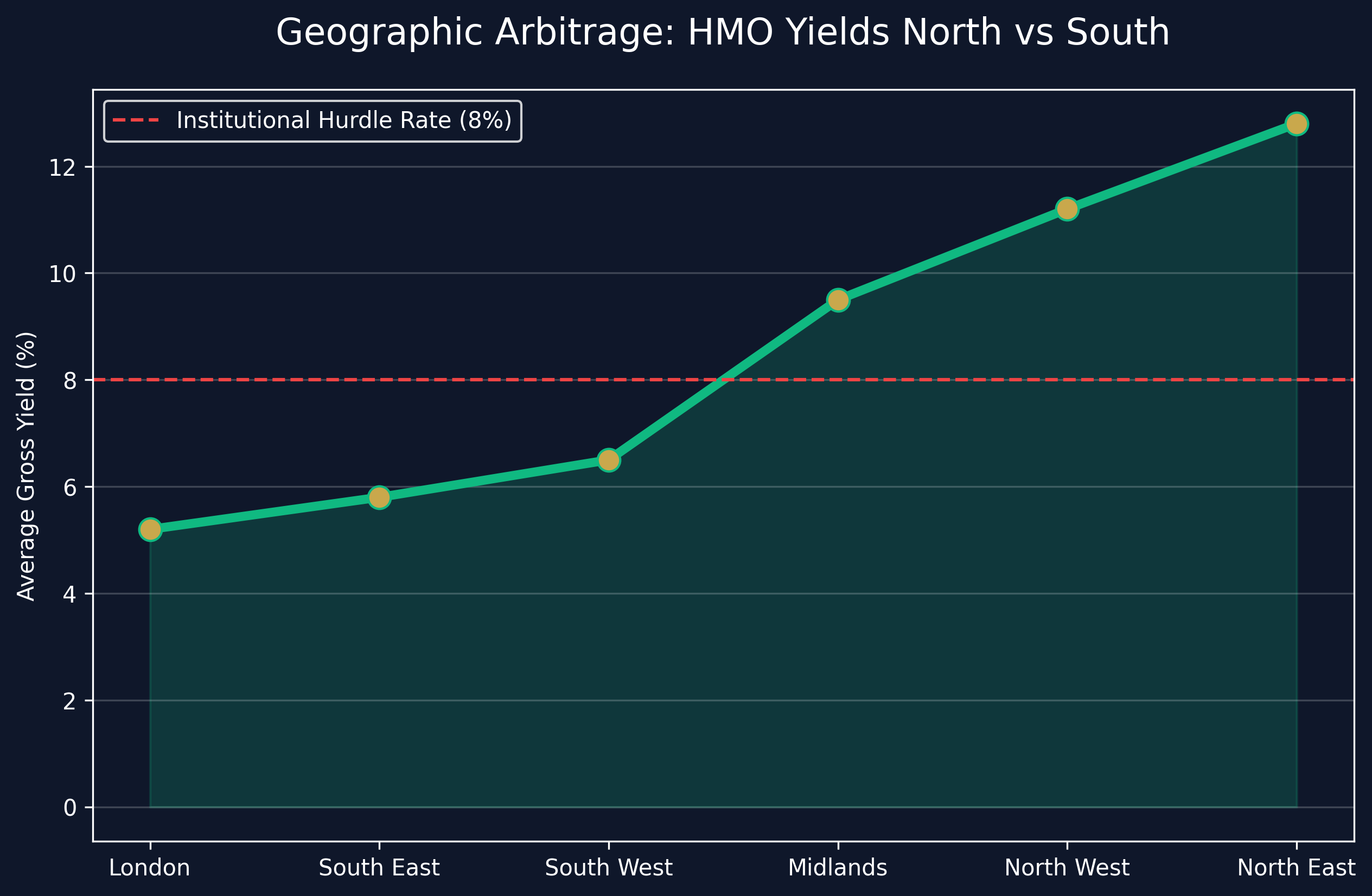

Strategy 2: Geographic Arbitrage (North vs. South)

The disparity in property prices versus rental income across the UK continues to widen. While London and the South East offer strong capital appreciation prospects, the gross yields rarely support complex HMO financing, especially under stressed Interest Coverage Ratios (ICR).

The Northern Powerhouse Yields

The most successful HMO investors in 2026 are deploying capital in Northern and Midlands cities, regardless of where they live.

- Target Cities: Liverpool, Manchester, Leeds, Sheffield, and Birmingham.

- Secondary Hubs: Look toward emerging markets like Sunderland, Middlesbrough, and parts of South Wales where the entry price is exceptionally low, but local employment (such as new gigafactories or tech hubs) drives robust rental demand.

- The Metric: Investors should target gross yields of 10% to 14% in these regions to ensure healthy net cash flow after the heavy operational expenses associated with HMOs.

The Remote Management Imperative

Geographic arbitrage necessitates remote management. You must build a highly competent local "power team," heavily reliant on a specialized, ARLA-registered HMO letting agent. Do not attempt to self-manage a highly-regulated asset 200 miles away. Factor a 10% to 15% management fee into your initial deal analysis; if the deal doesn't work with full management, it's not a viable deal.

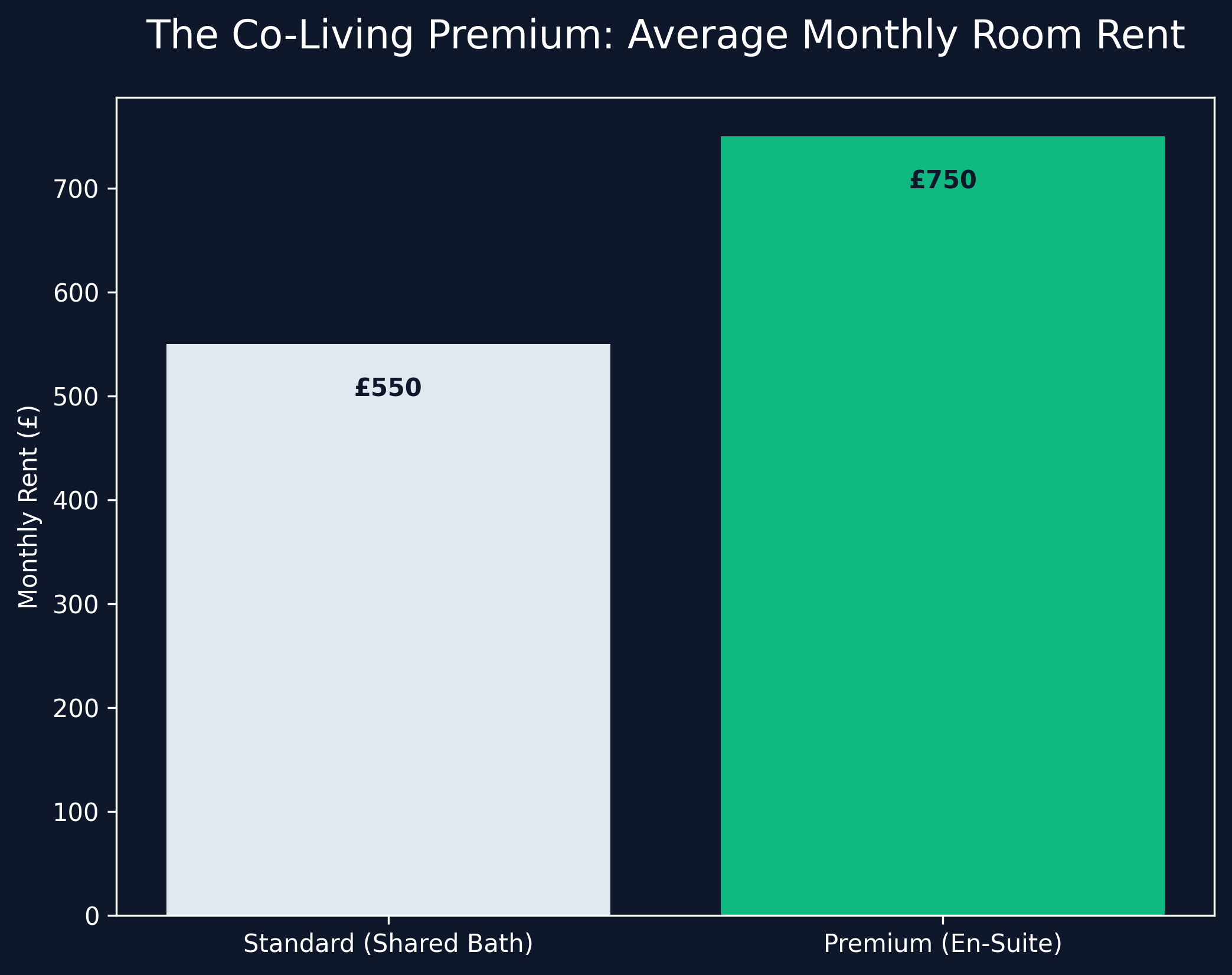

Strategy 3: The "Co-Living" Premium Experience

Today's HMO tenants—predominantly young professionals, travelling nurses, and mature post-graduates—are not content with subpar accommodation. They are paying premium rents and expect a product that reflects the "build-to-rent" (BTR) institutional aesthetic.

Designing for Retention

In the era of the Renters' Rights Act, tenant retention is your primary defense against costly voids. The "Co-Living" strategy focuses on high-end design to attract and keep tenants.

- En-Suites as Standard: The market expectation in 2026 is an en-suite bathroom for every room. While it increases the initial CapEx and reduces communal space, it commands a rent premium of £100-£150 per month over off-suite rooms and drastically reduces time-to-let.

- Enterprise-Grade Connectivity: "Fast broadband" is no longer a perk; it's a utility as essential as water. Install commercial-grade mesh Wi-Fi networks with explicit bandwidth management to support multiple tenants working from home concurrently.

- Bespoke Communal Spaces: Move away from forcing a sofa into an awkwardly shaped kitchen. Design dedicated, comfortable living rooms and consider incorporating dedicated co-working areas or small home gyms within the property.

- Aesthetic Distinction: Utilize interior designers. Feature walls, premium lighting fixtures, and high-quality, durable furniture (rather than flat-pack budget options) create an aspirational living environment that commands top-decile rents.

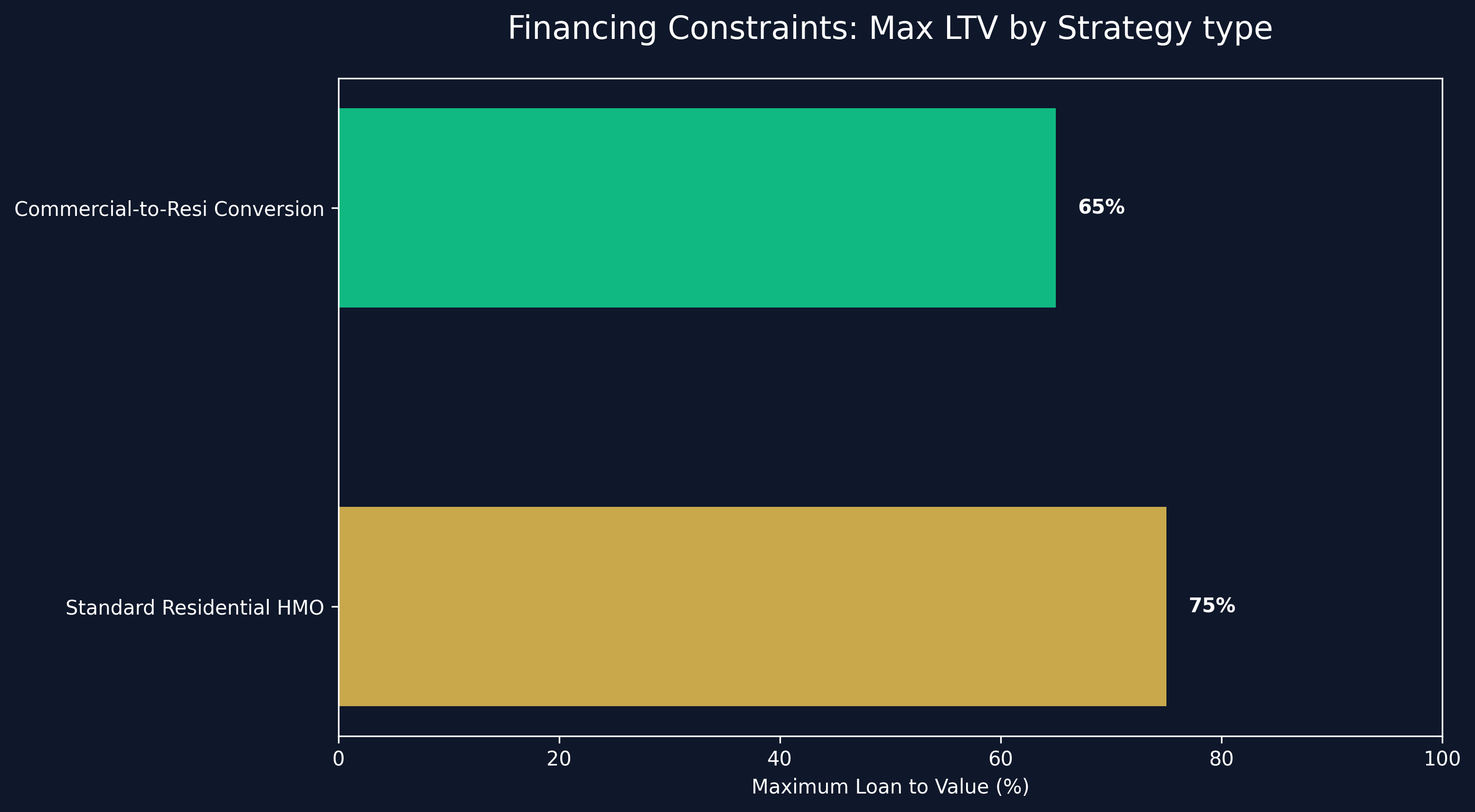

Strategy 4: Commercial-to-Residential Conversions

Given the regulatory friction of Article 4 directions limiting the conversion of standard housing stock, savvy investors are pivoting to commercial buildings.

The Permitted Development Advantage

Recent expansions in Permitted Development Rights (PDR) allow for the smoother transition of certain commercial spaces (Class E) into residential dwellings (Class C3/C4).

- Retail and Office Space: Vacant high-street retail with upper parts, or redundant office blocks, often offer exceptional square footage at a lower price per square foot than residential stock.

- The Challenge: These projects are heavily capital intensive and require bridging finance or commercial development loans, followed by a refinance onto an HMO term mortgage once tenanted. They also carry higher construction and planning risks (such as ensuring adequate natural light for all habitable rooms).

- The Reward: Successfully converting an empty commercial shell into a 10-bed, high-spec HMO creates massive equity uplift and un-locks double-digit yields that are nearly impossible to achieve by purchasing existing residential stock.

Strategy 5: Advanced Energy Efficiency (Future-Proofing)

The EPC 'C' mandate is merely the beginning. True professional investors are viewing energy efficiency not as a regulatory burden, but as a strategic advantage to attract eco-conscious tenants and protect their margins against volatile energy markets.

The "Bills Included" Dilemma

Most HMOs are let on a "bills included" basis, exposing the landlord to unlimited energy consumption. In 2026, relying solely on a "fair usage clause" in the tenancy agreement is insufficient.

- Strategic Upgrades: Beyond basic insulation, consider installing Air Source Heat Pumps (ASHPs) combined with smart multi-zone heating controls. This allows the landlord (or the management agent) to monitor and remotely cap heating temperatures in individual rooms, drastically reducing waste.

- Solar PV: Integrating solar panels and battery storage can offset a significant portion of communal electricity usage, directly improving the bottom line.

Summary

The optimal HMO strategy for 2026 is a synthesis of scale, location, and supreme quality. The market has bifurcated: amateur landlords operating tired, non-compliant 4-bed properties will face shrinking margins, regulatory fines, and extended void periods.

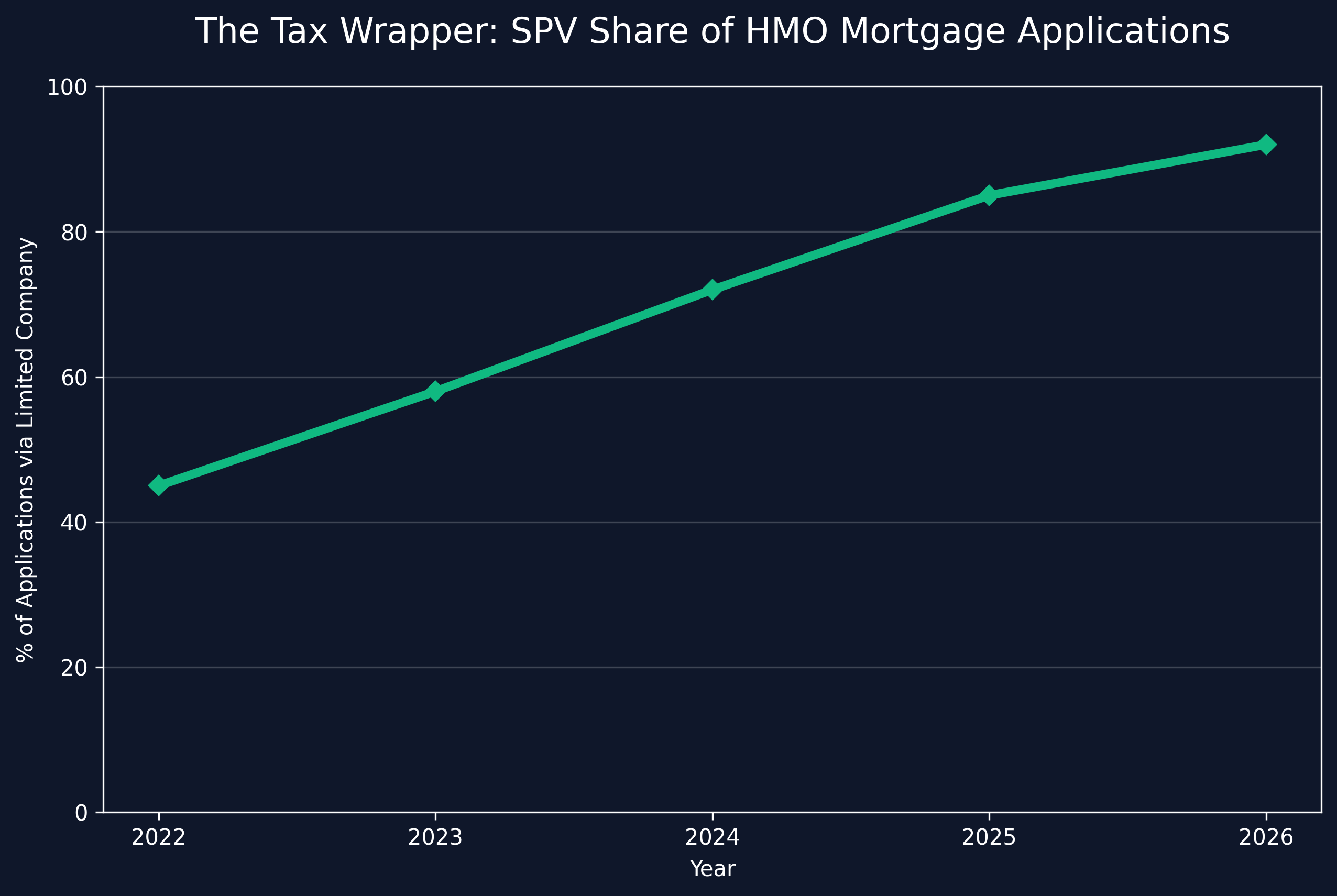

Conversely, investors who treat their HMO portfolio as a hospitality business—developing 6+ bed, high-specification co-living spaces in high-yield Northern and Midlands territories, wrapped in tax-efficient corporate structures—will capture the outsized returns that the HMO market continues to offer. Focus on the data, build a professional team, and execute with institutional precision.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →