The UK rental property market in 2026 is not the same game it was five years ago. Between a landmark new tenancy law, a tax regime that punishes the unprepared, and mortgage rates that have finally stabilised after years of volatility, the strategies that worked in 2021 will underperform—or outright fail—in this environment. The landlords who thrive in 2026 will be the ones who treat their portfolio as a business, not a side hustle.

This guide breaks down the most effective rental property strategies for 2026, backed by current market data, real regulatory timelines, and the financial modelling that separates profitable investors from those who quietly sell up and leave the sector.

Executive Summary

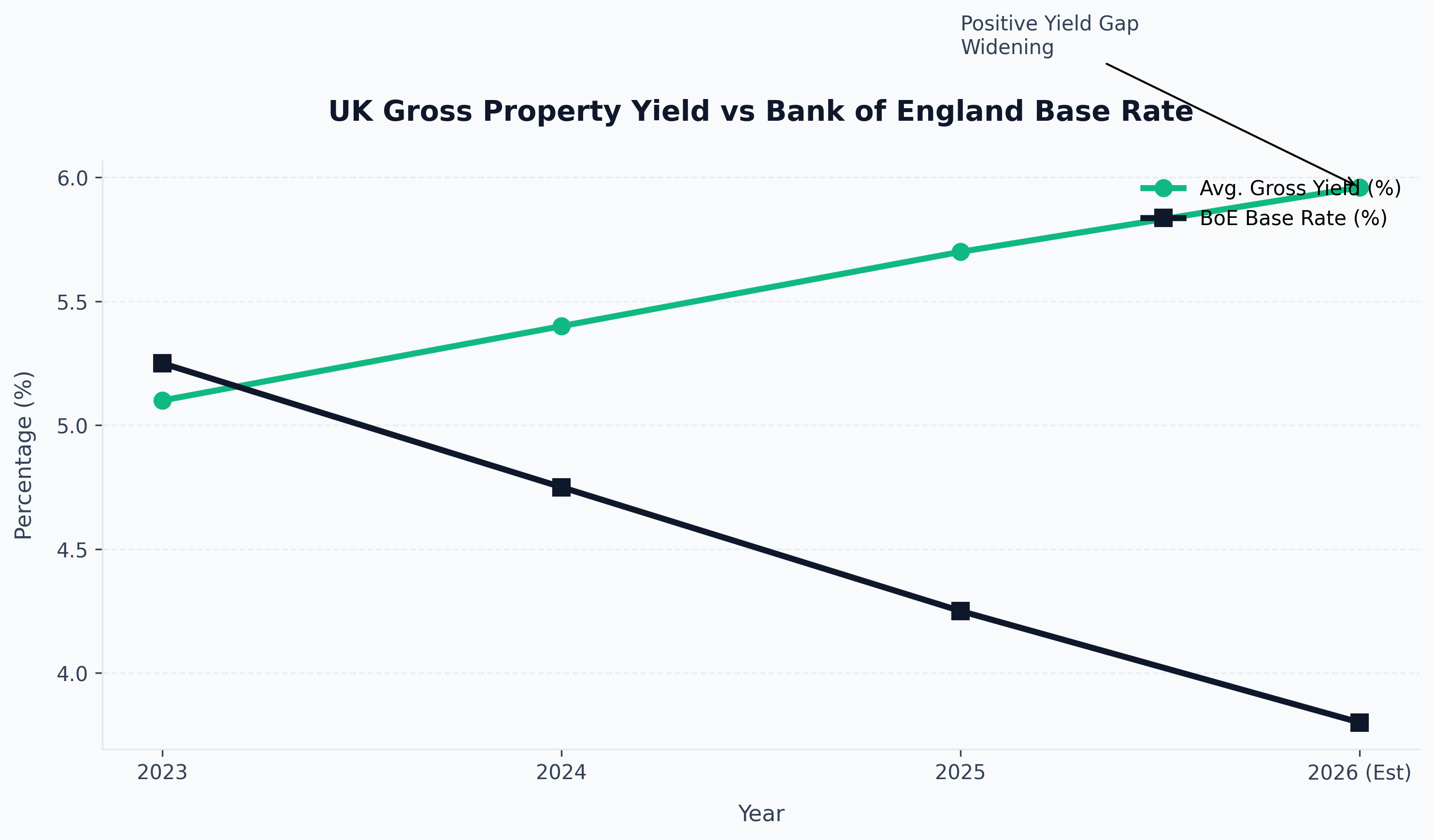

The 2026 UK rental market is defined by three forces: the Renters' Rights Act (effective 1 May 2026), stabilising interest rates in the 3.75–4.75% range, and persistent tenant demand driven by structural undersupply. National house prices are forecast to grow 2–4% annually, while rents are projected to rise 4–6% in high-demand regions. The most effective strategies centre on high-yield regional assets, corporate tax structuring, and operational professionalisation.

| Key Metric | 2026 Figure |

|---|---|

| Average UK gross rental yield | 5.96% |

| BTL mortgage rate range | 3.75%–4.75% |

| Projected national house price growth | 2%–4% |

| Projected 5-year rental growth (national) | 12% |

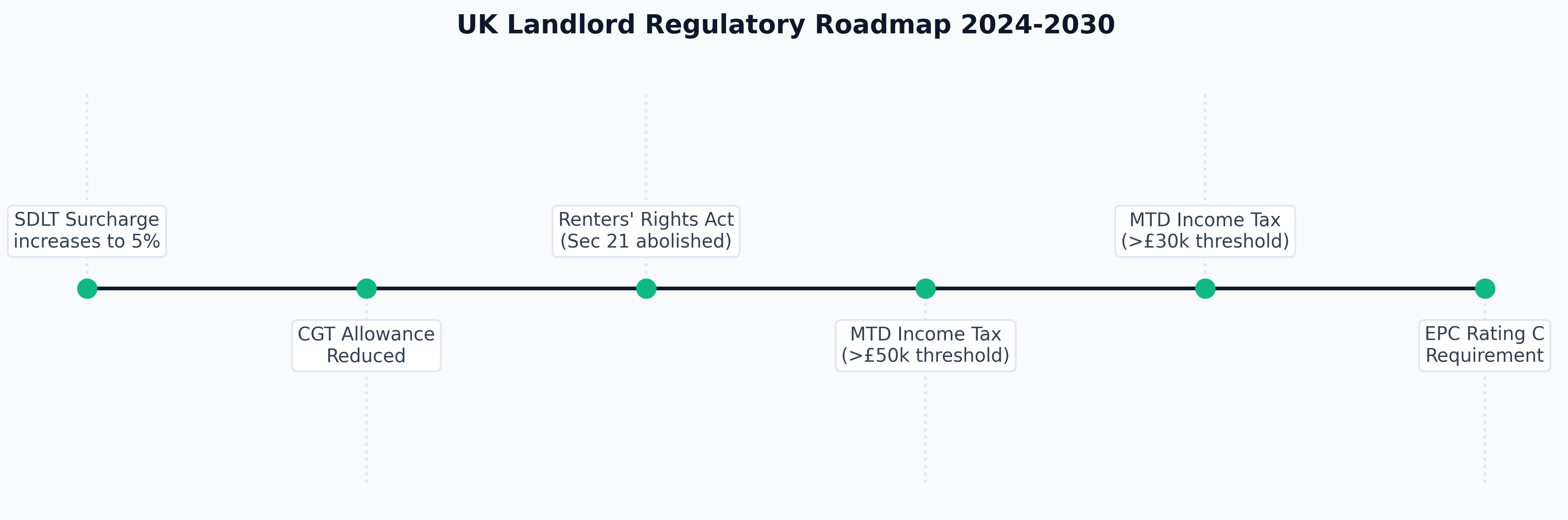

| SDLT surcharge on additional properties | 5% |

| Renters' Rights Act effective date | 1 May 2026 |

| MTD for Income Tax threshold (April 2026) | £50,000+ |

Strategy 1: Target High-Yield Regional Hotspots

The single most impactful decision a rental property investor makes in 2026 is location selection. The data overwhelmingly favours regional cities outside of London and the South East.

Why Regional Beats London

London's average gross yield sits stubbornly below 4.5%, crushed by entry prices that require enormous deposits and rental ceilings constrained by tenant affordability. Meanwhile, northern and midland cities consistently deliver gross yields between 6% and 8%, with some fully managed apartments achieving net yields of 8–10%.

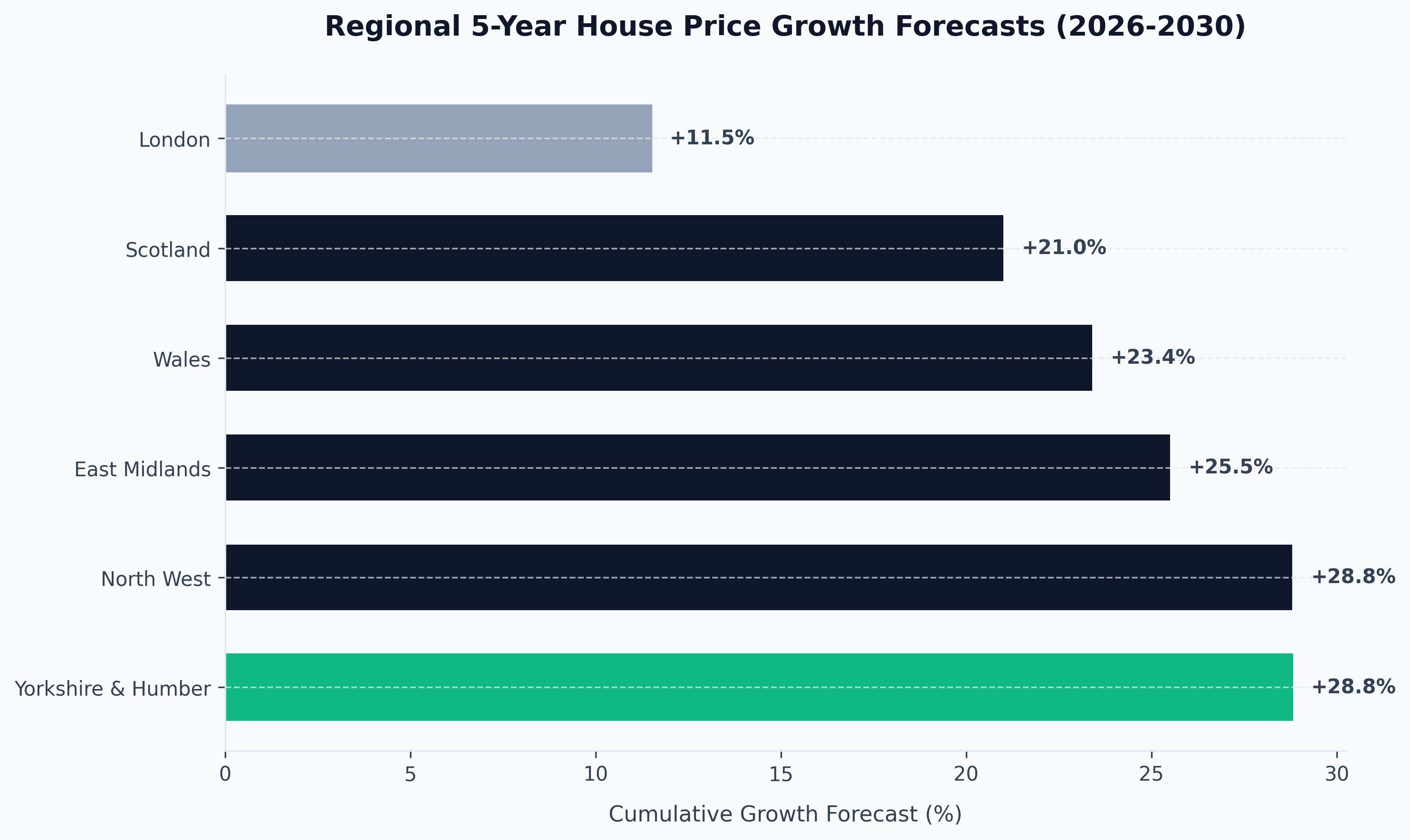

Savills forecasts average UK house price growth of 22.2% over the next five years, but the regional picture is far more compelling. Yorkshire and The Humber leads with a projected 28.8% increase, followed by the North West at a similar trajectory. These are markets where £120,000–£180,000 buys a two-bedroom terraced property generating £700–£850 per month in rent.

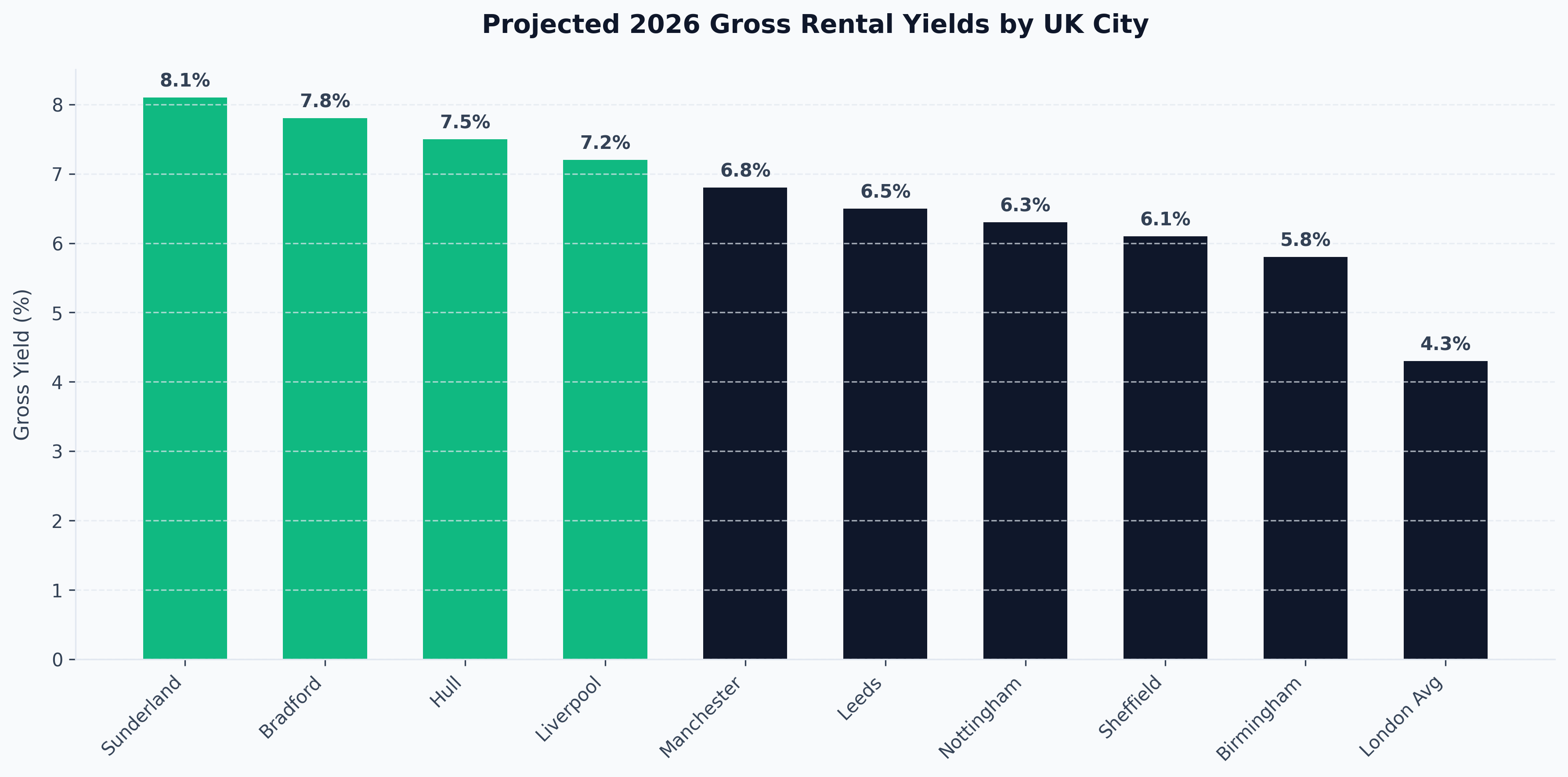

The 2026 Regional Yield League Table

| City | Average Gross Yield | Median Purchase Price | Key Demand Driver |

|---|---|---|---|

| Liverpool | 7.2% | £135,000 | Regeneration, student population |

| Manchester | 6.8% | £195,000 | Professional demand, MediaCity |

| Leeds | 6.5% | £175,000 | Financial services hub, university city |

| Nottingham | 6.3% | £155,000 | Two universities, affordable entry |

| Sheffield | 6.1% | £145,000 | Advanced manufacturing, growing tech sector |

| Hull | 7.5% | £95,000 | Ultra-low entry point, improving infrastructure |

| Bradford | 7.8% | £85,000 | Lowest entry prices in England |

| Birmingham | 5.8% | £185,000 | HS2 spillover, major regeneration |

| Warrington | 6.4% | £165,000 | Strategic location, logistics corridor |

| Sunderland | 8.1% | £80,000 | Nissan investment, university demand |

What Reddit Investors Are Saying

The sentiment across UK property forums and Reddit communities like r/HousingUK and r/UKPersonalFinance is mixed but revealing. Experienced landlords consistently warn against chasing headline yields without stress-testing the numbers. One recurring theme: "A 7% gross yield in a D-rated EPC terrace in a declining postcode is worse than a 5.5% yield in a modern-build flat near a transport hub."

The practical takeaway from social mining is clear—investors who succeed in 2026 are those who layer yield analysis with micro-location fundamentals: employment anchors, transport links, planned regeneration, and tenant demographic stability.

Strategy 2: HMO and Multi-Let Conversions

Houses in Multiple Occupation remain one of the highest-yielding strategies available to UK investors, but the 2026 regulatory environment demands rigorous compliance.

The HMO Yield Advantage

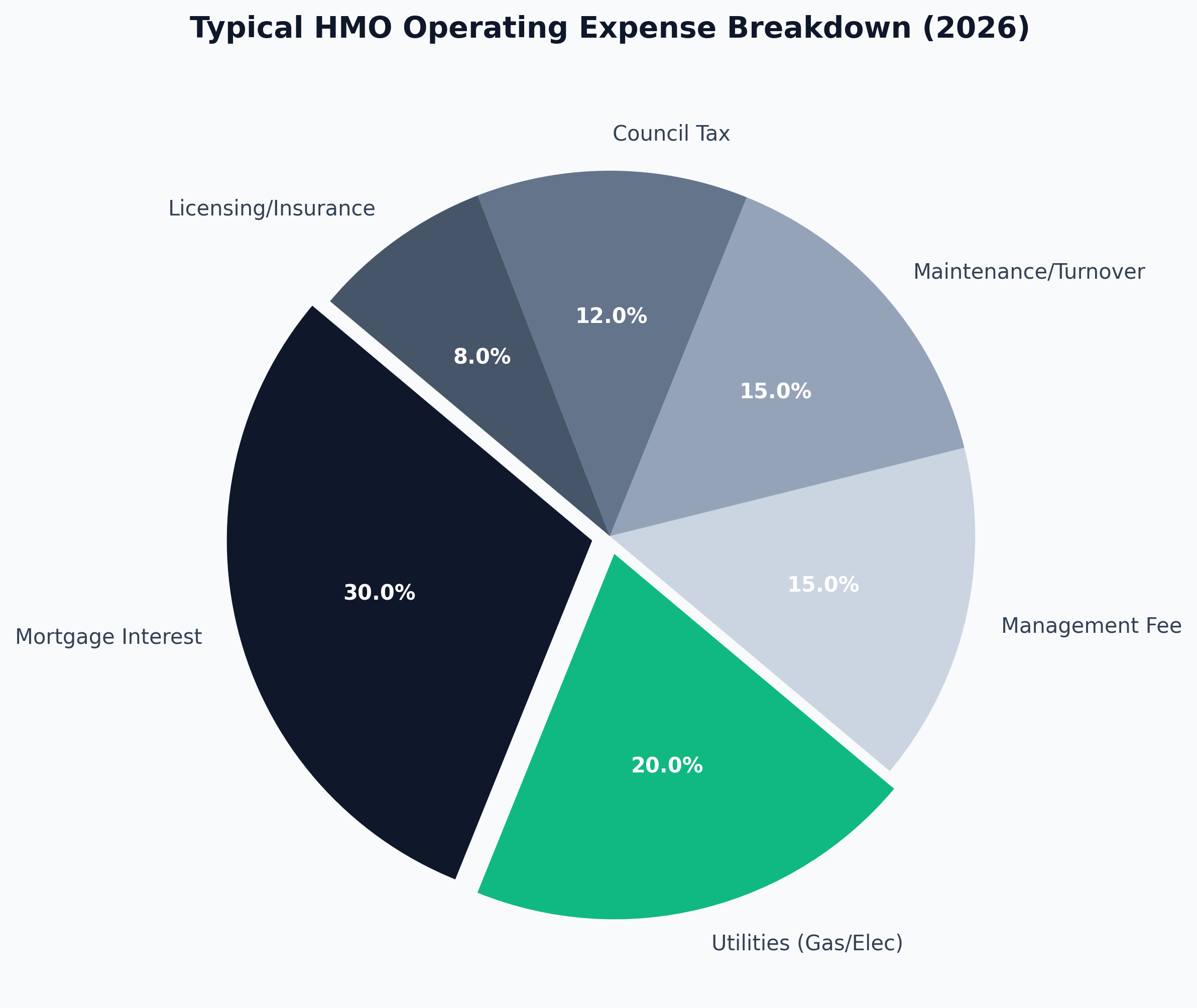

A standard single-let generating £750 per month in rent from a £150,000 property delivers a gross yield of 6%. That same property, converted into a licensed 4-bedroom HMO, could generate £1,600–£2,000 per month (£400–£500 per room), pushing the gross yield to 12.8–16%.

However, net yield is where the real analysis matters. HMOs carry substantially higher operating costs:

| Cost Category | Single Let (Annual) | HMO (Annual) |

|---|---|---|

| Council tax | Tenant pays | Landlord pays: £1,200–£1,800 |

| Utilities | Tenant pays | Landlord pays: £2,400–£3,600 |

| Management fee (10–15%) | £900 | £2,400 |

| Licensing & compliance | £0–£100 | £500–£1,200 |

| Higher maintenance/turnover | £500 | £1,500–£2,500 |

| Insurance premium | £250 | £600–£900 |

Even accounting for these costs, a well-managed HMO in a strong location typically delivers a net yield 3–5 percentage points above a single let on the same property.

Licensing and the Renters' Rights Act

The mandatory HMO licensing regime requires properties with five or more occupants from two or more households to hold a licence. Many local authorities have implemented Additional Licensing schemes covering smaller HMOs. Under the Renters' Rights Act, failure to comply with housing standards can trigger Rent Repayment Orders of up to 24 months' rent—a devastating financial penalty.

Before committing to an HMO conversion, investors must:

- Check the local authority's Article 4 Direction status — many councils now require planning permission for HMO conversions

- Budget £15,000–£30,000 for conversion costs including fire doors, escape routes, and en-suite facilities

- Secure the correct licence before advertising any rooms

- Implement professional management — HMOs are operationally intensive

Strategy 3: Off-Plan and New-Build Investment

Purchasing off-plan property—buying before or during construction at a discounted price—remains a high-performing strategy in 2026, particularly in cities undergoing major regeneration.

Why Off-Plan Works in the Current Market

The mechanics are straightforward. Developers offer units at 10–20% below projected market value to fund construction. The investor typically pays a reservation fee (£2,000–£5,000) and then a staged deposit (usually 20–30% split across construction milestones). By completion, the property has appreciated in line with—or above—the wider market, delivering instant equity.

Key off-plan hotspots for 2026 include:

- Liverpool Waters — the £5.5bn mixed-use regeneration zone with projected yields of 7–8%

- Manchester Salford Quays — ongoing MediaCity expansion driving professional rental demand

- Birmingham Smithfield — the city's largest regeneration project, replacing the old Bull Ring markets

- Leeds South Bank — a 253-acre regeneration area expected to double the size of the city centre

The Risks to Manage

Off-plan investment is not without risk. Developer insolvency, construction delays, and completion valuations coming in below the purchase price are all documented hazards. Mitigating these requires:

- Developer due diligence — check Companies House filings, previous project completion records, and financial accounts

- Stage-payment structures — avoid developers demanding more than 30% before completion

- Independent valuations — secure your own RICS valuation rather than relying on the developer's figures

- Exit strategy — ensure the local rental market can absorb the unit at the projected rent within 4–6 weeks

Strategy 4: Corporate Structure and Tax Optimisation

The 2026 tax landscape makes the question of how you hold property as important as which property you buy. For higher-rate taxpayers, the personal ownership model is increasingly punitive.

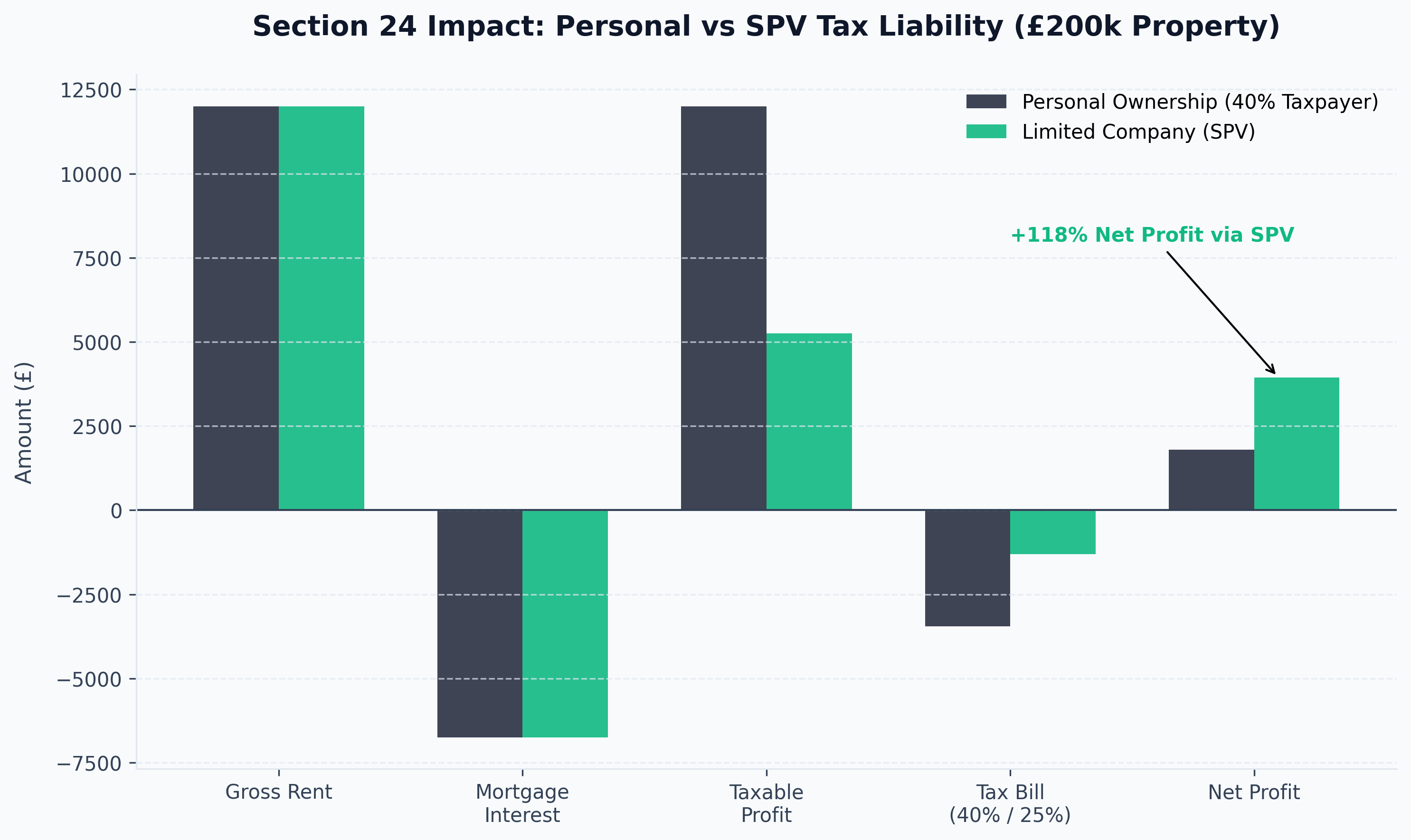

Section 24: The Tax Trap That Still Bites

Section 24 of the Finance (No. 2) Act 2015 restricts mortgage interest relief for individual landlords to the basic rate of income tax (20%). For a 40% taxpayer with a £150,000 interest-only mortgage at 4.5%, this creates a phantom tax liability on income they never actually received.

Worked example — £200,000 property, £150,000 mortgage at 4.5%:

| Metric | Personal Ownership | Ltd Company (SPV) |

|---|---|---|

| Annual rent | £12,000 | £12,000 |

| Mortgage interest | £6,750 | £6,750 |

| Actual profit | £5,250 | £5,250 |

| Taxable income | £12,000 (with 20% credit) | £5,250 |

| Tax liability (40% personal / 25% corp) | £3,450 | £1,313 |

| Net profit after tax | £1,800 | £3,937 |

The difference is stark: £2,137 more per property per year retained through a limited company. Over a 10-property portfolio, that is £21,370 annually—enough to fund an additional acquisition every two years from tax savings alone.

Making Tax Digital: Prepare Now

From 6 April 2026, landlords with gross property income exceeding £50,000 must comply with Making Tax Digital (MTD) for Income Tax. This means:

- Digital record-keeping using HMRC-compatible software (spreadsheets alone no longer qualify)

- Quarterly income and expenditure submissions to HMRC

- A points-based penalty system for late or inaccurate filings

Landlords earning £30,000–£50,000 will be brought into the regime from April 2027. The practical implication is clear: if you are still managing your books with a paper folder and an annual call to your accountant, 2026 is the year that approach becomes non-compliant.

Recommended MTD-compatible platforms include Landlord Studio, Hammock, FreeAgent, and Xero with property add-ons.

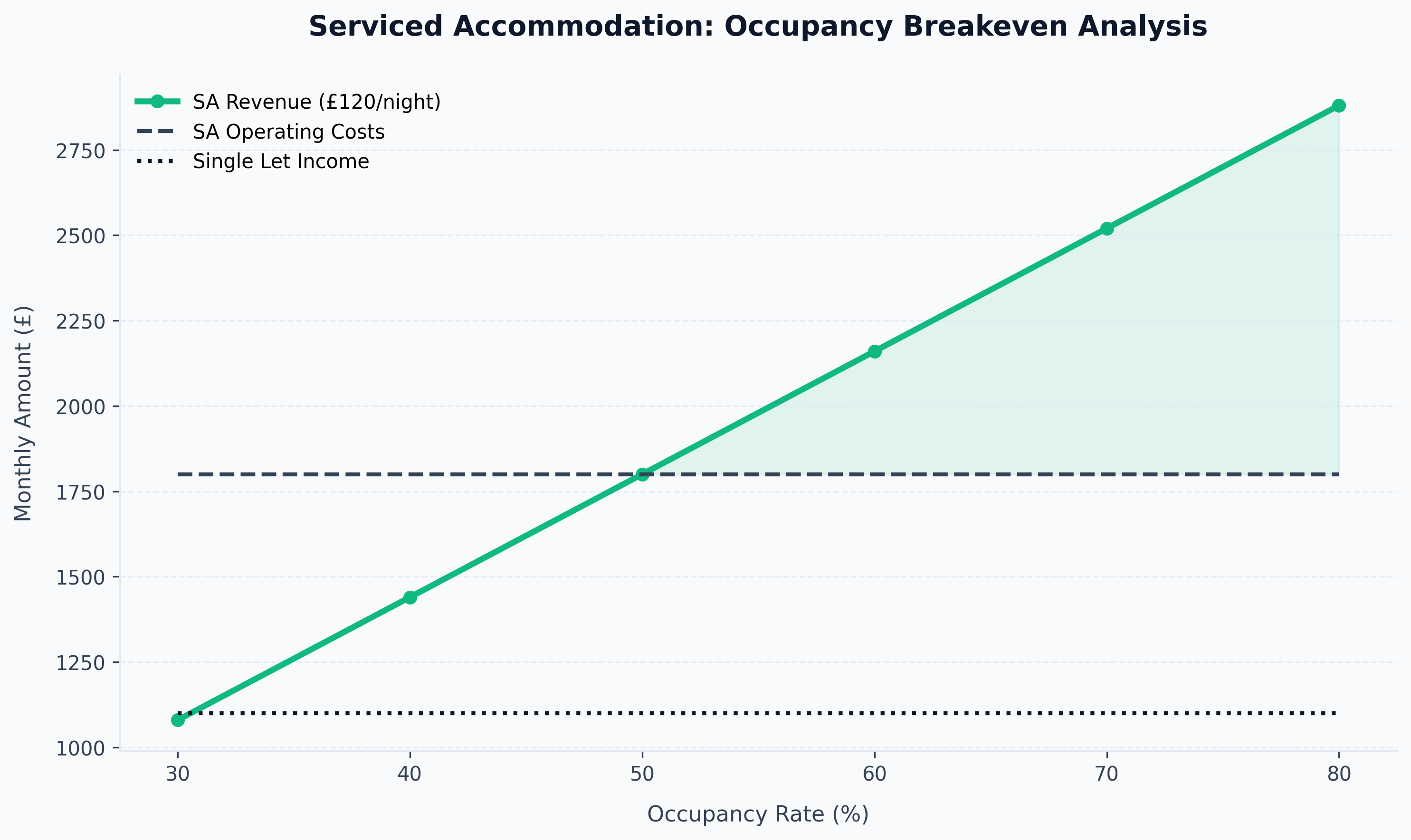

Strategy 5: Serviced Accommodation and Short-Term Lets

Serviced accommodation (SA)—renting properties on a nightly or weekly basis through platforms like Airbnb and Booking.com—offers the highest revenue potential per property but demands the most active management.

The Revenue Premium

A two-bedroom apartment in Manchester generating £950 per month as a standard let (£11,400 per year) could achieve £100–£150 per night as a serviced unit. At 70% occupancy, that translates to £25,550–£38,325 per year—a 124–236% revenue uplift.

However, the cost base is substantially higher:

| Expense | Annual Cost |

|---|---|

| Cleaning (between guests) | £3,600–£6,000 |

| Linen and consumables | £1,200–£2,400 |

| Platform commissions (15–20%) | £3,800–£7,600 |

| Utilities (landlord pays) | £2,400–£3,200 |

| Furnishing depreciation | £1,500–£2,500 |

| Management (if outsourced, 20–25%) | £5,100–£9,500 |

After costs, a well-run SA unit in a strong location can realistically deliver £8,000–£12,000 net annually—still significantly above the standard let model, but requiring either hands-on involvement or a specialist management company.

Regulatory Tightening in 2026

London's 90-day rule remains in place, limiting entire-home Airbnb lets to 90 nights per year without planning permission. Other cities, including Edinburgh, Bath, and parts of the Lake District, have introduced or are consulting on similar restrictions. Before committing to an SA strategy, investors must verify local planning requirements and registration schemes.

The Renters' Rights Act also introduces new obligations around switching from short-term to long-term lets and vice versa, requiring careful legal advice before deploying this strategy.

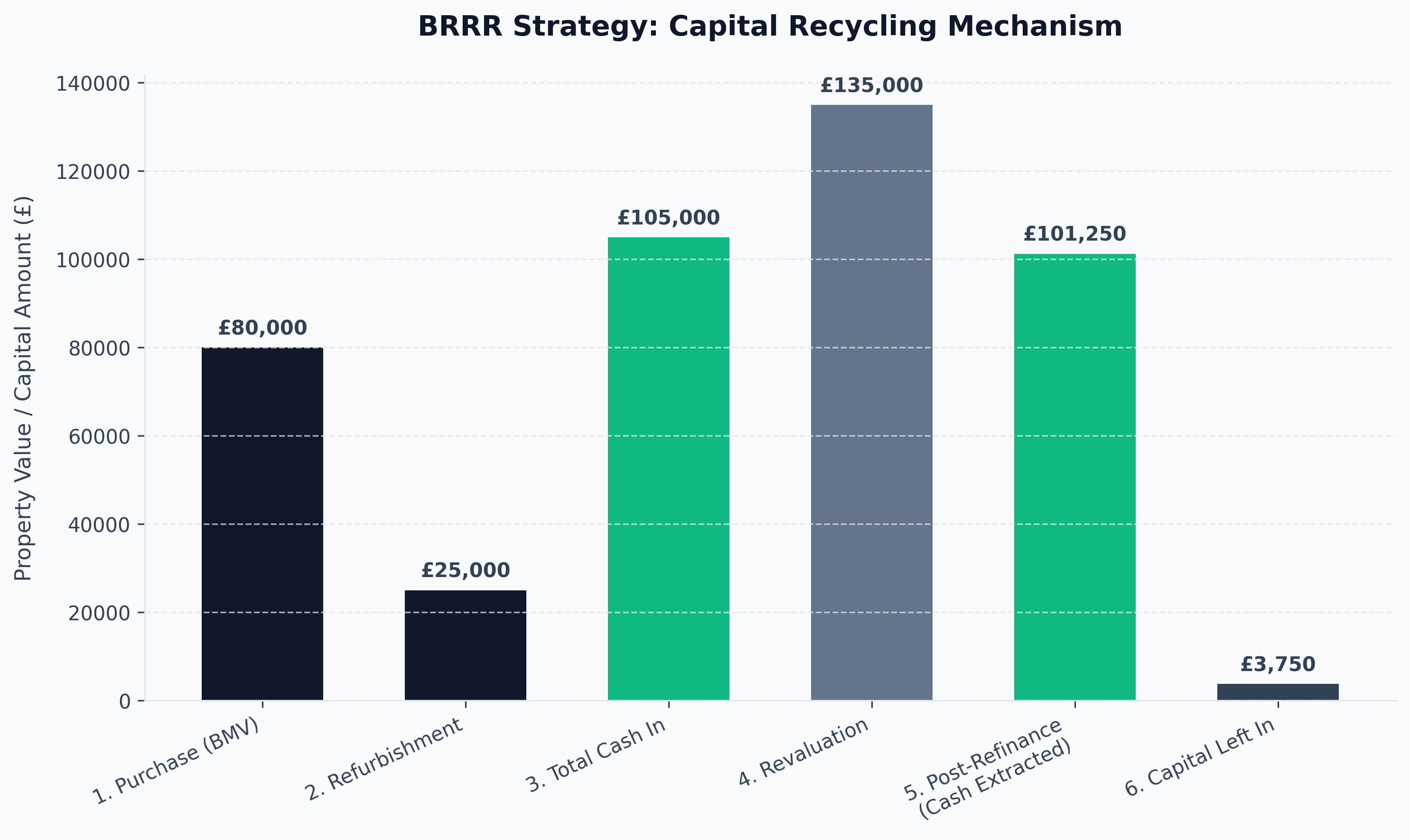

Strategy 6: The BRRR Method — Buy, Refurbish, Refinance, Rent

The BRRR strategy remains the gold standard for investors who want to recycle capital and scale a portfolio rapidly. The concept is simple: purchase a below-market-value property, refurbish it to increase its value, refinance to pull out the invested capital, and rent it for ongoing income.

How BRRR Works in 2026

Step 1 — Buy below market value (BMV). Target auction properties, repossessions, or probate sales. Expect to purchase at 20–30% below market value.

Step 2 — Refurbish. Invest £15,000–£40,000 in cosmetic and structural improvements. Focus on kitchen, bathroom, flooring, and EPC upgrades. A property bought for £80,000 and refurbished for £25,000 could revalue at £130,000–£140,000.

Step 3 — Refinance. Secure a BTL mortgage at 75% LTV on the new valuation. On a £135,000 valuation, that releases £101,250—recovering most or all of your original £105,000 investment.

Step 4 — Rent. The refurbished property now generates rental income while your original capital is freed to repeat the process.

BRRR in the 2026 Interest Rate Environment

With BTL mortgage rates stabilising at 3.75–4.75%, the BRRR model remains viable but with tighter margins than the sub-2% era. The critical success factor is the refurbishment-to-revaluation ratio: every pound spent on refurbishment must create at least £2 in added property value. Overcapitalisation—spending £40,000 on a property where the uplifted value only increases by £30,000—kills the strategy.

Investors using the BRRR method in 2026 should also factor in the 5% SDLT surcharge on additional properties, which has increased upfront costs significantly since April 2025.

Navigating the Renters' Rights Act 2026

No article on 2026 rental strategies is complete without a detailed understanding of the legislation that will reshape the landlord-tenant relationship.

Key Provisions Effective 1 May 2026

| Provision | Impact on Landlords |

|---|---|

| Abolition of Section 21 | No more "no-fault" evictions; all possession claims require Section 8 grounds |

| Periodic tenancies only | Fixed-term ASTs are replaced by rolling APTs; tenants can leave with 2 months' notice |

| Rent increases capped | One increase per year via Section 13; challengeable at tribunal if above market rate |

| Rental bidding banned | Landlords and agents cannot invite or accept bids above the advertised rent |

| Discrimination prohibited | Cannot refuse tenants on benefits or with children |

| Pets must be considered | Landlords must reasonably consider pet requests; can require pet damage insurance |

| Rent Repayment Orders | Up to 24 months' rent for non-compliance |

What This Means Practically

The extinction of Section 21 is not the catastrophe some landlord forums predict, but it does require a fundamental shift in operations:

Tenant referencing becomes mission-critical. Without the ability to end a tenancy without cause, selecting the right tenant from the outset is your single most important risk management tool. Invest in comprehensive referencing: credit checks, employment verification, landlord references, and affordability assessments.

Property condition must be impeccable. Tenants can now challenge poor conditions through the new Property Ombudsman, and substandard properties are at risk of Rent Repayment Orders. Proactive maintenance is no longer optional—it is a legal imperative.

Professional management justifies its fee. The complexity of Section 8 evictions, tribunal processes, and compliance monitoring makes professional letting agents a cost-effective insurance policy, not an indulgence.

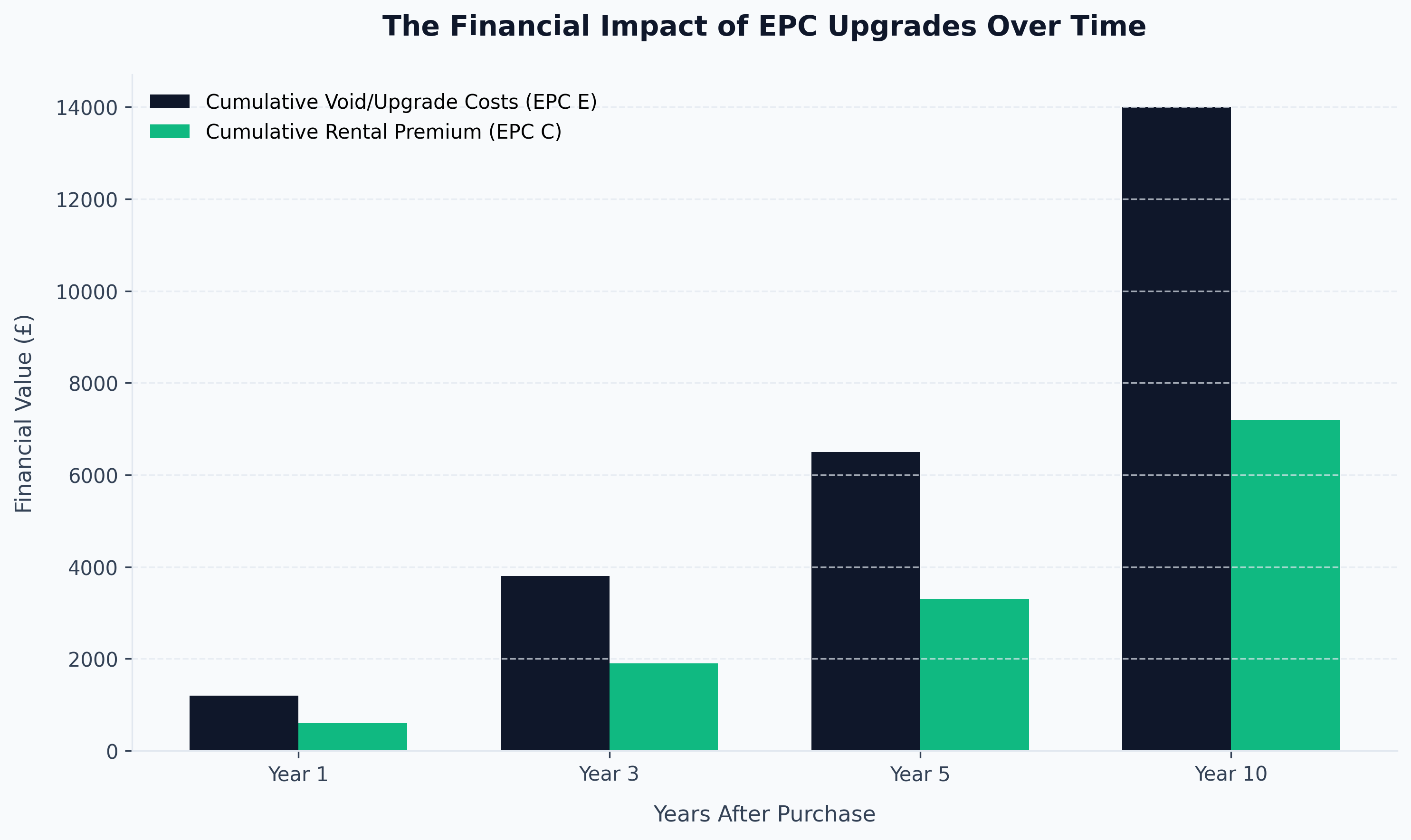

EPC Strategy: The Hidden Profit Lever

Energy efficiency is no longer just a compliance checkbox—it is a profit lever that directly impacts tenant demand, rental premiums, and future asset value.

The 2026 EPC Landscape

The government's trajectory is clear: a minimum EPC rating of C for all rental properties by 2030, with phased implementation likely hitting new tenancies as early as 2028. Properties currently rated D or below face mandatory upgrades that can cost anywhere from £5,000 for basic insulation and boiler upgrades to £15,000+ for properties requiring heat pumps, external wall insulation, or double glazing replacement.

Why Smart Investors Upgrade Now

Tenants increasingly prioritise energy efficiency because it directly reduces their monthly costs. A property upgraded from an EPC E to a C can save a tenant £500–£800 per year on energy bills—a tangible benefit that translates into stronger demand, lower void periods, and the ability to command a rental premium of 5–8%.

For investors acquiring properties in 2026, the calculation is straightforward: buy the worst EPC in the best street, upgrade it, and the combined rental premium plus capital appreciation will outstrip the retrofit cost within 3–5 years.

Financing Strategy for 2026

The mortgage market has stabilised, offering clarity for investors planning their capital deployment.

BTL Mortgage Rates and Stress Tests

Mainstream BTL mortgage rates sit between 3.75% and 4.75% in early 2026, with the Bank of England Base Rate expected to drift down further through the year. Lenders apply stress tests requiring rental income to cover mortgage payments at 125–145% of the stressed rate (typically 5.5%).

Practical implication: a property with a £150,000 mortgage at a 5.5% stress rate requires a minimum annual rent of £10,312–£11,962. On a monthly basis, that is £860–£997. Properties in low-yield areas that cannot meet this threshold will require a larger deposit (35–40% rather than 25%) to pass underwriting.

Remortgage Strategy

In a declining rate environment, proactive remortgaging is essential. Landlords sitting on fixed rates agreed in 2023–2024 at 5.5–6% should be monitoring the market for opportunities to switch to sub-4.5% products, potentially saving £150–£250 per month per property.

FAQ

Is buy-to-let still worth it in 2026? Yes, but it requires a more professional approach than ever. Investors who treat it as a business—with proper tax structuring, professional management, and data-driven location selection—continue to achieve net returns of 5–8% when combining yield with capital growth.

What is the best rental property strategy for beginners in 2026? Start with a single-let property in a high-yield regional city (Liverpool, Leeds, Nottingham). Use a limited company structure if you are a higher-rate taxpayer. Budget for a 25% deposit plus 5% SDLT surcharge plus 3% for legal and setup costs. Keep a 6-month mortgage payment reserve for voids and maintenance.

How much deposit do I need for a buy-to-let in 2026? Most lenders require a minimum 25% deposit. On a £150,000 property, that is £37,500 plus approximately £7,500 in SDLT surcharge and £3,000–£4,000 in legal, survey, and setup costs. Total upfront capital: approximately £48,000–£49,000.

Should I buy rental property through a limited company? If you are a higher-rate taxpayer (40%+) or plan to build a portfolio of 3+ properties, a limited company (SPV) structure is almost certainly more tax-efficient due to full mortgage interest deductibility against corporation tax. Consult a specialist property tax accountant before committing.

What areas have the highest rental yields in 2026? Sunderland (8.1%), Bradford (7.8%), Hull (7.5%), Liverpool (7.2%), and Manchester (6.8%) lead the current yield tables. However, yield must be balanced against tenant demand quality, capital growth prospects, and local regulatory environment.

Actionable Next Steps

Run your numbers with 2026 data. Use current mortgage rates (3.75–4.75%), the 5% SDLT surcharge, and realistic maintenance budgets (10–15% of gross rent) to stress-test any potential acquisition. If the deal does not cash flow positive at a 5.5% stress rate, walk away.

Speak to a specialist property tax accountant. The difference between personal and limited company ownership can be worth thousands per property per year. Do not rely on generic advice—get a personalised analysis based on your income bracket and portfolio size.

Start MTD compliance now. Even if you fall below the £50,000 threshold for April 2026, you will likely be captured by April 2027 at £30,000. Set up compliant software today rather than scrambling under deadline pressure.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →