Attempting to scale a high-yield property portfolio in the UK while relying on amateur "High Street" financing is a mathematical impossibility in 2026. Standard retail Buy-to-Let mortgages are fundamentally incapable of processing the complex commercial velocity required to operate a profitable 6-bed House in Multiple Occupation (HMO).

When amateur investors transition from single-family dwellings to large-scale HMO conversions, they hit a brutal reality wall: the underwriting mechanics completely change. You are no longer purchasing a residential house; you are acquiring a heavily regulated, cash-flowing commercial business that happens to exist within four brick walls.

In an environment of persistently tight monetary policy, high bridging debt costs, and extreme Prudential Regulation Authority (PRA) oversight, understanding how to finance Houses in Multiple Occupation UK is the only metric separating institutional-grade syndicates from insolvent rookies.

This comprehensive guide will deconstruct the exact 2026 commercial matrices used by elite property operators to secure specialist HMO term loans, utilize violent short-term bridging capital, navigate "Sui Generis" commercial valuations, and engineer algorithmic Interest Coverage Ratio (ICR) compliance.

1. The Fundamental Shift: Residential vs Commercial Funding

The single most disastrous assumption an investor can make is applying residential underwriting logic to an HMO asset.

Exhausting the Retail Horizon

If you purchase a standard 3-bedroom semi-detached property and rent it out to a single family, a mainstream high-street bank applies a highly rigid, algorithmic stress test. They look at your personal income, the historic average rent for similar houses on that street, and grant a simple term loan wrapped in heavy Section 24 tax penalties.

High-street lenders fundamentally abhor complexity. An HMO introduces multiple ASTs (Assured Shorthold Tenancies), transient tenant turnover, heightened legislative compliance, and immense local authority licensing (Mandatory, Additional, and Selective). Consequently, the moment you instruct your solicitor that the intended use is a House in Multiple Occupation, standard retail lenders entirely withdraw their capital.

Accessing Specialist Institutional Capital

To finance an HMO, you must pivot away from the High Street and interface with "Challenger Banks," Specialist Buy-to-Let lenders, and boutique Commercial Finance Houses. These institutions do not fear complexity; they aggressively price it.

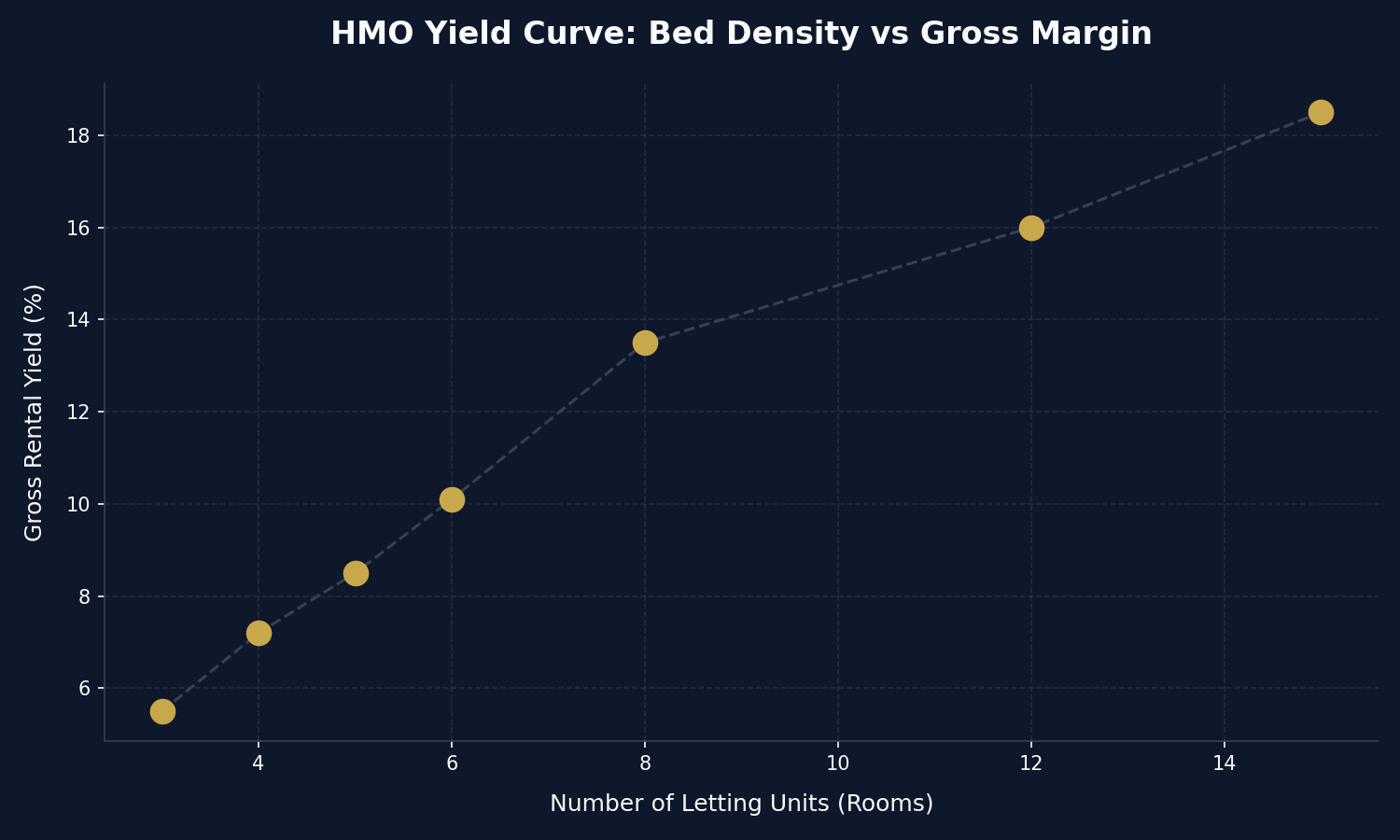

These specialist lenders understand that a £200,000 asset generating £3,000 per month across six rooms is a significantly stronger covenant than the exact same £200,000 asset generating £900 per month from a single family. They utilize bespoke underwriting algorithms to underwrite the business of the HMO, meaning you are judged on the velocity of your commercial yield, not your personal PAYE salary.

2. The Algorithmic Guardrail: Master the ICR Stress Test

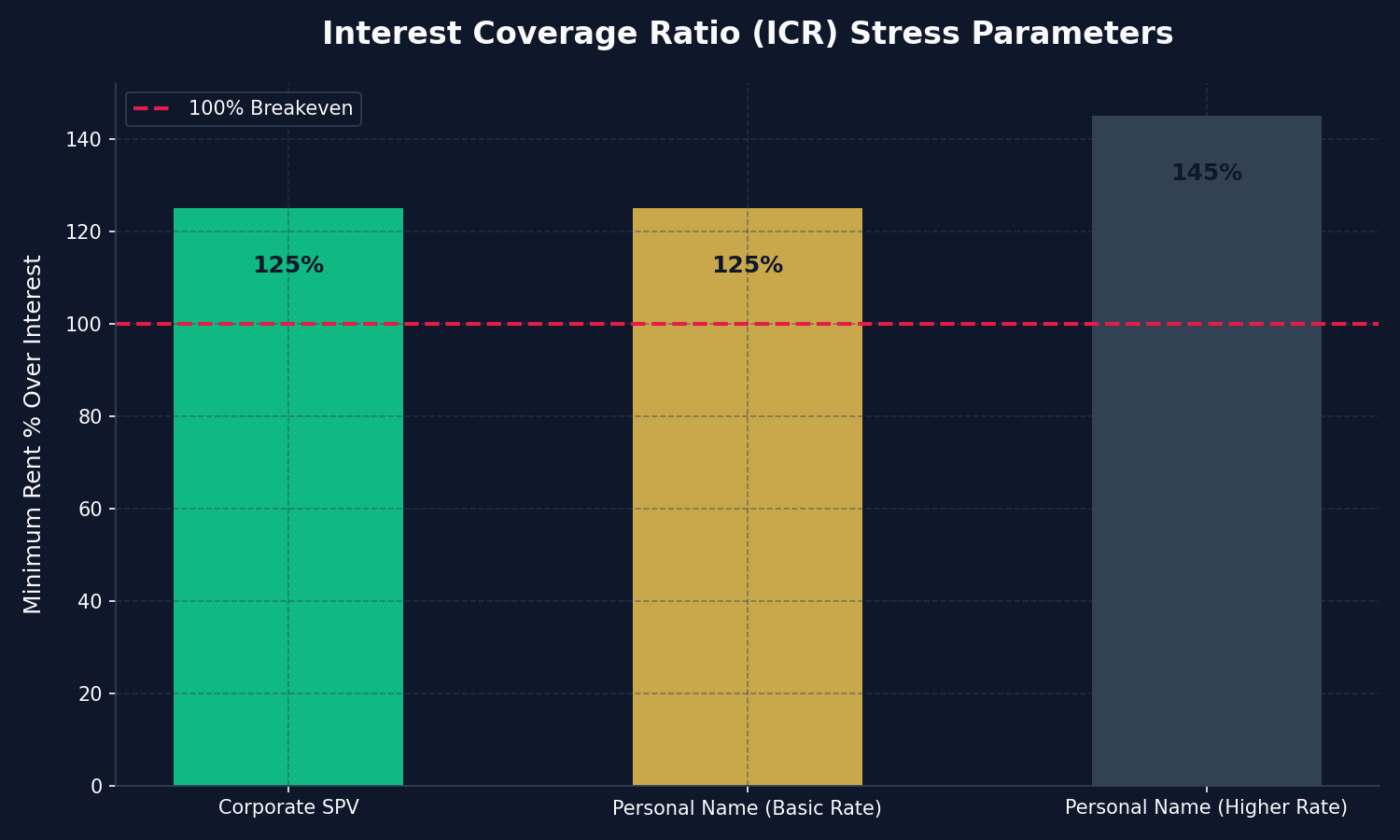

In 2026, you do not simply ask a bank for money; you must mathematically prove your asset can survive a macroeconomic crisis. The weapon the banks use to ensure this survival is the Interest Coverage Ratio (ICR).

The ICR calculates exactly how many times your gross rental income covers the theoretical mortgage interest payment. Failing the ICR test means zero capital deployment, regardless of how much equity you hold.

The Personal Name Penalty (145% Stress)

If you attempt to secure an HMO mortgage in your personal name, the bank acknowledges that the HMRC will heavily tax your gross income under Section 24 (preventing you from deducting the mortgage interest as an operating expense). Because your tax burden is artificially inflated, the bank requires an enormous safety buffer to ensure you don't default. They apply a staggering 145% ICR stress test, usually pegged at a fictitious 5.5% or 6% interest rate.

If the stress test demands your rent covers the interest 1.45 times over, your maximum loan size is radically compressed, leaving tens of thousands of pounds as "dead equity" trapped in the asset.

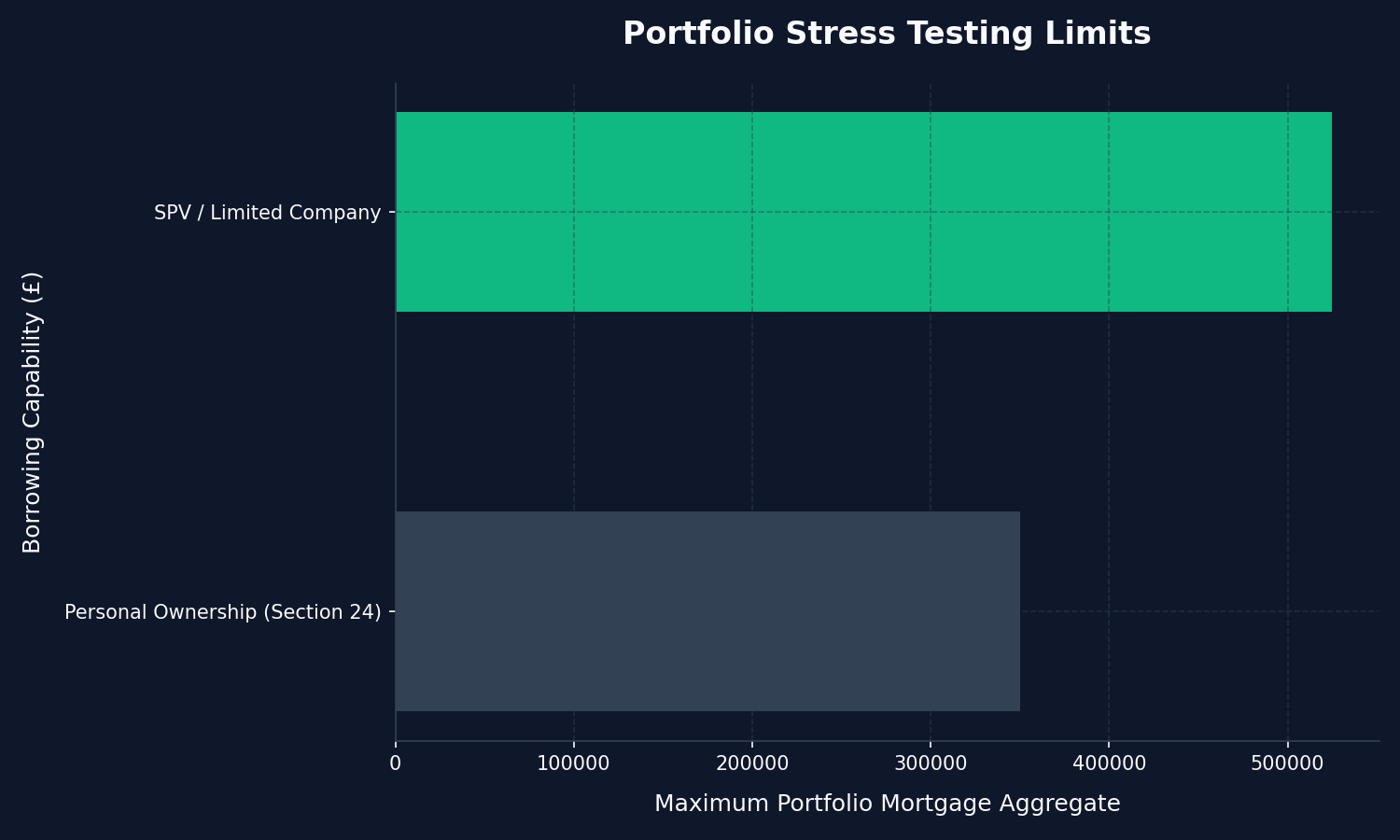

SPV Dominance (125% Stress)

This is why professional syndicates never operate in personal names. By acquiring the HMO via a Limited Company Special Purpose Vehicle (SPV), the transaction is classed as a standard corporate structure paying absolute Corporation Tax. Mortgage interest is recognized as a 100% deductible business expense. Because the tax environment is fundamentally safer, institutional lenders drop the ICR stress test down to 125%.

That 20% differential allows you to dramatically increase the commercial leverage against the asset, releasing significantly more tax-free liquid capital back to your balance sheet.

3. The 2026 Valuation Arbitrage: "Bricks" vs "Yield"

When extracting capital from an HMO (specifically during a BRRRR Strategy execution), the single most critical variable is the final valuation assigned by the bank’s surveyor. If you do not understand how an HMO is valued, you cannot calculate how to finance Houses in Multiple Occupation UK.

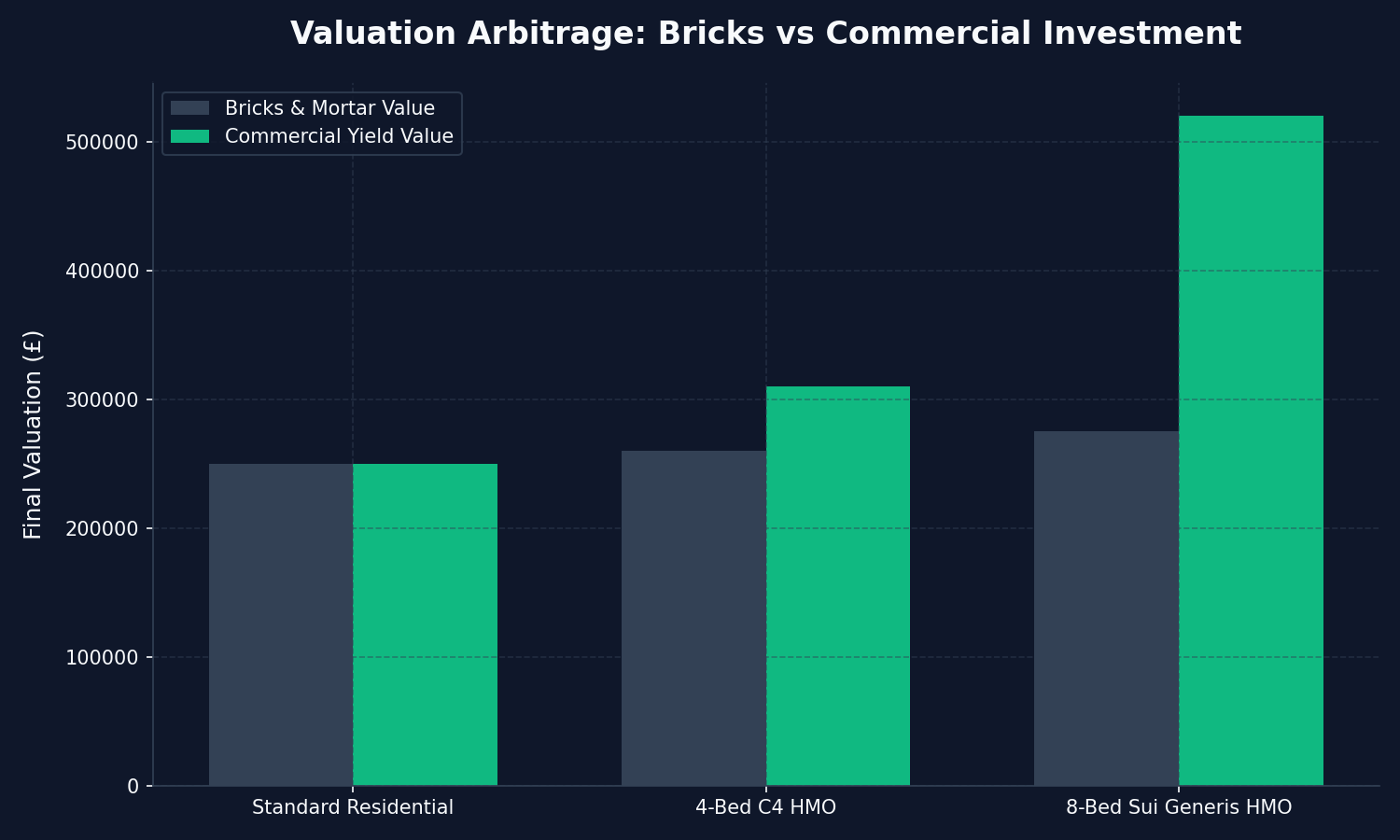

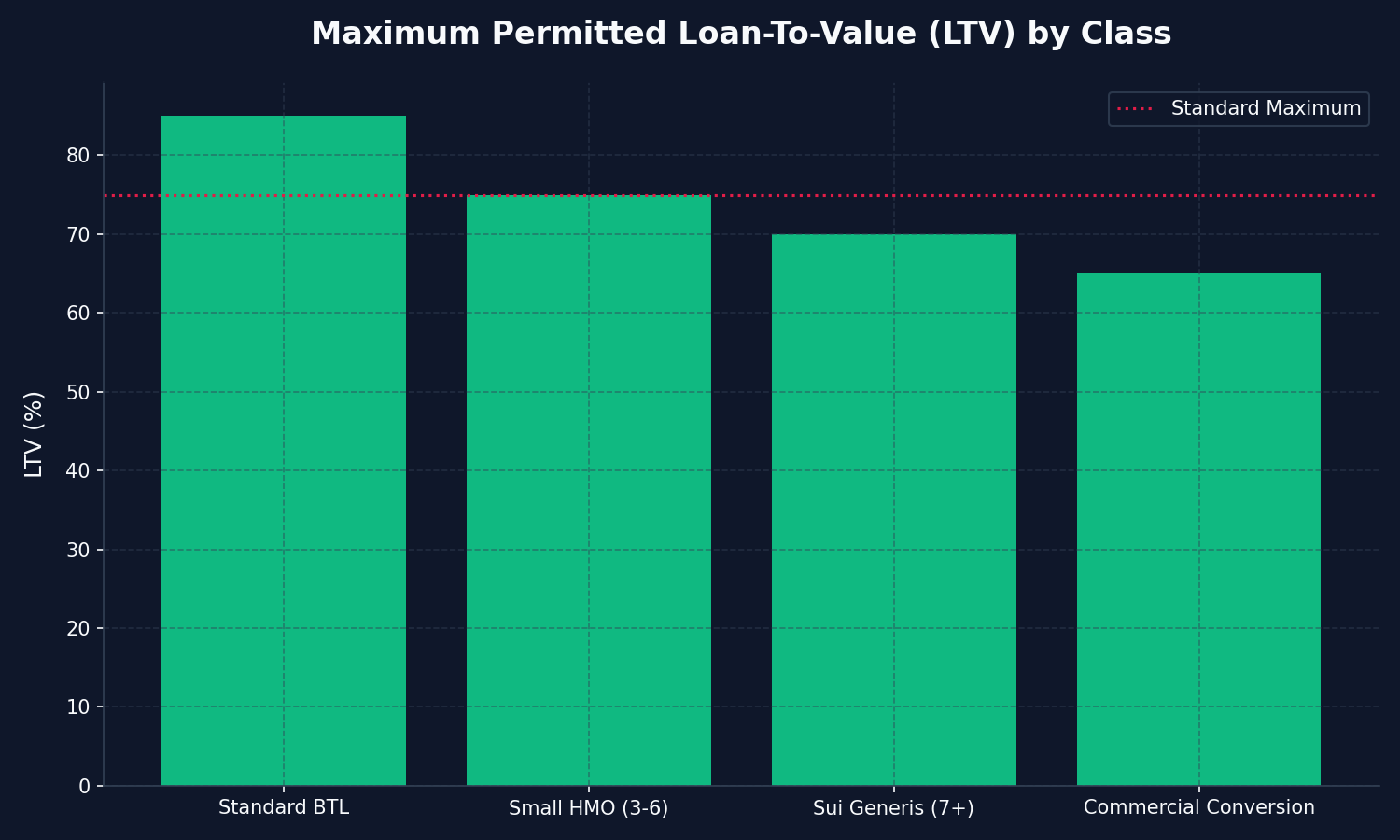

Standard "Bricks and Mortar" Valuation (Small HMOs)

If you are financing a highly standard 3-to-4 bed HMO falling under 'C4' use-class, the surveyor will typically execute a "Bricks and Mortar" valuation. This is deeply pessimistic. The surveyor ignores the fact that your 4 rooms generate £2,200 a month. Instead, they look at what a standard family would pay for the house if it were stripped of its HMO status. If the family house next door sold for £150,000, your HMO is valued at £150,000.

The Ultimate Goal: "Commercial Investment" Valuation (Large HMOs)

For professional investors constructing large-scale, high-yield assets (typically 7+ bedrooms or bespoke "Sui Generis" properties), standard bricks and mortar valuations break down completely. A heavily structured 8-bed co-living space cannot physically be used as a standard family home.

In this scenario, specialist lenders utilize a Commercial Investment Valuation. The surveyor values the property purely as a cash-generating commercial business, entirely disconnected from the residential houses on the same street.

They calculate the final GDV (Gross Development Value) using a Yield Multiplier.

- Gross Annual Rent: £50,000

- Local Commercial Yield Expectation: 10%

- Commercial Valuation: £500,000

(Even if the physical residential street ceiling is only £250,000, the commercial yield forcibly drives the valuation to half a million pounds. This is how multi-millionaires are minted via valuation arbitrage).

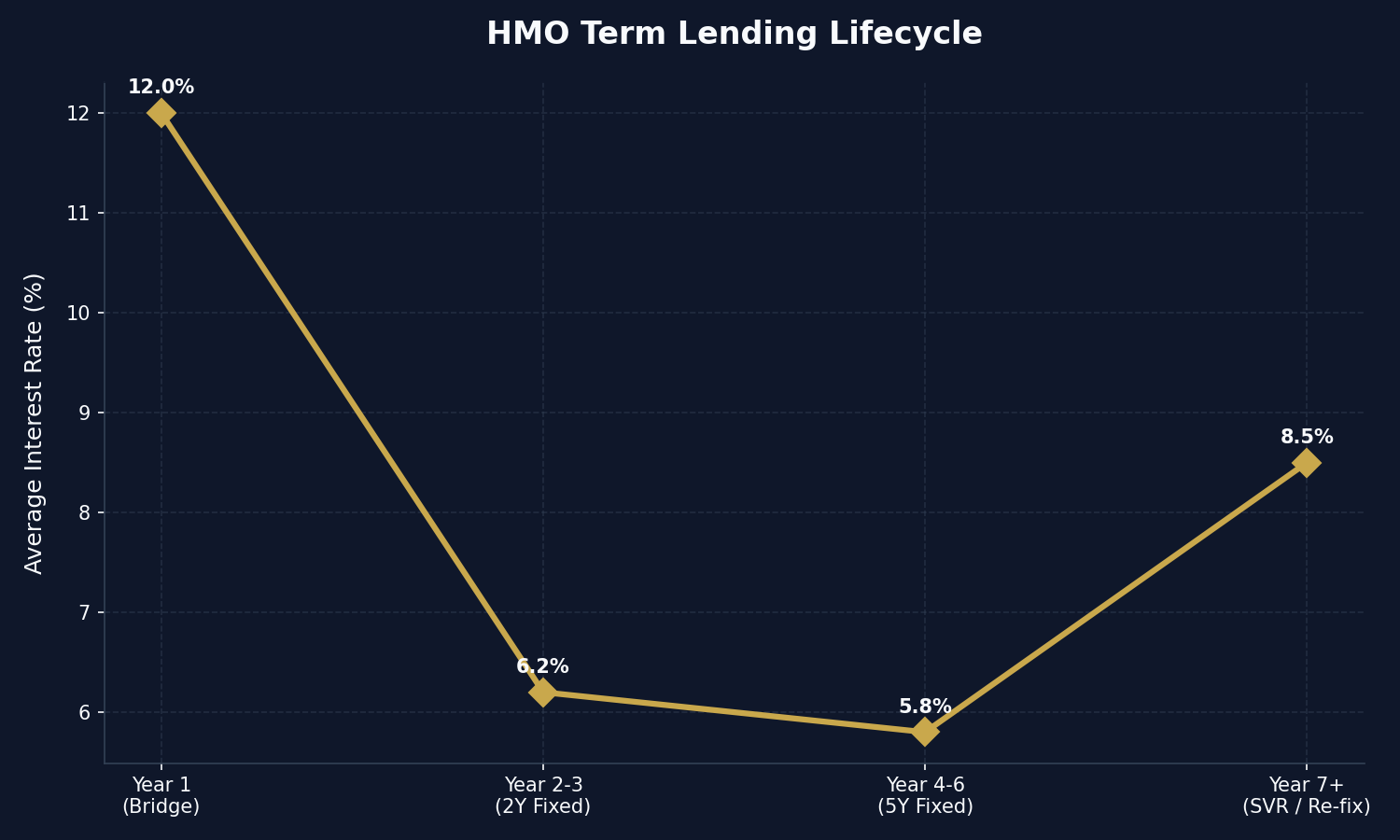

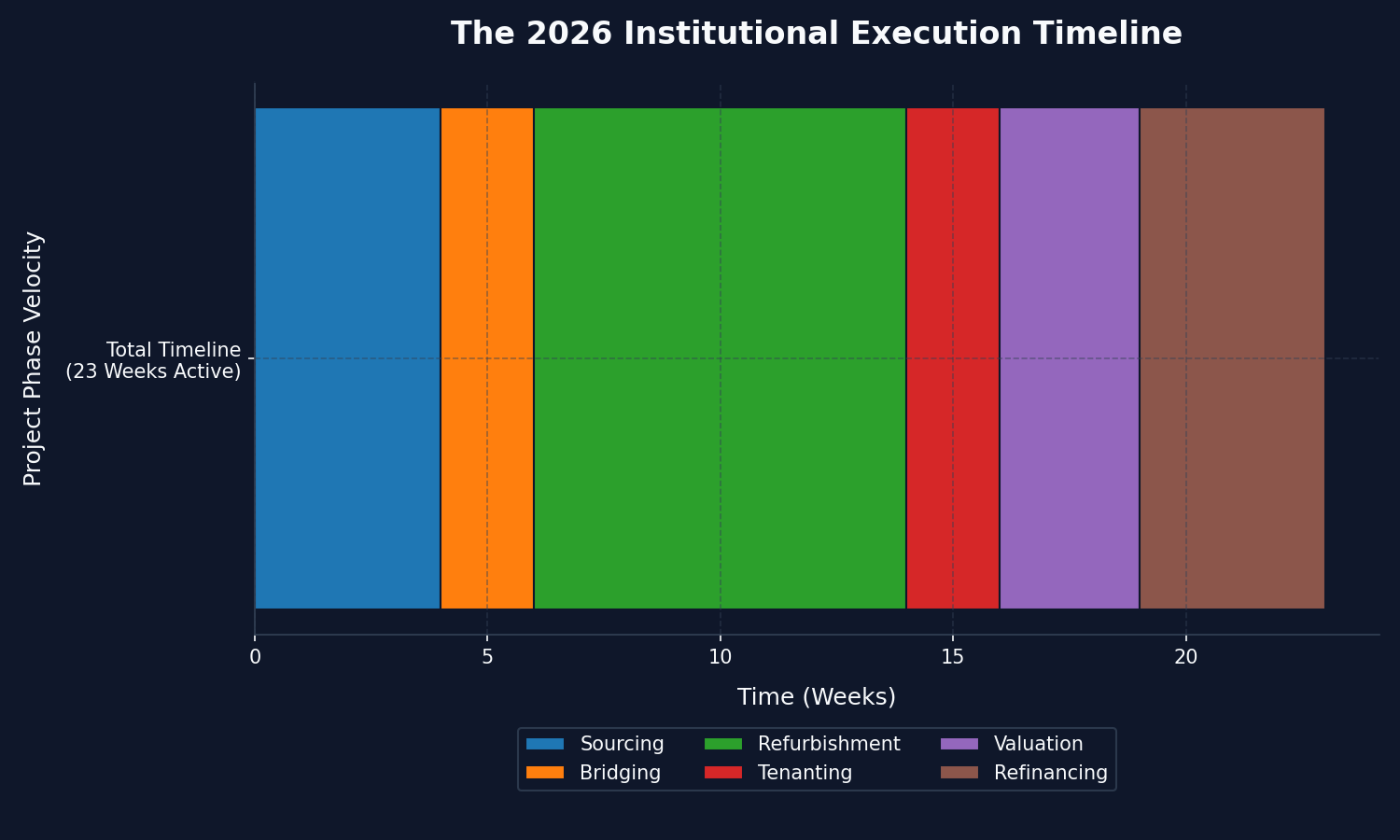

4. Acquiring the Asset: The Velocity of Bridging Finance

You cannot purchase a dilapidated, un-mortgageable house at an auction hoping to use a 5-year BTL mortgage. Standard lenders demand the property is fundamentally habitable (functional kitchen, working bathroom) on Day 1.

Therefore, the acquisition phase of an HMO project requires aggressive, short-term liquidity. This is the domain of Bridging Finance.

The Anatomy of an HMO Bridge

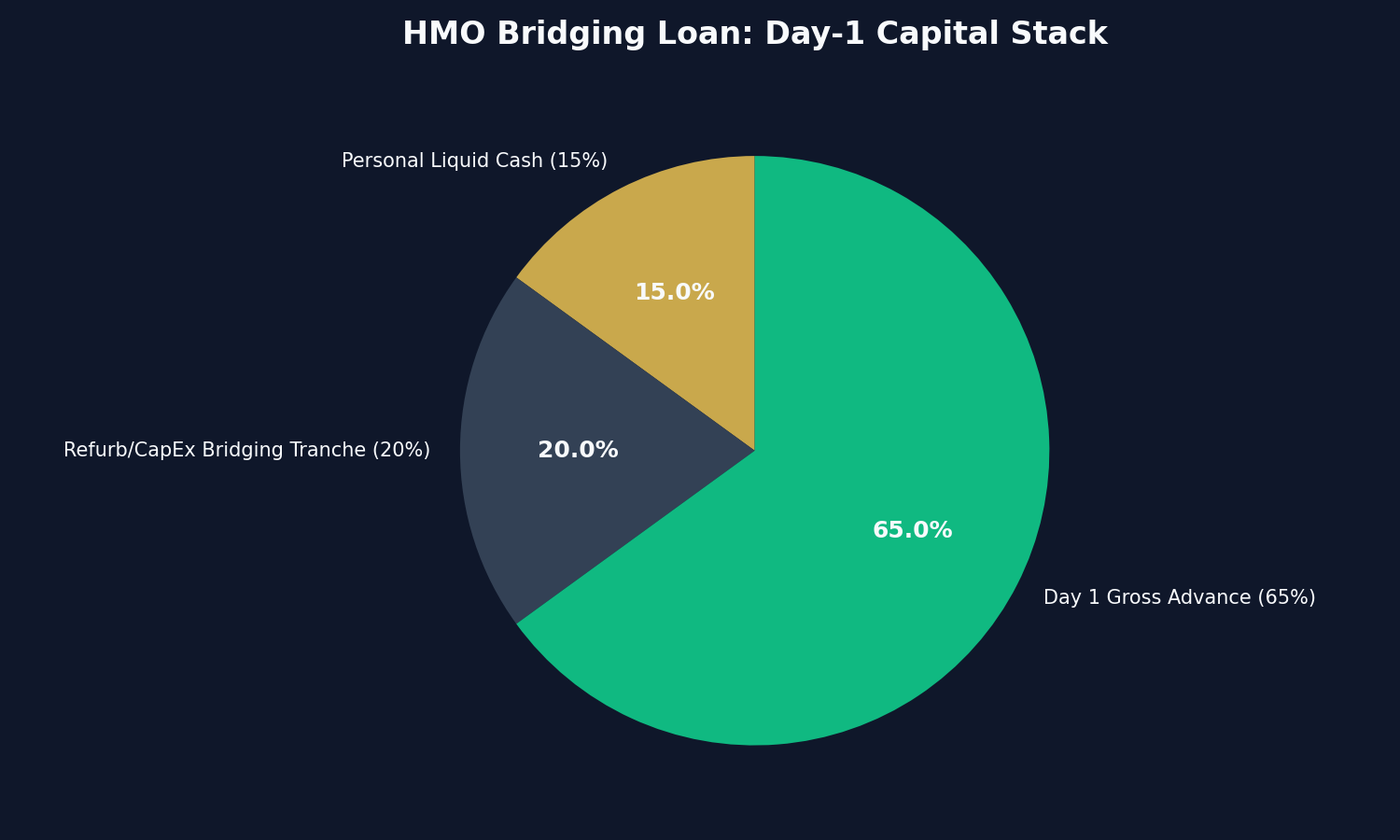

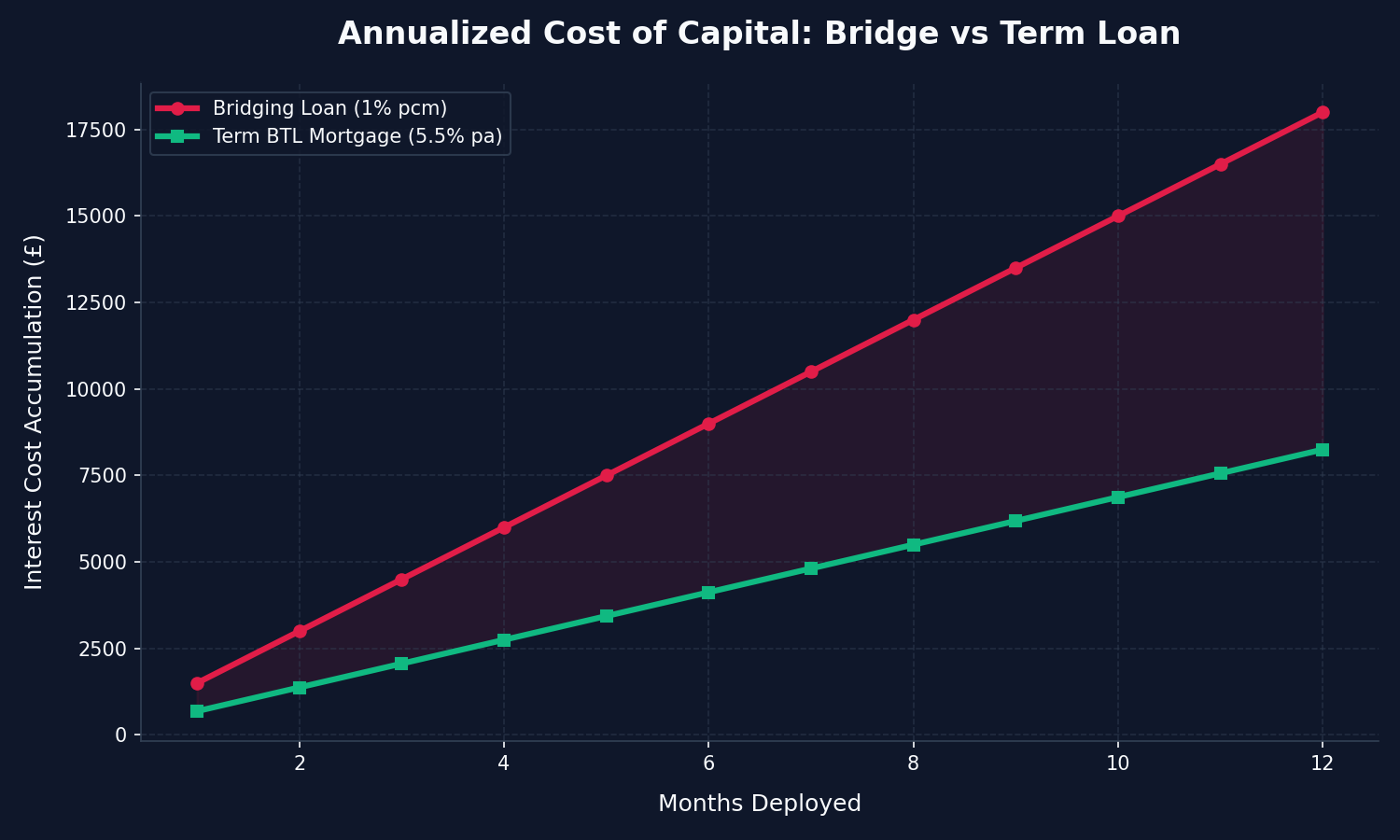

A bridging loan is a violent, highly expensive (approx 1% per month), short-term (6-18 months) debt instrument utilized purely for speed and acquisition leverage. Professional operators use bridging finance to secure 75% LTV against the distressed purchase price of the asset. Because it is an unregulated commercial loan, bridging lenders do not care if the property lacks an EPC or a kitchen; they only care about your "Exit Strategy."

Your exit strategy is strictly: Refurbish the asset, secure the expensive HMO license, tenant it at high yields, and refinance onto a long-term, cheaper specialist HMO mortgage to pay off the bridging debt.

The Retained Interest Trap

Amateurs fail to calculate the devastating holding costs of bridging finance. If you borrow £200,000 at 1%, you bleed £2,000 every single month. To protect themselves, bridging lenders "retain" or "roll up" the interest into the loan facility upfront. You do not pay the £2,000 a month out of your own pocket; it is deducted from the gross loan advance.

You must act with extreme velocity. If your builder delays the structural knock-throughs by three months, your bridging interest aggressively annihilates your net capital margin. In 2026, robust property flipping calculators and brutal project management are not suggestions; they are prerequisites for bridging survival.

5. Development Finance: Heavy Structural Conversions

If your HMO project requires significant structural intervention—such as massive basement excavations, two-storey wrap-around extensions, or converting a sprawling, derelict commercial pub into a 15-bed mega-HMO—standard bridging finance is mathematically inefficient.

Heavy structural projects utilize Development Finance.

Tranches and Milestones

Unlike a bridging loan that hands you a static lump sum on day one, Development Finance operates dynamically. The lender advances a percentage of the purchase price on Day 1. They then hold the hundreds of thousands of pounds required for the refurbishment in a restricted facility, releasing it to you in "Tranches" (installments) only as you hit specific structural milestones.

Example: You personally fund the heavy foundation work. An independent surveyor visits the site, confirms the foundations are structurally sound, and approves the "drawdown." The lender then wires you the funds to reimburse your outlay and immediately commence the brickwork.

This completely neutralizes the lender's risk while providing you with institutional-grade capital to fund massive, high-GDV commercial HMO projects that physically could not be executed using personal savings.

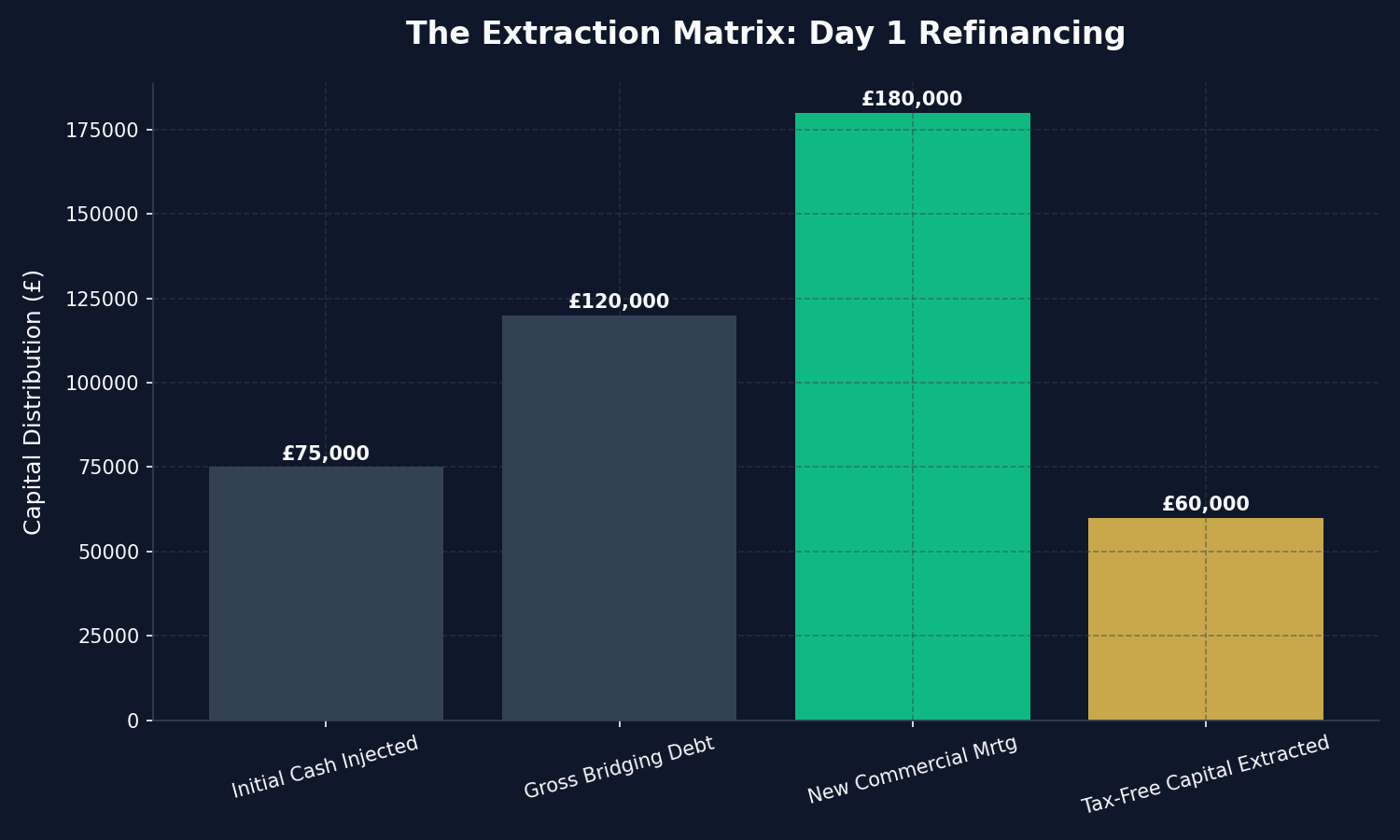

6. The "Six-Month Rule" & Day-1 Refinancing (The Golden Key)

Historically, attempting to finance an HMO quickly was blocked by a catastrophic retail banking regulation known as "The Six-Month Rule."

High-street lenders rigidly enforced a strict anti-money laundering and anti-fraud protocol: If you purchased a property using bridging debt or cash, you were legally prohibited from refinancing it for a fresh commercial mortgage until you had owned the asset for a minimum of six months.

If you aggressively completed your HMO refurbishment in 8 weeks, you were forced to sit paralyzed for 4 additional months, continually paying thousands of pounds in punitive bridging interest while you waited for month 6 to arrive.

The 2026 Day-1 Reflex

Elite commercial brokers explicitly bypass the six-month rule. By aggressively targeting specialized "Challenger Banks" and institutional HMO lenders, professionals can execute Day-1 Refinancing.

The moment the building control signs off the final electrics and the ASTs (rental contracts) are executed with the tenants, the broker triggers the long-term refinance. The bridging debt is instantly cleared, the capital is immediately extracted, and the asset is transitioned onto a stable 5-year fixed rate. Eliminating 4 months of dead holding costs is one of the most powerful arbitrage techniques in modern property scaling.

7. Licensing and Lender Compliance: The Non-Negotiable Barrier

You cannot answer how to finance Houses in Multiple Occupation UK without fundamentally addressing local authority licensing. Lenders will not deploy capital into an illegal asset.

Mandatory, Additional, and Selective Licensing

In 2026, the legislative matrix surrounding HMOs is intensely localized.

- Mandatory Licensing: Governed by national law, any property housing 5 or more unrelated occupants sharing amenities requires a mandatory HMO license.

- Additional Licensing: Aggressive local councils can enforce additional licensing on smaller HMOs (e.g., 3-4 occupants) in specific postcodes to throttle development.

- Article 4 Directions: A brutal planning restriction preventing the conversion of a standard family home (C3) into a small HMO (C4) without explicit, full planning permission.

A specialist HMO lender’s underwriter will aggressively audit your compliance. Before the surveyor is even instructed, the lender will demand absolute proof that the property resides in a zone permitting HMO conversion, or that you have already secured the requisite planning permission and licensing status. Attempting to bypass local authority law results in an instant mortgage rejection.

8. Portfolio Financing: Scaling Beyond 4 Assets

A defining characteristic of the 2026 UK market is the aggressive consolidation of individual landlords into professional portfolio operators. The Prudential Regulation Authority (PRA) fundamentally rewrote the rules for any investor controlling more than 4 mortgaged properties.

The Portfolio Landlord Stress Test

If you are refinancing your 5th property (perhaps a new 6-bed HMO), the lender will not just underwrite the new asset; they apply a brutal forensic audit across your entire existing portfolio.

If you own three low-yielding, legacy single-family buy-to-lets in London that fail the 125% ICR stress test because interest rates spiked, the lender will instantly reject the mortgage application for your brand-new, highly profitable Northern HMO. The weakness of your legacy assets infects the financing potential of your new acquisitions.

This forces professional syndicates to aggressively prune underperforming assets, maintaining a portfolio-wide LTV below 65% and explicitly ensuring every single property in the corporate structure maintains a ruthless ICR surplus.

9. Leveraging the Elite: The Role of the Specialist Commercial Broker

Unlike standard buy-to-let yield metrics, where you can utilize highly automated online comparison sites to secure a 2-year fixed product, HMO financing is inherently relationship-driven.

The finest institutional HMO products do not exist on public websites. They are routed exclusively through highly vetted, FCA-regulated specialist commercial brokers.

A specialist broker does not simply find a rate; they actively engineer the transaction:

- They instantly identify which lender’s surveyor is most likely to grant a Commercial Valuation rather than a Bricks & Mortar valuation.

- They possess direct telephone access to the bank's Senior Underwriter to manually explain the complexity of a massive 12-bed Sui Generis conversion.

- They structure the extraction velocity, pairing the heavy 75% Bridging Loan on day one directly with the guaranteed Challenger Bank Refinance on month four.

Attempting to execute large-scale HMO financing without an elite commercial broker acting as the interface between you and institutional capital is mathematically inefficient and commercially reckless.

Conclusion: Debt is Your Primary Weapon

Understanding how to finance Houses in Multiple Occupation UK is not an administrative afterthought; it is the absolute core foundation of the investment. An HMO is fundamentally a complex financial derivative leveraging physical bricks to extract high-yield corporate spread.

In the highly regulated 2026 environment, amateurs who rely on personal names, standard retail lenders, and generic high-street advice will find their capital violently trapped behind 145% ICR stress tests and six-month artificial waiting periods.

To dominate, you must operate like an institutional syndicate. Exploit Special Purpose Vehicles. Demand Commercial Valuations. Leverage specialist bridging debt for rapid distressed acquisition, and utilize elite brokers to execute Day-1 refinancing, achieving the ultimate goal of the property investor: absolute and total extraction of your liquid capital, ready to deploy into the next commercial victory.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →