2026 UK Property Flip ROI Calculator

Dynamically model your MAO (Max Allowable Offer), capitalized holding attrition, and absolute Project ROI based on live bridging structures.

Asset Variables

Time & Exit Metrics

Mathematical Diagnostic

Entering the UK real estate market intending to “buy, refurbish, and sell” without absolute mathematical clarity is professional suicide. Countless investors, blinded by daytime television aesthetics, aggressively hunt down run-down properties, mentally calculate a vague renovation budget, and assume market inflation will cover the difference. This approach is no longer functional.

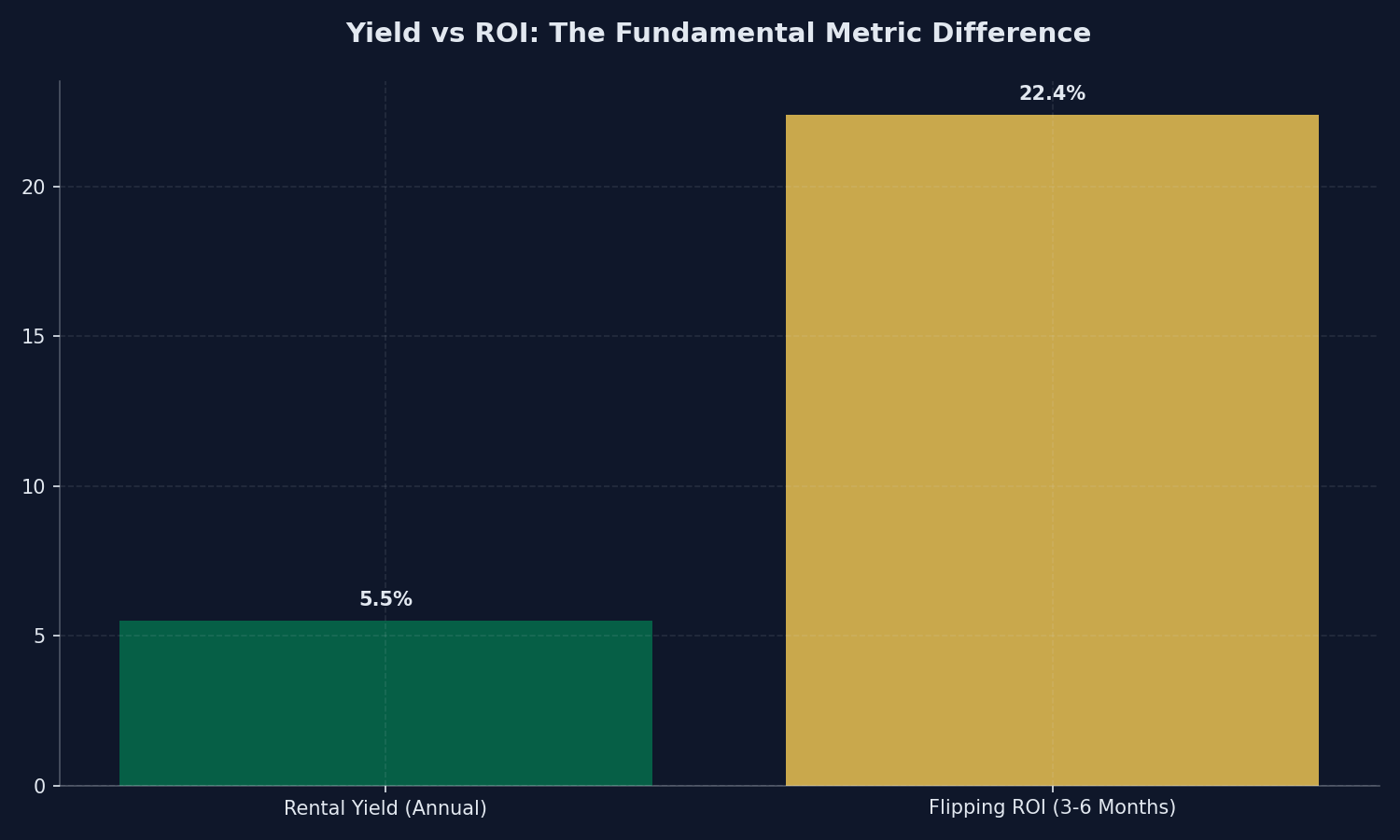

In 2026, the margin for error in the UK flipping sector has been almost entirely eradicated. With persistently high bridging finance rates, volatile raw material costs, and punitive Stamp Duty Land Tax (SDLT) surcharges, success is mathematically manufactured. A critical issue, however, is that many novice investors fundamentally confuse the metrics they are supposed to be measuring. They eagerly search for a property flipping yield calculator uk, failing to realise that "yield" is the entirely wrong metric for a flip.

This comprehensive guide will deconstruct the vast difference between Rental Yield and Flipping ROI, expose the hidden variables that destroy flipping margins, and explain how rigorous data-driven modeling—incorporating the legendary “70% Rule”—separates the professional flippers from the casualties.

1. The Definitive Distinction: Yield vs. Return on Investment (ROI)

The first step in achieving commercial success is understanding your metrics. Real estate vocabulary is often highly abused by inexperienced agents or course-sellers who conflate terminology to make bad deals appear lucrative.

The Misunderstanding of "Yield"

Put simply, yield refers to the annual recurring income generated by an asset, expressed as a percentage of its value. If you buy a house for £100,000 and the tenant pays £5,000 a year in rent, your Gross Yield is 5%. It is a measurement of passive cash flow velocity over time.

Therefore, a "property flipping yield calculator" is an oxymoron. When you are flipping a house, there is no tenant. There is no annual recurring income. You are not holding the asset long enough to generate an annualized income stream. If you are calculating yield on a flip, you are inadvertently underwriting a "Buy-to-Let" or BRRR property strategy, not a straightforward buy-and-sell flip.

The True Measurement: Project ROI and Absolute Profit

When flipping property, your only concern is capital growth and capital extraction. You are manufacturing equity. The metrics you must obsess over are:

- Net Profit: The absolute monetary sum remaining after every single expense is deducted from the final sale price.

- Project ROI (Return on Investment): Your net profit expressed as a percentage of the total cash you physically deployed into the project.

- Annualized ROI: Your Project ROI adjusted for the time the capital was deployed. Making a 20% return in three months is infinitely superior to making a 20% return in twelve months.

2. The Core Formula for Flipping Profitability

Before we integrate complex data visualization, we must outline the foundational calculation that governs every single flip in the UK market.

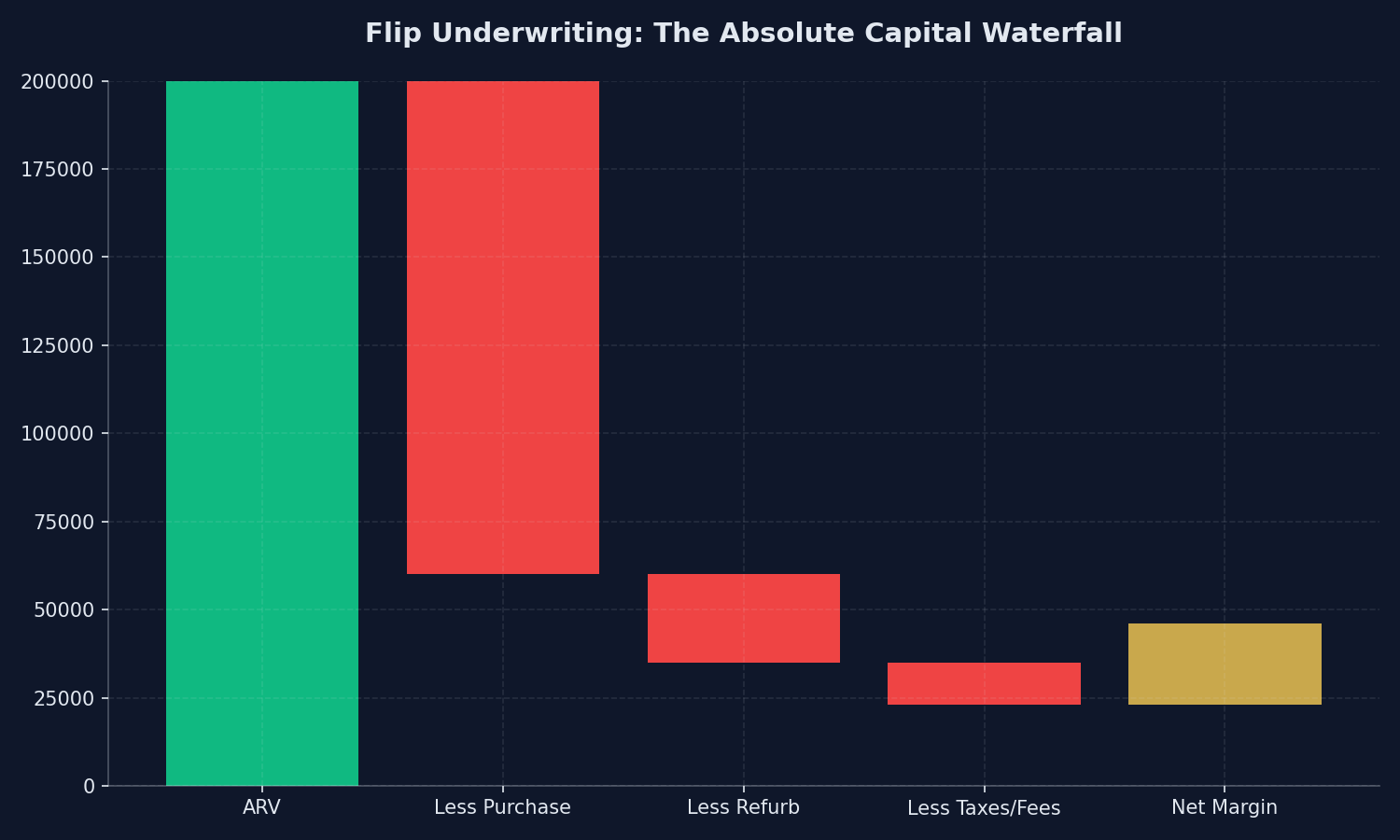

Gross Development Value (GDV) / After Repair Value (ARV) Minus Total Acquisition Costs Minus Total Refurbishment Costs Minus Total Holding Costs Minus Cost of Sale = Net Profit

Let us break these five pillars down into granular detail, exposing exactly where amateur investors hemorrhage their capital.

3. Pillar One: Accurately Projecting the GDV

Your Gross Development Value (GDV) or After Repair Value (ARV) is the estimated total market value of the property once it has been fully renovated to a high standard and put back on the open market.

This is the very first number you must calculate, and it is where the most devastating mistakes occur. An amateur will look at a dilapidated 3-bedroom semi-detached house on a street where pristine 3-bedroom semi-detached houses sell for £250,000, and assume their ARV is £275,000 simply because they plan on installing a very expensive kitchen.

The Market Dictionary: The market—dictated by local surveyors and comparable mortgage valuations—cares very little about the specific brand of your kitchen worktops. If the absolute ceiling price for a 3-bedroom semi on that specific street is £250,000, your property will likely be down-valued by the buyer's mortgage lender if you attempt to push it to £275,000, regardless of how beautiful the interior is.

A professional uses a true ROI property calculator strictly anchored to localized, data-driven "sold prices" from the Land Registry over the last three months, applying brutal conservatism to their ARV assumptions.

4. Pillar Two: The Weight of Acquisition Costs

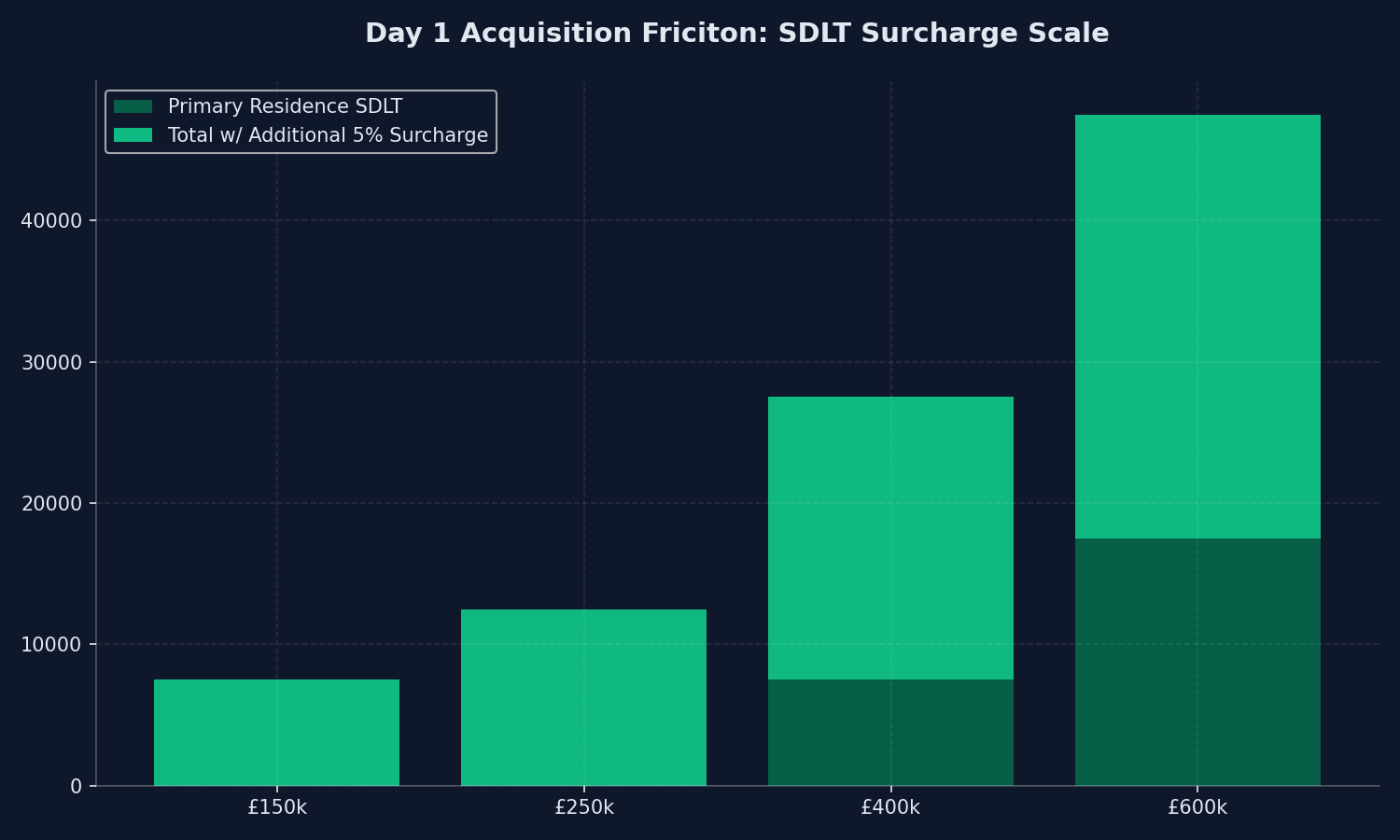

Acquiring the property is significantly more expensive than merely finding the deposit. In the 2026 tax environment, acquisition friction is one of the heaviest variables compressing your overall property flipping margin.

- Stamp Duty Land Tax (SDLT): If you are flipping properties, you likely already own your own residential home (or conduct the flip via a Limited Company). This means you are hit with the punitive 5% SDLT surcharge on additional properties from day one. On a £200,000 purchase, you immediately lose £10,000 to the Treasury before you even pick up a paintbrush.

- Legal Fees and Conveyancing: Buying an un-mortgageable property via auction or utilizing bridging finance requires specialized, rapid-execution conveyancing. These solicitors charge heavily, easily running upwards of £1,500 to £2,500.

- Sourcing Fees: If you utilized a property sourcing agency to find the distressed asset, you are paying an upfront finder’s fee of £2,000 to £5,000.

- Survey Fees: Comprehensive structural and damp surveys are mandatory when flipping distressed assets.

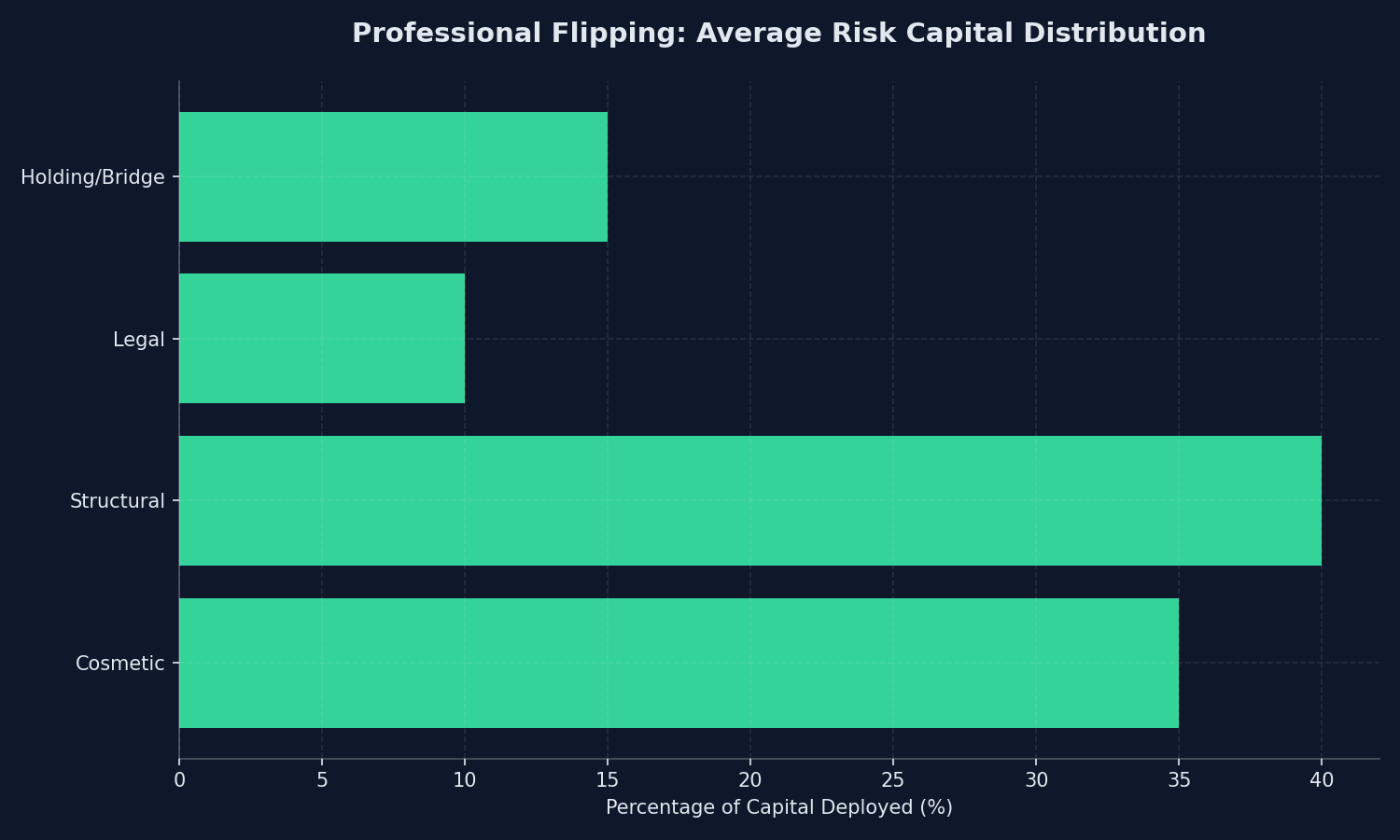

5. Pillar Three: Meticulous Refurbishment Modeling

This is the most visible aspect of a flip and consequently the area most calculators attempt to address. However, a generic calculator is highly dangerous because it fails to account for structural volatility.

A cosmetic flip (painting, flooring, a standardized kitchen swap) is relatively easy to price. However, achieving massive ROI often requires a structural renovation profit model. This involves moving load-bearing walls, replacing total electrical rewires, damp-proof coursing, or total roof replacements.

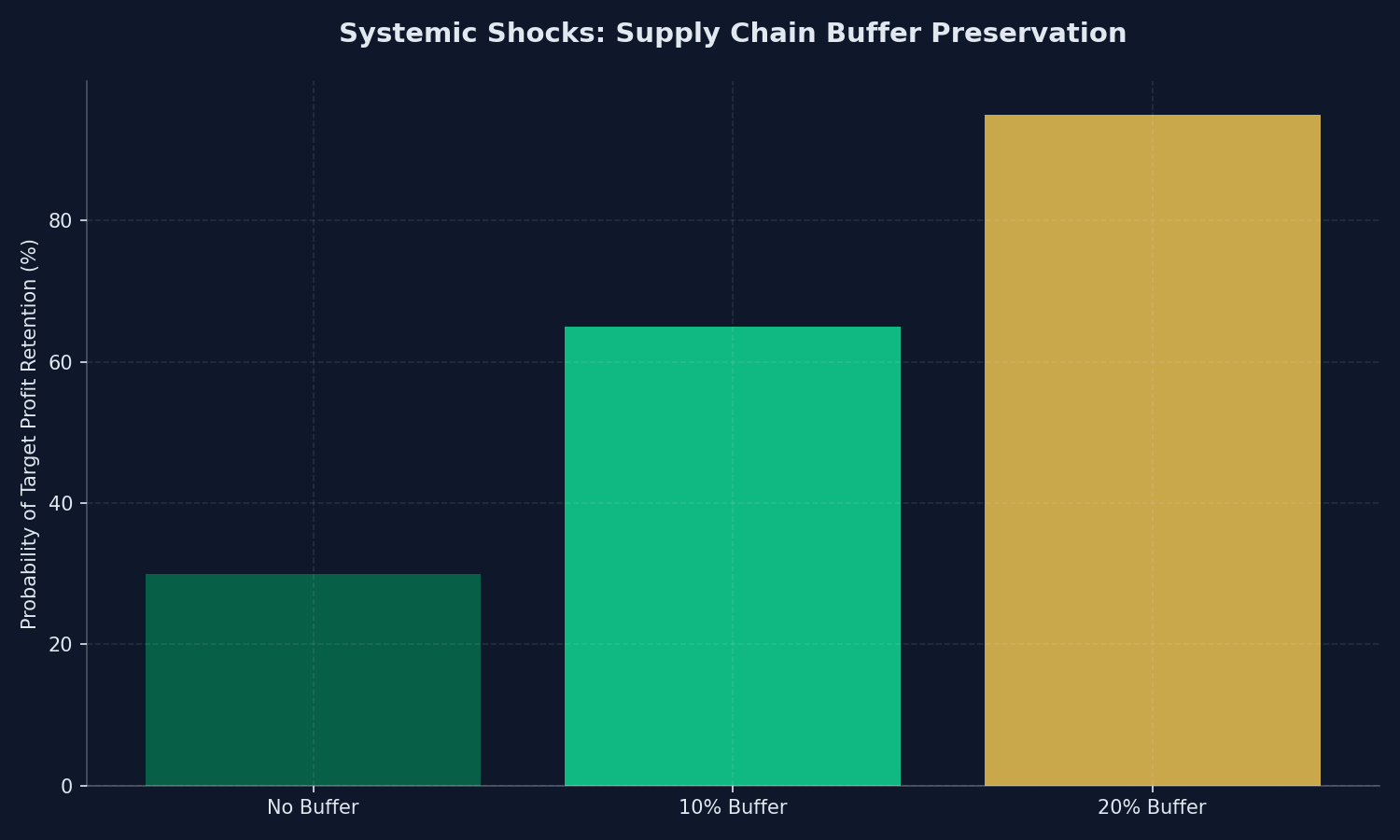

The greatest trap here is the contingency buffer. In 2026, due to severe supply chain tightness and a national shortage of skilled tradespeople, the cost of raw materials and labor fluctuates wildly. An elite investor strictly bakes a 15% to 20% hard contingency buffer into their renovation budget. If the bathroom tiles jump in price by 30%, or if severe dry rot is discovered behind the plaster, the buffer absorbs the shock, insulating the absolute net profit.

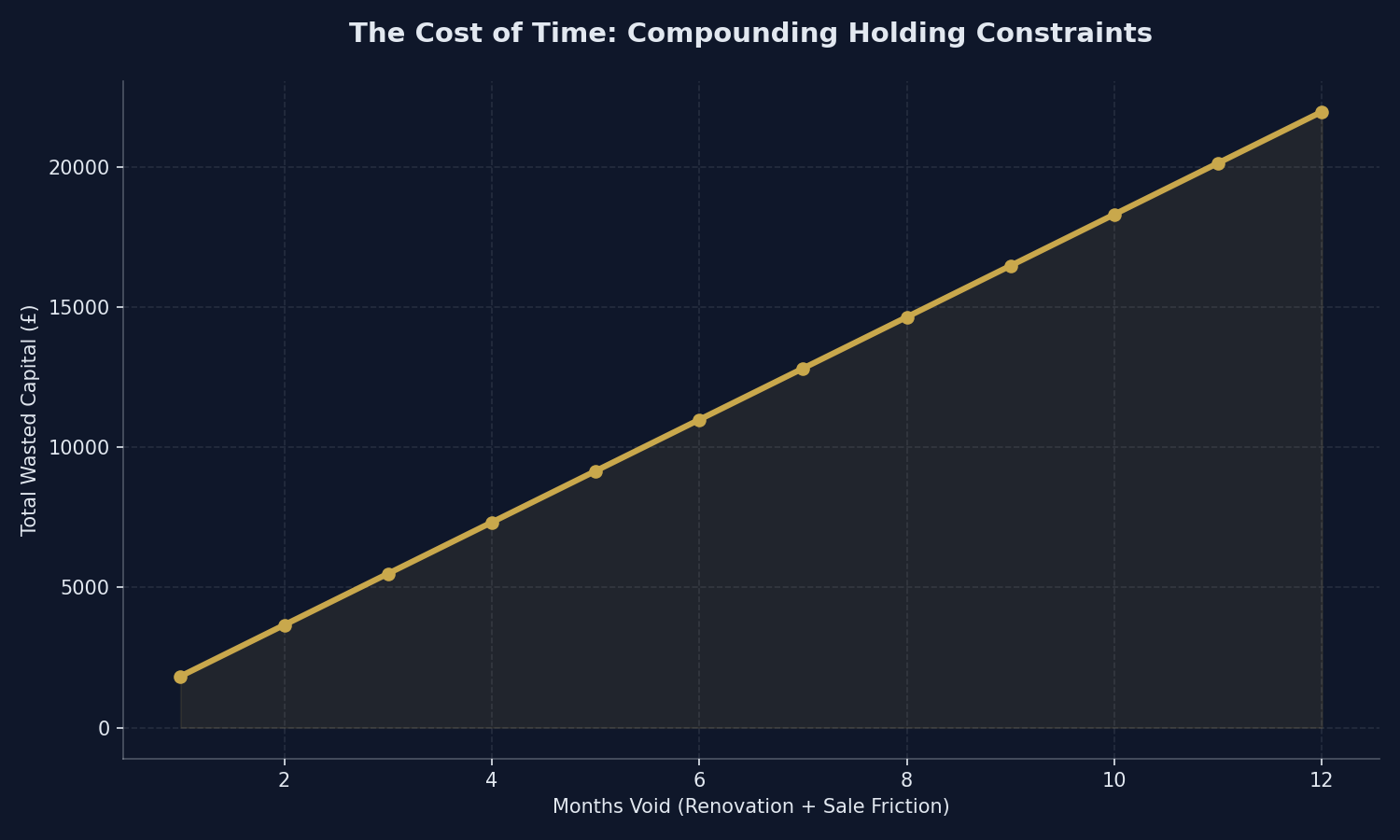

6. Pillar Four: The Silent Assassin – Holding Costs

The single largest differentiator between a theoretical highly profitable spreadsheet and a catastrophic real-world loss is the miscalculation of holding costs. This is the structural reason why the "flipping versus renting" dynamic is so mathematically distinct.

Holding costs represent the daily financial bleed you suffer simply by owning the property during the renovation and sales period.

- Capitalized Bridging Finance: Unless you are buying outright in cash, you are likely using short-term bridging finance at roughly 1% per month. Because you have no rental income to service the debt, the interest is "retained" or "capitalized." If you borrow £150,000 at 1%, you lose £1,500 every single month.

- Council Tax: In heavy-handed UK jurisdictions in 2026, councils aggressively penalize empty homes. You must pay council tax, sometimes at a 200% premium, while the property is empty.

- Vacant Property Insurance: Standard landlord insurance is invalid if the property is gutted and empty. Specialist unoccupied insurance is punishingly expensive.

- Utilities: The standing charges and usage for the builders’ tools.

The timeline is the ultimate enemy. If your spreadsheet models a 3-month turnaround, but a delayed local authority search or a slow conveyancing buyer drags the sale out to 7 months, bridging finance will devour thousands of pounds of your net profit while the physical house sits empty, fully renovated.

7. Pillar Five: Exiting the Deal (Cost of Sale)

You only realise the profit when the funds clear your bank account. Selling the property incurs strict, unavoidable friction.

- Estate Agent Fees: Standard high-street agents command between 1% and 1.5% (+ VAT) of the final sale price.

- Legal Fees for Selling: Your solicitor must push the paperwork through to completion.

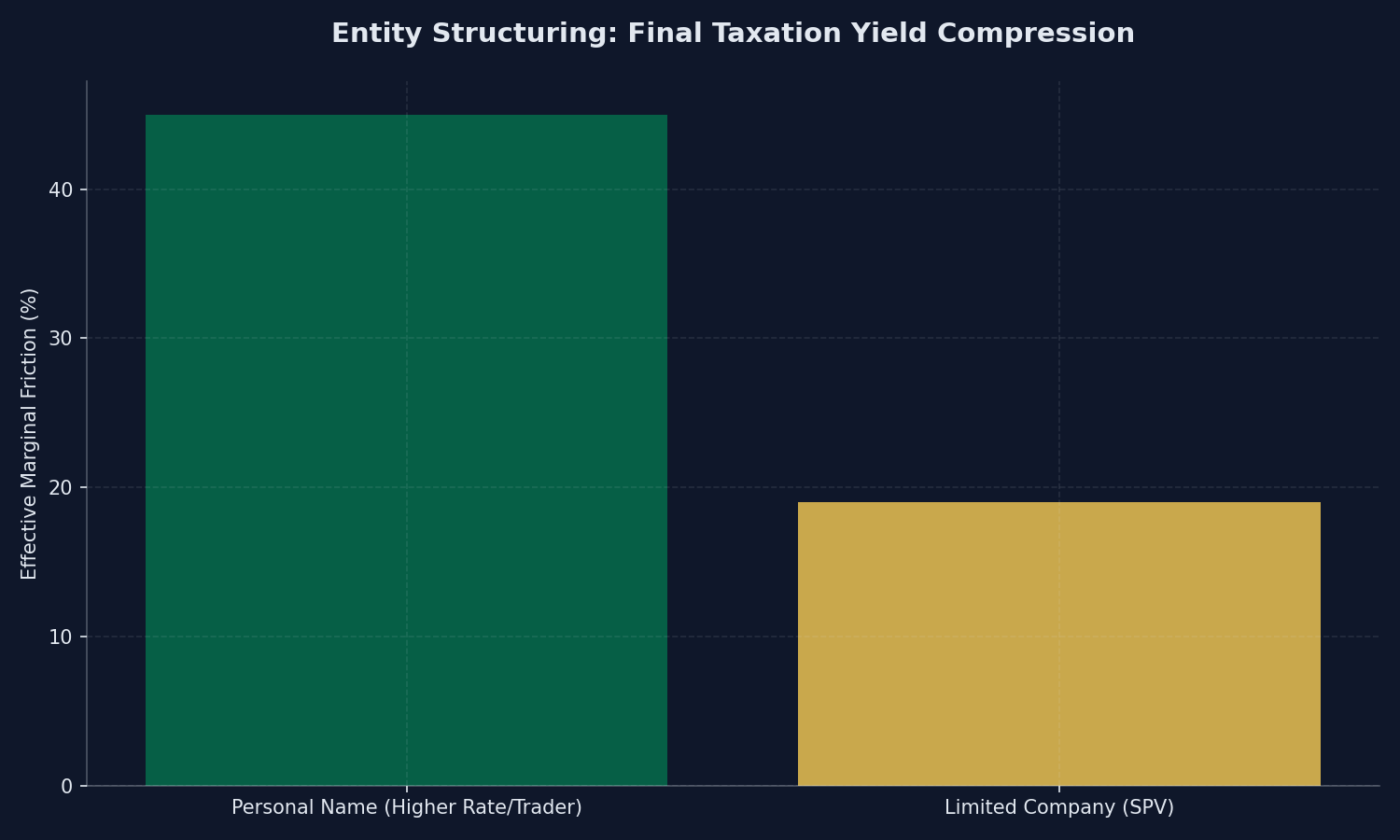

- Capital Gains/Corporation Tax: Upon completion, the HMRC will take their share. Be acutely aware that if you execute multiple flips a year in your personal name, HMRC may classify you as a "trader" generating Income, rather than an investor realizing Capital Gains, drastically increasing your tax burden up to 40% or 45%. This is why elite investors execute entirely inside SPV corporate structures (paying standard Corporation Tax).

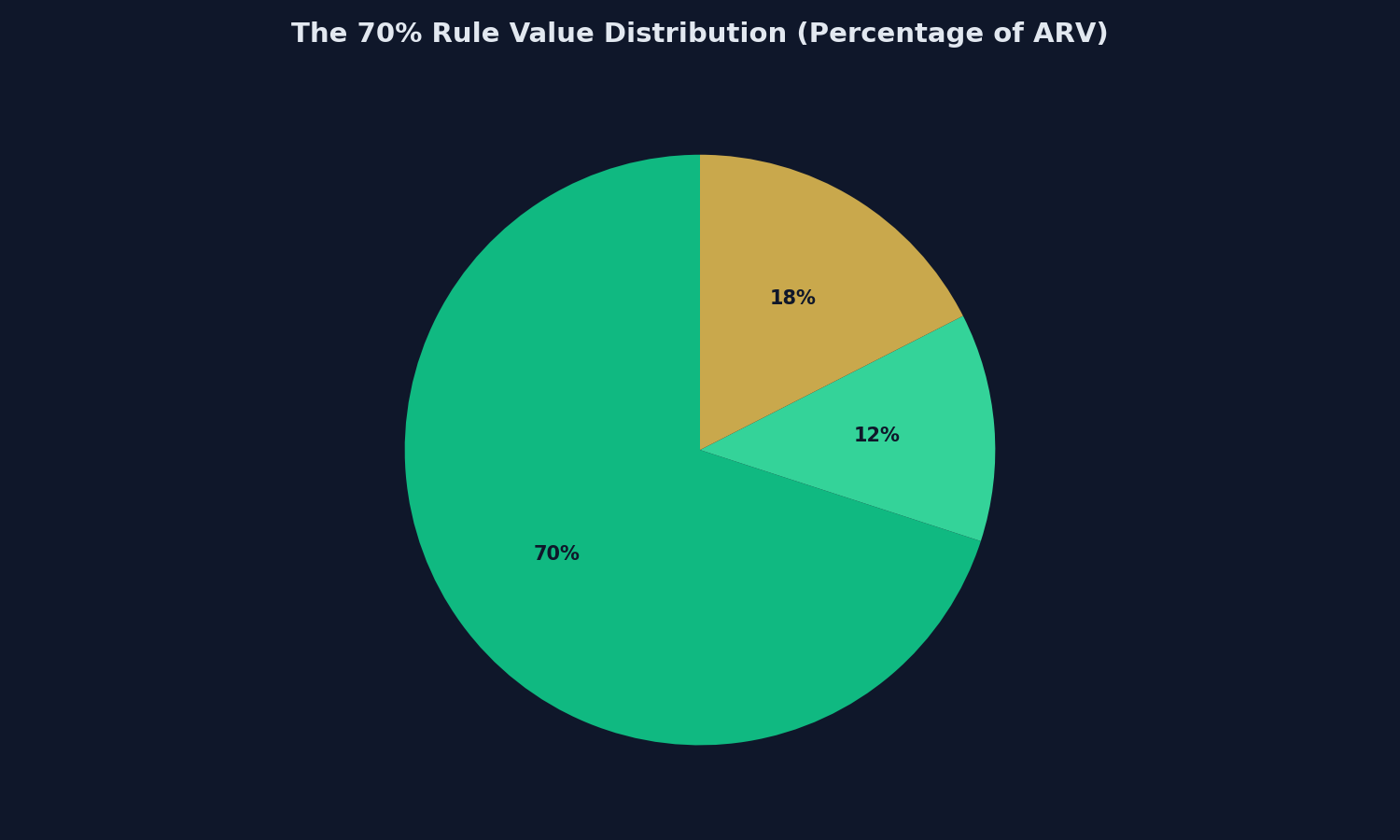

8. Adapting The "70% Rule" for 2026

To avoid executing all five pillars of complex math on every single Rightmove listing they view, professional investors utilize a blunt-force filtration algorithm heavily popularized in the US but highly effective in the UK: The 70% Rule.

The rule dictates the absolute maximum you should ever bid on a distressed property to guarantee a sufficient buffer for holding costs, unexpected renovation spikes, and a baseline 15% to 20% Net Profit margin.

The Formula: Maximum Allowable Offer (MAO) = (ARV x 0.70) – Estimated Refurbishment Costs

Example:

- You find a damaged house. You conservatively calculate its ARV at £200,000.

- 70% of the ARV is £140,000. (The 30% gap is the dedicated buffer for profit, holding costs, fees, and SDLT).

- Your builder quotes £25,000 for the renovation.

- £140,000 - £25,000 = £115,000.

If the vendor demands £135,000, the professional investor walks away instantly. The 70% Rule prevents emotional purchasing by enforcing a mathematical ceiling that mathematically engineers a profit.

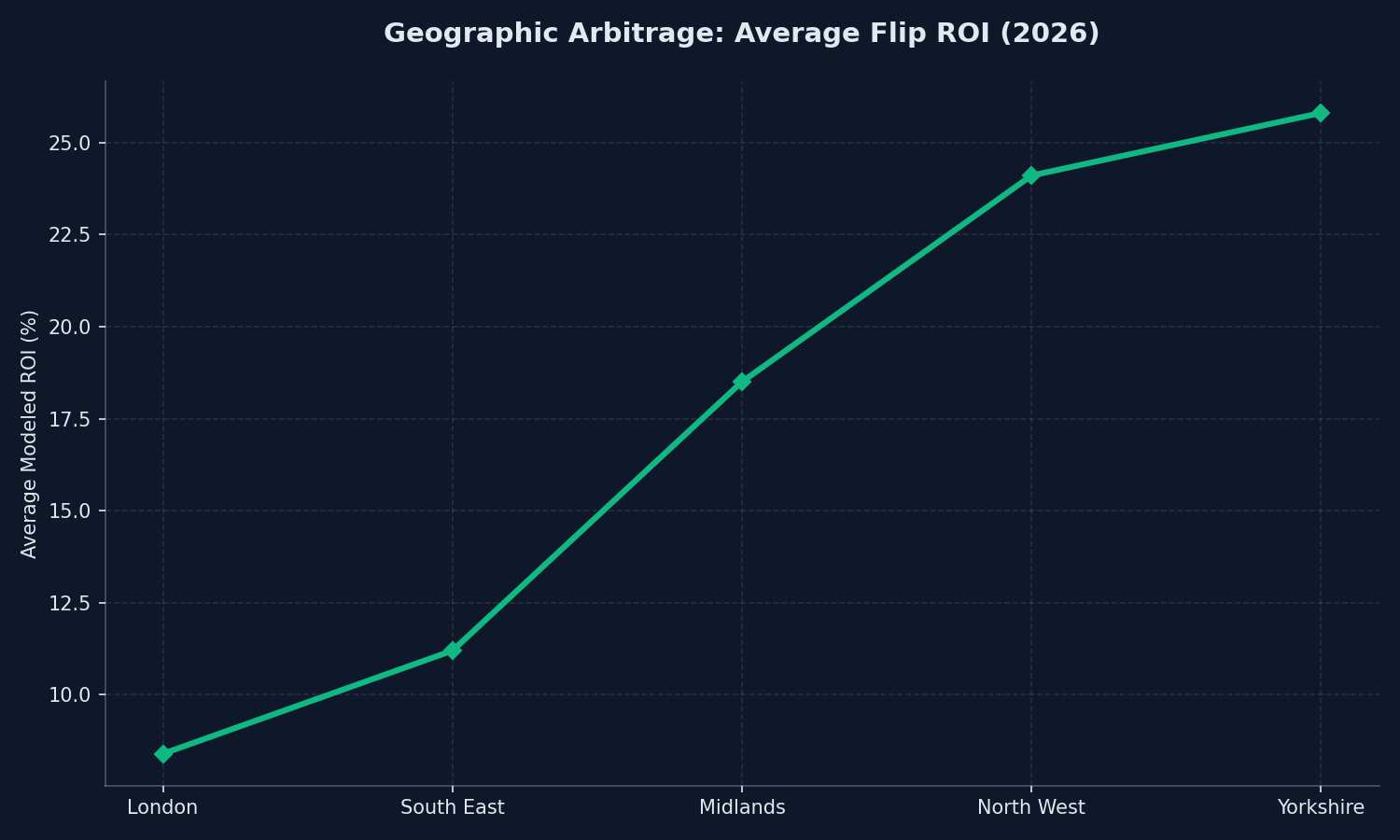

9. North vs South: The Geographic Arbitrage

Yield algorithms and flipping models are hyper-sensitive to geography. In 2026, attempting to flip standard residential property in <a href="/post/foreign-investment-in-<a href="/post/foreign-investment-in-london-real-estate" style="color:#c9a84c;text-decoration:underline;font-weight:500">london-real-estate" style="color:#c9a84c;text-decoration:underline;font-weight:500">London or the wider South East carries extreme systemic risk.

The entry prices are astronomically high. A dilapidated terrace in zones 3 or 4 might require £450,000 to acquire. To utilize bridging finance on £450,000 is to accept an interest bill so large it inherently destroys the margin. Furthermore, the 5% SDLT surcharge scales aggressively, wiping out tens of thousands of pounds on day one.

Conversely, the North of England (specifically regions around Manchester, Leeds, and the East Midlands) offers immense geographical arbitrage. When entry prices sit securely under £150,000, bridging finance costs remain highly manageable, SDLT friction is minimized, and the physical cost of labor is functionally cheaper. This high velocity of cheaper capital allows a Northern investor to execute three £15,000-profit flips in the exact same timeframe a Southern investor spends wrestling with the bridging debt on a single half-million-pound asset.

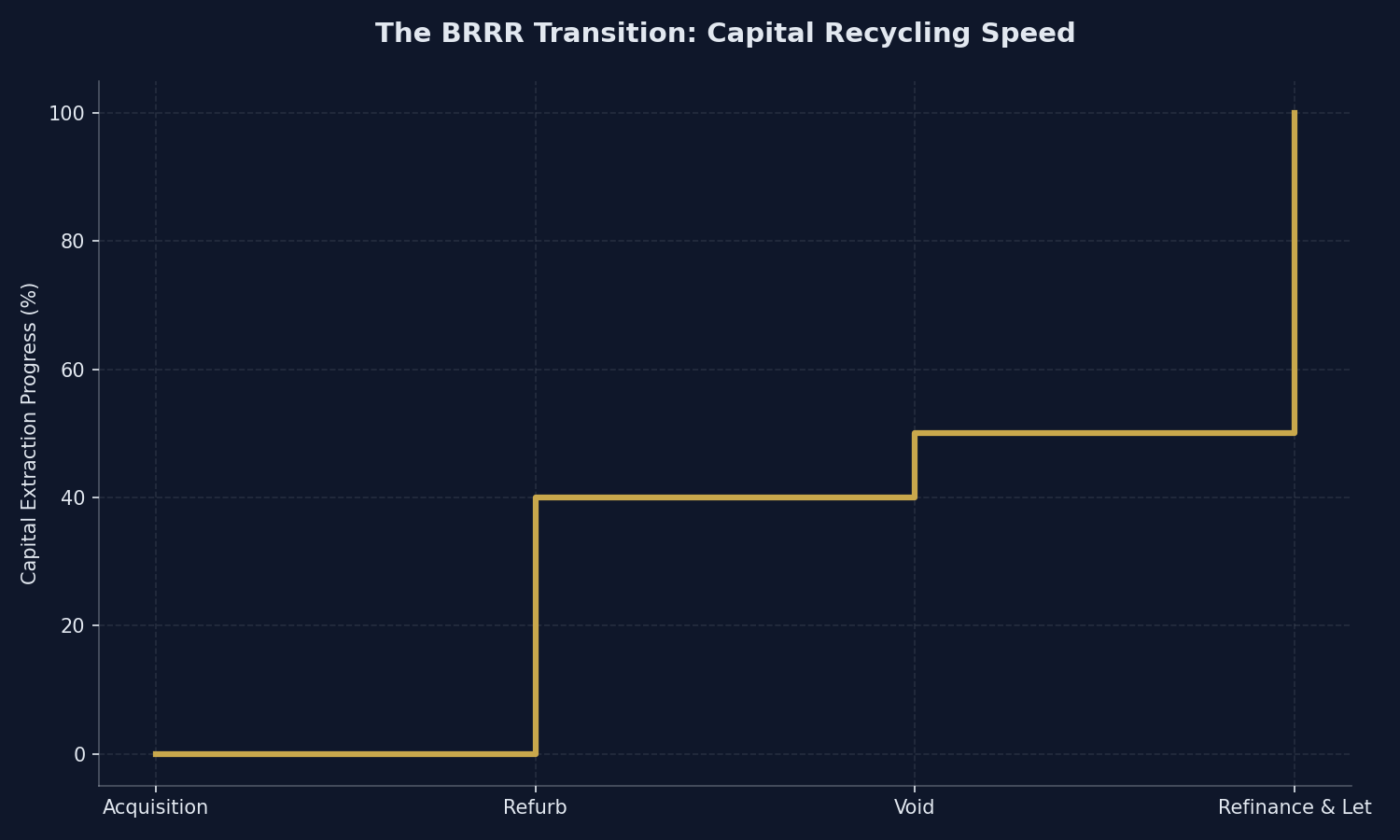

10. The BRRR Method: The Yield Calculator Crossover

While we have established that a "property flipping yield calculator uk" is technically incorrectly phrased for a true flip, there is one major strategy where flipping mechanics directly intersect with long-term yield mathematics: The BRRR Method.

In the BRRR strategy (Buy, Refurbish, Refinance, Rent), you act exactly like a flipper during the first 6 months. You buy distressed, you enforce the 70% rule, and you aggressively renovate. However, instead of selling the property to realize the capital gain (and paying heavy corporation tax on that sale), you hold onto the asset.

You instruct a surveyor to value the newly renovated property at its new, highly elevated ARV. You then take out a standard 75% Buy-to-Let mortgage against that new valuation. Because the new valuation is so high, the 75% loan you extract is often large enough to pay off 100% of your initial bridging finance and reimburse all your physical renovation capital.

At this exact pivot point, the asset ceases to be a flip and becomes a passive rental. It is here that you must deploy a true rental yield calculator to ensure the localized rent can actually service the new, larger BTL mortgage you just placed against the property.

Conclusion: Modeling Your Escape Velocity

Relying on "gut feeling" or hoping the broader UK property market inflates while you own a property is not an investment strategy; it is gambling disguised as construction. Real estate is fundamentally a game of spreadsheets, stress-tests, and data-driven conservatism.

By abandoning the hunt for a fictional "flipping yield" and intensely focusing your mathematics strictly on absolute Net Profit, localized ARV ceilings, and ruthless holding-cost calculations, you insulate yourself from the volatility of the 2026 market. Respect the 70% rule, aggressively manage your bridging timelines, and execute your flips with the clinical precision of a hedge fund underwriter.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →