When property investors hit the financial ceiling of standard single-family Buy-to-Lets, they inevitably face the most polarizing question in UK real estate: is Houses in Multiple Occupation worth it?

Historically, packing six students into a poorly heated terraced house was a guaranteed path to massive cash flow. However, the UK property market has profoundly evolved. Entering 2026, the regulatory landscape—governed by severe Article 4 directions, aggressive mandatory local authority licensing, and the deeply structural shifts of the Renters' Rights Act—has fundamentally transformed the HMO asset class.

HMOs offer unique advantages and brutal challenges. They have become highly professionalized, corporate-grade operations. To determine if an HMO strategy aligns with your capital deployment goals, we must ruthlessly examine the exact pros and cons from both the perspective of an institutional landlord, and the modern tenant.

What is an HMO?

An HMO, or House in Multiple Occupation, is defined under UK housing law as a single property rented out by at least three people who are not from one "household" (e.g., a family) but who share basic amenities such as the bathroom or kitchen.

This encompasses standard university student shared houses, large-scale professional "co-living" environments, and some specific types of self-contained properties converted into bedsits.

The Regulatory Strata (2026 Context)

It is scientifically critical for investors to understand that "HMO" is not a singular definition; it exists on a highly regulated spectrum:

- C4 HMOs: Properties housing 3 to 6 unrelated individuals. In many areas, standard residential homes (C3) can be converted to C4 without explicit planning permission, unless the local council has enacted an Article 4 direction.

- Sui Generis HMOs: Massive properties housing 7 or more unrelated people. These exist completely outside the standard use-class system and require absolute, full commercial planning permission.

- Mandatory Licensing: If your property houses 5 or more unrelated people, it falls under national mandatory licensing. You must pay the local council for a heavily audited operational license.

While an HMO can be a highly lucrative, high-yield venture for professional landlords and provide flexible, affordable living options for tenants, they demand significant lifestyle and operational commitments.

Advantages for Landlords

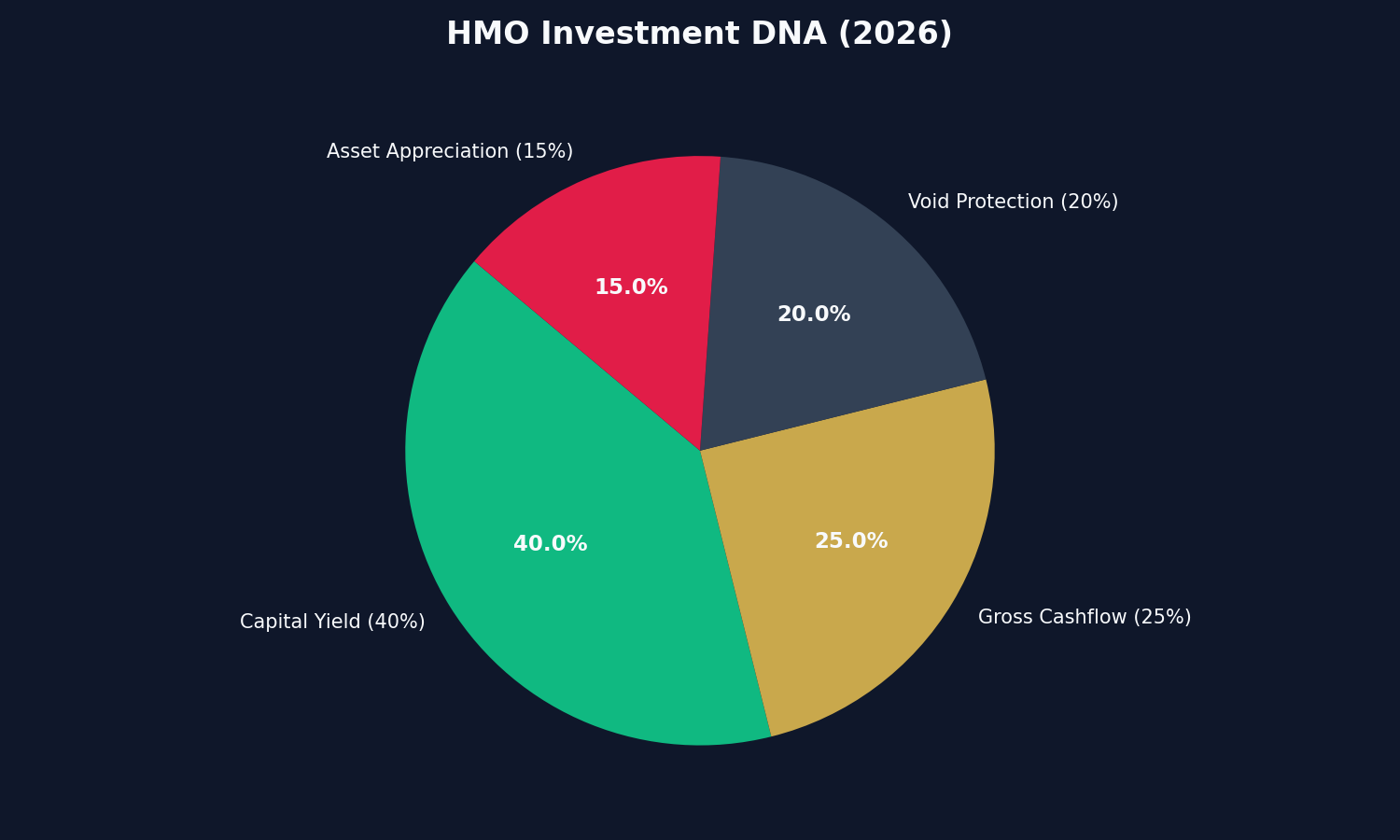

For an investor aggressively scaling a portfolio, the advantages of an HMO are entirely mathematical. The core operational directive of an HMO is yield compression: maximizing the revenue per square foot of physical real estate.

1. Higher Rental Yields

The undisputed primary benefit of an HMO is the sheer velocity of the rental yield. Renting out rooms individually systematically breaks the ceiling of local property values.

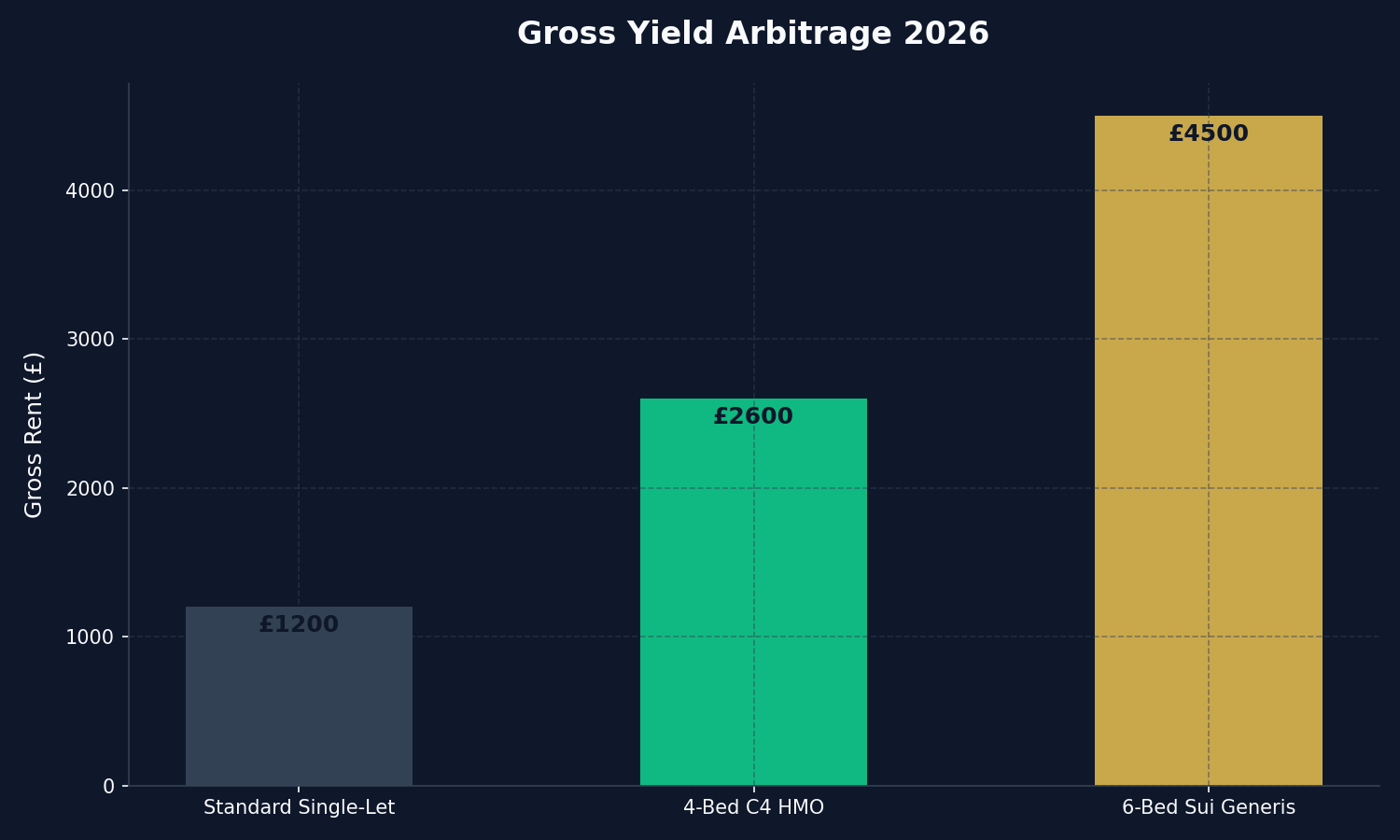

If a 4-bedroom property in Nottingham is let to a single family, the local market cap might dictate a maximum gross rent of £1,200 per month (yielding roughly 5%). If that exact same property is licensed as a 4-bed HMO and rented to young professionals at £650 per room, the gross rent explodes to £2,600 per month. You are extracting a massive 11% gross yield from the exact same brick-and-mortar footprint.

This gross margin absorption is why institutional syndicates aggressively hunt for large, distressed properties suitable for Sui Generis conversion.

2. Diversified Income Stream (Void Protection)

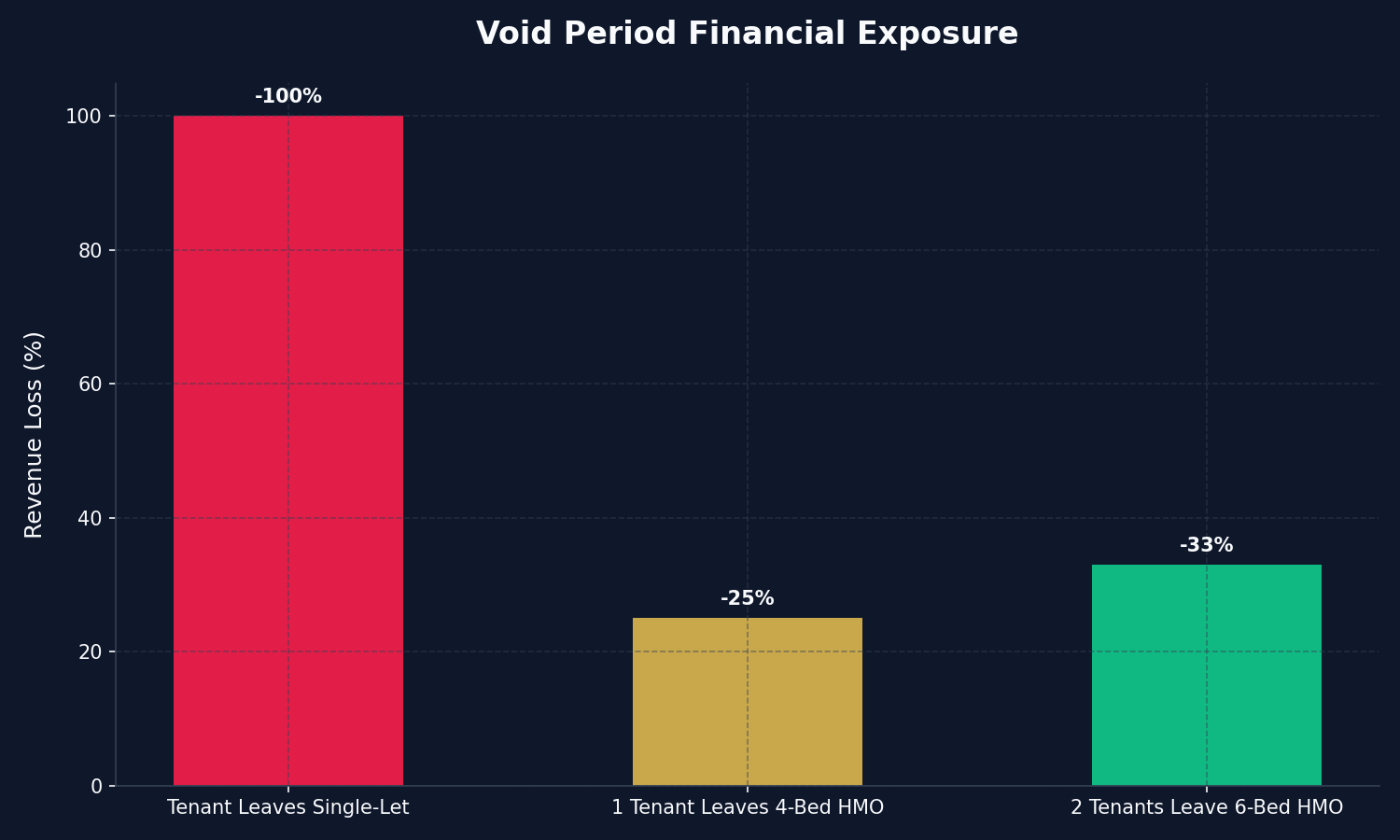

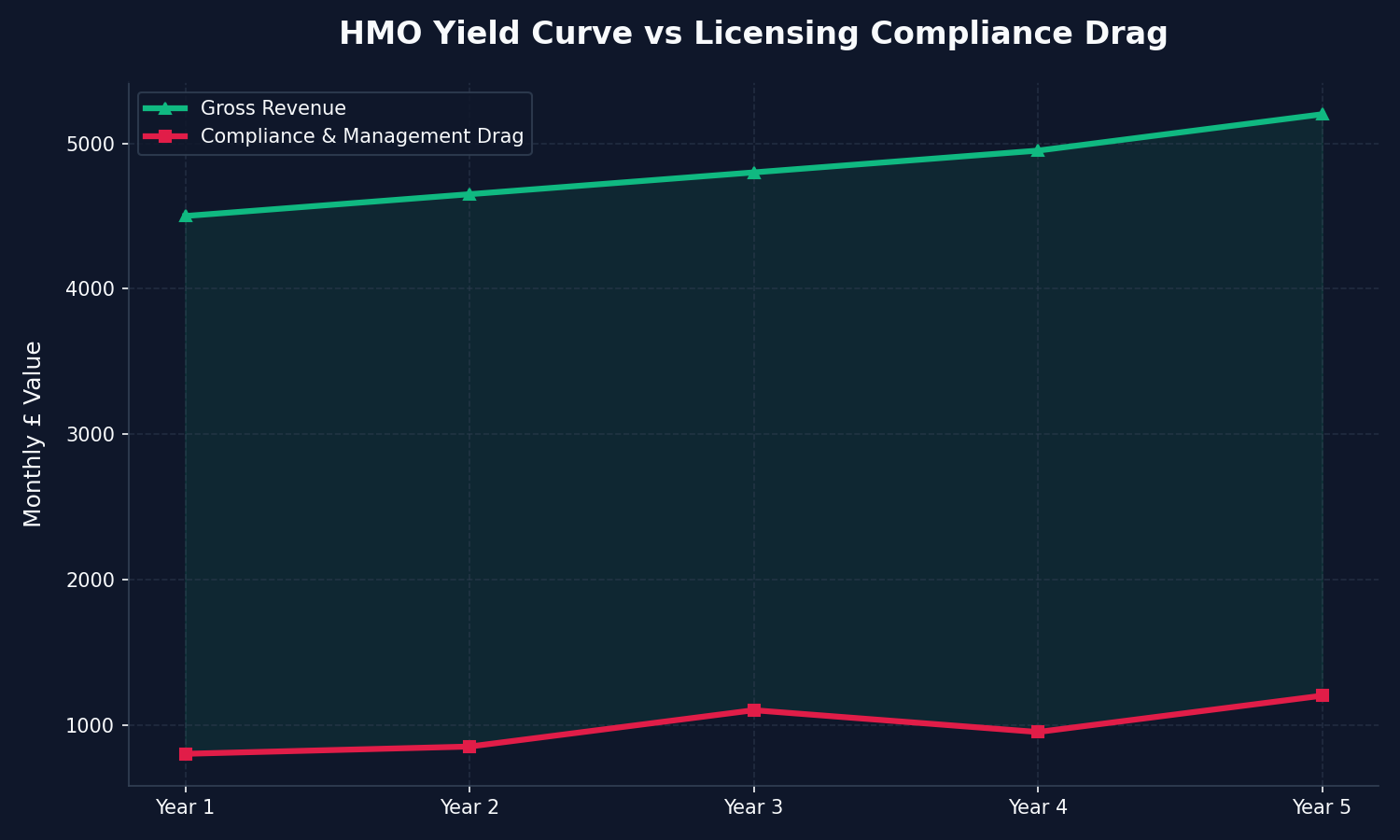

With a standard single-let property, the landlord's risk profile is binary: the property is either 100% occupied or 100% void. If a family moves out, your income drops to zero instantly, yet your mortgage, insurance, and council tax liabilities remain absolute.

An HMO physically mitigates this binary risk. By operating multiple Assured Shorthold Tenancies (ASTs) or individual room licences simultaneously, the landlord spreads their financial exposure. If one tenant vacates room 4, the property is still 80% occupied, and the remaining four tenants are happily covering the core mortgage debt and operational expenses. This diversified income stream mathematically guarantees cash flow stability during tenant transitions.

3. Increased Market Demand

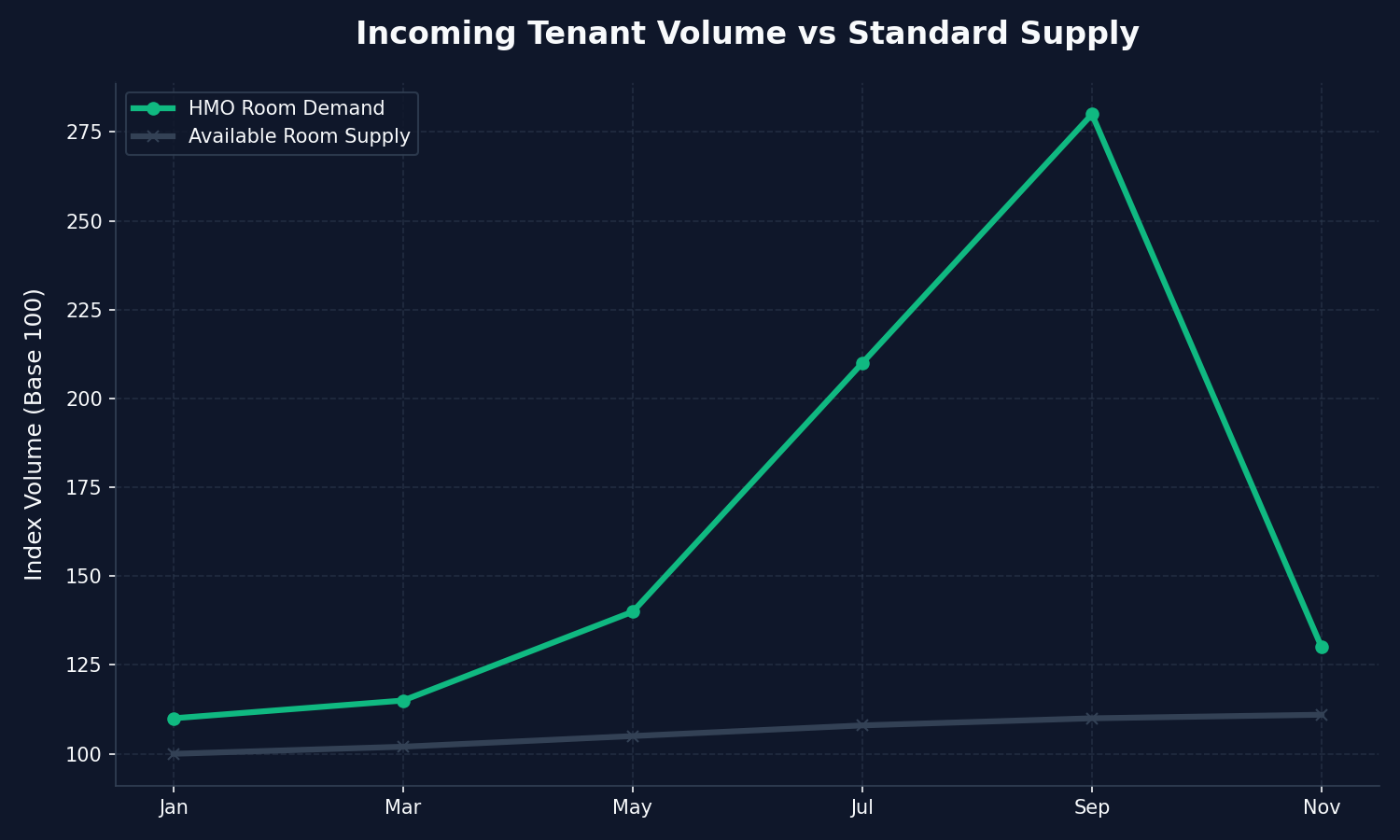

The macroeconomic reality of 2026 dictates severe housing shortages and massive inflationary pressures on independent living. Young professionals graduating from prestigious universities can rarely afford to rent a £1,500 1-bedroom flat in urban hubs like Manchester, Birmingham, or London.

Consequently, the demand for highly premium, " Boutique Co-living" HMOs has skyrocketed. Tenants are actively seeking the affordability of an HMO, wrapped in the aesthetic of a high-end hotel with inclusive bills and high-speed fibre broadband. By catering to this specific demographic, professional landlords ensure a relentless, waiting-list driven stream of high-quality potential tenants.

Disadvantages for Landlords

The high yields of an HMO are not free money; they are compensation for enduring operational complexity and legal liability. Amateur landlords attempting to run HMOs routinely face financial ruin due to regulatory oversight.

1. Severe Regulatory Compliance & Article 4

The days of unmonitored HMO conversions are dead. To answer is Houses in Multiple Occupation worth it, you must confront the 2026 regulatory gauntlet.

Landlords must ensure the property passes brutal health and safety audits (fire doors with intumescent strips, interlinked mains-powered smoke alarms, emergency lighting, and specific room-size minimums).

Furthermore, Article 4 Directions have weaponized local councils. Councils can arbitrarily remove your permitted development rights, meaning you cannot convert a standard house into a 3-bed HMO without full planning permission—permission they will almost certainly deny to prevent "HMO clustering." Attempting to operate an unlicensed HMO in these regions results in limitless fines and Rent Repayment Orders (RROs), where you must legally refund 12 months of rent back to the tenants.

2. Higher Turnover Rates and Void Costs

While an HMO protects against absolute 100% voids, it mathematically ensures a significantly higher turnover frequency. A single family might stay in a house for five years; an HMO tenant might only stay for nine months while they transition to a new job or save for their own deposit.

This hyper-turnover creates hidden financial attrition. Every time a tenant leaves, the landlord incurs referencing fees, deposit protection friction, inventory checks, deep cleaning costs, and the inevitable wear-and-tear repairs required to make the room acceptable for the next occupant.

3. Management Complexity & Capital Expenditure

An HMO is not passive real estate; it is an active hospitality business. When you rent a single-let, the family generally cuts the grass and changes lightbulbs. In an HMO, you are the facility manager.

With five unrelated adults sharing a kitchen, wear-and-tear accelerates exponentially. White goods break faster. Disputes over the heating thermostat occur daily (since the landlord is paying the bills). Because of this friction, the day-to-day management of an HMO is profoundly demanding. Professional operators entirely outsource this to specialist HMO letting agents, who charge 12% to 15% management fees, directly eroding the high gross yield back into a moderate net margin.

Advantages for Tenants

From the demand-side perspective, the UK rental market is fundamentally hostile. HMOs provide a critical lifestyle and financial bridging mechanism for an entire generation.

1. Absolute Affordability

The singular, driving force behind the explosion of HMO demand is pure affordability. For students, transient contractors, and young professionals starting their careers, saving a 5-week deposit for an £1,800 apartment, plus covering Council Tax, Gas, Electric, and Broadband individually is mathematically unviable.

HMOs completely socialize these costs. By offering a unified, all-inclusive monthly rent of £750, tenants enjoy the luxury of living in highly desirable, central-urban postcodes that they could never access on a single-let lease. It completely removes the anxiety of fluctuating winter energy bills.

2. Strategic Flexibility

Modern careers demand extreme agility. A junior doctor or a tech consultant may only need to be stationed in Leeds for eight months before transferring to a hub in London.

Traditional single-let properties demand rigid 12-to-24 month AST lock-ins. HMOs structurally accommodate transient lifestyles. Because the landlord relies on high turnover and high demand, they routinely accept 6-month, or even 3-month cyclical leases. This allows tenants the absolute flexibility to scale their living arrangements dynamically without being trapped by punitive break clauses.

3. Community Living and Networking

Particularly in an era of intense remote work and digital isolation, moving to a new city alone is daunting.

High-end, professional HMOs (often branded as "Co-living" spaces) offer an immediate, pre-built social network. Tenants have the opportunity to interact in communal lounges, share networking opportunities, and rapidly form a community. Some elite landlords actively curate their HMO demographics, deliberately mixing tech workers with creatives to foster a vibrant, harmonious household culture.

Disadvantages for Tenants

However, the communal nature of an HMO requires severe compromises. The lower price point demands an inherent sacrifice of environmental control.

1. Lack of Absolute Privacy

When you cross the threshold of your bedroom door, your privacy ends. Sharing a house with five other adults intrinsically mandates a loss of isolation.

Waiting to use the main shower before work, navigating around someone else cooking in the communal kitchen, and absorbing the ambient noise of a busy household are daily realities. For introverted individuals, or those working highly intensive night shifts, the lack of a totally silent, controlled environment can lead to severe operational burnout.

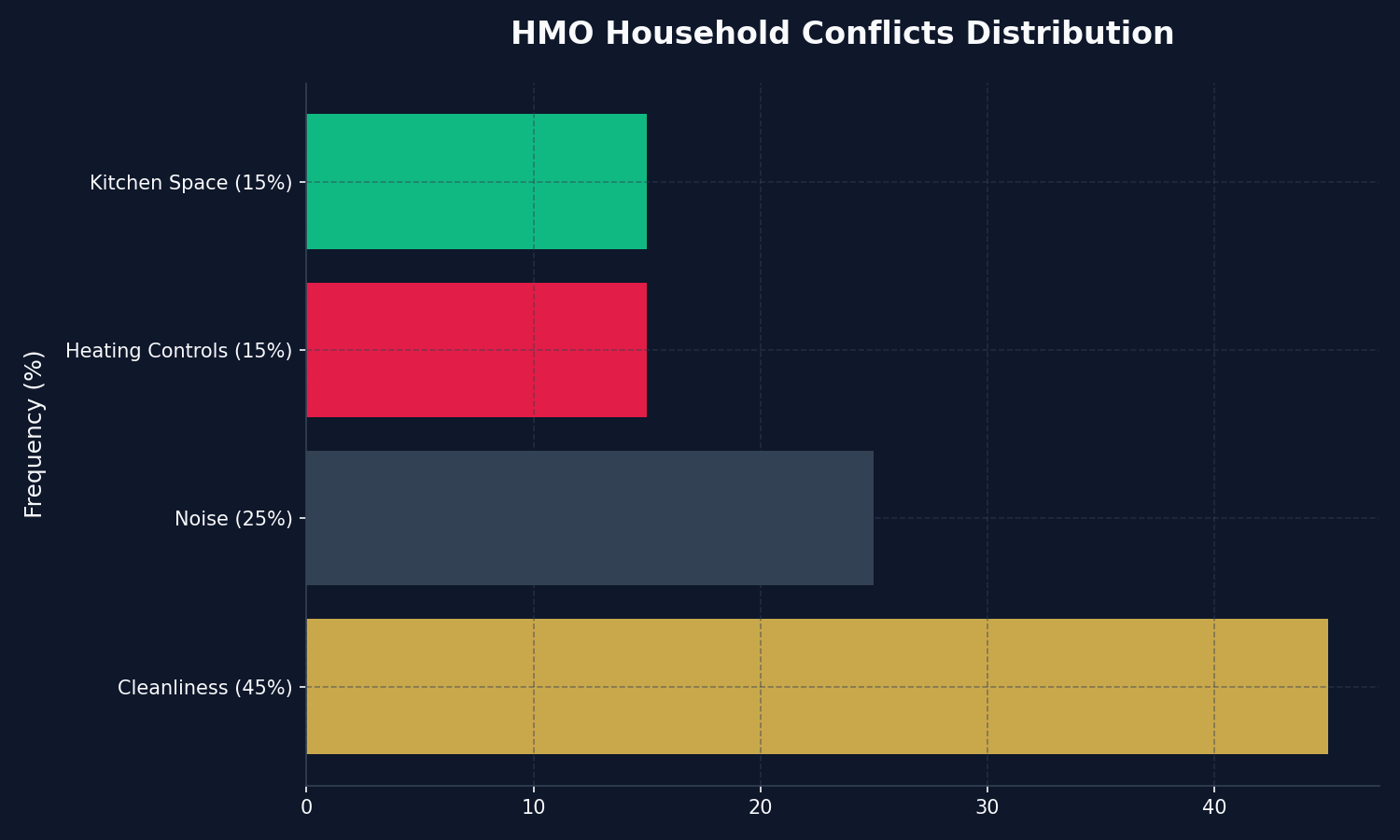

2. Interpersonal Conflicts

Combining five individuals from different backgrounds, holding different professional standards of cleanliness, differing sleep schedules, and varied social habits into a single kitchen is a recipe for inevitable tension.

Conflict over stolen food, unwashed dishes, guests staying over late at night, or noise volume are the hallmark of poorly managed HMOs. If a landlord fails to firmly enforce a "House Rules" charter, a single toxic tenant can completely devastate the wellbeing of the entire household, prompting a mass exodus of the good tenants.

3. Limited Control Over Living Environment

Tenants who rent a whole property enjoy absolute sovereignty over their environment; they choose the broadband provider, they adjust the thermostat, and they decide if they want a pet.

In an HMO, tenants are merely licensing a fraction of the asset. The landlord controls the heating timer (often locking it remotely to prevent energy waste). The landlord bans pets due to allergy control for other rooms. The landlord handles the garden maintenance. Decisions regarding the aesthetic and functionality of the property are dictated from the top down, leaving the tenant with zero autonomy over their broader living environment.

Conclusion: Balancing the Scales

So, is Houses in Multiple Occupation worth it?

The reality is that HMOs present a highly bifurcated set of advantages and challenges. For institutional landlords and aggressive BRRRR Strategy investors, the potential for massive, double-digit rental yields and deeply diversified income is the holy grail of property physics. But this wealth is hard-earned; it demands rigorous regulatory compliance, expensive commercial financing, and the stomach for constant, complex management.

For tenants, HMOs are a financial lifeline. They provide vital affordability, transient flexibility, and instant community in an otherwise brutal housing market, but they exact a heavy toll on personal privacy and environmental autonomy.

In 2026, the amateur HMO landlord is dead. If you are willing to operate your property portfolio as a ruthless, compliant, high-end hospitality business, the HMO model remains the single most powerful cash-generating engine in UK real estate.

Whether you are seeking to acquire a compliant HMO, structure a commercial Refinance, or calculate the exact yield on your next flipping project, the data-driven approach is your only defense against failure. Ensure your local licensing is watertight before you deploy your capital.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →