Securing the right finance is the cornerstone of any successful property portfolio. Understanding how to finance buy-to-let property in the UK is no longer just about finding the lowest interest rate; it is about structuring your debt to withstand regulatory shifts, tax changes, and fluctuating base rates.

As we look toward 2026, the landscape of UK property investment is undergoing a profound transformation. The implementation of the Renters' Rights Act in May 2026, the expansion of Making Tax Digital (MTD) for Income Tax, and the lingering effects of Section 24 have fundamentally altered the mathematics of property investment. The era of the heavily leveraged, amateur landlord operating in their personal name is largely over.

Today, property investment is a professional discipline. It requires a data-driven approach to capital allocation, a deep understanding of stress testing, and a strategic view of corporate structures. Whether you are acquiring your first asset or scaling a multi-million-pound portfolio, the mechanism you use to fund your purchases will dictates your cash flow, your tax liability, and your ultimate return on investment (ROI).

At Shaded Canvas, we prioritize empirical data over speculation. This comprehensive guide dissects the realities of financing buy-to-let property in 2026, offering actionable strategies for navigating a complex financial environment.

The 2026 Financial Landscape: A New Era for Landlords

Before exploring specific financing methods, it is crucial to understand the macroeconomic and regulatory environment shaping the market in 2026.

The Trajectory of Interest Rates

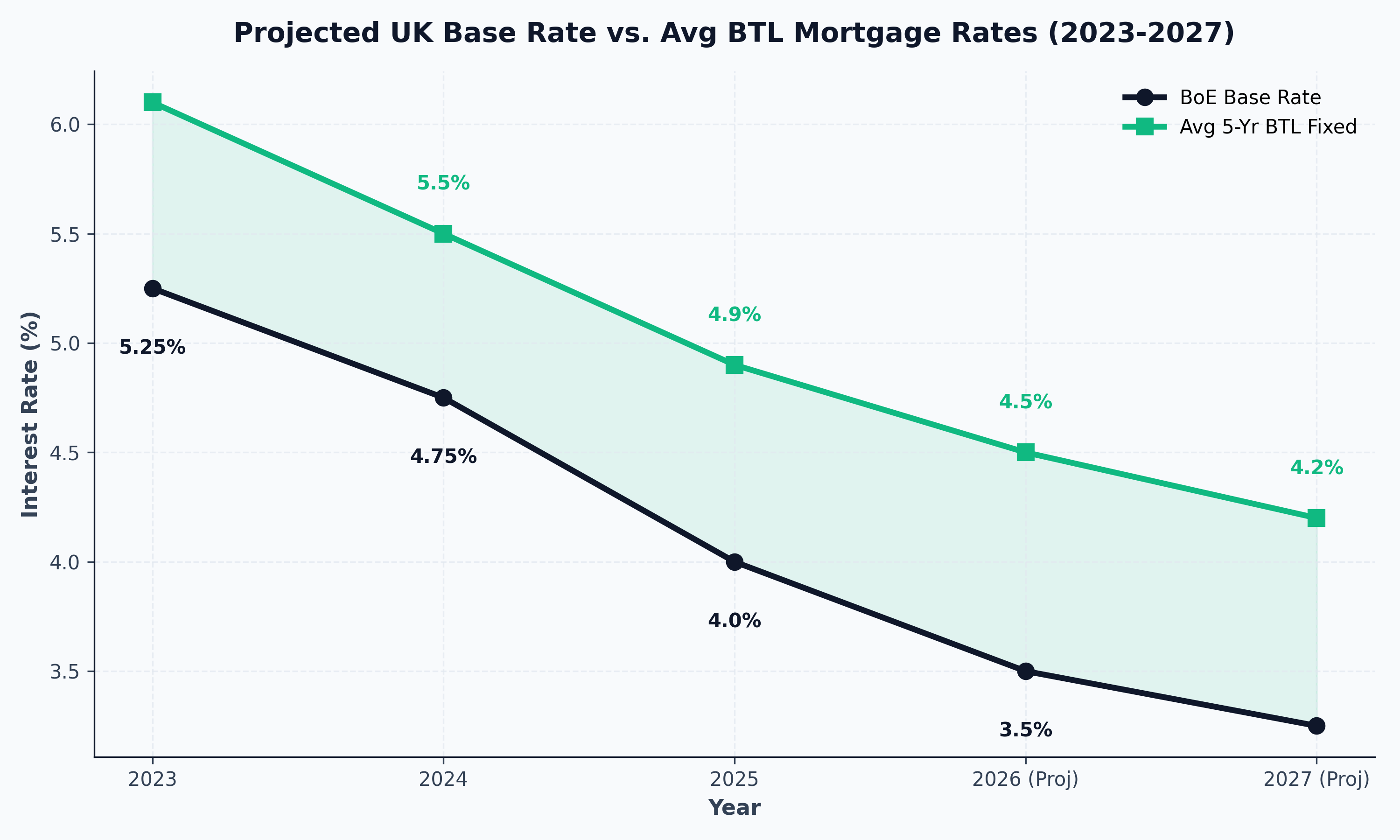

The aggressive rate hikes that characterized 2023 and early 2024 are receding. Current forecasts anticipate the Bank of England Base Rate to stabilize between 3.0% and 3.75% throughout 2026. Consequently, average five-year fixed buy-to-let mortgage rates are expected to settle around the 4.5% mark.

While this represents a significant improvement from the peaks of recent years, it is a permanent departure from the ultra-low rates of the 2010s. Investors must calibrate their models to this "new normal." The focus has shifted from maximizing leverage on low-yielding assets to acquiring high-yielding assets (such as HMOs or properties in northern regional hotspots) that can comfortably service debt at 4.5% to 5.5%.

(Figure 1: Projected UK Base Rate vs. Average BTL Mortgage Rates 2024-2027)

(Figure 1: Projected UK Base Rate vs. Average BTL Mortgage Rates 2024-2027)

Regulatory and Tax Pressures

The strategic choice of financing is heavily influenced by the UK government's sustained regulatory squeeze on the private rented sector (PRS).

- Section 24 (The Tenant Tax): Individual landlords can no longer deduct mortgage interest from their rental income before calculating their tax liability. Instead, they receive a basic rate (20%) tax credit. For higher-rate (40%) and additional-rate (45%) taxpayers, this dramatically reduces net profitability, often pushing them into higher tax brackets based purely on gross turnover.

- Making Tax Digital (MTD) for Income Tax: From April 2026, landlords earning over £50,000 annually must maintain digital records and submit quarterly updates to HMRC. This necessitates robust, professionalized accounting systems.

- The Renters' Rights Act (May 2026): The abolition of Section 21 evictions and the transition to periodic tenancies increase the operational risk for landlords. Lenders are acutely aware of this increased risk profile, emphasizing the need for strong financial buffers and rigorous tenant referencing.

These factors universally point toward one major trend in BTL finance: the migration to corporate structuring.

Strategy 1: The Buy-to-Let (BTL) Mortgage

The buy-to-let mortgage remains the primary engine of growth for most property investors. However, obtaining one requires navigating a strict set of criteria that differs fundamentally from residential lending.

How BTL Mortgages Differ from Residential Mortgages

When you apply for a residential mortgage, the lender assesses your personal income (salary) against your personal outgoings to determine affordability.

When you apply for a BTL mortgage, the lender assesses the asset. They are primarily concerned with whether the property itself generates sufficient income to cover the debt, even under stressed conditions.

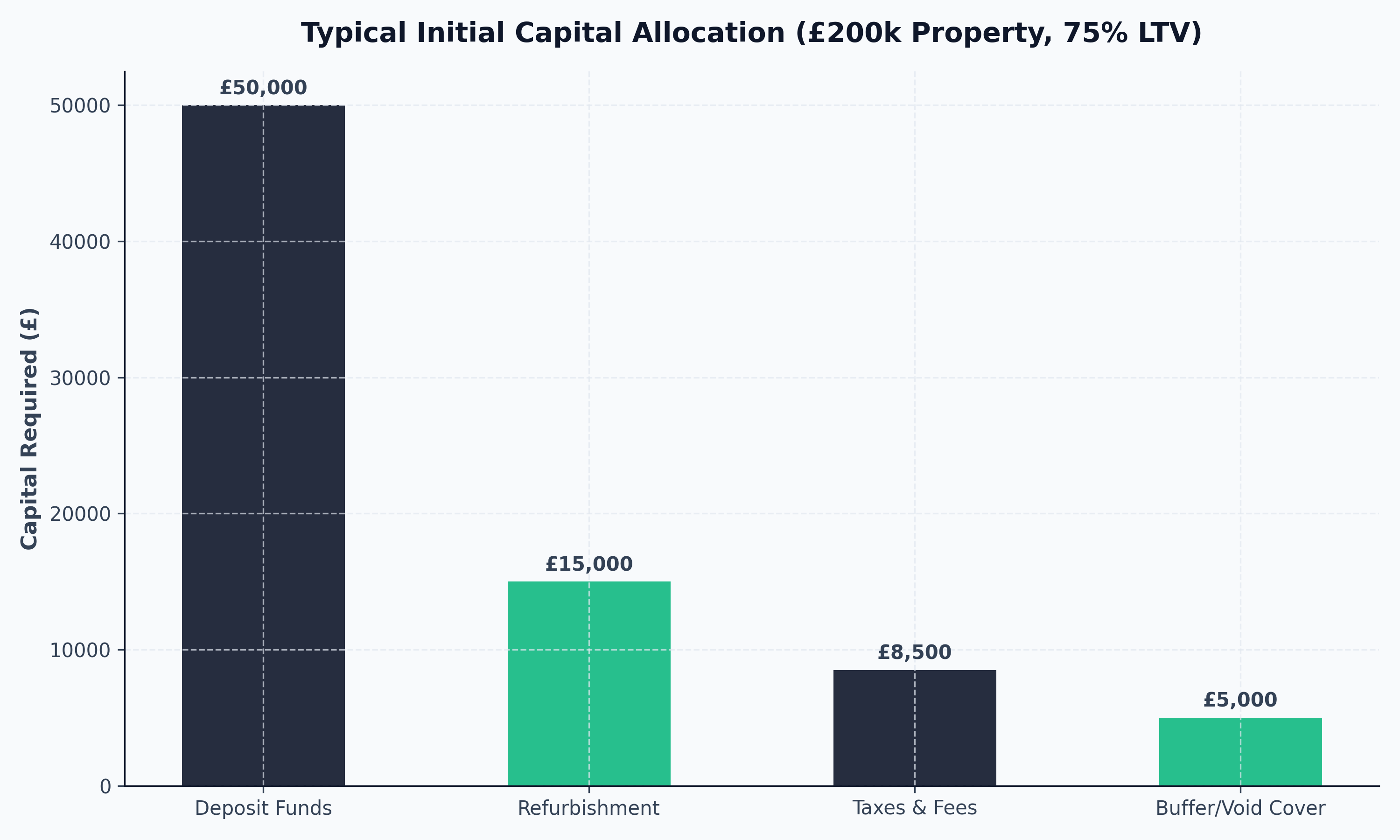

- Deposits: You cannot buy an investment property with a 5% deposit. BTL lenders typically require a minimum deposit of 25% (a 75% Loan-to-Value or LTV ratio). To access the most competitive interest rates, a deposit of 35% or 40% (60% LTV) is often necessary.

- Interest-Only vs. Repayment: The vast majority of BTL mortgages are issued on an "interest-only" basis. Your monthly payments only cover the interest accrued; the principal loan amount remains unchanged. This maximizes monthly cash flow, allowing you to build an emergency fund or accumulate capital for the next deposit. The exit strategy (repaying the capital) usually involves selling the property or refinancing.

- Interest Rates and Fees: BTL mortgages inherently carry higher interest rates and significantly higher arrangement fees than residential products. It is not uncommon to see arrangement fees of 2% to 5% of the loan amount, which can be added to the mortgage balance.

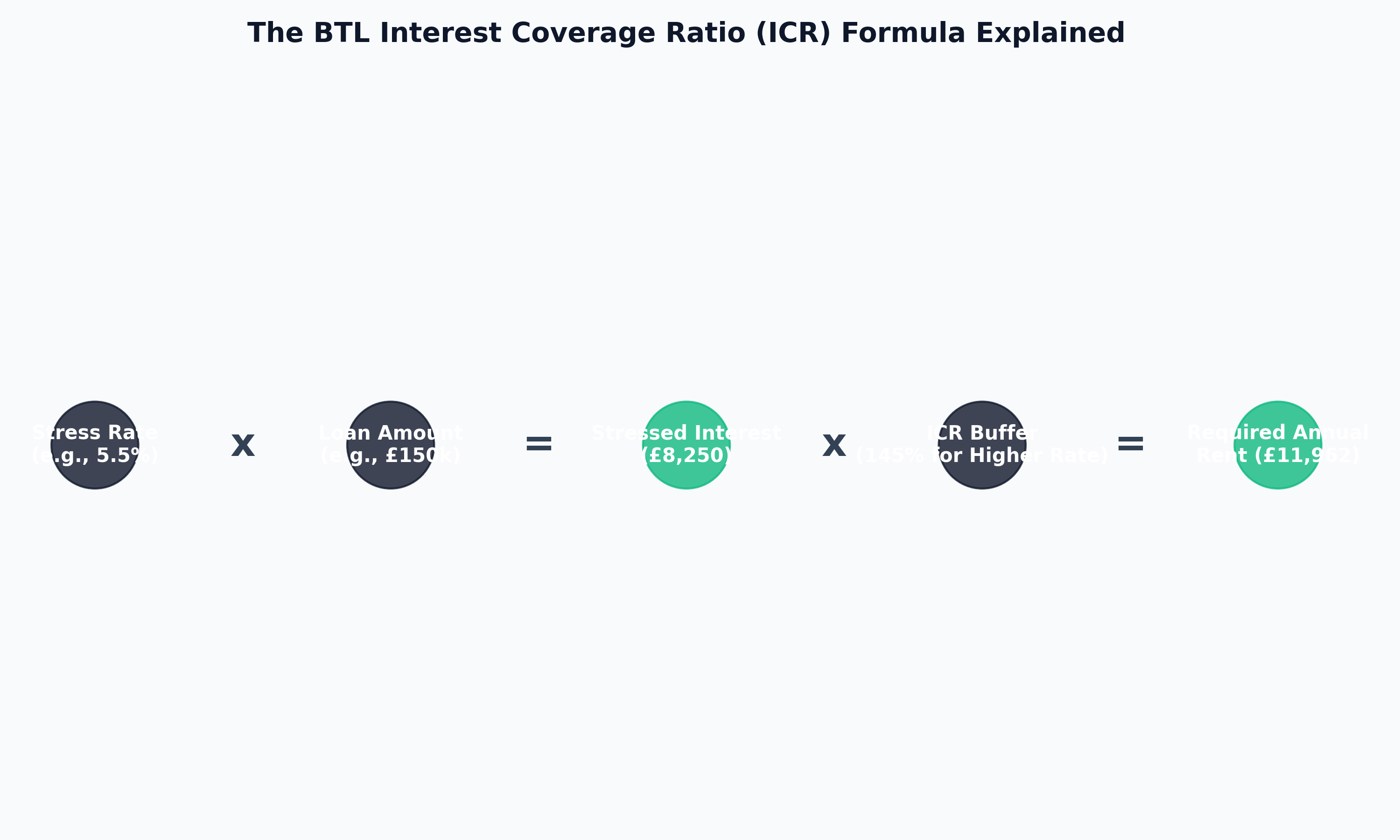

The All-Important Stress Test: ICR

The defining metric of a BTL mortgage application is the Interest Coverage Ratio (ICR). This is the formula lenders use to ensure the rental income easily covers the mortgage payments.

Traditionally, the formula required the gross rental income to be at least 125% of the mortgage interest payment, calculated at a stressed interest rate (often 5.5% or 2% above the pay rate).

However, due to Section 24, the ICR rules have bifurcated based on the borrower's tax status:

- Basic Rate Taxpayers (and Limited Companies): Usually subject to an ICR of 125%.

- Higher/Additional Rate Taxpayers: Usually subject to an ICR of 145% (to account for the higher tax burden they face on rental income).

(Figure 2: The ICR Formula Explained visually)

(Figure 2: The ICR Formula Explained visually)

Example Calculation (Higher Rate Taxpayer):

- Property Value: £200,000

- Loan Amount (75% LTV): £150,000

- Stress Rate: 5.5%

- Annual Stressed Interest: £150,000 * 5.5% = £8,250

- Required ICR: 145%

- Required Annual Rent: £8,250 * 1.45 = £11,962.50 (or roughly £997 per month).

If the market rent for that property is only £850 per month, the mortgage application will be declined at 75% LTV. The investor must either put down a larger deposit to reduce the loan amount (and therefore the required rent) or find a higher-yielding property.

Social Mining Insight: The Refinance Trap

We continuously monitor platforms like Reddit (r/UKProperty) and Property118 to gauge real-time investor sentiment. A prevailing theme for 2025/2026 is the "refinance trap." Many investors who locked in 5-year fixed rates at 2% in 2021 are now facing remortgage rates of 4.5%. Because of the stringent ICR stress tests at these higher rates, many find they can no longer borrow the same amount they initially did, effectively trapping them on expensive Standard Variable Rates (SVR) unless they inject significant cash to reduce the LTV. This underscores the necessity of aggressive cash-flow management.

Strategy 2: The Limited Company (SPV) Approach

As previously mentioned, the landscape has decisively shifted toward corporate ownership. Investing via a Special Purpose Vehicle (SPV)—a limited company set up specifically to hold and manage property—is now the standard for serious investors.

If you are a higher-rate taxpayer purchasing a new property in 2026, buying in your personal name is almost certainly a strategic error.

The Financial Mechanics of an SPV

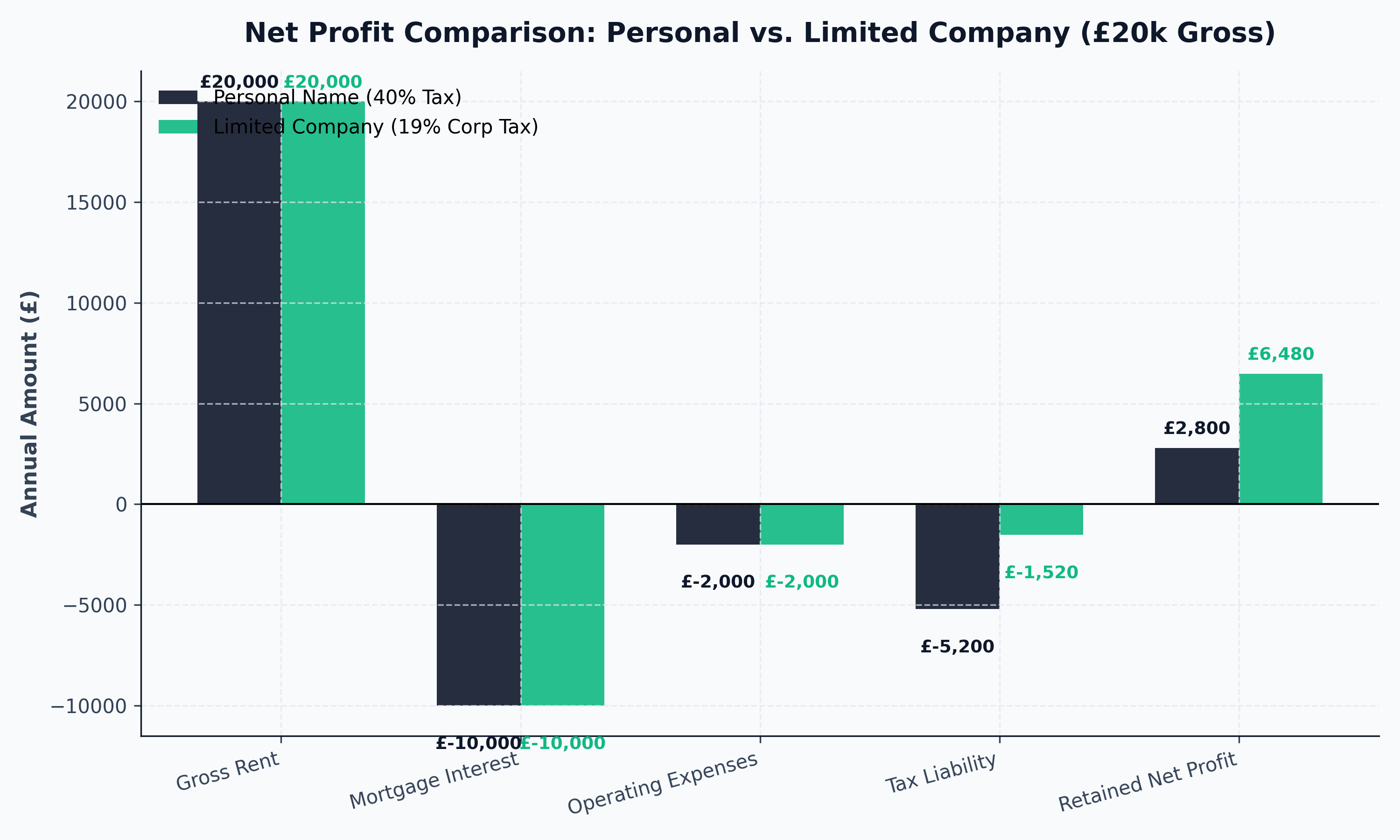

- Profit Extraction vs. Portfolio Growth:

- Personal Name: You are taxed on the profit immediately, regardless of whether you spend it or leave it in the bank. If you earn £100,000 from your day job, your property profits are immediately text at 40% or 45%.

- Limited Company: The company pays Corporation Tax (19% on profits up to £50,000; up to 25% on profits over £250,000). You only pay personal tax (Dividend Tax) when you extract the money from the company. If your goal is to acquire multiple properties, an SPV allows you to pay the lower Corporation Tax rate, retain the remaining 81% of the profit within the company wrapper, and use that gross capital to fund the next deposit. This accelerates compound growth dramatically.

- Full Interest Deductibility: Unlike personal ownership, limited companies are completely exempt from Section 24. A limited company treats mortgage interest as a standard business expense, deducting it fully from gross rental income before calculating taxable profit.

- More Generous Stress Testing: Because companies are not subject to the Section 24 tax penalty, lenders calculate their ICR at 125%, regardless of the directors' personal tax brackets. This allows SPVs to achieve higher leverage (borrow more money against the same rental income) than individuals.

(Figure 3: Waterfall Chart: Net Profit Comparison - Personal vs. Limited Company at 40% Tax Rate)

(Figure 3: Waterfall Chart: Net Profit Comparison - Personal vs. Limited Company at 40% Tax Rate)

The Downsides of Corporate Finance

It is not a universal panacea. Financing through an SPV comes with distinct compromises:

- Higher Mortgage Costs: Lenders view corporate lending as slightly higher risk. Consequently, SPV mortgage rates are typically 0.5% to 1.0% higher than personal BTL rates.

- Double Taxation on Income: If you need the rental income to live on now, an SPV is less efficient. The company pays Corporation Tax, and then you pay personal Dividend Tax when you withdraw the cash. (However, if you are a basic rate taxpayer, personal ownership might still be optimal).

- Administrative Overhead: Running a company requires filing annual accounts with Companies House, submitting corporation tax returns, and paying increased accountancy fees.

- Transferring Existing Properties is Expensive: You cannot simply "move" a personally owned property into a company. It legally constitutes a sale. The company must buy the property from you at market value, triggering Capital Gains Tax (CGT) for you personally, and Stamp Duty Land Tax (SDLT) plus the secondary home surcharge for the company.

Strategy 3: Cash Purchasing

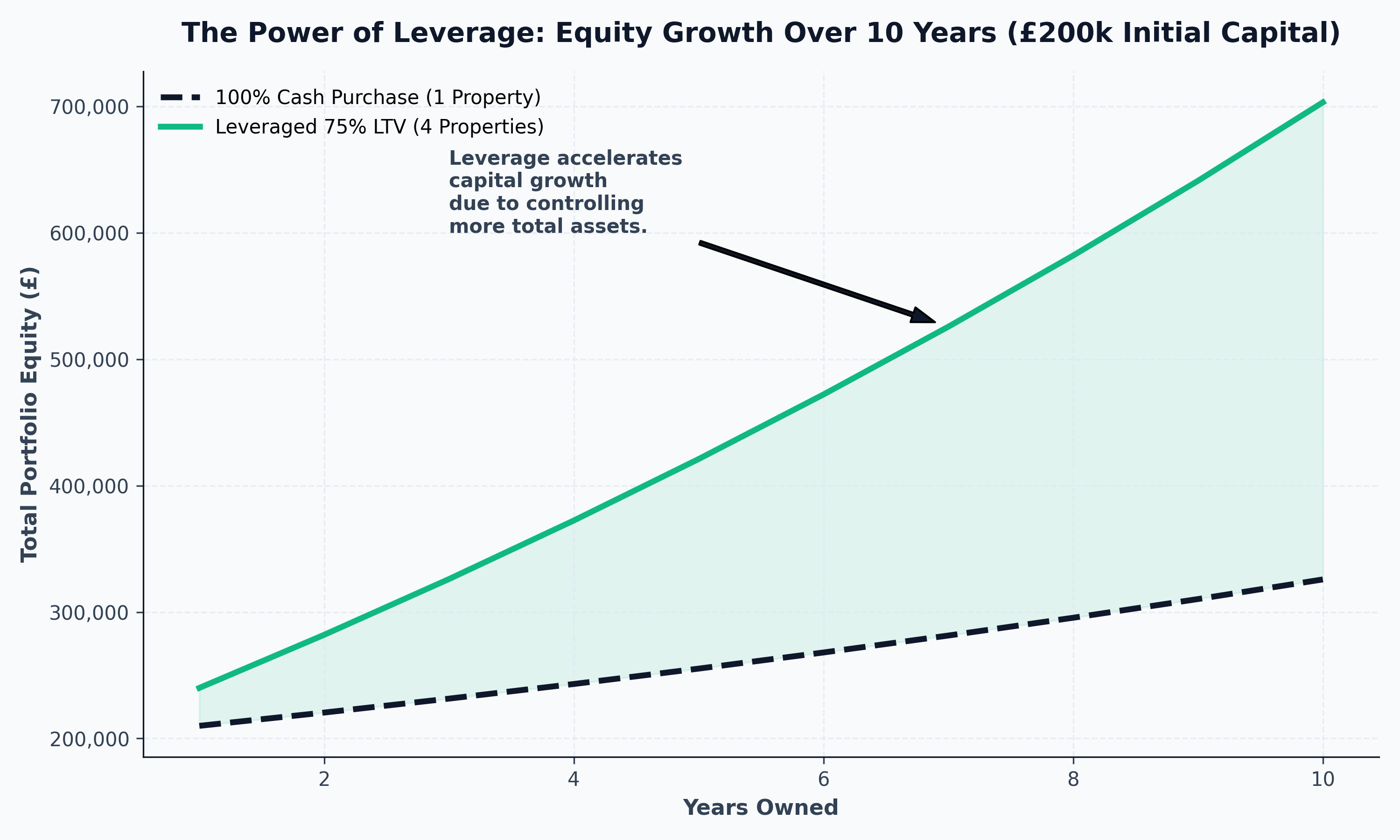

Leverage (using mortgages) is the traditional mechanism for accelerating property wealth, but there is a growing contingent of investors opting to buy with 100% cash. This strategy fundamentally alters the risk-reward dynamic.

The Argument for Cash

- Absolute Risk Mitigation: A property owned outright cannot be repossessed if interest rates spike or if the property sits vacant for six months. It provides ultimate peace of mind.

- Maximized Monthly Cash Flow: Without a mortgage payment consuming 50% to 70% of the gross rent, your monthly net income is maximized. Every pound of rent (minus maintenance and tax) goes into your pocket.

- Purchasing Power and Speed: Cash buyers are the apex predators of the property market. They can complete transactions in weeks rather than months, bypassing lender valuations and underwriting delays. This speed and certainty allow cash buyers to aggressively negotiate purchase prices, often securing properties significantly below market value, particularly at auctions or from motivated sellers.

(Figure 4: Cash vs Mortgage: Cash Flow vs Total ROI over 10 Years)

(Figure 4: Cash vs Mortgage: Cash Flow vs Total ROI over 10 Years)

The Severe Limitations of Cash

While safe, buying in cash is highly inefficient from a return-on-capital methodology.

The Opportunity Cost of Leverage: Imagine you have £200,000 in cash to invest.

- Scenario A (Cash): You buy one property for £200,000. It generates £12,000 a year in rent. At a 5% capital growth rate, the property increases in value by £10,000 in year one. Your return is £22,000.

- Scenario B (Leverage): You use the £200,000 to put down four £50,000 deposits (25%) on four £200,000 properties. You now control £800,000 worth of real estate. At a 5% capital growth rate, your portfolio increases in value by £40,000 in year one. You also collect rent from four properties (though this is offset by four mortgage payments).

By eschewing leverage, you drastically limit your exposure to capital appreciation, which is historically where the vast majority of property wealth is generated.

Furthermore, deploying £200,000 into a single asset represents terrible diversification. If that specific property has a major issue (e.g., subsidence, a nightmare tenant), 100% of your investment capital is compromised.

Strategy 4: The BRRR Method (Buy, Refurbish, Refinance, Rent)

For those looking to rapidly scale their portfolio without requiring endless injections of fresh capital, the BRRR strategy remains the most mathematically sound approach. It operates on the principle of forced appreciation.

The Mechanics of BRRR Finance

- Buy: You purchase a dilapidated, unmortgageable, or highly undervalued property. Because standard BTL lenders will not lend on unhabitable properties (e.g., properties missing a functioning kitchen or bathroom), you must finance the initial purchase using cash or Bridging Finance.

- Bridging Finance is short-term, high-interest debt (often 0.7% to 1.5% per month) designed to fund a purchase for 6 to 12 months. It is secured against the asset.

- Refurbish: You deploy capital to renovate the property, modernizing it and bringing it up to a high standard, aiming to significantly increase its market value.

- Refinance: Once the refurbishment is complete and the property is habitable, you apply for a standard, long-term BTL mortgage based on the new, higher valuation (the Gross Development Value or GDV).

- Rent: You place a tenant in the newly refurbished property, generating the income required to satisfy the lender's ICR stress test.

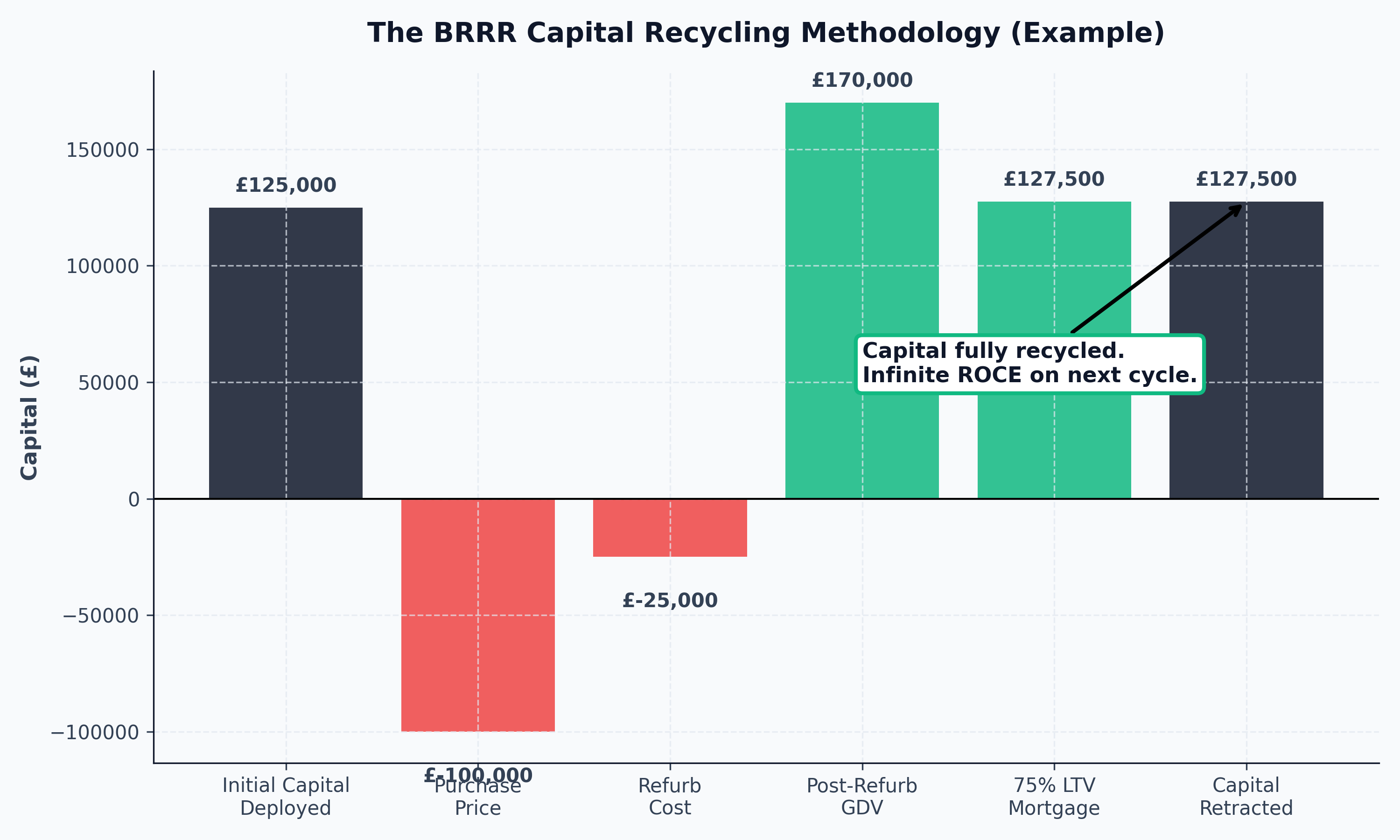

(Figure 5: The BRRR Capital Recycling Cycle)

(Figure 5: The BRRR Capital Recycling Cycle)

The Goal: Infinite ROI

The objective of BRRR is to pull all (or most) of your initial capital back out of the deal during the refinance phase.

Data Snapshot Example:

- Purchase Price (Cash): £100,000

- Refurbishment Costs: £25,000

- Total Capital Deployed: £125,000

- New Valuation (Post-Refurb): £170,000

- New BTL Mortgage (75% of new value): £127,500

In this scenario, the investor receives £127,500 from the new mortgage. This pays off the initial £125,000 investment plus leaves £2,500 in the bank. They now own a cash-flowing asset with zero of their own money left in the deal. Their Return on Capital Employed (ROCE) is technically infinite.

The Risks of BRRR in 2026

BRRR is an advanced strategy with significant execution risk.

- The Valuation Gap: The entire strategy hinges on the surveyor agreeing with your post-refurbishment valuation. If you spend £25,000 but the surveyor only down-values the end product at £140,000, you will leave significant capital trapped in the deal.

- Build Cost Inflation: Material and labor costs remain highly volatile. A project that runs over budget destroys the profit margin.

- The Six-Month Rule: Most traditional mortgage lenders will not allow you to refinance a property until you have owned it for at least six months. This means you must cover the expensive bridging finance interest for a minimum of half a year, regardless of how fast you finish the build.

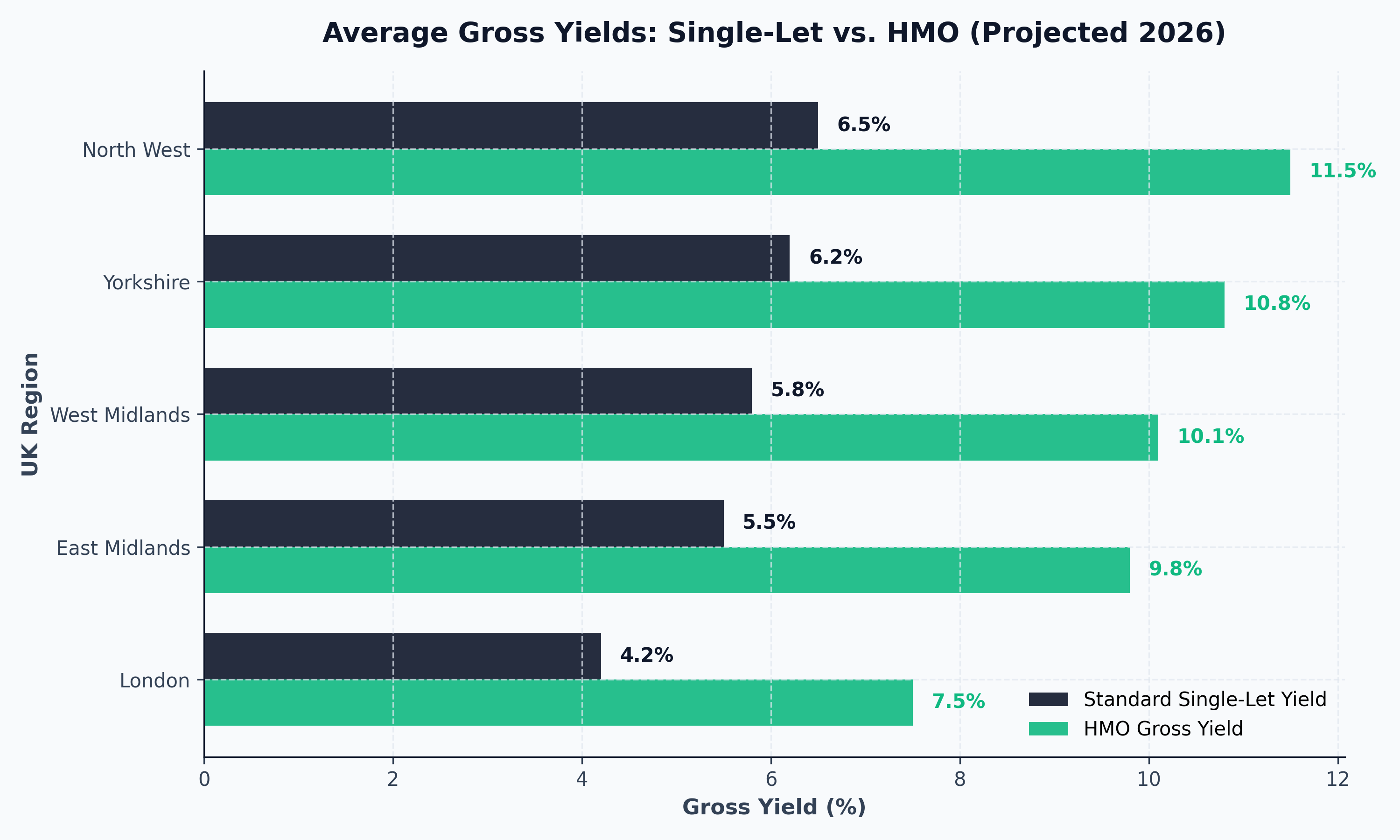

Strategy 5: Financing HMOs and Multi-Lets

Houses in Multiple Occupation (HMOs) involve renting individual rooms within a single property to unrelated tenants. This strategy is highly attractive because it significantly increases the gross rental yield compared to single-let properties.

However, financing an HMO is vastly more complex.

(Figure 6: Average Yields: Single Let vs HMO by Region)

(Figure 6: Average Yields: Single Let vs HMO by Region)

Commercial vs. Standard BTL Valuation

When you finance a standard property, the lender values it based on comparable local sales ("bricks and mortar" valuation).

When you finance an established, licensed HMO (especially those with 6+ rooms), specialized lenders may offer a Commercial Valuation. A commercial valuation ignores the bricks-and-mortar value and instead values the asset as a revenue-generating business, applying a yield multiple to the net income.

If you generate £40,000 a year in rent from a large HMO, a commercial valuation will often result in a significantly higher appraised value than a standard valuation. This allows the investor to borrow considerably more money against the asset.

The Financing Hurdles for HMOs

- Experience Requirements: Most standard BTL lenders simply will not lend on an HMO. You must use specialized HMO mortgage products. Crucially, almost all specialized lenders require you to have proven experience as a landlord (usually 1-2 years owning standard BTLs) before they will extend debt for an HMO.

- Higher Rates and Lower LTVs: Because HMOs are considered higher risk (more wear and tear, higher tenant turnover, regulatory complexity), the interest rates are typically higher than standard BTLs, and maximum LTVs may be capped at 70% rather than 75%.

- Licensing and Compliance: Your financing is strictly contingent upon holding the correct regulatory documentation. Lenders will demand proof of Article 4 compliance (planning permission to convert a family home to an HMO) and the appropriate mandatory or additional council licenses.

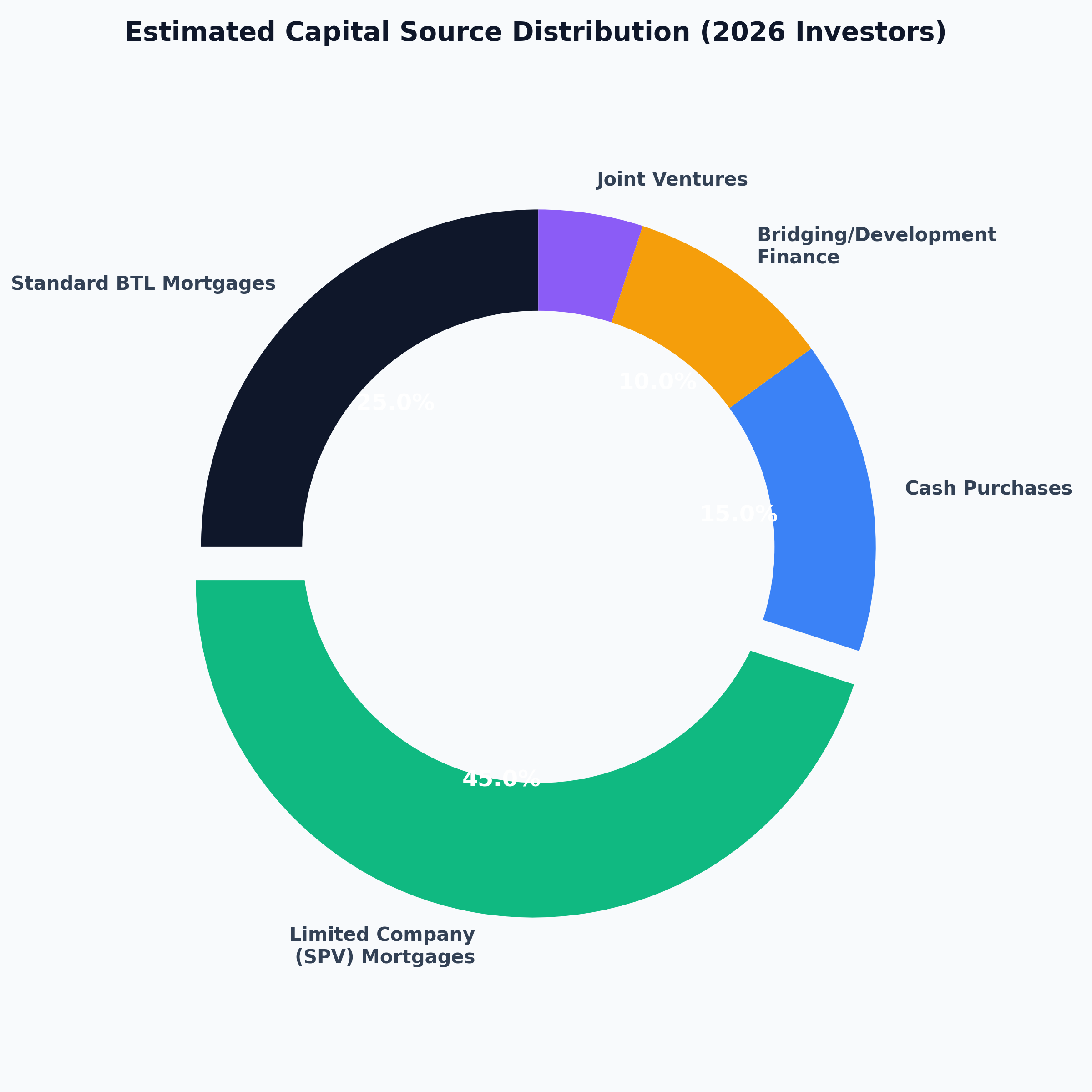

Alternative Financing Models

While mortgages, cash, and bridging are the pillars of the industry, sophisticated investors utilize secondary structures.

1. Joint Ventures (JVs)

If you lack capital but possess time and expertise (deal sourcing, project management), you can partner with a "cash investor." The cash partner funds the deposit and the refurbishment, while the expert partner manages the execution. Profits and equity are split (often 50/50). This requires rigorous legal structuring and shareholders' agreements to protect both parties.

2. Seller Finance (Lease Options)

A Lease Option Agreement (LOA) allows you to take control of a property without buying it or using a mortgage. You agree to lease the property from a motivated seller (who perhaps cannot sell on the open market or is in negative equity) for a fixed monthly sum, with the option to purchase the property at a pre-agreed price at a set date in the future (e.g., 5 years). You then act as the landlord, charging market rent and pocketing the difference. This requires zero deposit, but is highly complex legally and relatively rare in practice.

3. Developer Payment Plans

When purchasing entirely off-plan direct from a developer, developers often allow you to pay the deposit in installments over the 18-24 month build period. Once the property is complete, you then secure a standard BTL mortgage to pay the remaining balance. This reduces the immediate capital outlay.

(Figure 7: Funding Sources Breakdown: Where 2026 Investors Source Capital)

(Figure 7: Funding Sources Breakdown: Where 2026 Investors Source Capital)

Preparing Your Application: What Lenders Want to See

To secure the best financing terms in an increasingly rigorous regulatory environment, investors must approach lenders with institutional-grade preparation.

- Impeccable Credit File: Lenders scrutinize credit histories meticulously. Ensure you are on the electoral roll, have zero missed payments, and maintain low credit utilization ratios on personal cards. Use platforms like Experian and Checkmyfile months before applying.

- Clean Bank Statements: Lenders will request 3-6 months of personal bank statements to assess your financial prudence. Avoid using overdrafts, relying on payday loans, or exhibiting erratic spending patterns.

- A Track Record (If Scaling): If you are expanding your portfolio, lenders will analyze your existing properties. They want to see that your current assets are well-maintained, tenanted, and generating strong cash flow. Keep meticulous spreadsheets of your portfolio's performance.

- Proof of Deposit Source: Under strict Anti-Money Laundering (AML) regulations, you must prove a clear, auditable trail for your deposit funds. Whether it is savings, an inheritance, or an equity release from another property, the documentation must be watertight.

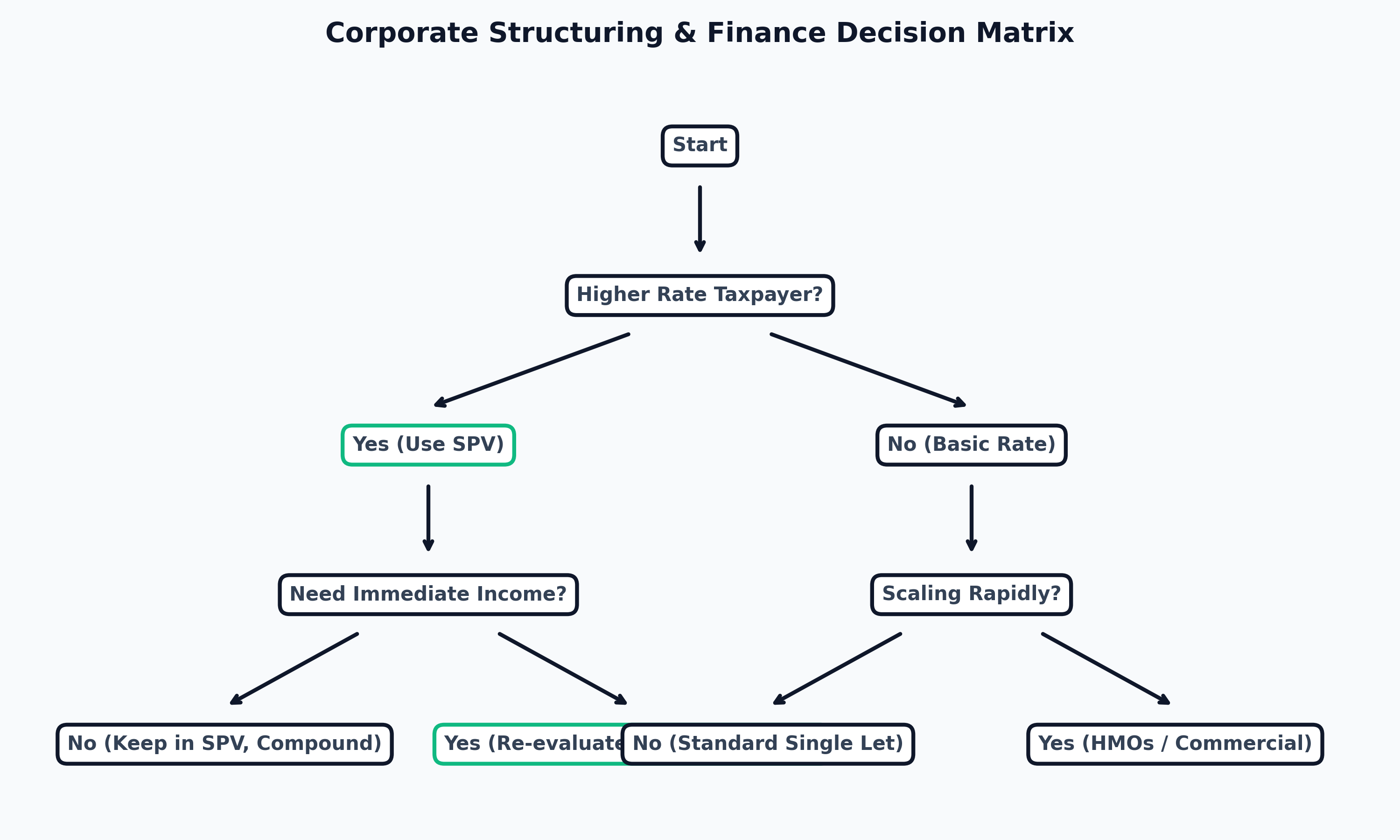

The Ultimate Checklist: Financing Your Next Deal

Navigating the financial maze in 2026 requires discipline. Before committing capital to any asset, run through this execution checklist:

- Determine Corporate Structure: Speak to a property tax accountant. Calculate the net difference of buying in your personal name vs. a Limited Company based on your specific life circumstances and income bracket.

- Engage a Whole-of-Market Broker: Do not go direct to a high-street bank. Work with a specialized BTL mortgage broker who has access to the full spectrum of lenders, including those that do not deal directly with the public.

- Run the Stress Test: Do not trust the agent's "projected yield." Run the numbers yourself. Can the property sustain a 145% ICR at a 5.5% stress rate? If the math fails, walk away from the deal.

- Model the EPC Reality: By 2030, properties will require an EPC rating of C. Factor in the capital cost of retrofitting (insulation, heat pumps) into your initial financial model. If upgrading a property will cost £15,000, that must be deducted from your available deposit capital.

- Secure an Agreement in Principle (AIP): Obtain an AIP before making offers. In a competitive market, sellers prioritize buyers holding proof of funds.

(Figure 8: Strategic Decision Tree: Which Finance Route Should I Choose?)

(Figure 8: Strategic Decision Tree: Which Finance Route Should I Choose?)

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial, legal, or tax advice. Property prices can go down as well as up. Always consult with a qualified, FCA-regulated financial advisor, mortgage broker, and certified accountant tailored to your specific circumstances before making any investment decisions.

(Figure 9: The Impact of Section 24 on Personal Yields)

(Figure 9: The Impact of Section 24 on Personal Yields)

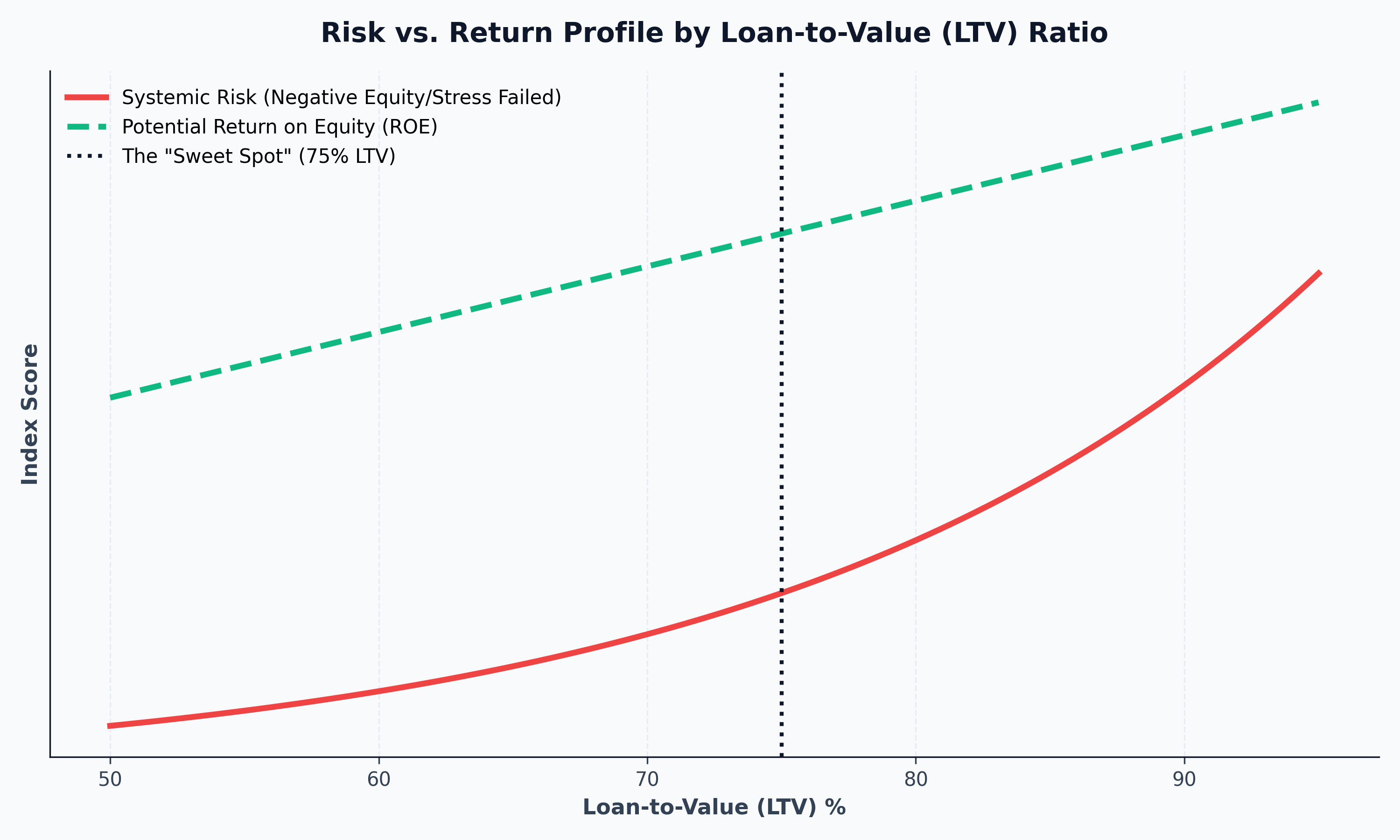

(Figure 10: Loan-to-Value (LTV) Risk Distribution Curve)

(Figure 10: Loan-to-Value (LTV) Risk Distribution Curve)

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →