The question every property investor asks eventually — "what's the best type of property to invest in?" — has no universal answer, but it does have a clear framework. The right investment type depends entirely on your capital, risk tolerance, time commitment, and whether you're optimising for yield, growth, or both.

This is the definitive breakdown. No sales pitches. No "passive income with zero effort" fantasies. Just the numbers, the trade-offs, and the strategies that actually work in 2026's UK market.

The Investment Landscape in 2026

Before diving into property types, understand the environment you're operating in.

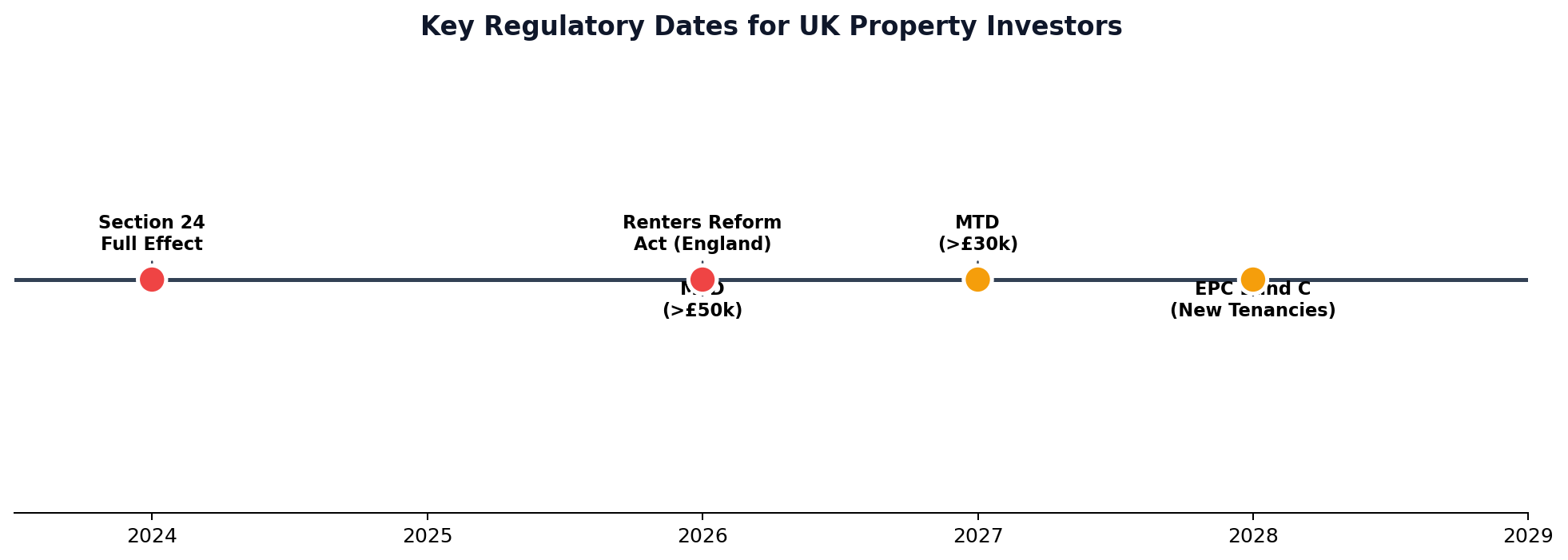

House prices are forecast to rise 2-4% nationally in 2026, after a largely flat 2026. The Bank of England base rate is settling around 3.75-4%, making mortgage affordability significantly better than the 5.25% peak. The Renters Reform Act comes into full force in England from May 2026, abolishing Section 21 "no-fault" evictions. Making Tax Digital applies to landlords earning over £50,000 from April 2026.

The market is professionalising. Amateur landlords who bought a flat "because property always goes up" are exiting. Strategic investors who understand their numbers — yield, cash flow, stress-tested returns — are the ones building wealth.

Standard Buy-to-Let: The Foundation Strategy

Best for: Beginners, hands-off investors, long-term wealth building

Standard buy-to-let remains the backbone of UK property investment. You buy a residential property, let it to a single household, and collect monthly rent. It's straightforward, well-understood, and the easiest strategy to finance.

The Numbers in 2026

| Metric | Typical Range |

|---|---|

| Gross yield | 5-7% (regional dependent) |

| Net yield (after costs) | 3-5% |

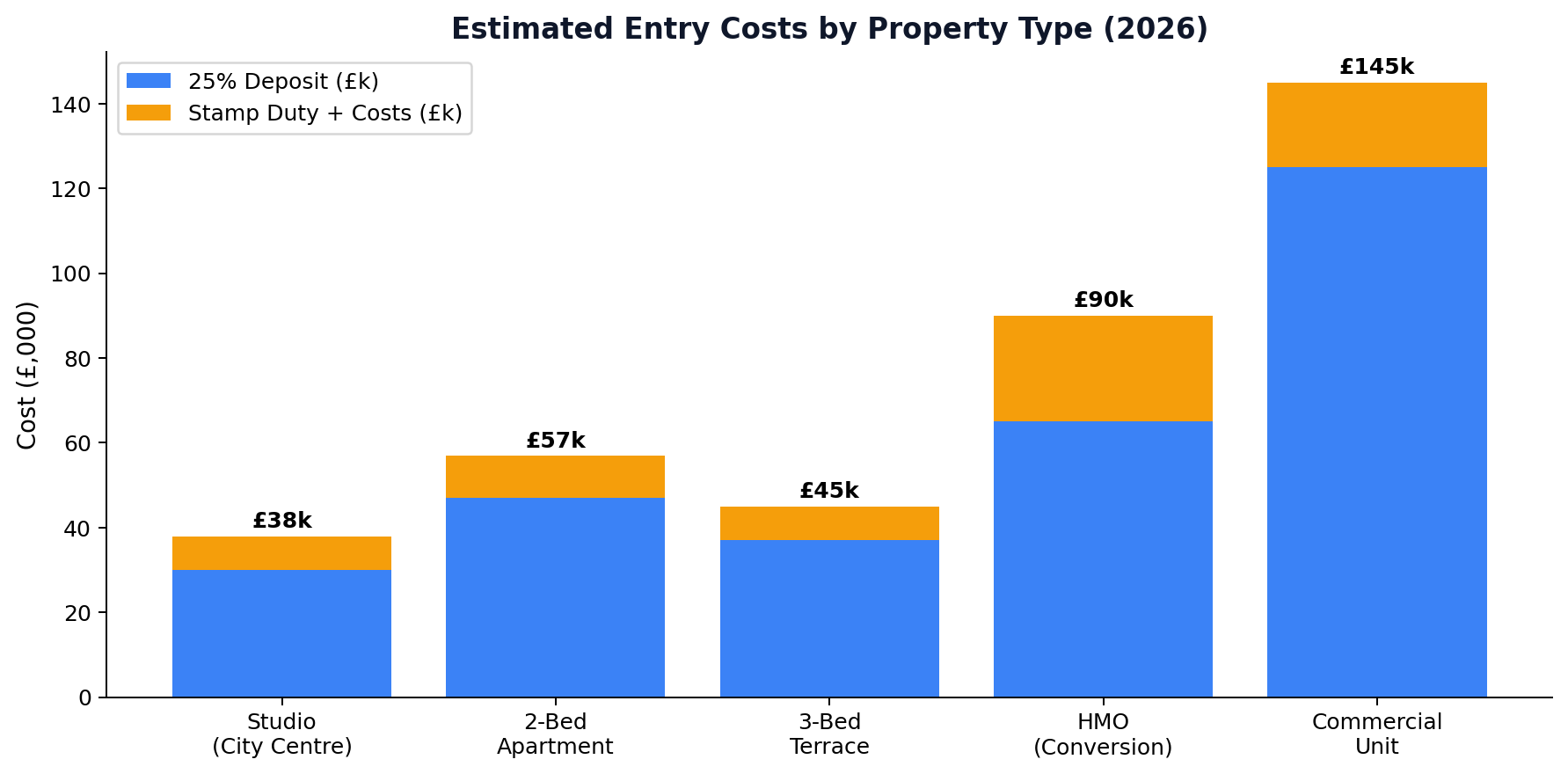

| Entry capital needed | £30,000-£75,000 (25% deposit + costs) |

| Average monthly rent (UK) | £1,300+ |

| Void periods | 2-4 weeks per year |

| Management cost | 8-12% of rent if outsourced |

The best buy-to-let locations in 2026 are overwhelmingly in the North and Midlands. Liverpool offers gross yields of 7-8%, Manchester 6-6.5%, Leeds 5.5-6.5%, and Nottingham 6-7%. London, by contrast, typically delivers 3-4% gross yields — barely covering mortgage payments.

When Buy-to-Let Works

- You want predictable, stable income with minimal drama

- You're investing via an SPV (limited company) for tax efficiency

- You're targeting properties that meet or exceed EPC Band C

- You have a long-term horizon (10+ years)

When It Doesn't

- You need high cash flow immediately

- You're buying in expensive southern areas where yields are compressed

- You haven't stress-tested against rate rises to 6%+

Houses in Multiple Occupation (HMOs): The Yield Maximiser

Best for: Experienced investors, cash flow focused, higher risk tolerance

HMOs — properties rented by the room to three or more unrelated tenants — generate significantly higher yields than standard buy-to-let. Where a three-bedroom terraced house might generate £900/month as a single let, the same property as an HMO could produce £1,500-£2,000/month.

The Numbers in 2026

| Metric | Typical Range |

|---|---|

| Gross yield | 8-14% |

| Net yield | 5-9% |

| Entry capital needed | £50,000-£120,000 |

| Room rents | £400-£700/month per room |

| Void risk | Lower (spread across tenants) |

| Management intensity | High |

The Regulation Reality

HMOs face significantly more regulation than standard buy-to-let. Mandatory licensing applies to any property with five or more occupants forming two or more households. Many councils have introduced Additional Licensing schemes covering smaller HMOs. Article 4 Directions in numerous cities mean you need planning permission to convert a dwelling to an HMO.

The key phrase from experienced HMO investors in 2026: "vanilla HMOs are not working anymore." Success requires premium positioning — quality furnishing, en-suite bathrooms where possible, communal spaces that actually work, and professional management. The days of six beds crammed into a Victorian terrace with one bathroom are numbered.

The Best HMO Cities

- Liverpool: Strong student and professional demand, relatively affordable conversions

- Manchester (Fallowfield, Rusholme): Yields of 8-9% in student areas

- Leeds: Growing professional tenant base, particularly in the medical and financial sectors

- Nottingham: Major university city with consistent demand

- Birmingham: Large young professional population, strong rental demand

Serviced Accommodation: The Cash Flow King

Best for: Active investors, hospitality-minded, high cash flow requirements

Serviced accommodation — essentially running a short-term rental like a hotel without the staff — can generate the highest cash flow of any residential strategy. A two-bedroom apartment that produces £1,200/month as a standard let could generate £2,500-£4,000/month as serviced accommodation.

The Numbers in 2026

| Metric | Typical Range |

|---|---|

| Gross income potential | 2-3x standard rental |

| Net yield | 7-15% (when managed well) |

| Entry capital needed | £40,000-£100,000+ |

| Average occupancy target | 70-80% |

| Operating costs | Higher (cleaning, utilities, platform fees) |

| Management intensity | Very high |

The Reality Check

Serviced accommodation is not passive income. It's a hospitality business that happens to use property. You need:

- Consistent marketing across Airbnb, Booking.com, and direct channels

- Professional cleaning between every guest

- 24/7 guest communication

- Furniture and styling investment

- Local council compliance (many now require planning permission for short-term lets)

- Insurance specifically covering short-term let use

The investors who succeed with serviced accommodation treat it as a business, not a property investment. The ones who fail are typically landlords who listed their buy-to-let on Airbnb and expected the money to start flowing.

Best Locations

Corporate lets perform best in city centres near business districts — Manchester, Birmingham, Edinburgh, and Bristol are the strongest performers. Holiday lets work best in tourist areas — the Lake District, Cornwall, Scottish Highlands, and coastal towns.

Commercial Property: The Institutional Play

Best for: Experienced investors with larger capital, seeking long leases and stability

Commercial property is a fundamentally different asset class from residential. Leases are longer (typically 5-25 years), tenants are responsible for more costs (under Full Repairing and Insuring leases), and yields can be attractive — but the entry costs and risks are different.

The Numbers in 2026

| Metric | Typical Range |

|---|---|

| Gross yield | 5-9% |

| Lease length | 5-25 years |

| Entry capital needed | £100,000-£500,000+ |

| Tenant responsibility | Usually repairs + insurance |

| Void risk | Higher (harder to fill) |

| Capital growth | Sector dependent |

The Strongest Sectors in 2026

Industrial and Logistics: This is the standout sector. E-commerce growth continues to drive demand for warehouses, distribution centres, and last-mile delivery hubs near major cities. Industrial property has consistently outperformed other commercial sectors for capital growth and rental growth.

Healthcare Real Estate: Investment in UK healthcare real estate hit a record £12 billion in 2026. Care homes, GP surgeries, and hospital buildings offer long leases backed by essential service demand. Ageing demographics make this a structural growth story.

Student Accommodation (Purpose-Built): PBSA offers reliable demand in university cities, often with management companies handling operations. Cities like Liverpool, Manchester, Leeds, Nottingham, and Birmingham are the strongest markets.

Retail: Selective retail — prime shopping centres, retail parks with anchor tenants, and convenience retail — is recovering after years of headwinds. Avoid secondary high street units.

Off-Plan Property: The Timing Play

Best for: Investors seeking below-market entry, capital growth, acceptance of construction risk

Off-plan investing — buying a property before or during construction — allows you to lock in today's price on a property that won't be completed for 18-36 months. If house prices rise during construction, you build instant equity.

The Advantages

- Below-market entry price (developers offer discounts to early buyers)

- Capital appreciation during build period

- Brand-new property = minimal maintenance, highest EPC ratings, most attractive to tenants

- Staged payment structure reduces immediate capital outlay

The Risks

- Developer insolvency — your deposit may be at risk if the developer goes bust

- Completion delays — your money is tied up with no rental income

- Market downturn during build — the completed property could be worth less than you paid

- Snagging issues and build quality concerns

Off-plan works best when you're buying from an established, well-capitalised developer in a location with genuine demand fundamentals. It works worst when you're buying from a marketing company that's reselling a developer's units at an inflated price with "guaranteed" rental returns.

REITs and Property Funds: The Hands-Off Alternative

Best for: Investors who want property exposure without ownership headaches

Real Estate Investment Trusts allow you to invest in property through the stock market. You buy shares in a REIT, which owns and manages a portfolio of income-generating properties. REITs are required by law to distribute at least 90% of their rental income as dividends.

Why Consider REITs

- Liquidity: Buy and sell like any other share

- Diversification: Exposure to dozens or hundreds of properties

- No management: No tenants, no repairs, no midnight phone calls

- Low entry: Start with as little as £50

- Tax efficiency: Hold within an ISA for tax-free dividends and gains

- Professional management: Experienced teams making allocation decisions

The Trade-Off

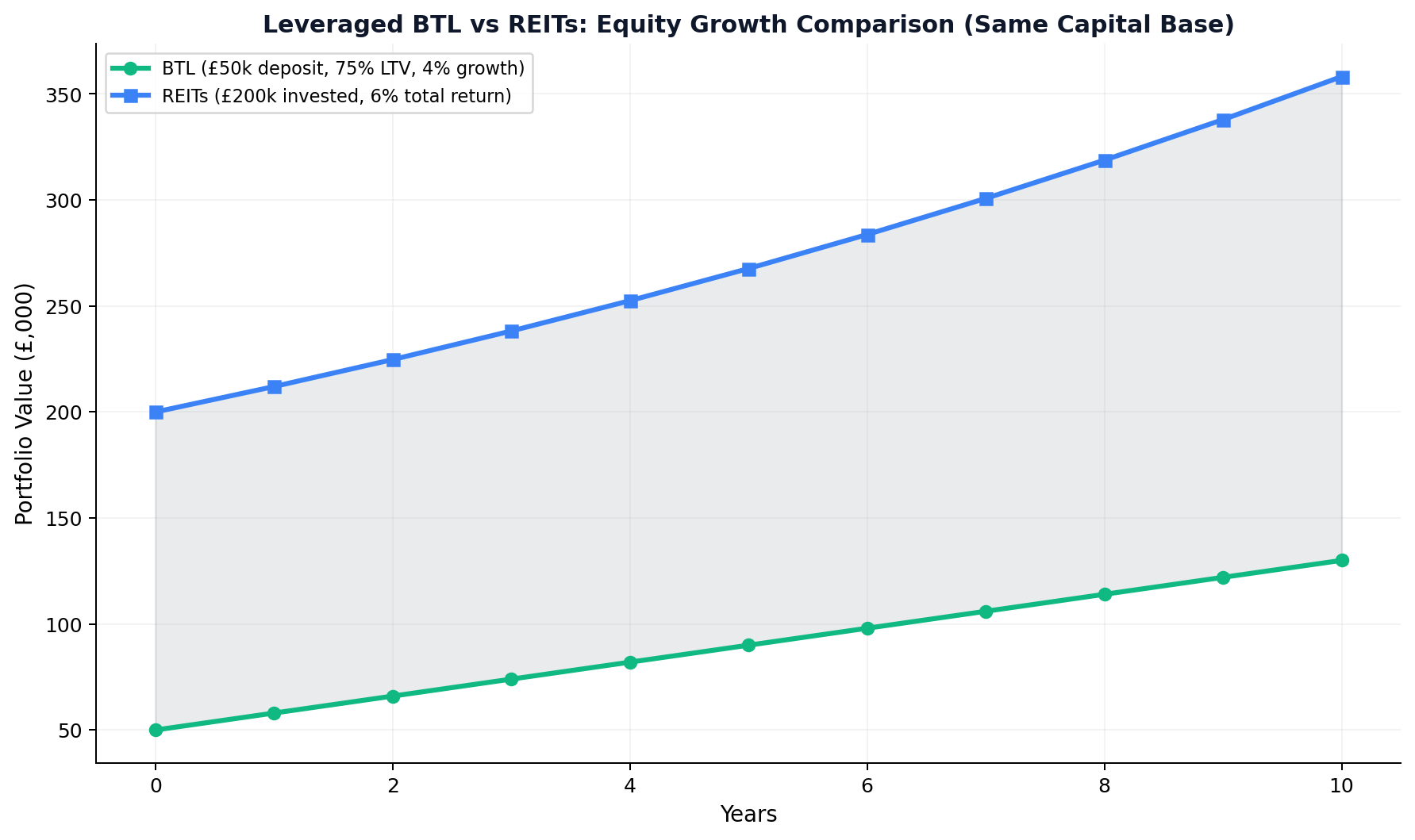

You sacrifice control, leverage benefits, and the forced savings discipline that comes with mortgage repayment. A £200,000 buy-to-let purchased with a 75% LTV mortgage gives you 4:1 leverage — a £200,000 REIT investment gives you 1:1. In a rising market, leverage amplifies returns. In a falling market, it amplifies losses.

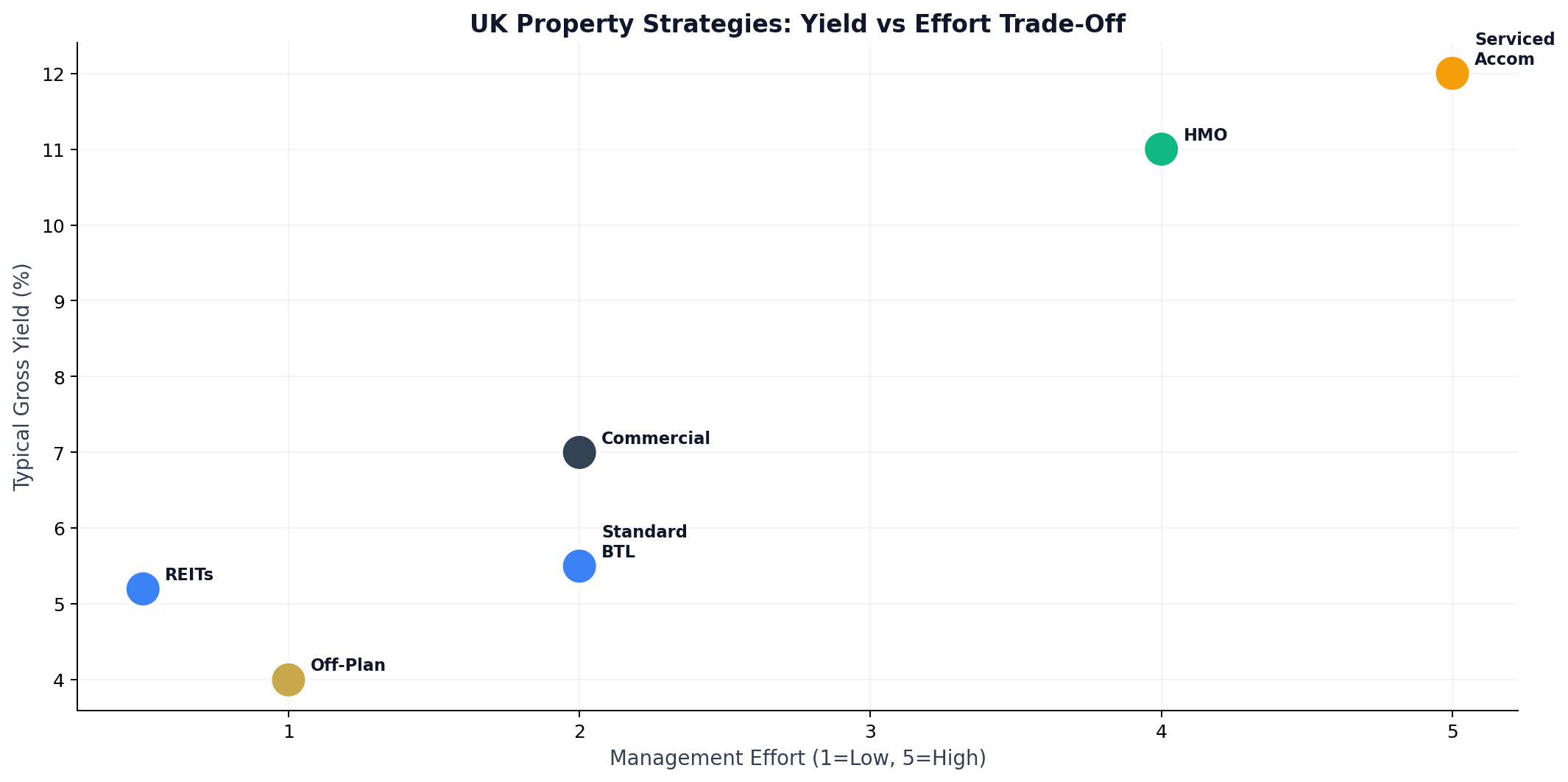

The Strategy Comparison Matrix

| Strategy | Yield | Capital Growth | Effort | Capital Needed | Risk |

|---|---|---|---|---|---|

| Standard BTL | ⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐ | ⭐⭐⭐ | ⭐⭐ |

| HMO | ⭐⭐⭐⭐⭐ | ⭐⭐ | ⭐⭐⭐⭐ | ⭐⭐⭐⭐ | ⭐⭐⭐ |

| Serviced Accom | ⭐⭐⭐⭐⭐ | ⭐⭐ | ⭐⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐⭐ |

| Commercial | ⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐ | ⭐⭐⭐⭐⭐ | ⭐⭐⭐ |

| Off-Plan | ⭐⭐ | ⭐⭐⭐⭐ | ⭐ | ⭐⭐⭐ | ⭐⭐⭐⭐ |

| REITs | ⭐⭐⭐ | ⭐⭐⭐ | ⭐ | ⭐ | ⭐⭐ |

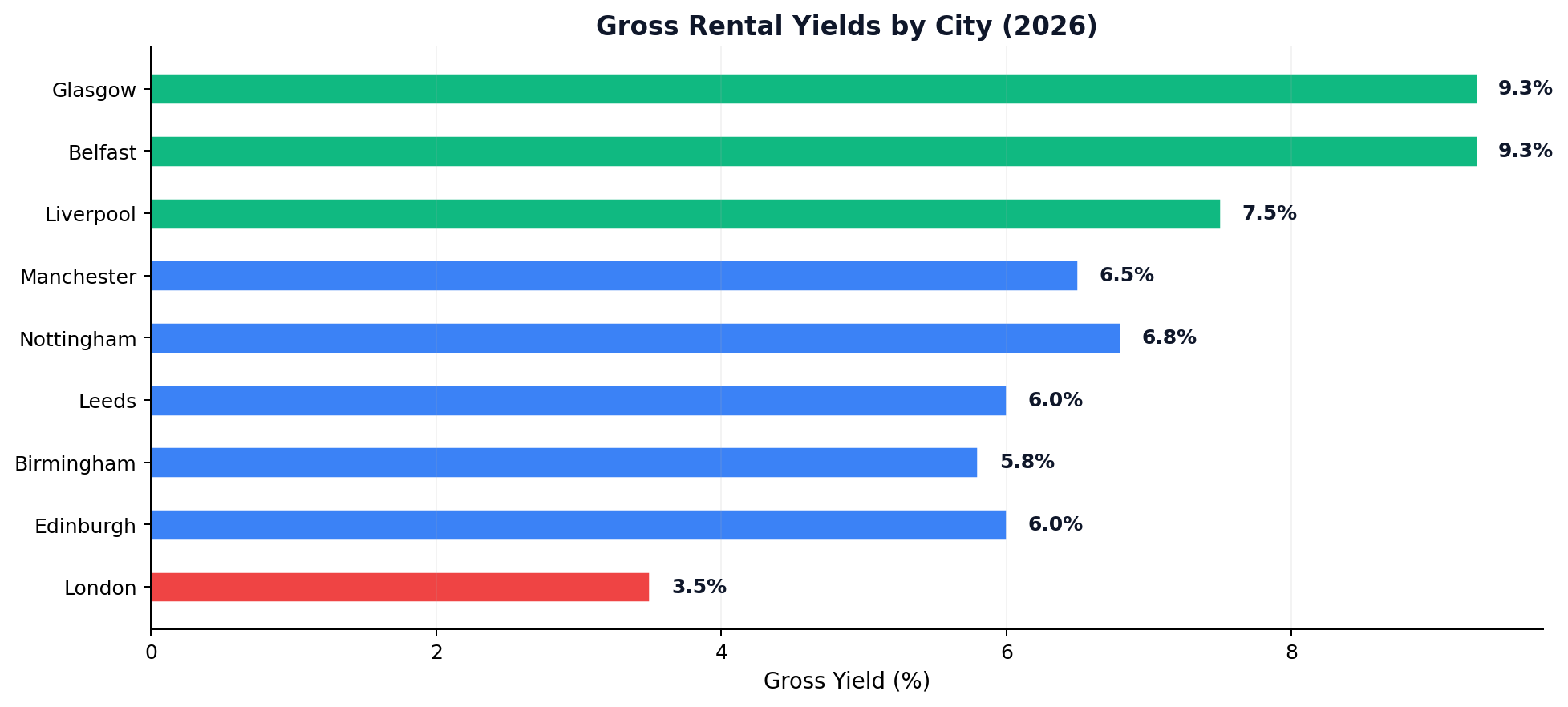

Where to Invest: The Top Cities in 2026

The data is clear on which cities offer the best fundamentals:

Glasgow leads for overall residential investment value — gross yields averaging 9.3%, strong economic resilience, and entry prices well below the UK average.

Liverpool delivers consistently high yields (7-10%), backed by £14 billion in regeneration projects and one of the lowest average property prices of any major UK city.

Manchester combines strong yields (6-6.5%) with significant capital growth potential, driven by a young, growing population and a booming tech sector.

Birmingham benefits from HS2 infrastructure investment, a large tenant market, and forecast price growth of 19.9% by 2028.

Edinburgh offers stability, strong employment, and growing demand — but at higher entry costs than other Scottish cities.

Belfast combines the UK's lowest price-to-earnings ratio with gross yields of 9.3%, though the market is smaller and less liquid.

The Decision Framework

Instead of asking "what's the best type of property to invest in," ask yourself these five questions:

How much time can you commit? If the answer is "minimal," stick with standard BTL or REITs. If "significant," HMO or serviced accommodation offers higher returns for more work.

What's your capital position? Under £50,000 available? Standard BTL in the North or REITs. Over £100,000? The full range of strategies opens up.

What's your priority — yield or growth? Yield-focused investors should look at HMOs and northern cities. Growth-focused investors should target regeneration areas and off-plan opportunities.

What's your tax situation? Higher-rate taxpayers should strongly consider SPV structures. Basic-rate taxpayers may still benefit from personal ownership.

What's your exit timeline? Short-term flippers need different strategies from long-term holders. The best returns in property come from holding through full market cycles (7-10+ years).

The Regulatory Landscape: What Every Investor Must Know

The 2026 regulatory environment demands attention:

- Renters Reform Act (England, May 2026): Abolishes Section 21, introduces rolling periodic tenancies. Landlords must now follow proper grounds for possession.

- EPC Requirements: Minimum Band C being phased in for new tenancies. Properties below Band C will become harder to let and eventually unlettable.

- Making Tax Digital (April 2026): Landlords earning over £50,000 from property must maintain digital records and file quarterly updates.

- Section 24 (In Full Effect): Mortgage interest relief is now a basic-rate tax credit only. Higher-rate taxpayers in personal ownership feel this most acutely.

FAQ: Best Type of Property to Invest in UK

What type of UK property gives the highest returns? HMOs typically offer the highest gross yields (8-14%), but require significantly more management and regulation compliance. Standard buy-to-let in northern cities offers the best balance of yield and simplicity for most investors.

Is buy-to-let still worth it in 2026? Yes, but only with the right numbers. Properties must cash flow positively after all costs including mortgage payments stress-tested at 6-7%. Focus on high-yield locations in the North and Midlands rather than the South.

Should I buy property through a limited company? If you're a higher-rate taxpayer planning to build a portfolio, an SPV structure is almost always more tax-efficient. It allows full mortgage interest deduction against rental income and offers lower corporation tax rates (25%) versus higher-rate income tax (40-45%).

Is commercial property a good investment for beginners? Generally no. Commercial property requires larger capital, deeper market knowledge, and carries higher void risk. Start with residential buy-to-let and graduate to commercial once you have experience and capital.

What's the minimum deposit for a buy-to-let? Most buy-to-let lenders require 25% deposit. On a £150,000 property, that's £37,500 plus approximately £5,000-£8,000 in purchase costs (stamp duty, legal fees, surveys).

Which UK city has the best rental yields? Glasgow and Belfast lead with average gross yields around 9.3%. Liverpool follows closely at 7-10%, then Manchester at 6-6.5%. London consistently underperforms for yield at 3-4%.

📚 Related Reading

- Property Equity Investors UK: The Hard Truth About Building Wealth Through Bricks in 2026

- Property Sourcing Companies UK: The Complete Investor's Guide

- How to Reduce Taxes Legally in the UK

- Low-Risk Investments That Actually Work

- How to Start Over Financially

📚 Related Reading

- Best Capital Growth Property UK: Where Property Prices Are Actually Heading in 2026 and Beyond

- Passive Income Property UK: How to Build a Rental Portfolio That Actually Pays You in 2026

- Property Investments Manchester: The Definitive Investor's Guide to the UK's Most Dynamic City in 2026

- Buy dirt

- Hobbies That Make Money: Real "Cheat Codes" for Turning Your Passion Into Profit

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →