Houses in Multiple Occupation (HMOs) remain the highest-yielding residential asset class in the UK. A conventional buy-to-let (BTL) property in Manchester or Birmingham might generate a 5% to 6% gross yield. A well-structured, fully licensed 6-bed HMO in the same city can generate 12% to 15% gross yield, effectively doubling or tripling the income of the standard BTL model.

However, HMO finance is categorically different from standard BTL finance. High-street lenders (Barclays, NatWest, Halifax) will not touch HMOs. The licensing regime, fire safety compliance, Article 4 Direction restrictions, and room-size regulations create a labyrinth of underwriting complexity that only specialist commercial lenders will entertain.

If you are asking "How do I finance a House in Multiple Occupation?", this 3,000-word audit will walk you through every financial instrument available in 2026: specialist HMO mortgages, bridging-to-term strategies, SPV structuring for tax efficiency, and the precise mathematics of whether HMO yields genuinely survive after licensing and compliance capital expenditure.

What is a House in Multiple Occupation?

A House in Multiple Occupation is a residential property rented to three or more tenants forming two or more separate households, who share basic amenities such as a kitchen or bathroom.

Under the Housing Act 2004, any property meeting this definition requires a mandatory HMO licence from the local authority. Since October 2018, this applies to all qualifying HMOs regardless of the number of storeys—the previous exemption for properties under three storeys was removed.

The Commercial Logic of HMOs

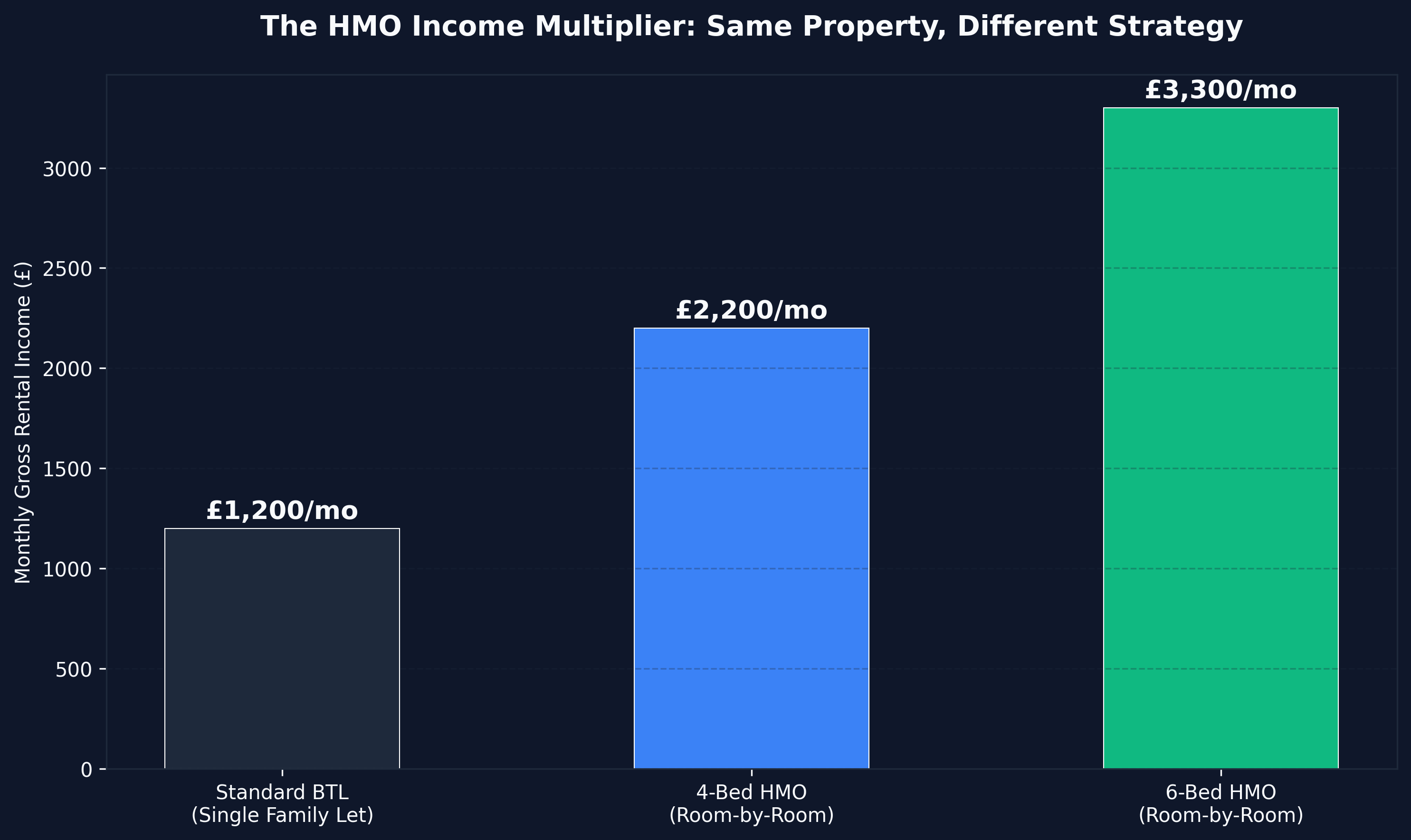

The fundamental maths are brutally simple. If you own a standard 4-bed terraced house and let it to a single family, you might achieve £1,200 per month.

If you convert that exact same 4-bed terraced house into a 6-bed HMO (adding two bedrooms by converting a dining room and large living area), and let each room individually at £550 per month, you achieve £3,300 per month.

That is a 175% increase in gross rental income from the same physical asset. This is why sophisticated property investment operators systematically convert standard housing stock into HMOs.

Phase 1: Acquiring the Property — Bridging Finance

The vast majority of HMO acquisitions in 2026 follow a two-stage financing model: Bridge first, then refinance onto a term mortgage.

Why? Because the properties most suitable for HMO conversion are uninhabitable, dilapidated terraced houses that fail the standard BTL mortgage criteria. No commercial lender will issue a 25-year mortgage on a property with a condemned boiler, a collapsing roof, and no fire safety infrastructure.

How Bridging Finance Works for HMOs

A bridging lender provides short-term capital (typically 6 to 18 months) secured against the asset. The loan funds both the purchase and the conversion works.

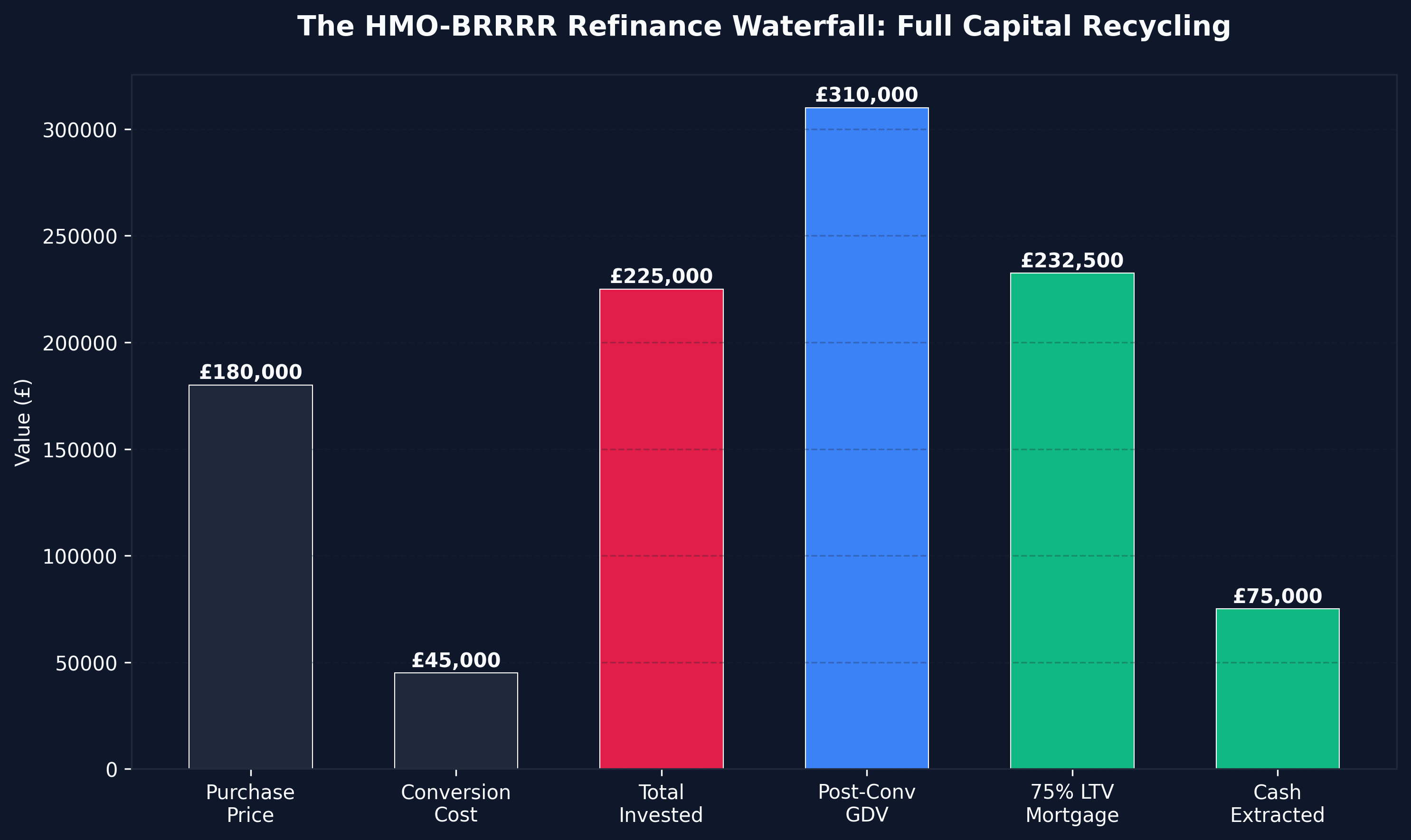

- Purchase Price: £180,000

- Conversion Budget (6-Bed HMO): £45,000

- Total Capital Required: £225,000

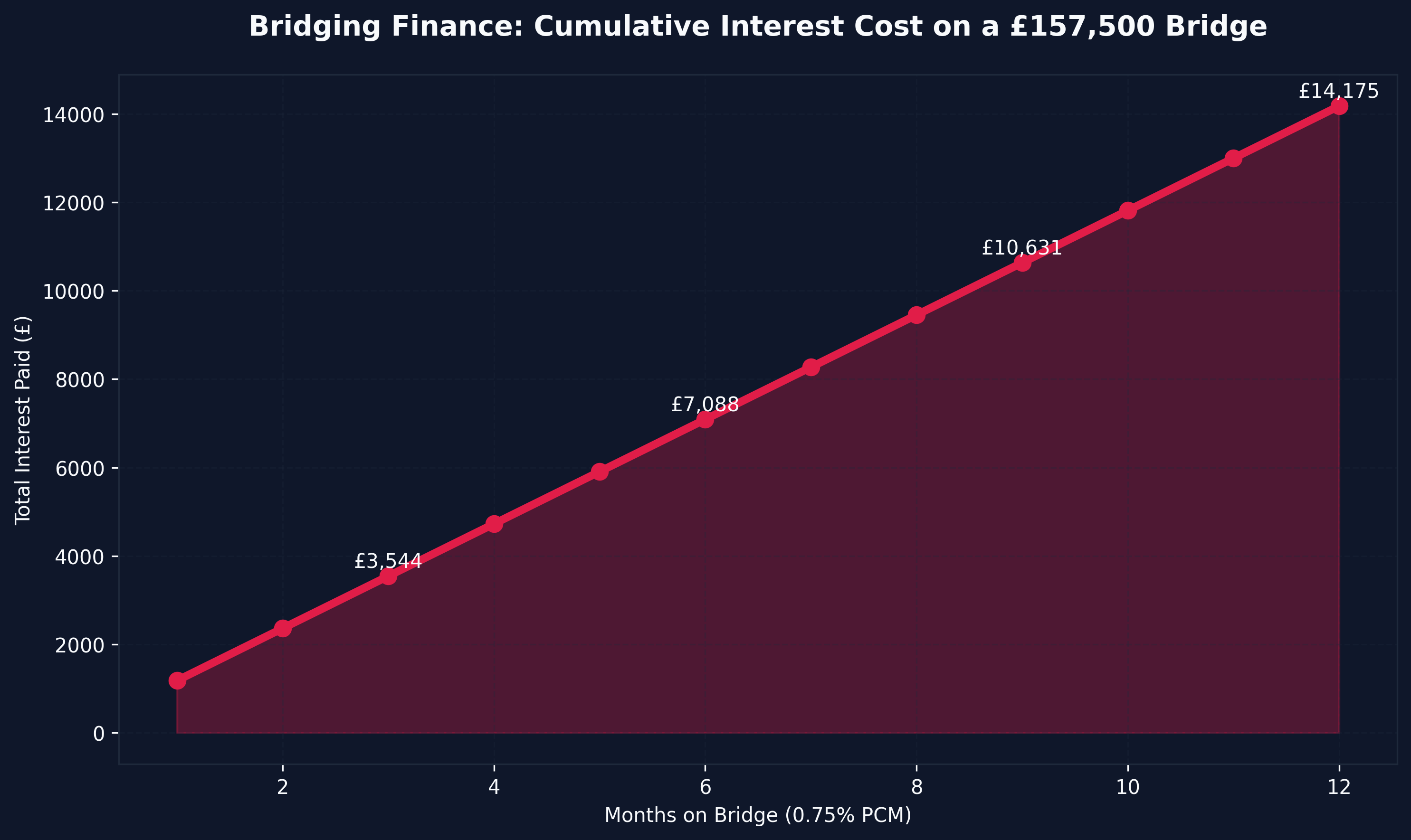

- Bridging LTV (70%): £157,500

- Investor Cash Required: £67,500

The bridging rate in 2026 typically sits between 0.55% and 0.85% per month (6.6% to 10.2% annualised), plus an arrangement fee of 1% to 2% of the loan value.

This is expensive debt. If your conversion takes 9 months on a £157,500 bridge at 0.75% per month, you will pay approximately £10,631 in interest alone before you generate a single pound of rental income.

This is the exact same mechanics as the BRRRR strategy, except the "Rehab" phase includes fire doors, emergency lighting, en-suite bathrooms, and HMO licensing compliance.

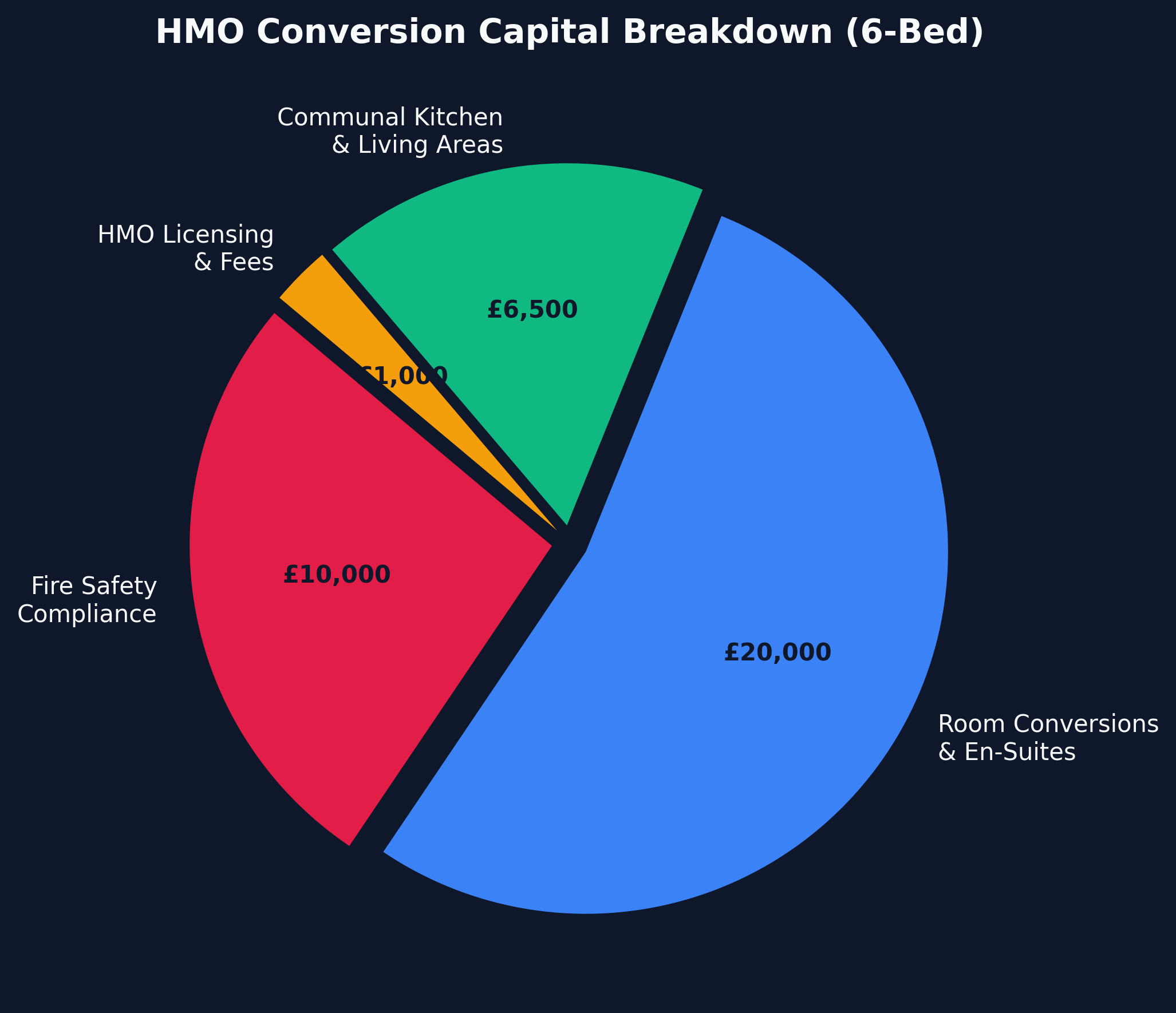

Phase 2: The HMO Conversion — What Your £45,000 Buys

Building regulations and HMO licensing requirements dictate the conversion scope. The capital is deployed across four critical workstreams:

1. Fire Safety Compliance (£8,000 – £12,000)

Every HMO requires:

- 30-minute fire doors on every habitable room

- Interlinked mains-wired smoke and heat detectors

- Emergency lighting on all escape routes

- Fire blankets in the communal kitchen

- A fire risk assessment by a qualified assessor

2. Room Conversions & En-Suites (£15,000 – £25,000)

Converting a dining room or reception room into a lettable bedroom requires damp-proofing, plastering, electrical first-fix, and potentially adding an en-suite shower room. En-suite rooms command a £75 to £125 per month premium over rooms with shared bathrooms.

3. Communal Kitchen & Living Areas (£5,000 – £8,000)

The local authority will inspect the communal kitchen against strict criteria: one cooker per five tenants, adequate refrigerator space, and extraction ventilation.

4. HMO Licensing Fees (£500 – £1,500)

The mandatory HMO licence is granted by your local council and is typically valid for 5 years. Fees vary dramatically by authority. Some councils charge £500; others (particularly London boroughs) charge upwards of £1,500.

The total licensing and compliance capital requirement adds roughly £1,000 to £2,000 per room to your conversion budget. This is the hidden cost that many novice HMO investors fail to model, which then destroys their projected yield.

Phase 3: The Specialist HMO Mortgage (Refinance)

Once the property is fully converted, licenced, and tenanted, you exit the bridging loan by refinancing onto a specialist HMO mortgage.

Who Offers HMO Mortgages in 2026?

High-street lenders (HSBC, Barclays, Lloyds) do not offer HMO-specific products. You must approach specialist commercial lenders:

- Paragon Bank — The dominant UK HMO lender. Offers up to 75% LTV on licensed HMOs.

- The Mortgage Lender (TML) — Offers enhanced HMO products with higher LTV tiers for experienced landlords.

- Precise Mortgages — Flexible HMO products for SPV structures.

- Shawbrook Bank — Offers "large HMO" products (7+ beds) at competitive rates.

- Foundation Home Loans — Competitive rates for smaller HMOs (3-6 beds).

The Critical Metrics

- Maximum LTV: 75% (some lenders offer 80% for experienced portfolio landlords)

- Interest Rate: 5.5% to 7.5% (fixed for 2 or 5 years) in 2026

- Minimum Property Value: Typically £100,000

- Stress Test: Lenders require a minimum Interest Coverage Ratio (ICR) of 125% to 145%, meaning your monthly rental income must exceed 125% to 145% of your monthly mortgage payment.

The Refinance Mathematics (Exiting the Bridge)

- Post-Conversion RICS Valuation (GDV): £310,000

- 75% LTV Mortgage: £232,500

- Original Bridge Debt: £157,500

- Cash Extracted on Refinance: £232,500 - £157,500 = £75,000

- Original Cash Invested: £67,500

You have extracted £75,000 from a deal where you invested £67,500. You have recycled 100% of your capital plus an additional £7,500 in profit, whilst retaining a fully tenanted 6-bed HMO generating £3,300 per month.

This is the exact BRRRR execution framework. To model these specific calculations, use our Buy Rehab Rent Refinance Repeat Yield Calculator UK.

SPV vs Personal Name: Tax-Efficient HMO Structuring

How you hold the HMO is as critical as how you finance it. In 2026, the tax implications are stark.

Personal Name Ownership

If you hold an HMO in your personal name and earn above £50,270, your rental profits are taxed at 40% Higher Rate Income Tax. Furthermore, since the 2020 Section 24 mortgage interest relief restriction, you can no longer deduct your mortgage interest from your rental profits. Instead, you receive a basic-rate (20%) tax credit. For higher-rate taxpayers, this effectively doubles the tax burden on leveraged HMO income.

SPV (Special Purpose Vehicle) Ownership

If you hold the HMO within a Limited Company (SPV), the rental profits are taxed at 25% Corporation Tax (2026 rate). Crucially, mortgage interest remains fully deductible as a business expense within the SPV, dramatically reducing your taxable profit.

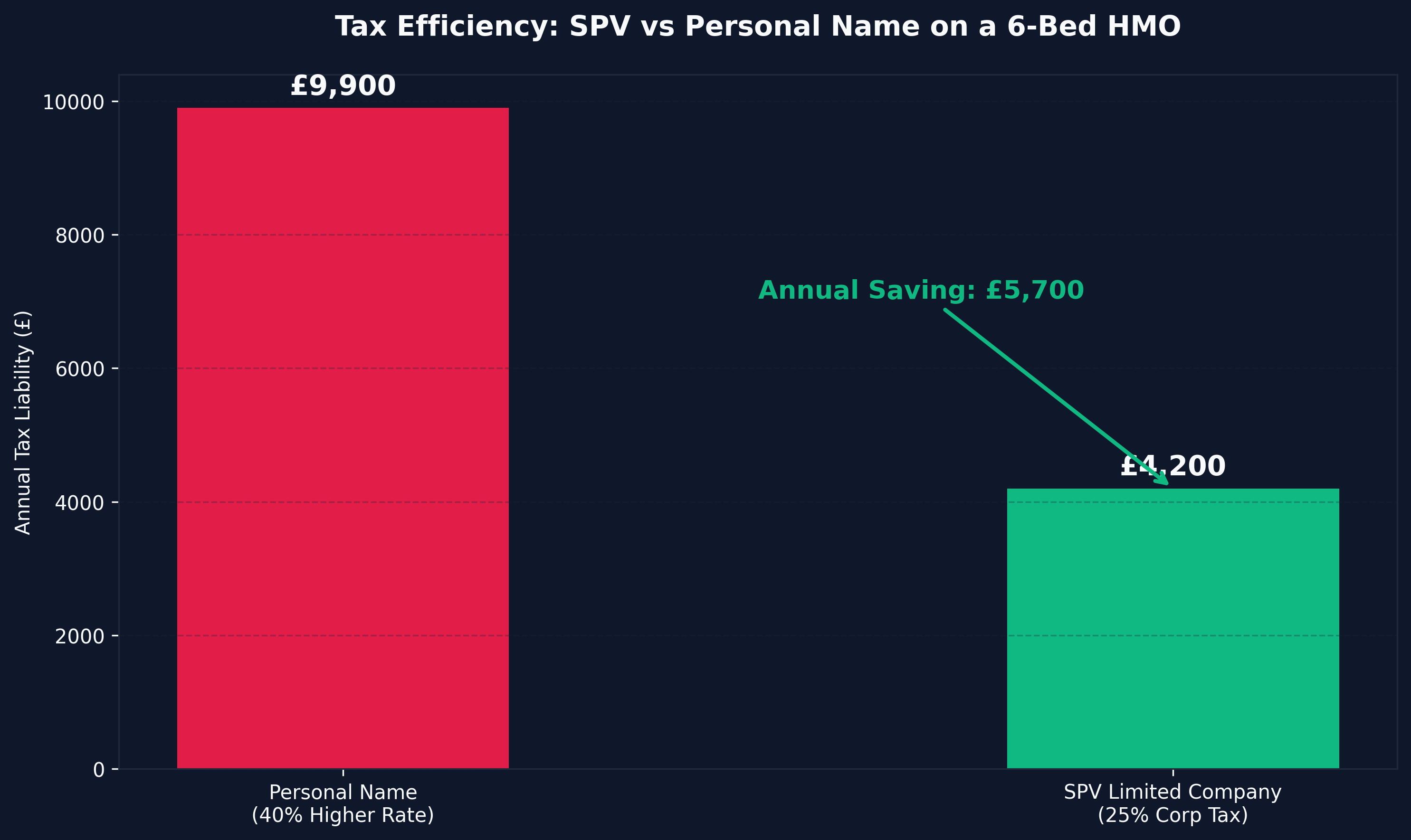

For the £3,300 per month HMO (£39,600 annual rent):

- Personal Name (40% taxpayer): ~£9,900 tax liability

- SPV (25% Corp Tax, full mortgage deduction): ~£4,200 tax liability

The SPV saves approximately £5,700 per year per HMO. Over a 10-year hold, that is £57,000 in tax savings on a single property.

For a comprehensive breakdown of SPV structuring, landlord tax optimization, and effective financing of investment property, see our detailed guide on how to finance rental property.

Article 4 Directions: The Planning Permission Trap

An Article 4 Direction is a local planning regulation that removes your permitted development rights to convert a standard dwelling (Use Class C3) into an HMO (Use Class C4) without full planning permission.

Many UK cities with high student populations (Nottingham, Leeds, Bristol, parts of Manchester) have enacted Article 4 Directions to prevent the over-concentration of HMOs in residential streets.

What This Means for Your Finance

If the property sits within an Article 4 zone, your planning application may be refused. If planning is refused, you cannot legally operate the HMO. If you cannot legally operate the HMO, neither your bridging lender nor your HMO mortgage provider will fund the deal.

Always check the Article 4 status before exchanging contracts. A simple enquiry to the local council's planning department will confirm whether the target property falls within a restricted zone.

Large HMOs (7+ Beds)

Properties housing seven or more tenants forming two or more households are classified as "Large HMOs" and always require full planning permission, regardless of Article 4 status. The planning process adds 8 to 12 weeks (and £462 in application fees) to your project timeline.

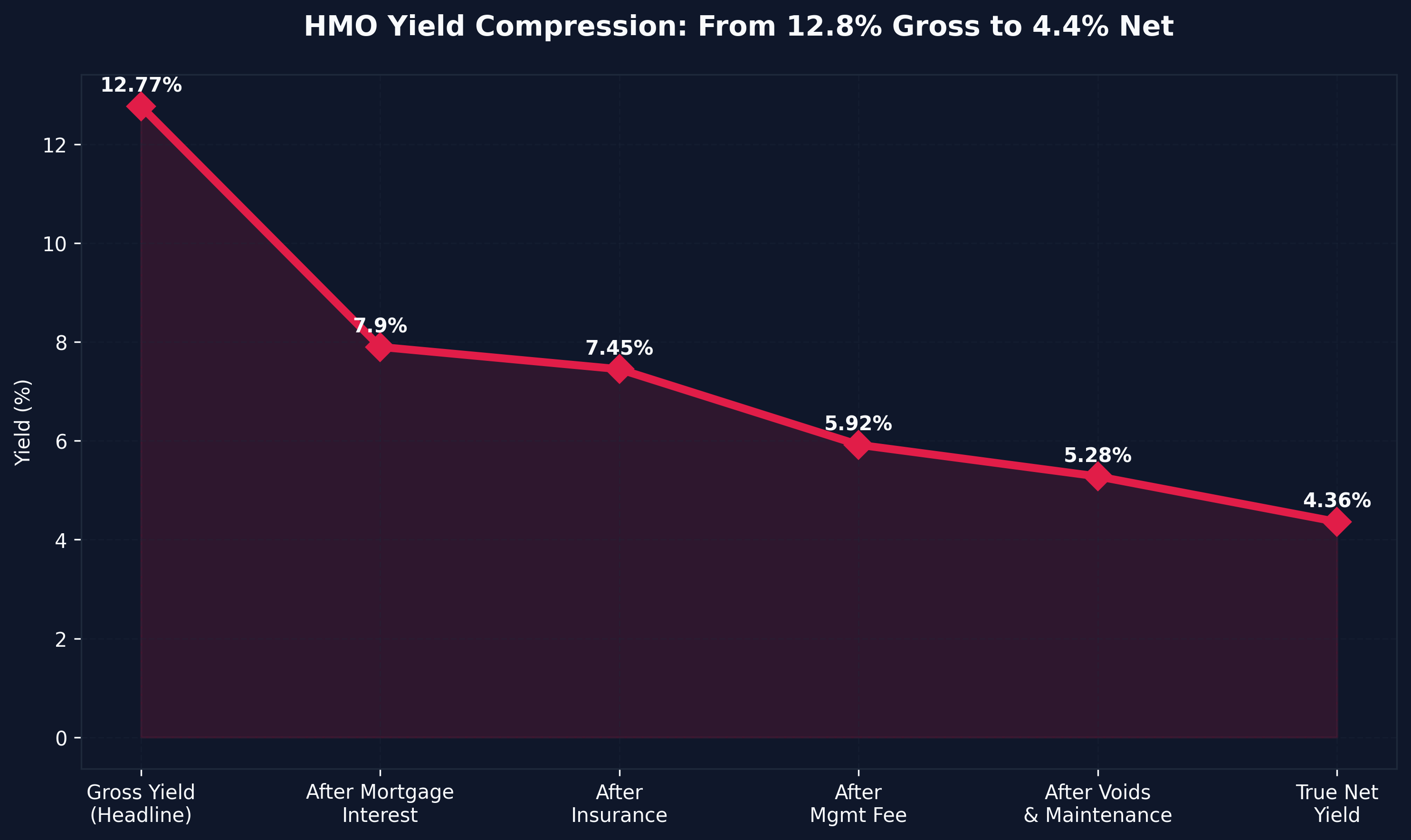

The True Yield After All Costs

Novice HMO investors frequently cite "15% gross yields" without accounting for the brutal operational costs that separate HMOs from standard BTL.

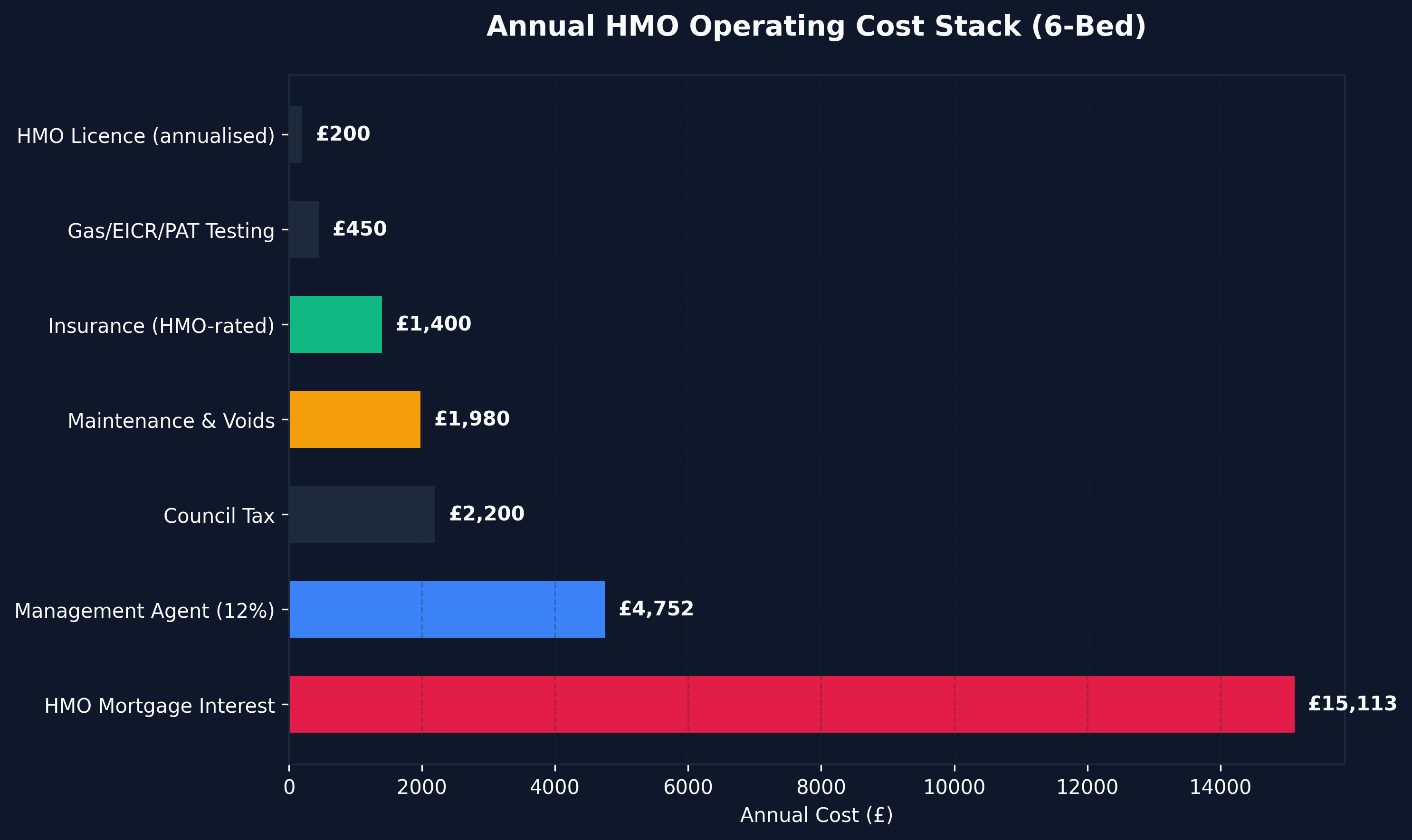

Realistic Annual Cost Stack for a 6-Bed HMO:

| Cost | Annual Amount |

|---|---|

| HMO Mortgage Interest (£232,500 @ 6.5%) | £15,113 |

| Council Tax (if not paid by tenants) | £2,200 |

| Buildings & Landlord Insurance (HMO-rated) | £1,400 |

| Gas Safety, EICR, PAT Testing | £450 |

| HMO Licence (annualised over 5 years) | £200 |

| Maintenance & Voids (5%) | £1,980 |

| Management Agent (12% of gross) | £4,752 |

| Total Annual Costs | £26,095 |

- Gross Annual Rent: £39,600

- Total Annual Costs: £26,095

- Net Annual Profit: £13,505

- True Net Yield on GDV (£310,000): 4.36%

- Cash-on-Cash Return (£0 left in deal via BRRRR): Infinite (if fully recycled)

The 15% gross yield compresses to a 4.36% net yield once all HMO-specific costs are factored in. However, because the BRRRR model allows full capital recycling, the Cash-on-Cash return can be mathematically infinite, making HMOs one of the most efficient passive income property UK assets when structured correctly.

Summary: Financing an HMO in 2026

Financing a House in Multiple Occupation requires a fundamentally different toolkit than standard buy-to-let. The two-phase Bridge → Convert → Refinance model is the dominant execution framework. You must navigate specialist lenders, fire safety compliance, Article 4 planning restrictions, and HMO-rated insurance policies.

However, if you model the mathematics correctly—confirming the RICS post-conversion GDV supports a 75% LTV refinance that fully repays your bridge—the HMO structure delivers yields that no other UK residential asset class can match.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →