Investing in student accommodation in the UK has transformed from a niche buy-to-let strategy into one of the most robust, high-yielding asset classes in the real estate sector. As we progress through 2026, the market dynamics present a unique landscape characterised by a structural undersupply of bespoke bedding, shifting tenant demographics, and evolving regulatory frameworks.

For property investors asking whether it is still viable to invest in student accommodation UK markets, the data points clearly toward a resilient sector. Driven by a burgeoning domestic 18-year-old population and sustained international demand, the asset class continues to outperform traditional residential buy-to-let properties in terms of gross rental yields.

The State of the UK Student Housing Market in 2026

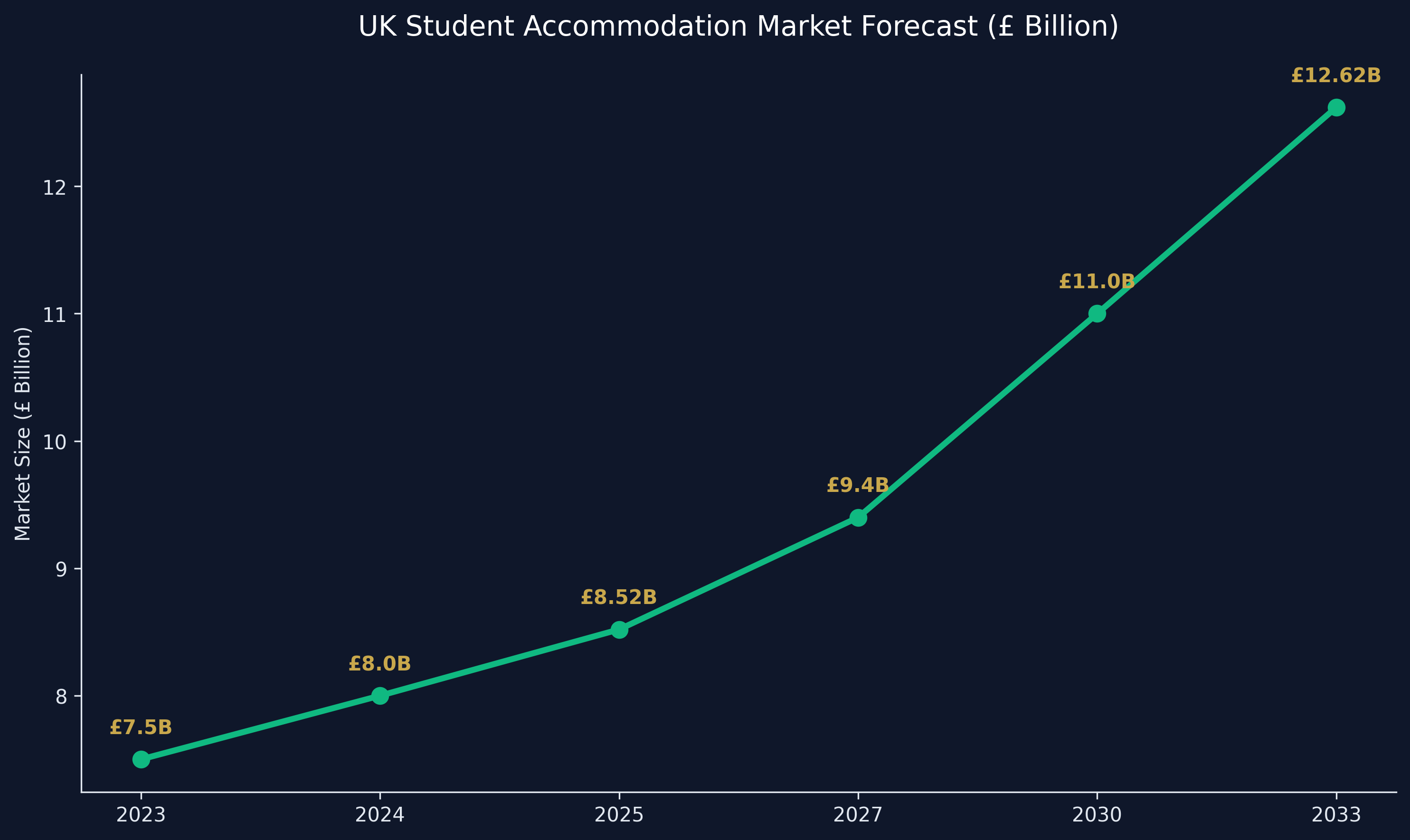

The student housing sector in the United Kingdom is currently experiencing a perfect storm of high demand and severely constrained supply. Historical data indicates that the market has grown substantially, and forecasts predict the UK student accommodation market will swell from £8.52 billion in 2025 to £12.62 billion by 2033, representing a Compound Annual Growth Rate (CAGR) of 5.45%.

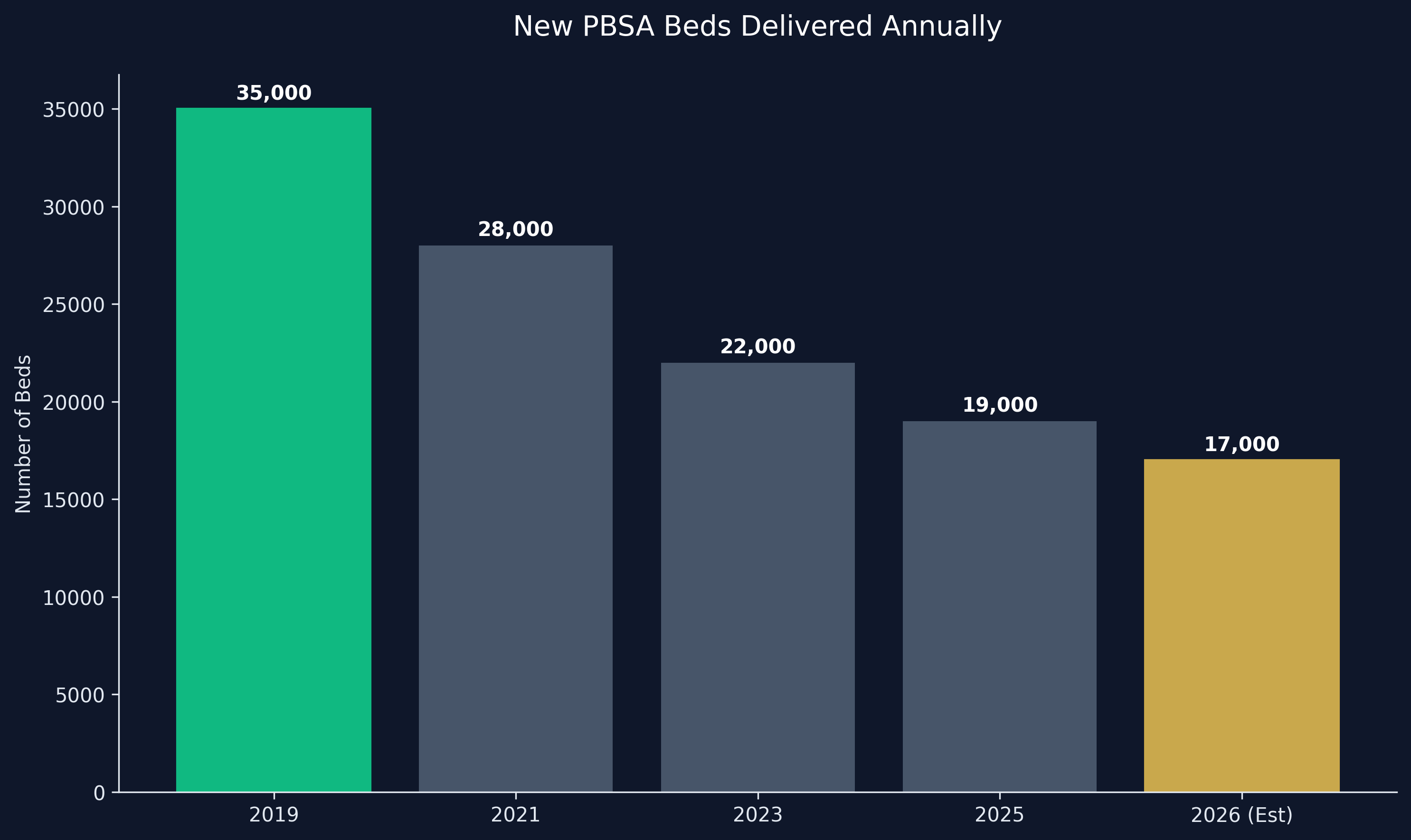

This growth is fundamentally underpinned by the UK’s reputation as a premier global higher education destination. However, the overarching theme defining the 2026 market is the chronic shortfall of available beds. With UCAS reporting record numbers of 18-year-old UK applicants by June 2025, the pressure on existing infrastructure has never been higher.

New developments are struggling to keep pace. Deliveries of new Purpose-Built Student Accommodation (PBSA) beds are down approximately 50% compared to pre-pandemic levels. Only around 17,000 new beds are expected to enter the market in 2026, hampered by high construction material costs, stringent planning permissions, and complex funding environments. This imbalance ensures that existing high-quality assets maintain near full occupancy and command premium rents.

Why Invest in Student Accommodation UK? Analyzing the Yields

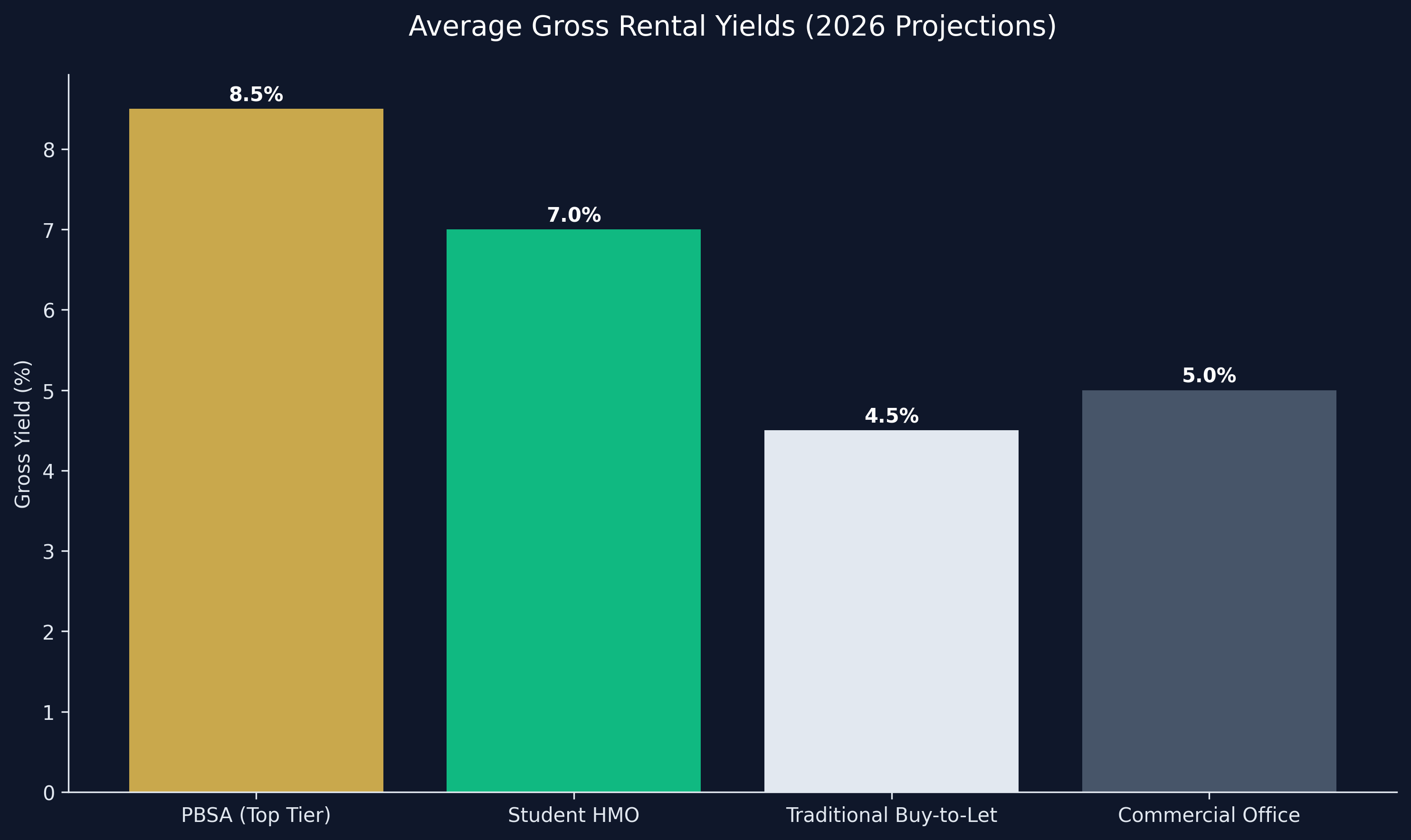

The primary attraction for investors entering the student property market is the potential for superior rental yields. While traditional residential buy-to-let yields have been squeezed by rising interest rates and stagnant wage growth relative to property prices, student accommodation continues to offer lucrative returns.

Superior Gross Rental Yields

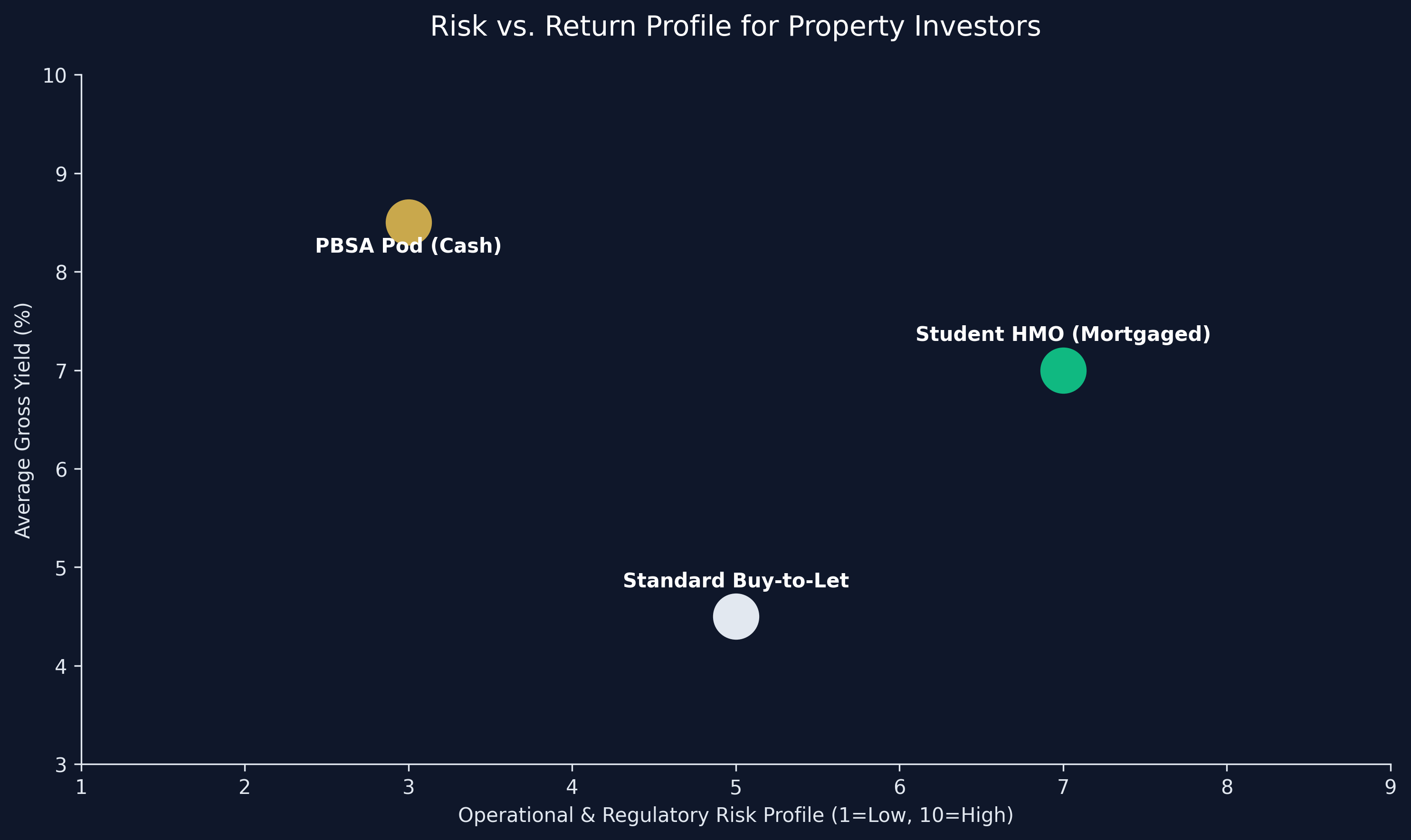

Across the UK, gross yields for student properties consistently range between 6% and 9%. In high-performing regional cities, targeted investments can even generate yields touching 10%. This significantly outpaces the UK average for standard residential properties, which often hover around the 4% to 5% mark.

The structure of student rentals—often let on 44 or 51-week contracts with built-in rent increases—secures a predictable income stream. Furthermore, the limited supply has allowed providers to implement necessary rent adjustments. In 2026, while the astronomical rent hikes seen post-pandemic have cooled, rental growth has stabilised at a sustainable 3% to 5% across major university hubs.

The True Cost of Operations

It is vital to distinguish between gross and net yields. Operational costs for student accommodations are inherently higher than standard residential lets. Fast tenant turnaround, increased wear and tear, and the inclusion of utility bills in the rental price eat into the gross figures. Despite these overheads, a well-managed PBSA or a compliant HMO in a high-demand area will typically deliver a net yield of 6% to 7%, outperforming alternative property investments.

The Supply and Demand Imbalance: A Structural Deficit

Understanding the investment thesis requires a deep dive into the supply and demand metrics. The UK is facing a structural deficit of student housing that cannot be resolved in the short to medium term.

The London Shortfall

Looking at the capital, projections indicate a staggering shortfall of over 83,000 student beds between 2020 and 2027. London attracts the highest volume of international students and domestic scholars, yet space for sprawling new PBSA developments is practically non-existent due to land values and zoning restrictions.

Regional Bottlenecks

This supply crunch is not restricted to London. Cities like Bristol, Manchester, and Glasgow are experiencing deep supply-demand imbalances. In 2020, data suggested there were 2.7 students competing for every available purpose-built bed. By 2024, the national shortfall was estimated at 580,000 beds. Moving into 2026, this figure has only compounded as development pipelines stall.

For the investor, this scarcity translates to minimal void periods. When demand categorically outstrips supply, landlords and PBSA operators possess significant pricing power, reducing the risk of vacant rooms during the academic year.

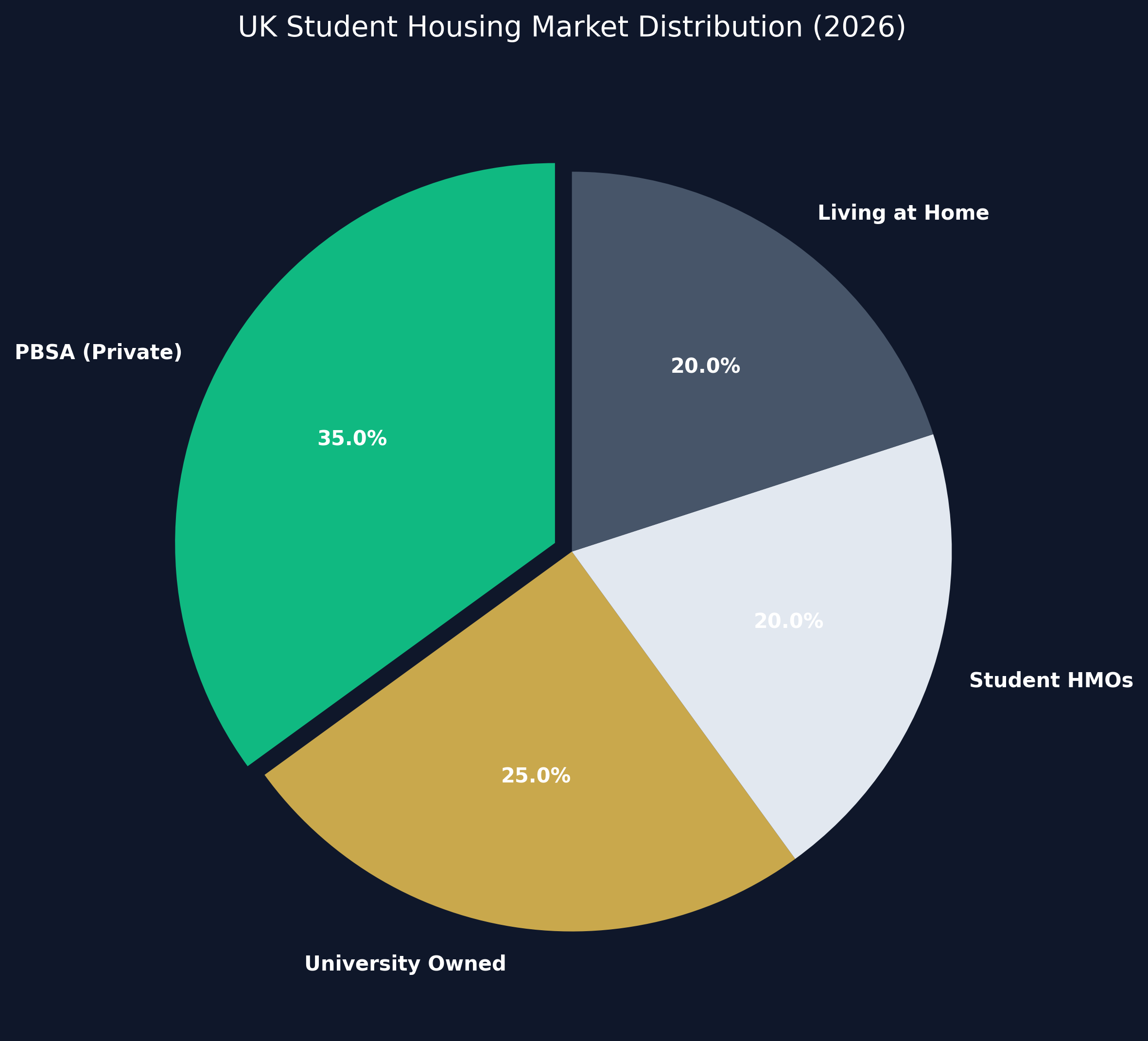

Purpose-Built Student Accommodation (PBSA) vs. HMOs

When you decide to invest in student accommodation UK, you are presented with two primary asset classes: Purpose-Built Student Accommodation (PBSA) and Houses in Multiple Occupation (HMOs). Each carries distinct operational models, risk profiles, and capital requirements.

Purpose-Built Student Accommodation (PBSA)

PBSAs are large-scale, modern developments designed entirely around the student experience. Investors typically purchase individual ‘pods’ (en-suite rooms sharing a communal kitchen) or self-contained studio flats within these complexes.

The Advantages:

- Completely Hands-Off: PBSAs are universally managed by specialist operators who handle marketing, tenant sourcing, maintenance, and rent collection.

- High Occupancy Drive: Modern students prefer the amenities offered—gyms, cinema rooms, hyper-fast Wi-Fi, and 24/7 security.

- Lower Entry Point: Prices for individual pods can start significantly lower than traditional housing, sometimes below £70,000 in regional markets.

The Drawbacks:

- Cash-Only Purchases: Mortgages on individual student pods are notoriously difficult to secure. High street lenders often view them as commercial propositions, meaning investors usually require liquid cash.

- Capital Appreciation: While yields are high, the resale market is limited to other investors. Capital growth is historically slower compared to standard residential property.

Houses in Multiple Occupation (HMOs)

An HMO involves purchasing a standard residential house and renting individual rooms to multiple unrelated students.

The Advantages:

- Capital Growth Potential: Because the asset remains a standard residential property, its underlying value follows the wider housing market trajectory, offering better capital appreciation prospects than PBSA pods.

- Financing Options: HMO mortgages are widely available, allowing investors to leverage their capital and build larger portfolios.

- Exit Strategy: If the student market in an area cools, the property can be converted back to a family home or rented to young professionals.

The Drawbacks:

- Management Intensive: HMOs require active, hands-on management. Even when using a letting agent, the administrative burden is higher.

- Regulatory Compliance: Landlords must navigate complex local council licensing requirements, particularly the influx of Article 4 directions which restrict the conversion of standard homes into HMOs.

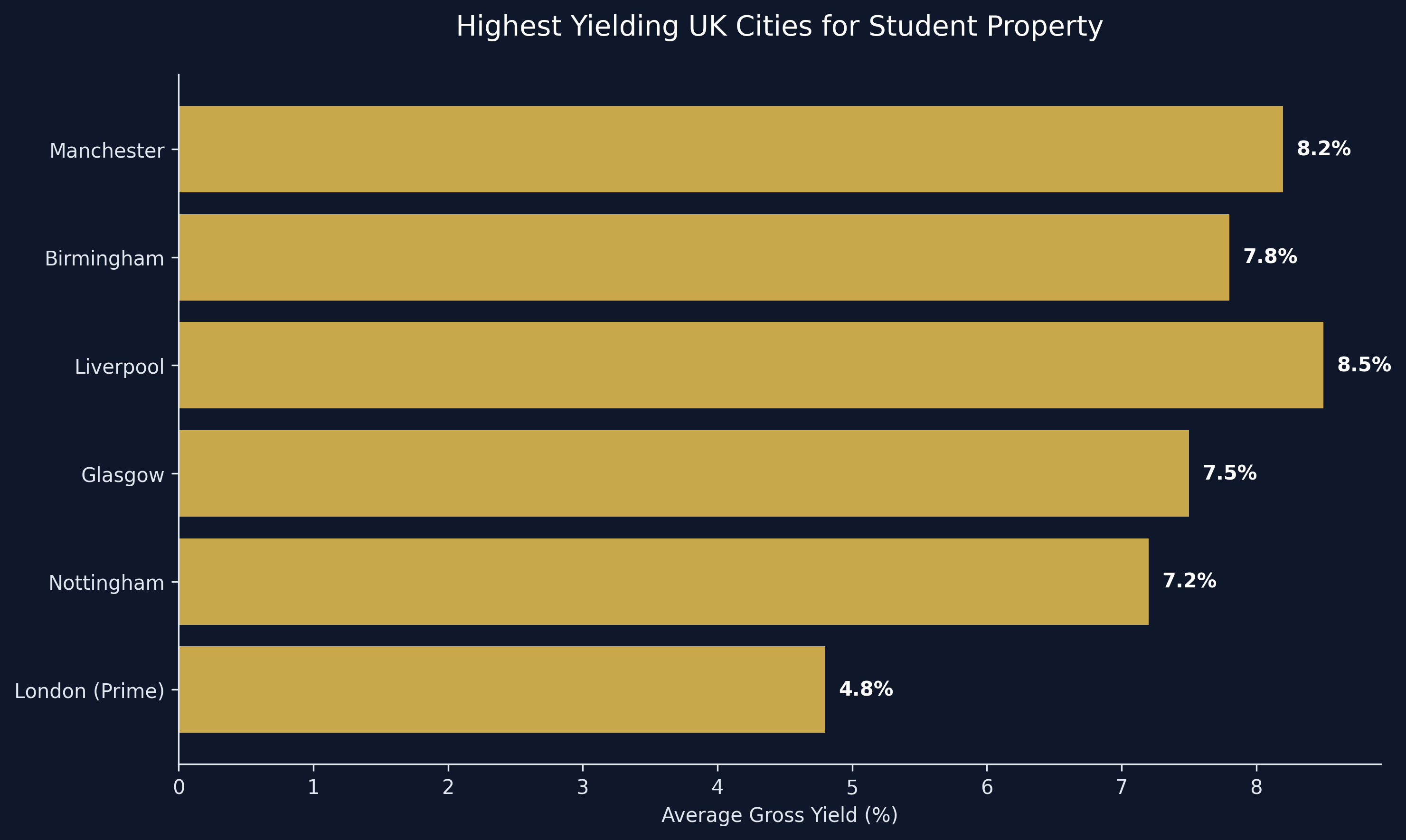

Top UK Cities for Student Property Investment in 2026

Location is the defining metric for student property success. The landscape in 2026 heavily favours regional hubs where the supply/demand imbalance is most acute and entry prices remain rational.

Manchester

Manchester boasts one of the highest student retention rates post-graduation in Europe. This creates a unique friction: second and third-year students are actively competing with young professionals for housing. This intense demand drives consistent rental growth, making both PBSA and HMO investments highly lucrative.

Birmingham

With five distinct universities and massive ongoing infrastructure projects like HS2, Birmingham’s student population is massive. The city offers lower capital entry points compared to London or the South East, alongside impressive gross yields routinely exceeding 7%.

Liverpool

Historically a powerhouse for student property, Liverpool continues to present strong use cases. Its three main universities draw over 70,000 students. Crucially, property prices are highly accessible, and the city frequently tops national tables for pure rental yield percentages.

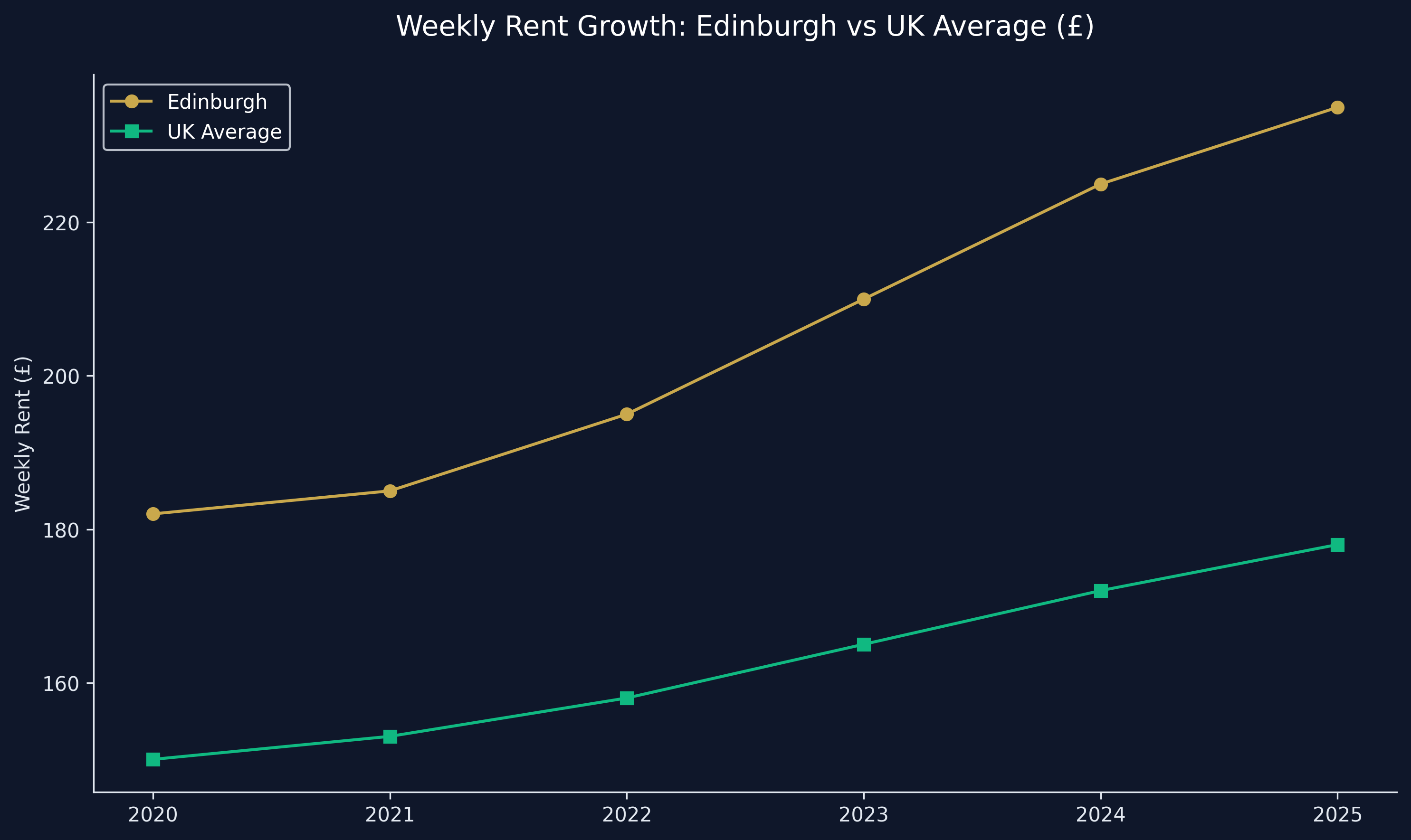

Edinburgh & Glasgow

Scotland’s two major cities suffer from severe bed shortages. Edinburgh, in particular, has witnessed dramatic rent increases, jumping from £182 per week in 2020 to an average of £235 by 2025. Stringent local planning laws severely limit new PBSA construction, guaranteeing high occupancy for existing landlords.

The Impact of International Students and Demographics

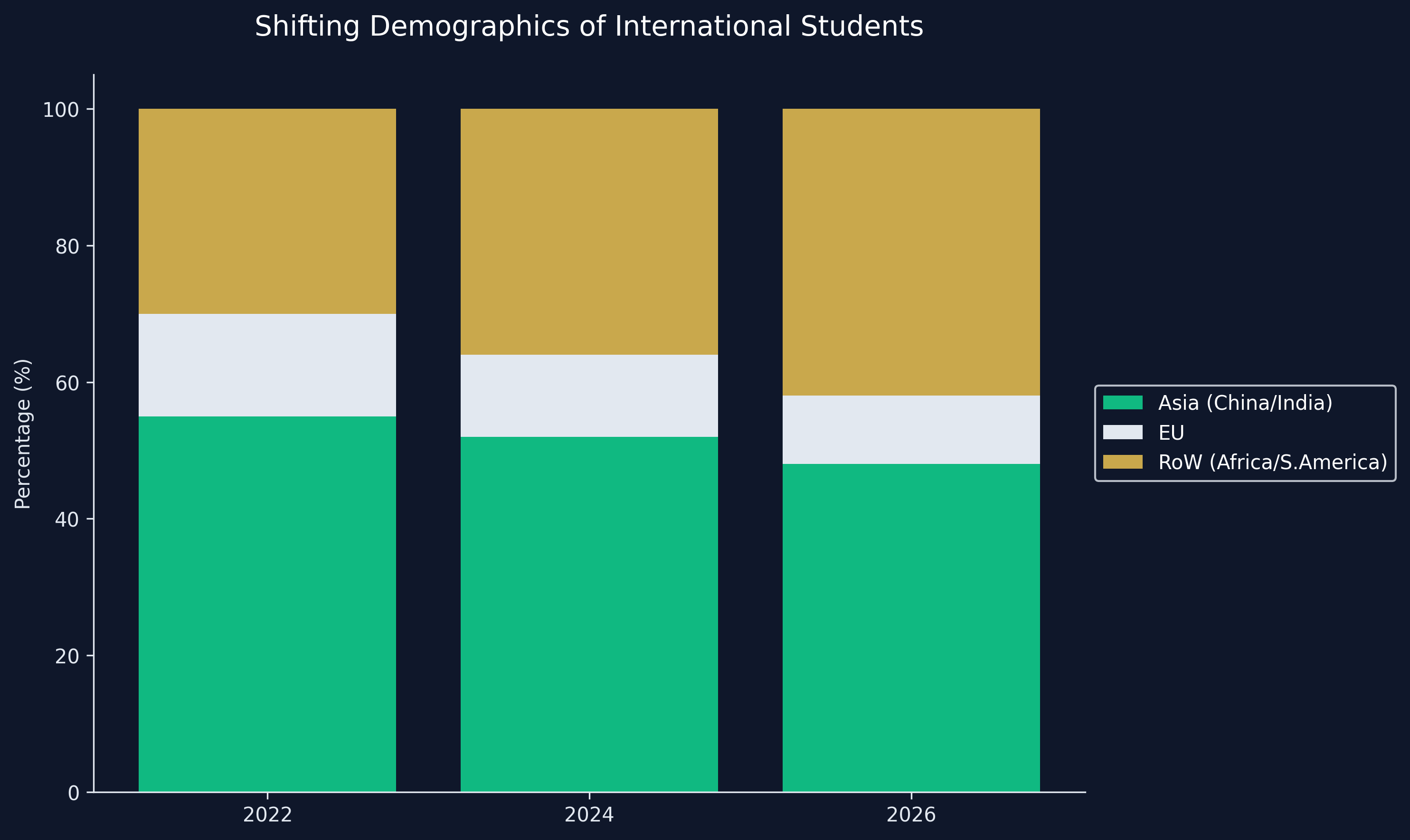

International students are the lifeblood of the premium student accommodation sector. They typically possess higher budgets, prefer the security and convenience of PBSA, and are more likely to book premium studios rather than standard cluster flats.

In 2026, the demographics of international arrivals are shifting. While dominant markets like China and India remain strong, universities are actively diversifying their intake, with rising numbers from Southeast Asia, South America, and Sub-Saharan Africa.

This diversification requires PBSA operators to adapt. High-end developments are now offering multilingual support, bespoke cultural orientation, and streamlined guarantor processes to attract this affluent demographic. However, investors must remain vigilant regarding government policy. Discussions surrounding levies on international student fees or changes to post-study work visas can directly impact enrollment figures, particularly at lower-tier universities. Therefore, investing in properties aligned with highly ranked, Russell Group institutions provides a crucial layer of structural defence.

Evolving Student Preferences: What Do Modern Tenants Want?

The modern student is a highly discerning consumer. The days of accepting damp, poorly insulated terraced housing are completely over. In 2026, students are prioritizing properties that act as holistic living environments rather than just a place to sleep.

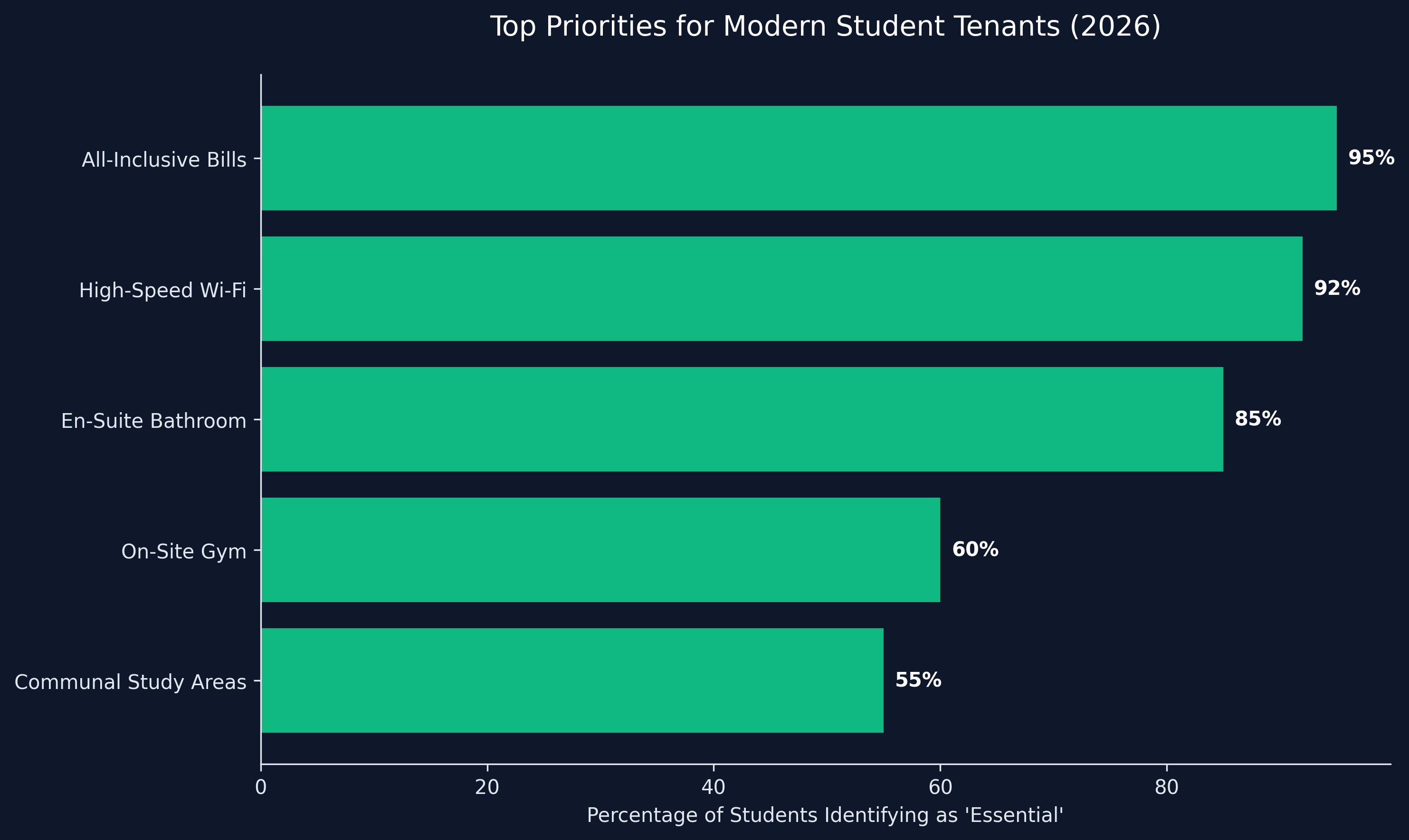

The "Bills-Included" Expectation

The energy crisis fundamentally altered market expectations. Today, students overwhelmingly demand rent models that are completely inclusive of gas, electricity, water, and broadband. Properties that do not offer an all-inclusive model face significantly longer void periods and discounted rental rates. PBSA naturally caters to this, but HMO landlords must adapt their pricing modules to match.

Well-being and ESG

Mental health and well-being have become prominent focus points. Premium PBSA developments now integrate biophilic design, ample natural light, dedicated quiet study zones, and on-site pastoral care. Furthermore, eco-conscious students are scrutinising the Environmental, Social, and Governance (ESG) credentials of their housing. Energy-efficient buildings with smart heating controls, solar integration, and excellent EPC ratings command premium rents and ensure future-proofing against incoming environmental legislation.

Connectivity

Hyper-fast, synchronous broadband is no longer an amenity; it is a fundamental utility. With the integration of AI tools, heavy media consumption, and hybrid learning models, robust Wi-Fi infrastructure is the primary determinant of tenant satisfaction and retention.

Understanding the Risks and Regulatory Changes

While the yields are attractive, to invest in student accommodation UK markets requires navigating specific sectoral risks and legislative hurdles.

Regulatory Complexity

The landscape for landlords has tightened significantly. The Renters' Right Act has moved into law, bringing sweeping changes to tenancy structures, potentially limiting the use of fixed-term contracts. This is particularly delicate for the student market, which relies on synchronized academic cycles.

Furthermore, the Building Safety Act 2022 has introduced intense regulatory complexity for high-rise PBSA blocks. Compliance costs are high, and this legislation is a primary reason why new development pipelines have dried up, subsequently boosting the value of existing, compliant buildings.

Resale Liquidity

Investors must approach PBSA with open eyes regarding liquidity. An individual student pod cannot be sold to an owner-occupier; the buyer pool consists entirely of other investors. If you require rapid capital extraction, PBSA may prove challenging. The asset should be viewed as a medium to long-term income generator rather than a vehicle for rapid capital flipping.

Oversupply Micro-Markets

While the national picture is one of undersupply, hyper-localised oversupply can occur. Certain specific postcodes within university cities have seen intense PBSA development. Investors must conduct granular, street-level due diligence to ensure their specific asset remains competitive against newer surrounding stock.

Financing Your Investment: Mortgages vs. Cash Buying

The financial structuring of a student property investment dictates the entry strategy.

For PBSA, cash is king. High-street lenders will generally refuse to mortgage individual student pods, citing the lack of alternative use if the student market collapses or the operating company faces administration. Some specialized commercial lenders will finance PBSA, but typically only at lower Loan-To-Value (LTV) ratios and at higher interest rates. Consequently, off-plan or completed PBSA units are marketed almost exclusively at cash-rich investors.

Conversely, HMOs benefit from access to a highly competitive mortgage market. Buy-to-let mortgages specifically tailored for student HMOs allow investors to utilize leverage. An investor with £150,000 could potentially purchase one high-end PBSA studio outright, or utilize that capital as deposits across three or four mortgaged HMO properties, thereby spreading risk and maximizing blended ROI over time.

Forecasting the Future: Market Growth to 2033

The macro outlook for the UK student accommodation sector remains overwhelmingly positive. Forecasting through to 2033, the market is structurally insulated against many of the economic shocks that trouble commercial office space or wider residential retail.

The fundamental truth remains: higher education in the UK is a globally sought-after export. As long as the elite universities maintain their global rankings, the influx of domestic and international capital will flow.

For the modern investor, the strategy for 2026 relies on asset selection. The highest returns will be captured by those who target strong regional cities experiencing deep structural undersupply, and who prioritize high-quality, energy-efficient, and professionally managed assets that meet the exacting standards of the modern student consumer. Whether opting for the pure, hands-off income of a PBSA pod, or the capital appreciation potential of a leveraged HMO, student accommodation firmly retains its status as a premier UK real estate asset.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →