Buying investment property through a limited company is no longer a niche strategy — it is the dominant approach. In 2025, approximately 80% of all new buy-to-let mortgage applications were made through corporate structures. The reason is simple: Section 24 made personal ownership punishingly expensive for higher-rate taxpayers, and the tax differential between personal and corporate ownership can exceed 17 percentage points on the same rental income.

This guide covers everything you need to know about buying property through a limited company in 2026: setup, tax treatment, mortgage options, incorporation of existing portfolios, and the strategic decision framework for choosing the right structure.

Last Updated: April 2026

Why Limited Company Buy-to-Let?

The Section 24 Problem

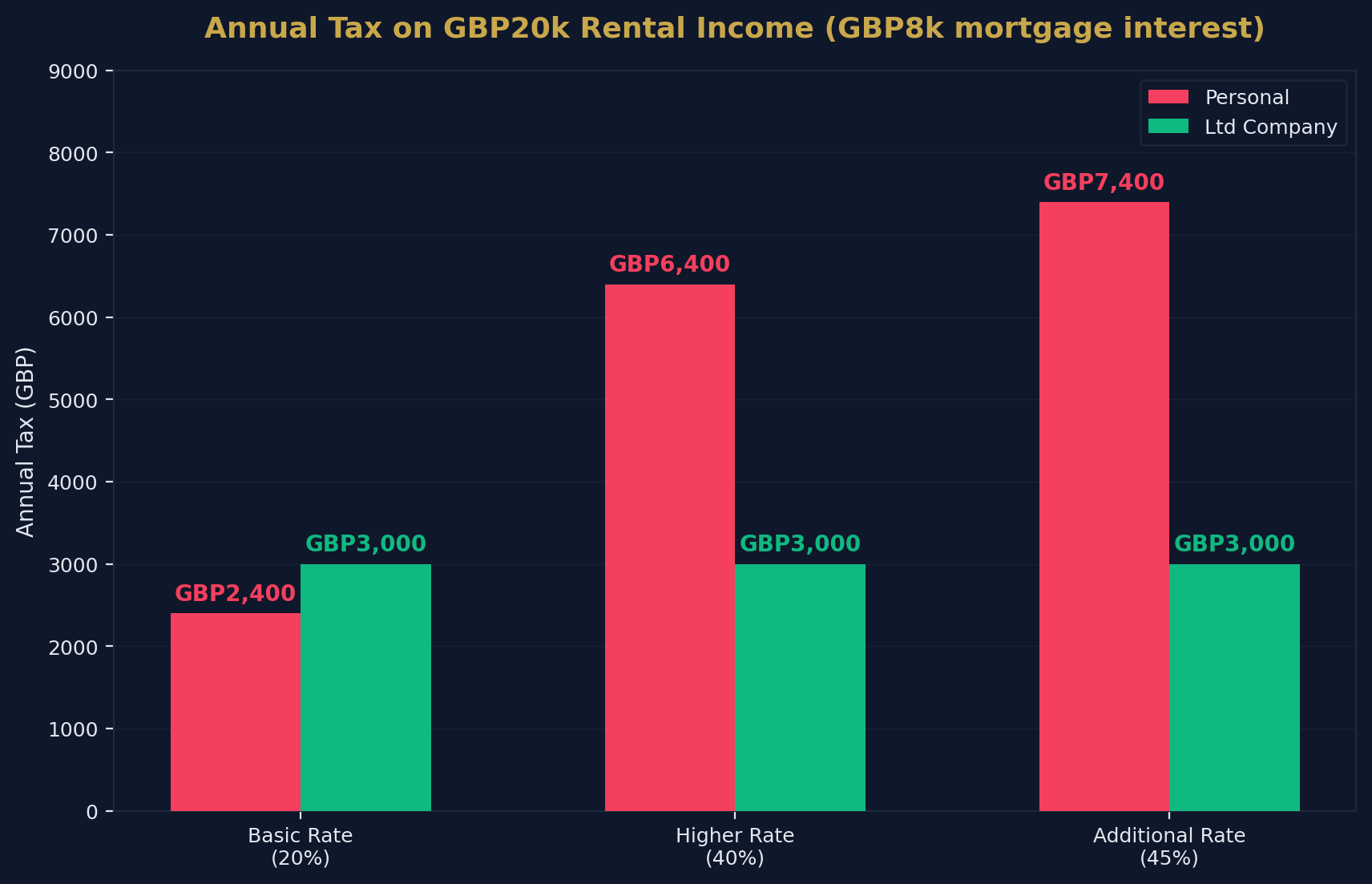

Before 2017, individual landlords could deduct 100% of their mortgage interest from rental income before calculating tax. Section 24 of the Finance Act 2015 gradually removed this relief. Since April 2020, the full restriction applies:

| Taxpayer | Old Treatment | Current Treatment (Personal) | Company Treatment |

|---|---|---|---|

| Basic rate (20%) | Full deduction | 20% tax credit | Full deduction |

| Higher rate (40%) | Full deduction | 20% tax credit only | Full deduction |

| Additional rate (45%) | Full deduction | 20% tax credit only | Full deduction |

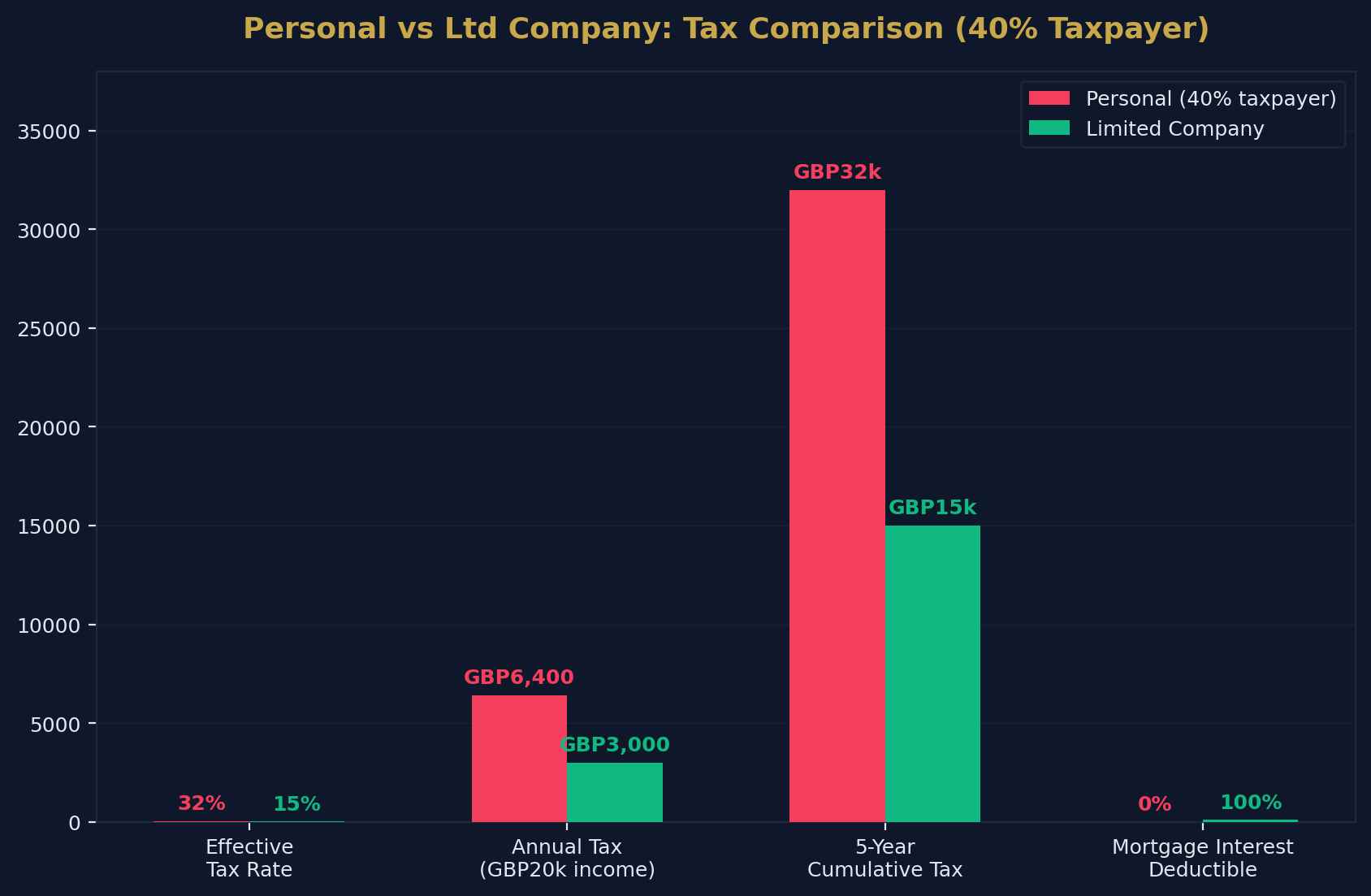

The impact is dramatic. A higher-rate taxpayer with £20,000 rental income and £8,000 mortgage interest:

| Metric | Personal Ownership | Limited Company |

|---|---|---|

| Rental income | £20,000 | £20,000 |

| Mortgage interest deduction | None (tax credit only) | £8,000 (full deduction) |

| Taxable profit | £20,000 | £12,000 |

| Tax due | £8,000 - £1,600 credit = £6,400 | £12,000 × 25% = £3,000 |

| Effective tax rate | 32% | 15% |

| Annual saving via Ltd | — | £3,400 |

Setting Up an SPV

What Is an SPV?

A Special Purpose Vehicle (SPV) is a limited company formed specifically to hold investment property. It is the standard structure used by professional investors.

Setup Process

| Step | Detail | Cost |

|---|---|---|

| 1. Choose a name | Must include "Limited" or "Ltd" | Free |

| 2. Register at Companies House | Online formation | £12–£50 |

| 3. Select SIC codes | 68100 (Buying/selling own real estate) and 68209 (Other letting/operating) | Free |

| 4. Appoint directors | You (and optionally a spouse/partner) | Free |

| 5. Issue shares | Typically 100 ordinary shares | Free |

| 6. Register for Corporation Tax | Via HMRC within 3 months of trading | Free |

| 7. Open a business bank account | Required for mortgage applications | Free–£15/month |

| 8. Appoint an accountant | Essential for annual accounts and CT600 | £500–£1,500/year |

Annual Compliance Costs

| Requirement | Cost | Deadline |

|---|---|---|

| Annual accounts (Companies House) | Included in accountant fee | 9 months after year-end |

| Corporation Tax return (CT600) | Included in accountant fee | 12 months after year-end |

| Confirmation Statement | £13 | Anniversary of incorporation |

| Corporation Tax payment | Variable | 9 months + 1 day after year-end |

| Making Tax Digital compliance | Included in accountant fee | Quarterly |

Total annual running cost (excl. tax): £500–£1,800

Corporation Tax Rates (2026)

Current Rates

| Profit Level | Rate |

|---|---|

| Up to £50,000 (small profits) | 19% |

| £50,001–£250,000 (marginal relief) | 19–25% (tapered) |

| Over £250,000 | 25% |

How Marginal Relief Works

For profits between £50,000 and £250,000, the effective rate sits between 19% and 25%. The formula creates a gradual taper — meaning a company with £100,000 profit pays approximately 22%.

For most individual property SPVs, profits will fall within the 19% small profits band — significantly lower than the 40–45% personal income tax rate.

Mortgages for Limited Companies

Key Differences from Personal BTL Mortgages

| Feature | Personal BTL | Ltd Company BTL |

|---|---|---|

| Interest rates | Lower (~4.5–5.5%) | Higher (~5.0–6.0%) |

| Arrangement fees | Standard | Often higher (1–2%) |

| LTV available | Up to 80% | Up to 75–80% |

| Personal guarantee | Not required | Always required |

| Lender choice | Wide | Growing (100+ lenders) |

| Stress test rate | ~5.5% | ~5.5–6.0% |

| ICR requirement | 125–145% | 125–145% |

Top Lenders for SPV Mortgages (2026)

| Lender | Indicative Rate (75% LTV, 5yr fix) | Notes |

|---|---|---|

| The Mortgage Works | ~5.2% | Nationwide subsidiary, competitive |

| BM Solutions | ~5.3% | Lloyds subsidiary, portfolio-friendly |

| Paragon | ~5.4% | Specialist, experienced portfolio lender |

| Landbay | ~5.5% | Tech-enabled, fast processing |

| Foundation Home Loans | ~5.3% | Specialist, complex income accepted |

| Aldermore | ~5.5% | Good for new SPVs |

The Personal Guarantee

Every limited company BTL mortgage requires a personal guarantee from the director(s). This means:

- You are personally liable if the company defaults

- The "limited liability" protection of the company does not shield you from mortgage debt

- This is universal — no lender will waive this requirement

Extracting Profits

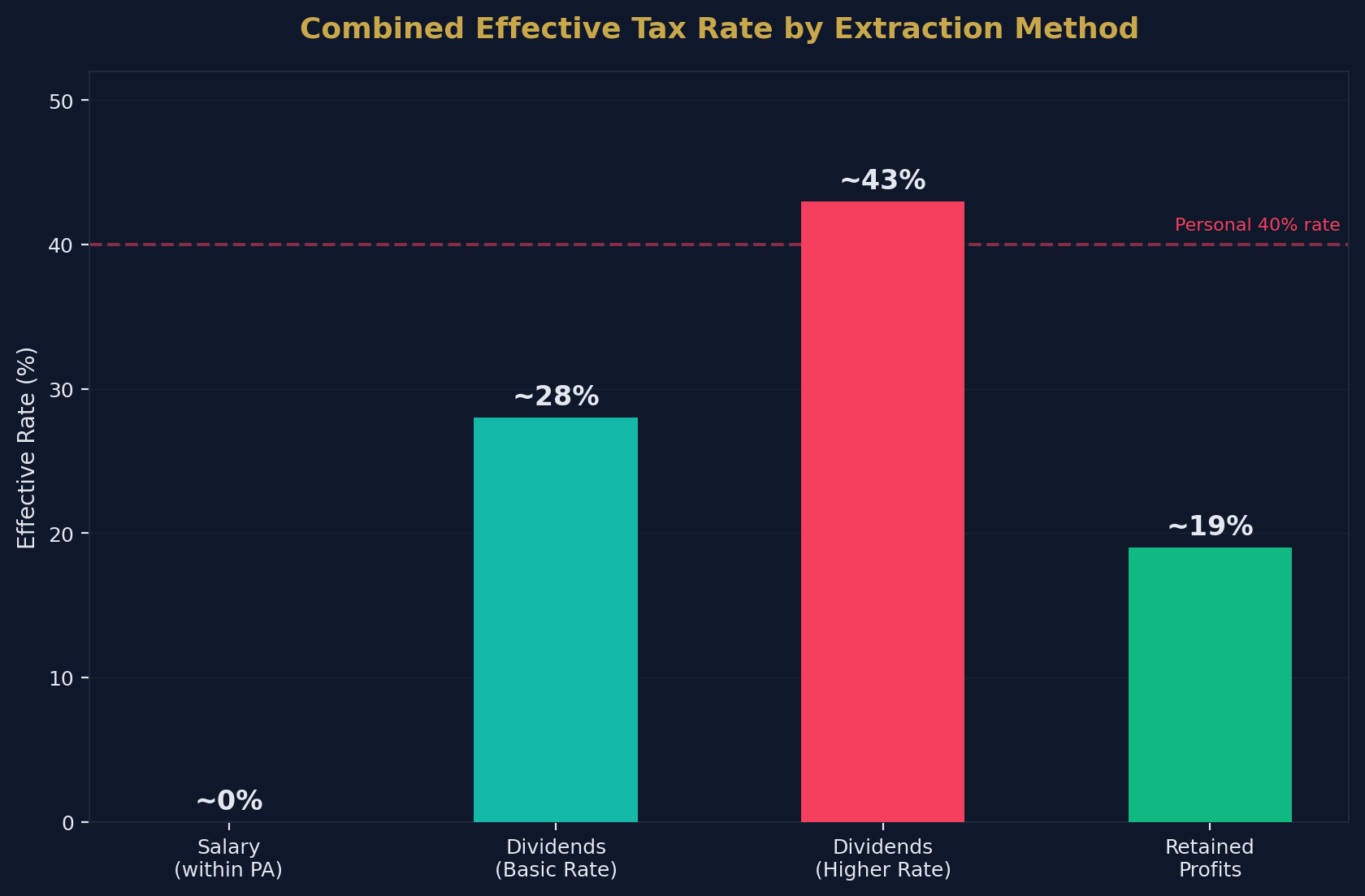

The Double Taxation Question

The headline corporation tax rate (19–25%) is only part of the picture. You also pay tax when extracting money from the company:

| Method | Company Tax | Personal Tax | Combined Effective Rate |

|---|---|---|---|

| Salary (up to £12,570 personal allowance) | Deductible expense | 0% (within PA) | ~0% + NIC |

| Dividends (basic rate) | 19–25% CT | 8.75% on dividends | ~26–31% |

| Dividends (higher rate) | 19–25% CT | 33.75% on dividends | ~39–47% |

| Retained profits | 19–25% CT | None (until extracted) | 19–25% |

The Optimal Strategy

For investors focused on portfolio growth, the strategy is clear:

- Pay yourself a small salary up to the personal allowance (£12,570) — deductible for the company, tax-free for you

- Retain profits within the company — pay only 19–25% corporation tax

- Use retained profits as deposits for the next property

- Repeat

This "retain and reinvest" approach is how professional investors compound portfolios at 19% tax vs 40%+ personally.

Incorporating an Existing Portfolio

Should You Transfer Personal Properties to a Company?

This is the most common question — and the answer is usually "it depends, and often no."

The Costs of Incorporation

| Tax | Trigger | Potential Cost (£300k property, £100k gain) |

|---|---|---|

| Capital Gains Tax | Transfer treated as disposal at market value | £24,000 (at 24%) |

| Stamp Duty | Company pays SDLT on market value + 5% surcharge | £20,000 |

| Mortgage fees | New company mortgage required | £2,000–£5,000 |

| Legal fees | Conveyancing for transfer | £1,500–£3,000 |

| Total | £47,500–£52,000 |

Incorporation Relief (Section 162 TCGA)

Section 162 can defer (not eliminate) the CGT — but it has strict conditions:

| Condition | Requirement |

|---|---|

| Transfer entire business | All assets (except cash) must transfer |

| Going concern | Business must be operational at transfer |

| Shares only | Consideration must be shares, not cash/loan |

| Business test | HMRC must accept rental activity as a "business" |

| From April 2026 | Must be actively claimed (no longer automatic) |

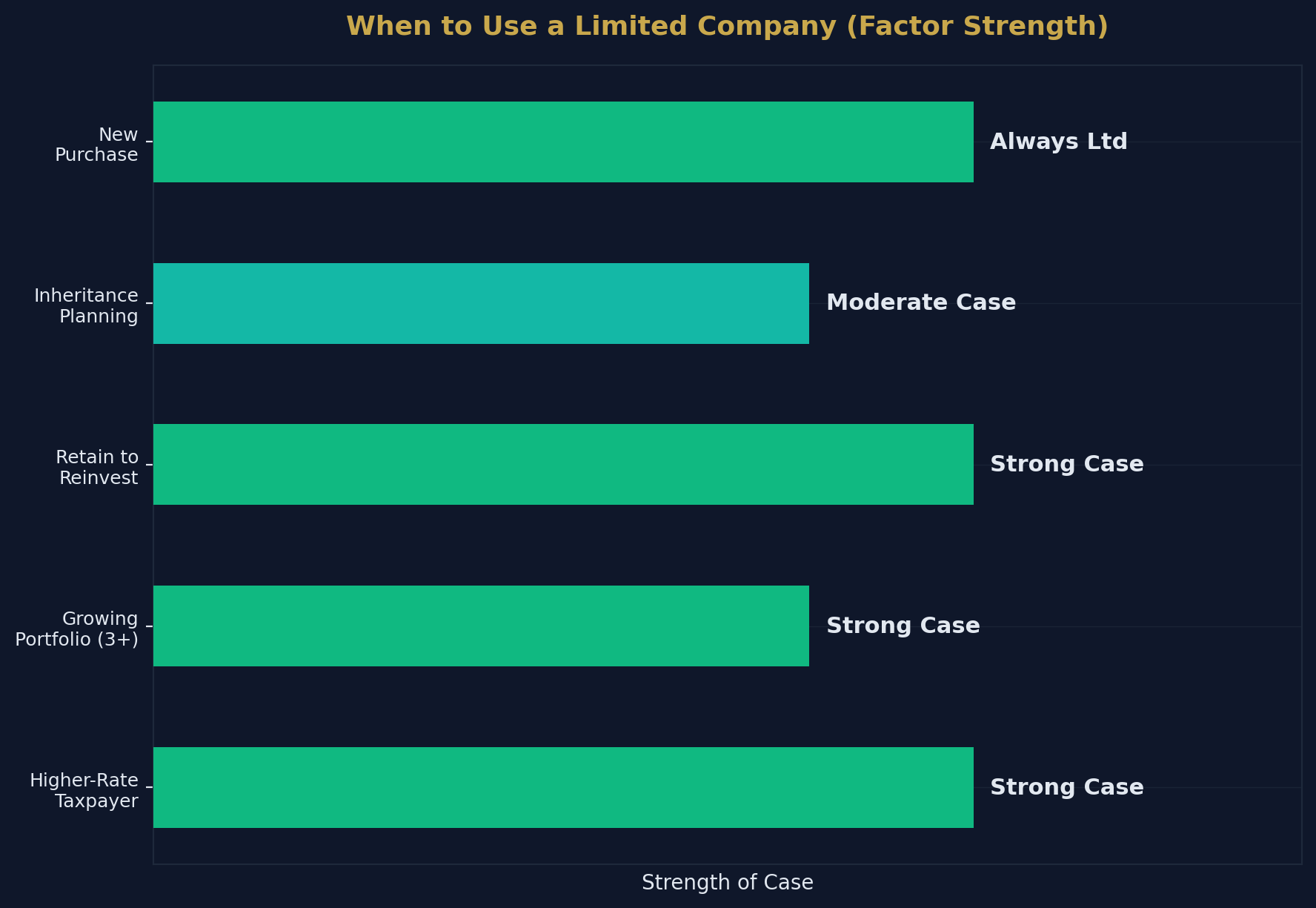

When Incorporation Makes Sense

| Scenario | Recommendation |

|---|---|

| New purchase, higher-rate taxpayer | ✅ Buy via Ltd company |

| Small portfolio (1–2 properties), basic-rate taxpayer | ❌ Stay personal |

| Large portfolio (5+), higher-rate, planning to grow | ⚠️ Model the numbers with an accountant |

| Minimal mortgage, nearing retirement | ❌ Usually not worth the costs |

| Inheritance planning priority | ✅ Shares are easier to transfer than property |

Advantages and Disadvantages

Advantages

| Advantage | Detail |

|---|---|

| ✅ Full mortgage interest deduction | Not subject to Section 24 |

| ✅ Lower tax on retained profits | 19% vs up to 45% |

| ✅ Reinvestment efficiency | Compound growth at lower tax rate |

| ✅ Inheritance planning | Transfer shares, not property |

| ✅ Professional credibility | Institutional approach |

| ✅ Renters' Rights Act compliance | Better documentation infrastructure |

Disadvantages

| Disadvantage | Detail |

|---|---|

| ❌ Higher mortgage rates | +0.3–0.5% vs personal |

| ❌ Personal guarantee required | Limited liability doesn't protect mortgage debt |

| ❌ Admin and compliance costs | £500–£1,800/year |

| ❌ Double taxation on extraction | Dividends taxed again at personal rates |

| ❌ No CGT annual exempt amount | Companies get no £3,000 AEA |

| ❌ Less privacy | Accounts filed at Companies House are public |

| ❌ SDLT surcharge on all purchases | 5% surcharge applies to every acquisition |

Decision Framework

Should You Use a Limited Company?

| Question | If Yes → | If No → |

|---|---|---|

| Are you a higher-rate (40%+) taxpayer? | Strong case for Ltd | Personal may work |

| Do you plan to grow beyond 3 properties? | Strong case for Ltd | Personal may work |

| Will you retain profits to reinvest? | Strong case for Ltd | Less advantage |

| Do you need rental income to live on? | Weaker case (extraction tax) | — |

| Are you buying your first BTL property? | Buy via Ltd from day one | — |

| Do you have existing personal properties? | Get specialist tax advice | — |

Worked Example: 5-Year Comparison

Scenario: £250,000 Property, 75% LTV, Higher-Rate Taxpayer

| Metric | Personal | Limited Company |

|---|---|---|

| Purchase price | £250,000 | £250,000 |

| Mortgage (75% LTV) | £187,500 | £187,500 |

| Annual rent | £14,400 | £14,400 |

| Annual mortgage interest | £10,200 | £10,200 |

| Other costs | £2,400 | £2,400 |

| Taxable profit | £14,400 (no interest deduction) | £1,800 |

| Tax due | £5,760 - £2,040 credit = £3,720 | £1,800 × 19% = £342 |

| After-tax profit | £-1,920 (loss after all costs) | £1,458 |

| 5-year cumulative saving via Ltd | — | £16,890 |

The 40% taxpayer loses money personally on the same property that generates £1,458/year profit through a company. This is why 80% of new BTL purchases are via Ltd.

How to Cite This Page

Limited Company Buy-to-Let: The Complete 2026 Guide. Shaded Canvas. Published April 2026. Available at: https://blog.shadedcanvas.co.uk/post/limited-company-buy-to-let-guide

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →