Every time mortgage rates rise, a geopolitical crisis hits, or a newspaper needs clicks, the same question surfaces: "Is the UK property market about to crash?" In 2026, with the Iran conflict pushing rates from 4.8% to 5.8%, landlord exits accelerating, and London prices falling, the question feels more urgent than ever.

The short answer: a broad-based crash is extremely unlikely. But that does not mean the market is risk-free. This analysis uses data — not opinion — to examine every crash trigger, compare 2026 conditions with the crashes of 1989 and 2008, and identify the real risks property investors should prepare for.

Last Updated: April 2026 | Data: ONS, Land Registry, Bank of England, UK Finance

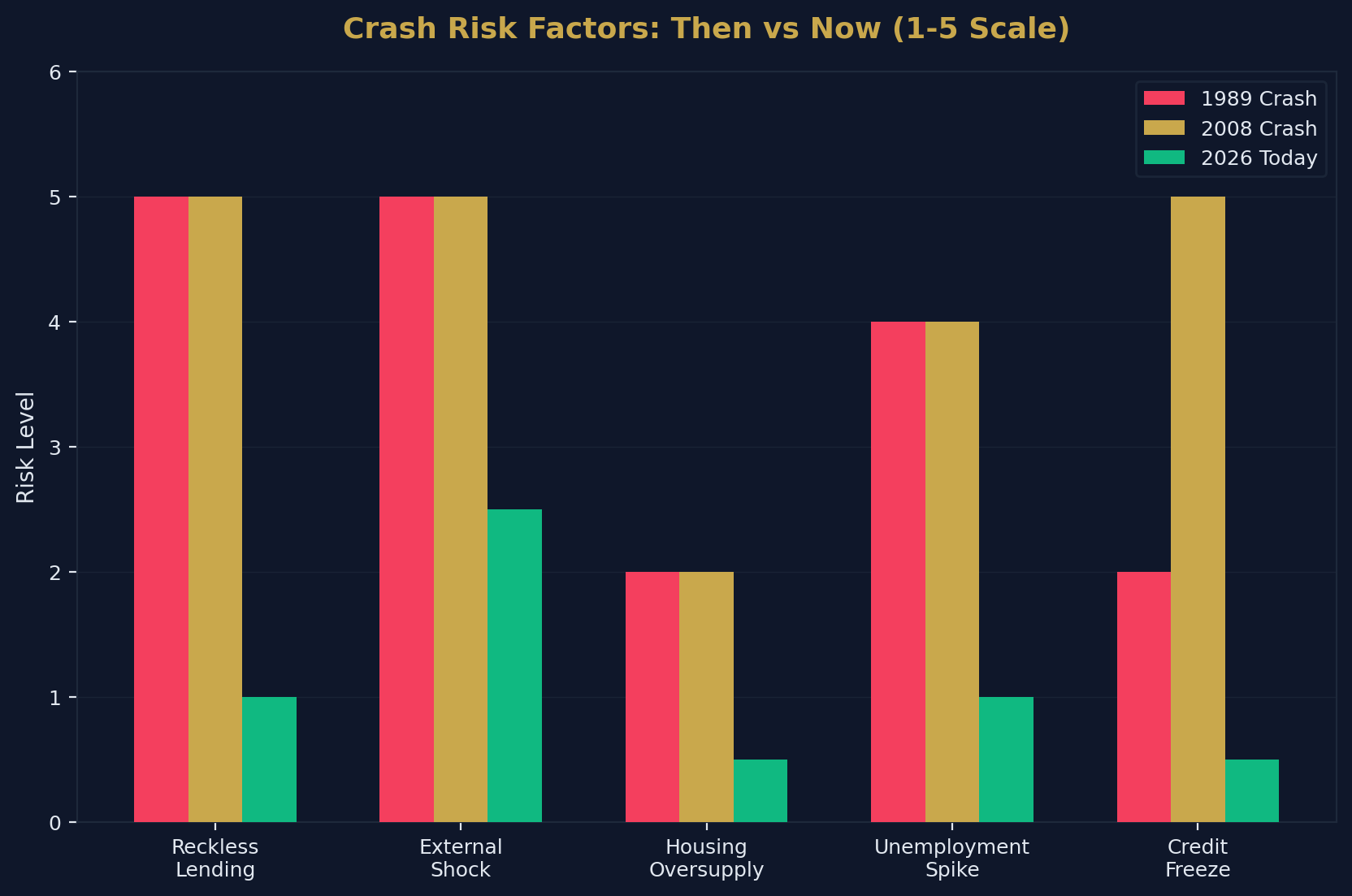

What Caused Previous UK Crashes

1989–1993: The Interest Rate Shock

| Factor | Detail |

|---|---|

| Trigger | Bank of England raised rates to 15% to fight inflation |

| Cause | MIRAS tax relief withdrawal created a buying frenzy in 1988 (Lawson Boom) |

| Price drop | -20% nationally (nominal) |

| Recovery time | 6 years to regain peak (1999) |

| Repossessions | 75,500 in 1991 alone |

| Lending standards | Loose — minimal affordability checks |

2008–2009: The Global Financial Crisis

| Factor | Detail |

|---|---|

| Trigger | US subprime mortgage collapse, global banking crisis |

| Cause | Reckless lending — self-certified "liar loans," 125% LTV mortgages, interest-only products |

| Price drop | -15 to -20% nationally |

| Recovery time | 5 years to regain peak (2013–2014) |

| Repossessions | 46,000 in 2009 |

| Lending standards | Extremely loose — income not verified |

The Common Thread

Both crashes shared three ingredients:

- Reckless lending — borrowers taking on unaffordable debt

- External economic shock — rate spikes or banking collapse

- Oversupply — more properties than buyers/tenants needed

The question for 2026: are any of these ingredients present today?

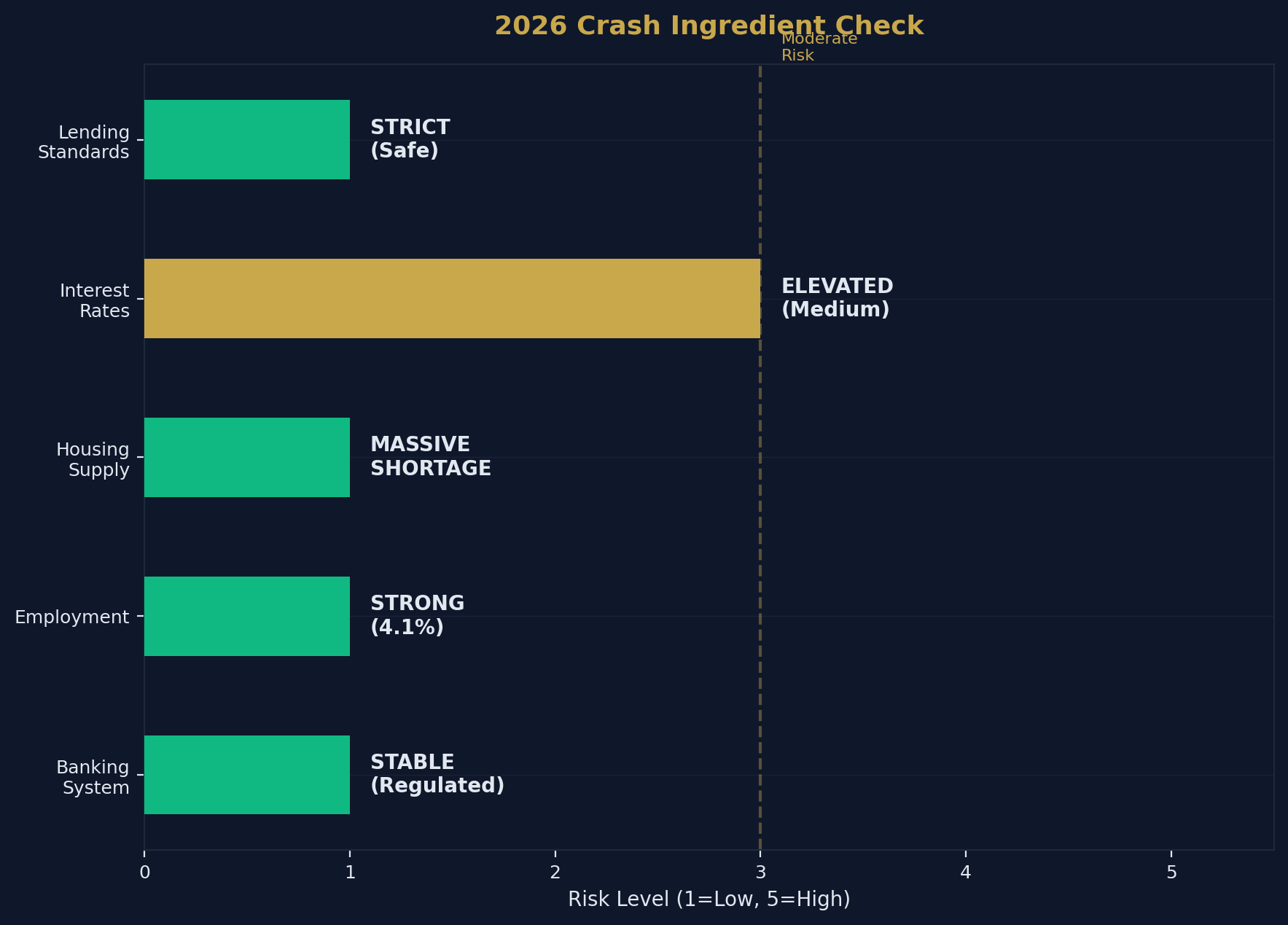

2026 Conditions: Crash Ingredient Check

Ingredient 1: Lending Standards

| Metric | Pre-2008 | 2026 |

|---|---|---|

| Self-certified mortgages | Widespread | Banned since 2014 |

| Average LTV (new lending) | 85–90% | 72% |

| 95%+ LTV share of lending | ~15% | <5% |

| Stress test requirement | None | Mandatory (at ~8–9%) |

| Income verification | Often skipped | Always verified |

| Interest-only (residential) | Very common | Rare (<10%) |

| Affordability check | Minimal | FCA-regulated, strict |

Verdict: ❌ Lending is not reckless. Post-2014 regulation means today's borrowers can afford their mortgages even if rates rise further. Arrears remain near historic lows.

Ingredient 2: External Shock

| Risk Factor | Status (April 2026) | Severity |

|---|---|---|

| Iran conflict → oil price surge | Active | Medium |

| Mortgage rates rising (4.8% → 5.8%) | Active | Medium |

| Inflation persistence | Moderate (~3.5%) | Medium |

| Bank of England base rate | 4.25% (holding) | Neutral |

| Unemployment | 4.1% (low) | Low risk |

| UK recession | Not in recession | Low risk |

Verdict: ⚠️ External pressure exists — but it is not at 1989 or 2008 levels. Rates are elevated but nowhere near 15%. The economy is not in recession. Employment is strong.

Ingredient 3: Supply vs Demand

| Metric | Detail |

|---|---|

| Annual housing need | ~300,000 homes |

| Annual completions | ~220,000 homes |

| Annual shortfall | ~80,000 homes |

| Cumulative shortage | 4.3 million homes (CPRE estimate) |

| Population growth | +0.5% per year |

| Net migration | 500,000+ (2024), declining in 2026 |

| Household formation | Outpacing supply |

Verdict: ❌ There is no oversupply. The UK has a massive, structural housing shortage. This is the single most important reason prices don't crash — there are always more buyers and tenants than homes.

What IS Happening Instead of a Crash

The Two-Speed Market

The UK is not crashing — it is diverging:

| Market Segment | Performance (2025–2026) |

|---|---|

| Northern cities (Manchester, Leeds, Liverpool) | +3–4% growth |

| Midlands (Birmingham, Nottingham) | +2–3% growth |

| Scotland (Glasgow, Edinburgh) | +3–3.5% growth |

| South West (Bristol, Bath) | +0.5–1.5% growth |

| South East | -0.5% (slight decline) |

| London | -3.3% (correction) |

| London flats specifically | -5 to -8% (significant correction) |

London is correcting — but London is not the UK. Northern markets are growing because they remain affordable relative to local incomes. Where to invest →

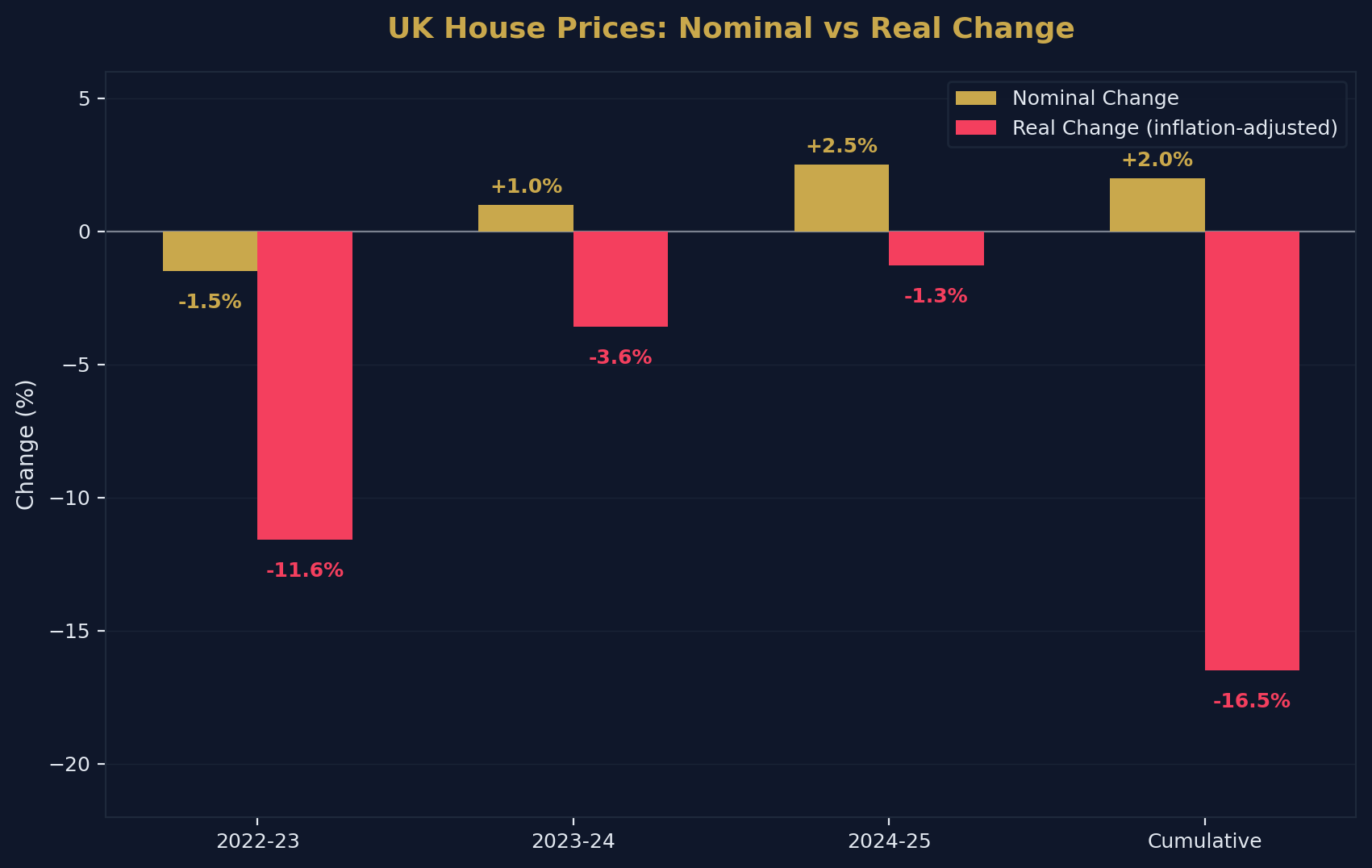

A "Real Terms" Correction Is Already Happening

When you adjust for inflation (which has run at 5–10% over 2022–2025), real house prices have already fallen significantly:

| Period | Nominal Change | Inflation | Real Change |

|---|---|---|---|

| 2022–2023 | -1.5% | +10.1% | -11.6% |

| 2023–2024 | +1.0% | +4.6% | -3.6% |

| 2024–2025 | +2.5% | +3.8% | -1.3% |

| Cumulative | +2.0% | +19.3% | -16.5% |

In real terms, prices have already fallen ~16.5% over three years. The correction has happened — it just happened through inflation rather than a nominal price crash.

The Real Risks for Investors

A crash may not be coming, but risks are real:

1. Interest Rate Risk

| Scenario | Impact on £200k property (75% LTV) |

|---|---|

| Current rate (5.5%) | £850/month |

| Rate rises to 6.5% | £1,000/month (+18%) |

| Rate rises to 7.5% | £1,160/month (+36%) |

Mitigation: Fix for 5 years. Stress-test at 8%. Ensure rental yield covers at 145% ICR minimum.

2. Regulatory Risk

| Regulation | Impact |

|---|---|

| Renters' Rights Act | Longer eviction timelines, higher compliance costs |

| EPC C deadline (2030) | £3,000–£10,000 upgrade cost per property |

| Making Tax Digital | Quarterly reporting burden (personal landlords) |

| Stamp duty surcharge (5%) | Higher acquisition costs |

Mitigation: Use limited company structures. Budget for compliance. Professional management.

3. Localised Corrections

Some micro-markets ARE at risk:

- London new-build flats — oversupply in certain developments

- Purpose-built student blocks — some cities saturated

- Over-leveraged portfolios — landlords who bought at peak rates

Mitigation: Focus on proven investment cities. Avoid oversaturated developments. Maintain conservative leverage.

What Smart Investors Are Doing

| Strategy | Detail |

|---|---|

| Buying Northern value | Acquiring below-market stock in Liverpool, Sheffield, Glasgow |

| Forced appreciation | Buying low-EPC properties, upgrading to C, capturing £10k+ uplift |

| Portfolio purchases | Acquiring from exiting amateur landlords at 10–15% discounts |

| Fixing rates | Locking in 5-year fixes while rates are available |

| Going Ltd | 80% of new BTL via limited companies for tax efficiency |

| Diversifying by city | Spreading risk across multiple regions |

The Bottom Line

| Question | Answer |

|---|---|

| Will the UK property market crash? | Extremely unlikely |

| Why? | Structural undersupply (4.3m homes), strict lending, strong employment |

| Is it risk-free? | No — rates, regulation, and local corrections are real |

| Should I wait to buy? | No — timing the market is impossible; time in the market matters |

| Where should I invest? | Northern cities with 6%+ yields |

How to Cite This Page

Will the UK Property Market Crash in 2026? What the Data Actually Shows. Shaded Canvas. Published April 2026. Available at: https://blog.shadedcanvas.co.uk/post/uk-property-market-crash-2026

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →