Property is one of the most heavily taxed asset classes in the UK — and the tax burden is increasing. This page consolidates every critical property tax statistic for 2026, from stamp duty receipts and capital gains tax revenues to rental income tax, council tax, ATED, and the forthcoming Making Tax Digital obligations. Whether you are a landlord planning your tax strategy, an investor evaluating after-tax returns, or a researcher tracking fiscal policy, this is the definitive reference.

Last Updated: April 2026 | Next Update: July 2026

Key Property Tax Statistics at a Glance

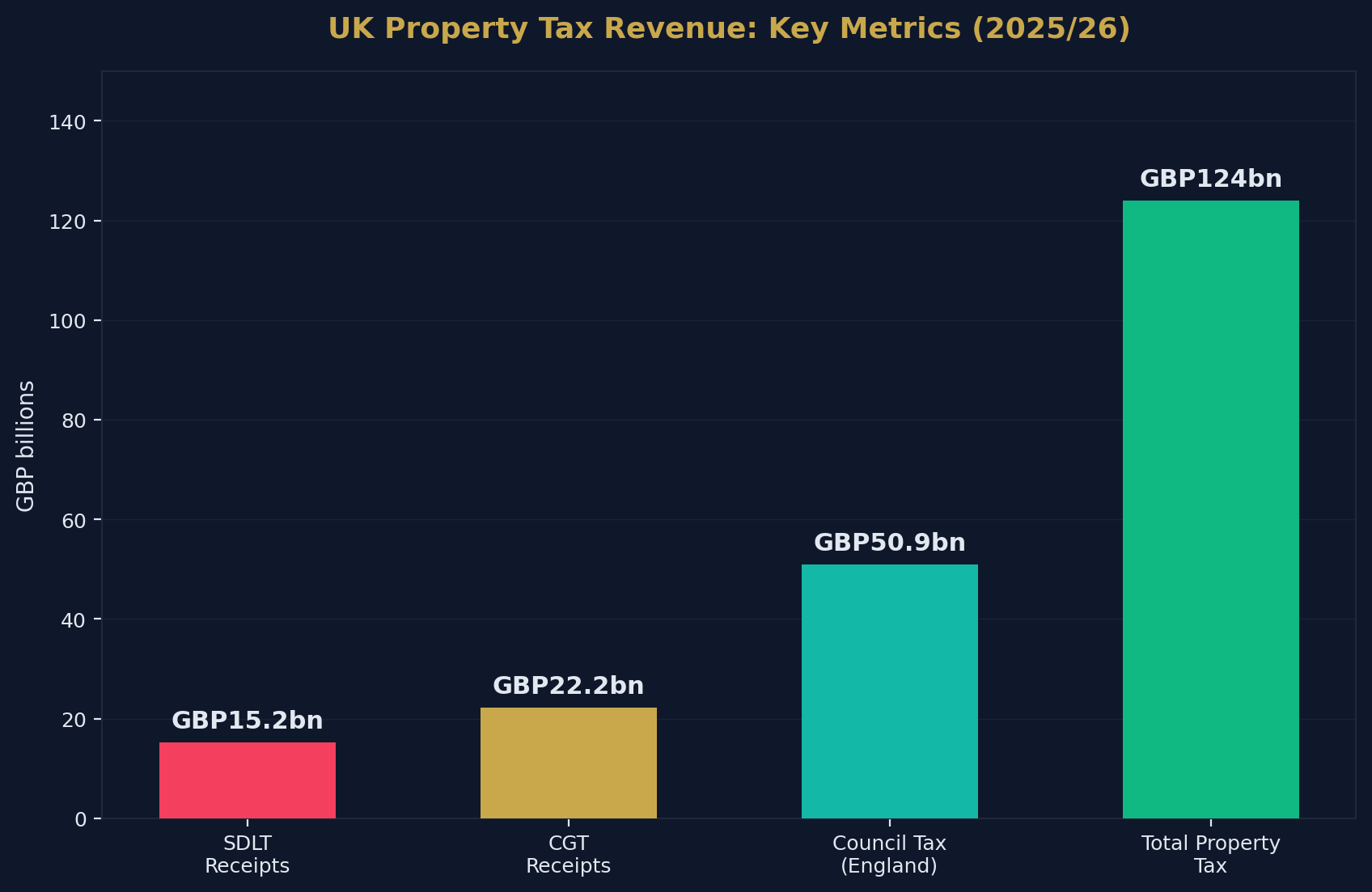

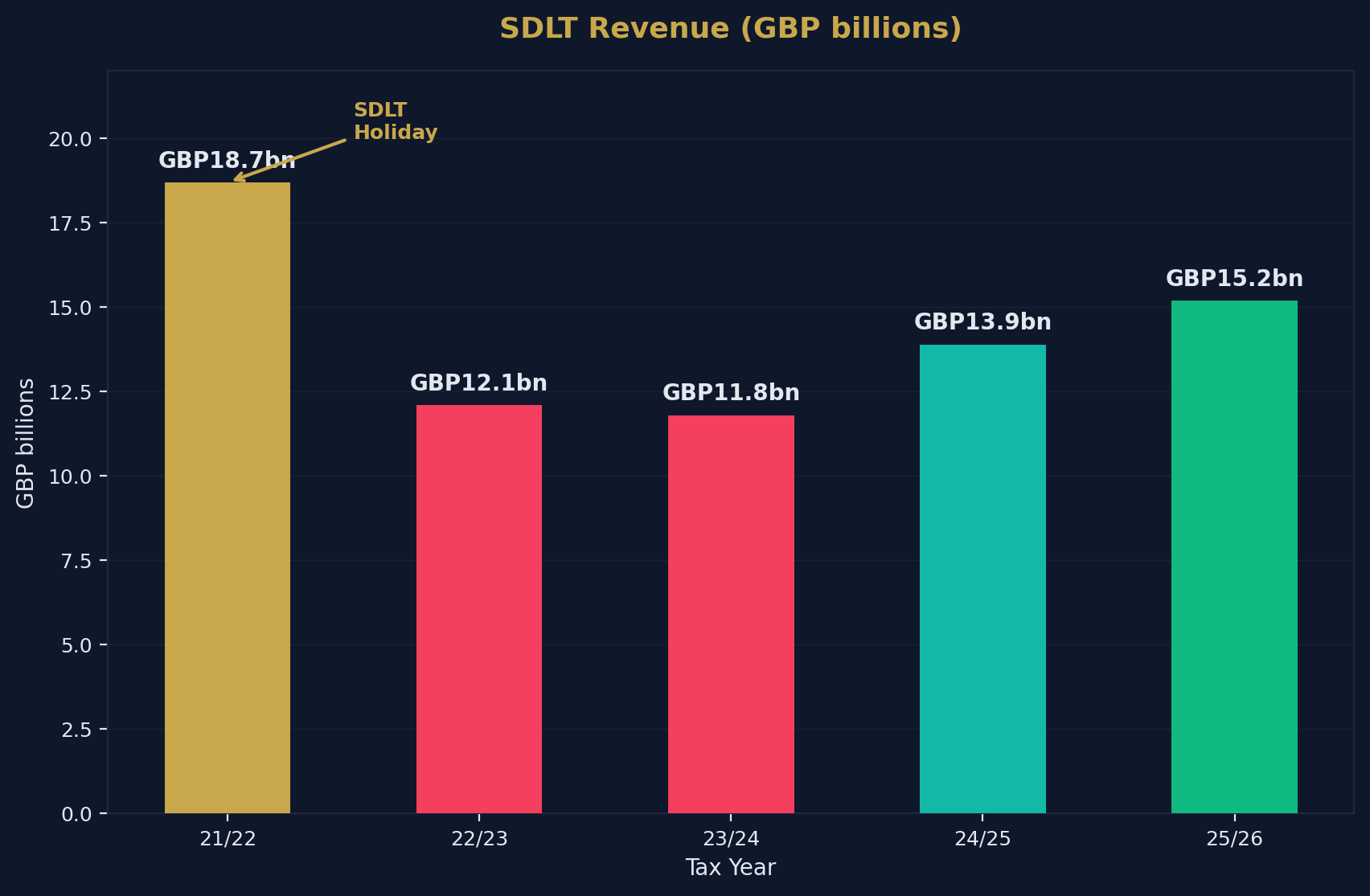

- HMRC collected £15.2 billion in SDLT for 2025/26 — up 9.2% year-on-year.

- Total Stamp Taxes (including SDLT) reached £20.0 billion for the year.

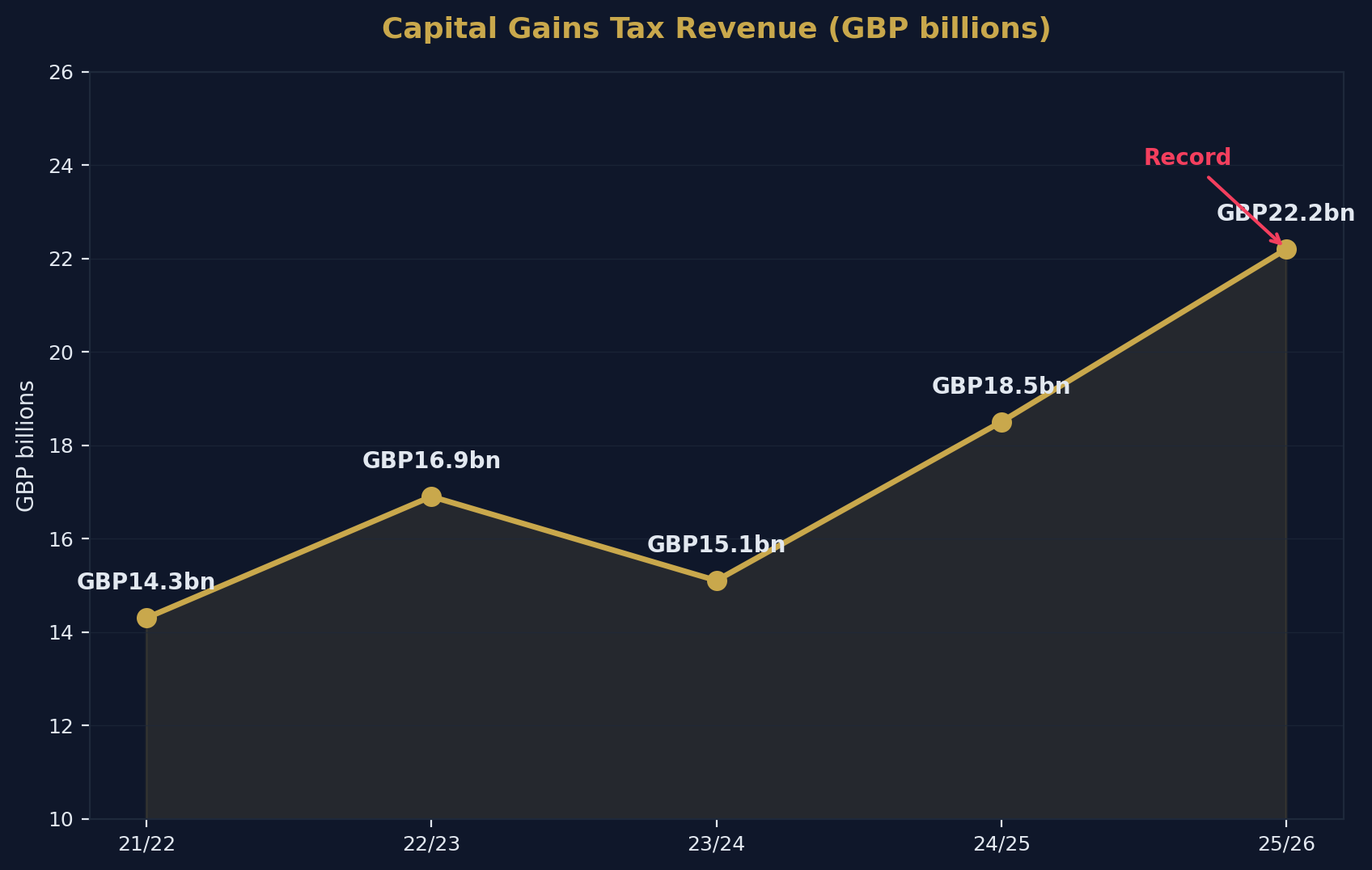

- CGT receipts hit a record £22.2 billion in 2025/26 — up from £16.9 billion.

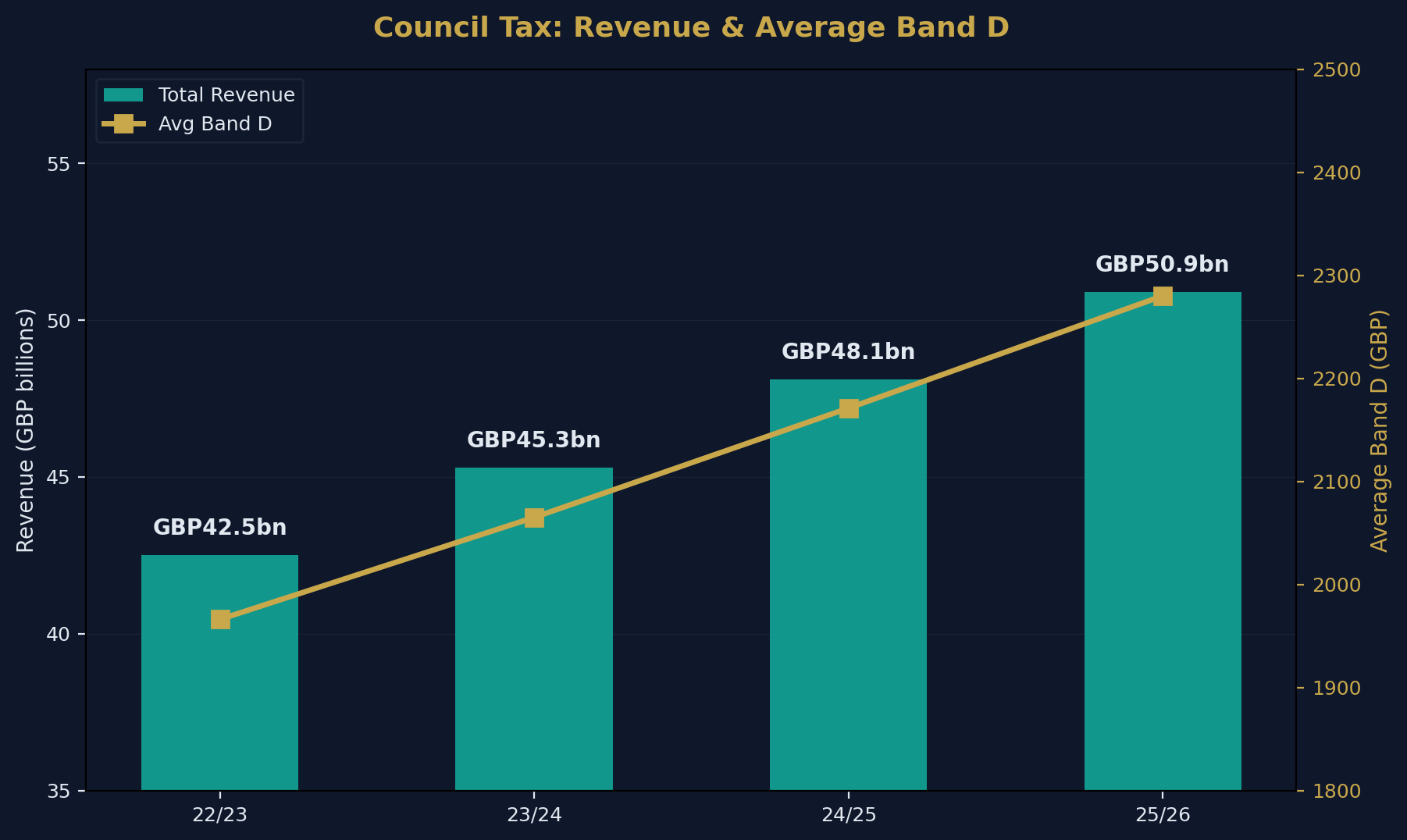

- Council tax in England raised £50.9 billion (net) in 2025/26.

- Average Band D council tax is £2,280 — up 5.0% year-on-year.

- CGT rates on residential property: 18% (basic rate) and 24% (higher rate).

- The CGT annual exempt amount has been reduced to £3,000 (from £12,300 in 2022/23).

- Making Tax Digital applies from April 2026 for landlords with >£50,000 gross income.

- Income tax rates on property income will increase by +2 percentage points from April 2027.

- The <a href="/post/stamp-duty-on-buy-to-let" style="color:#c9a84c;text-decoration:underline;font-weight:500">SDLT surcharge on additional dwellings is 5% (raised from 3% in October 2024).

- A "high-value council tax surcharge" on £2m+ properties begins April 2028.

- ATED charges increased 3.8% for 2026/27.

- Property-related taxes generate approximately £90+ billion per year for the Exchequer.

Source: Shaded Canvas analysis of HMRC, OBR, DLUHC, and UK Finance data. Last updated April 2026.

Stamp Duty Land Tax (SDLT)

SDLT Revenue

| Year | SDLT Receipts | YoY Change |

|---|---|---|

| 2021/22 | £18.7 billion | SDLT holiday distortion |

| 2022/23 | £12.1 billion | -35% (rate reversal) |

| 2023/24 | £11.8 billion | -2% |

| 2024/25 | £13.9 billion | +18% |

| 2025/26 | £15.2 billion | +9.2% |

SDLT Rates (From 1 April 2025)

Standard Residential:

| Band | Rate |

|---|---|

| Up to £125,000 | 0% |

| £125,001 – £250,000 | 2% |

| £250,001 – £925,000 | 5% |

| £925,001 – £1,500,000 | 10% |

| Over £1,500,000 | 12% |

First-Time Buyer Relief:

| Band | Rate |

|---|---|

| Up to £300,000 | 0% |

| £300,001 – £500,000 | 5% |

Additional Dwellings Surcharge: +5% on each band

SDLT Bill Examples

| Property Value | Standard | FTB | BTL/2nd Home |

|---|---|---|---|

| £200,000 | £1,500 | £0 | £11,500 |

| £300,000 | £5,000 | £0 | £20,000 |

| £400,000 | £10,000 | £5,000 | £30,000 |

| £500,000 | £15,000 | £10,000 | £40,000 |

| £750,000 | £27,500 | N/A | £65,000 |

Capital Gains Tax (Property)

CGT Revenue and Changes

| Year | Total CGT Receipts | Key Changes |

|---|---|---|

| 2021/22 | £14.3 billion | — |

| 2022/23 | £16.9 billion | Previous peak |

| 2023/24 | £15.1 billion | AEA reduced to £6,000 |

| 2024/25 | £18.5 billion (est.) | AEA reduced to £3,000; rates raised |

| 2025/26 | £22.2 billion | Record — landlord disposals surge |

Current CGT Rates on Residential Property

| Taxpayer | Rate |

|---|---|

| Basic rate | 18% |

| Higher/additional rate | 24% |

| Non-resident | 18% / 24% |

| Company (corporation tax) | 25% |

The Landlord Disposal Effect

The surge in CGT receipts is directly linked to landlord exits from the private rented sector:

- An estimated 220,000 households are exiting the PRS

- Each disposal generates a CGT liability (unless principal private residence relief applies)

- Average capital gains on BTL properties: £80,000–£150,000 depending on region and holding period

- At 24% on a £100,000 gain = £24,000 CGT per disposal

Income Tax on Rental Income

Key Statistics

| Metric | Figure |

|---|---|

| Estimated rental income tax receipts | ~£6.5 billion/year |

| Number of landlords filing rental income | ~2.2 million |

| Section 24 restriction | Full (20% basic rate credit only) |

| MTD threshold (from April 2026) | >£50,000 gross income |

| MTD extended (from April 2027) | >£30,000 gross income |

Tax Comparison: Personal vs Limited Company

| Metric | Personal Landlord (40% taxpayer) | Limited Company |

|---|---|---|

| Rental income | £20,000 | £20,000 |

| Mortgage interest (£8,000) | 20% tax credit only = £1,600 | Full deduction |

| Taxable profit | £20,000 | £12,000 |

| Tax due | £8,000 - £1,600 = £6,400 | £12,000 × 25% = £3,000 |

| Effective rate | 32% | 15% |

This 17 percentage point differential is the primary driver behind the limited company revolution — 75–80% of new BTL purchases now use corporate structures.

Council Tax

Council Tax Revenue and Rates

| Year | Total Revenue (England) | Avg Band D | YoY Increase |

|---|---|---|---|

| 2022/23 | £42.5 billion | £1,966 | +3.5% |

| 2023/24 | £45.3 billion | £2,065 | +5.1% |

| 2024/25 | £48.1 billion | £2,171 | +5.1% |

| 2025/26 | £50.9 billion | £2,280 | +5.0% |

Council Tax Bands (2025/26 Average, England)

| Band | Property Value (1991) | Average Annual Charge |

|---|---|---|

| A | Up to £40,000 | £1,520 |

| B | £40,001–£52,000 | £1,773 |

| C | £52,001–£68,000 | £2,027 |

| D | £68,001–£88,000 | £2,280 |

| E | £88,001–£120,000 | £2,787 |

| F | £120,001–£160,000 | £3,293 |

| G | £160,001–£320,000 | £3,800 |

| H | Over £320,000 | £4,560 |

The Revaluation Question

Council tax bands are still based on 1991 property values — making them wildly out of date. A £68,000 Band D property in 1991 could be worth £400,000+ today. The government has announced a "high-value council tax surcharge" on properties worth over £2 million (at 2026 valuations), beginning April 2028.

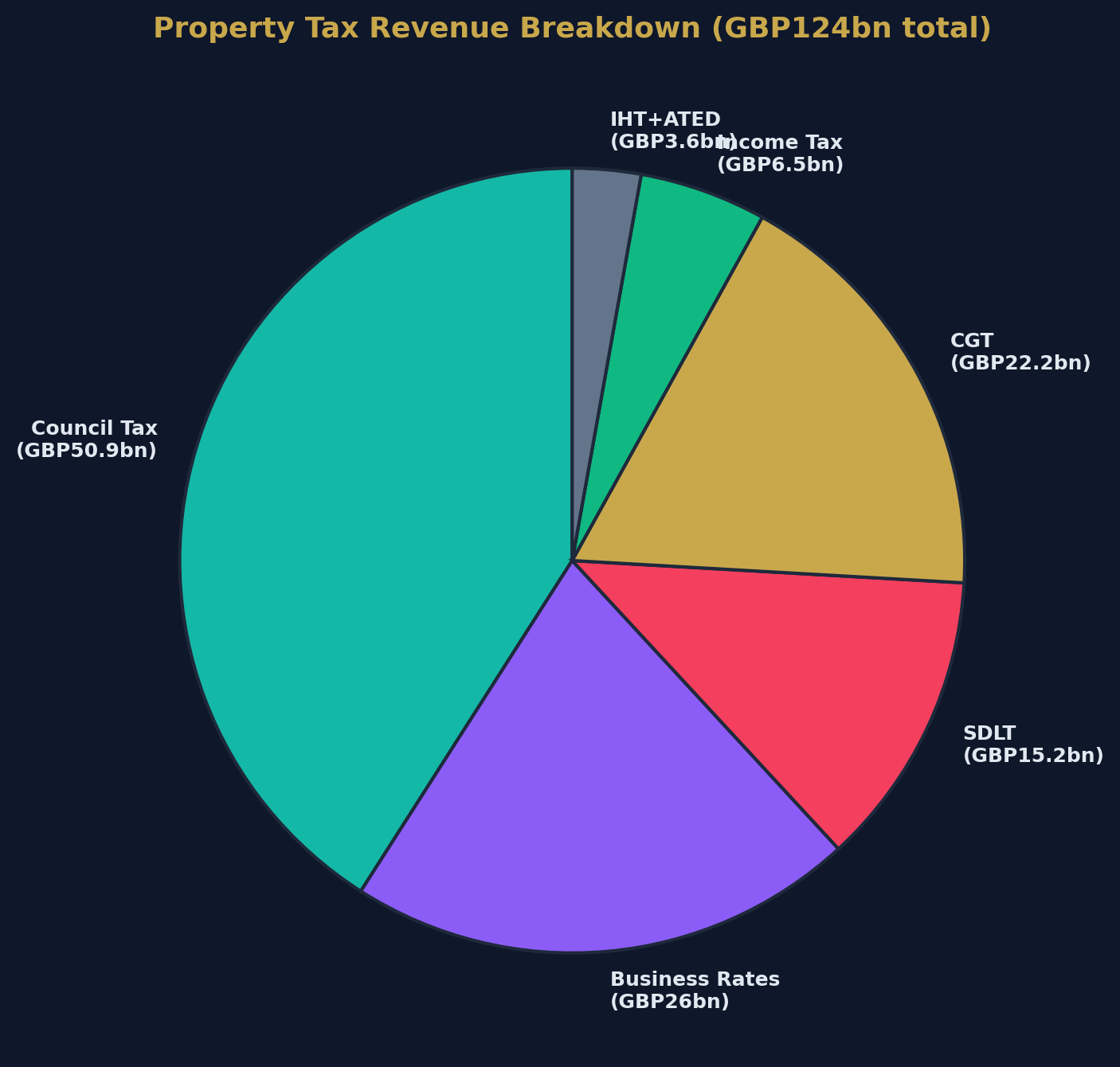

Total Property Tax Burden

All Property-Related Taxes (2025/26)

| Tax | Revenue |

|---|---|

| Council Tax | £50.9 billion |

| Stamp Duty Land Tax | £15.2 billion |

| Capital Gains Tax | £22.2 billion |

| Income Tax (rental) | ~£6.5 billion |

| Inheritance Tax (property share) | ~£3.5 billion |

| ATED | ~£0.1 billion |

| Business Rates (commercial property) | ~£26 billion |

| Total | ~£124 billion |

Property-related taxes represent approximately 12–15% of all government revenue — making housing one of the most strategically important tax bases for the Exchequer.

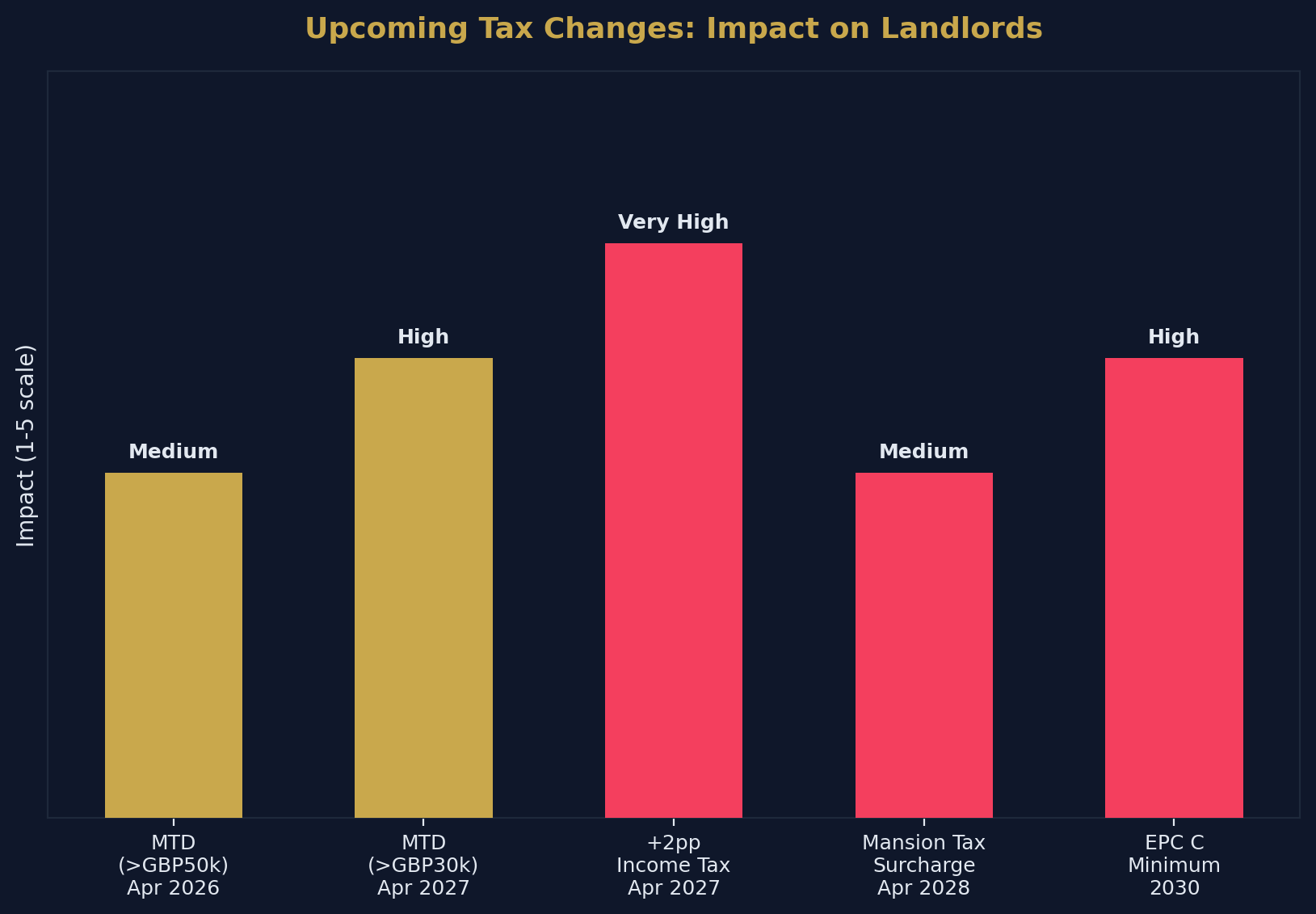

Tax Timeline for Landlords (2026–2028)

| Date | Change | Impact |

|---|---|---|

| April 2026 | MTD for ITSA (>£50k income) | Quarterly digital reporting |

| October 2026 | Expected CGT reporting changes | Potential administrative changes |

| April 2027 | MTD extended (>£30k income) | More landlords in scope |

| April 2027 | +2pp income tax on property income | 22%/42%/47% rates |

| April 2028 | High-value council tax surcharge | Properties over £2m |

| Ongoing | Section 24 restrictions | Full impact (20% credit only) |

| Expected 2030 | EPC C minimum | £5,000–£15,000 per property |

Tax Optimisation Strategies

Legal Tax Planning for Property Investors

| Strategy | Potential Saving | Complexity |

|---|---|---|

| Limited company ownership | 15–30% on income tax | Medium |

| Spouse/partner income splitting | Up to £12,570 tax-free | Low |

| Capital allowances (furnished lettings) | £1,000 property allowance | Low |

| Incorporation relief | Deferral of CGT on transfer | High |

| Pension contributions from rental income | 20–45% tax relief | Medium |

| Offset losses against future gains | Reduces CGT liability | Low |

For investors who buy through a sourcer, the finder's fee set out in the property sourcing agreement is a further acquisition cost to budget alongside these taxes.

Methodology and Data Sources

| Source | Data Type | Coverage |

|---|---|---|

| HMRC | SDLT, CGT, Income Tax receipts | UK |

| OBR | Tax revenue forecasts | UK |

| DLUHC | Council tax levels and revenue | England |

| UK Finance | Mortgage/property data | UK |

| Savills/Hamptons | Landlord tax analysis | UK |

How to Cite This Page

UK Property Tax Statistics 2026. Shaded Canvas. Published April 2026, updated quarterly. Available at: https://blog.shadedcanvas.co.uk/post/uk-property-tax-statistics-2026

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →