The UK rental market is at a structural inflection point. After three years of intense tenant competition and double-digit rent rises, the market is rebalancing — but supply remains 23–33% below pre-pandemic levels and affordability is stretched to breaking point. This page consolidates every critical rental market statistic for 2026, from tenant demographics and rent-to-income ratios to supply dynamics, Build-to-Rent growth, and the impact of the Renters' Rights Act.

Whether you are a tenant benchmarking your rent, an investor analysing demand, or a policymaker tracking housing affordability, this is the definitive reference.

Last Updated: April 2026 | Next Update: July 2026

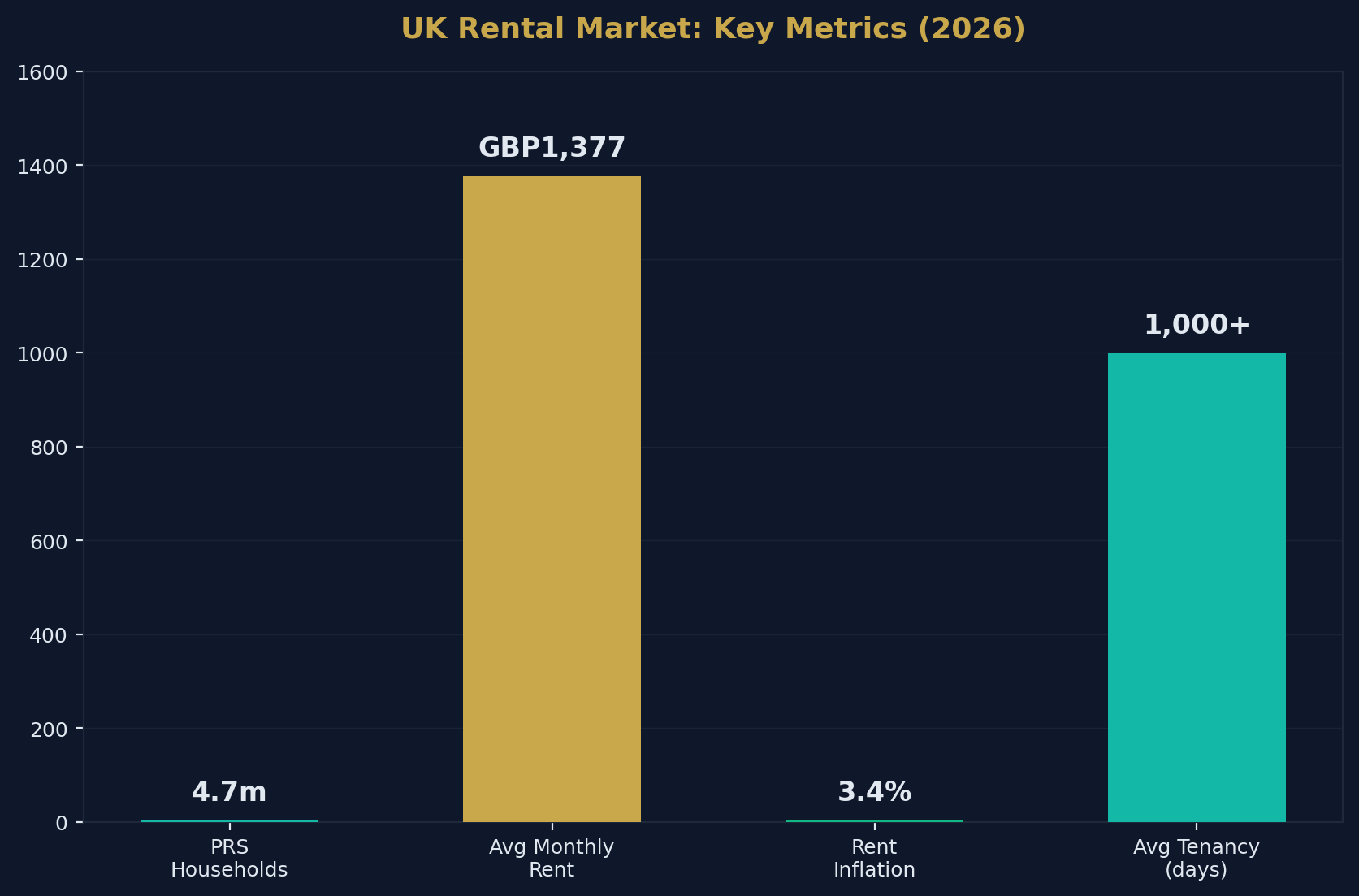

Key Rental Market Statistics at a Glance

- There are approximately 4.7 million privately rented households in England.

- The average UK monthly private rent is £1,377 (ONS, March 2026).

- Annual rent inflation has decelerated to 3.4% — the lowest since March 2022.

- London rents average £2,280/month; North East rents average £772/month.

- The average UK renter spends 41% of take-home pay on rent.

- London renters spend 48% of take-home pay on rent.

- The average tenancy length in England & Wales is 1,000+ days (~2.7 years).

- Rental stock remains 23–33% below pre-pandemic levels.

- Enquiries per rental property have fallen to ~4.8 — down from 8+ in 2022 but double the 2019 average.

- 26% of rental listings now require price reductions to attract tenants.

- Build-to-Rent investment reached £5.3 billion in 2025, projected at £5.7bn for 2026.

- BTR occupancy rates average ~97%.

- The Renters' Rights Act takes effect 1 May 2026 — abolishing Section 21 evictions.

- Savills forecasts cumulative rental growth of 12% over 2026–2030.

- Renters aged 25–34 remain the largest demographic group in the PRS.

- Renters aged 55+ are the fastest-growing demographic — now 1 in 5 private renters.

Source: Shaded Canvas analysis of ONS, Zoopla, Rightmove, English Housing Survey, and Savills data. Last updated April 2026.

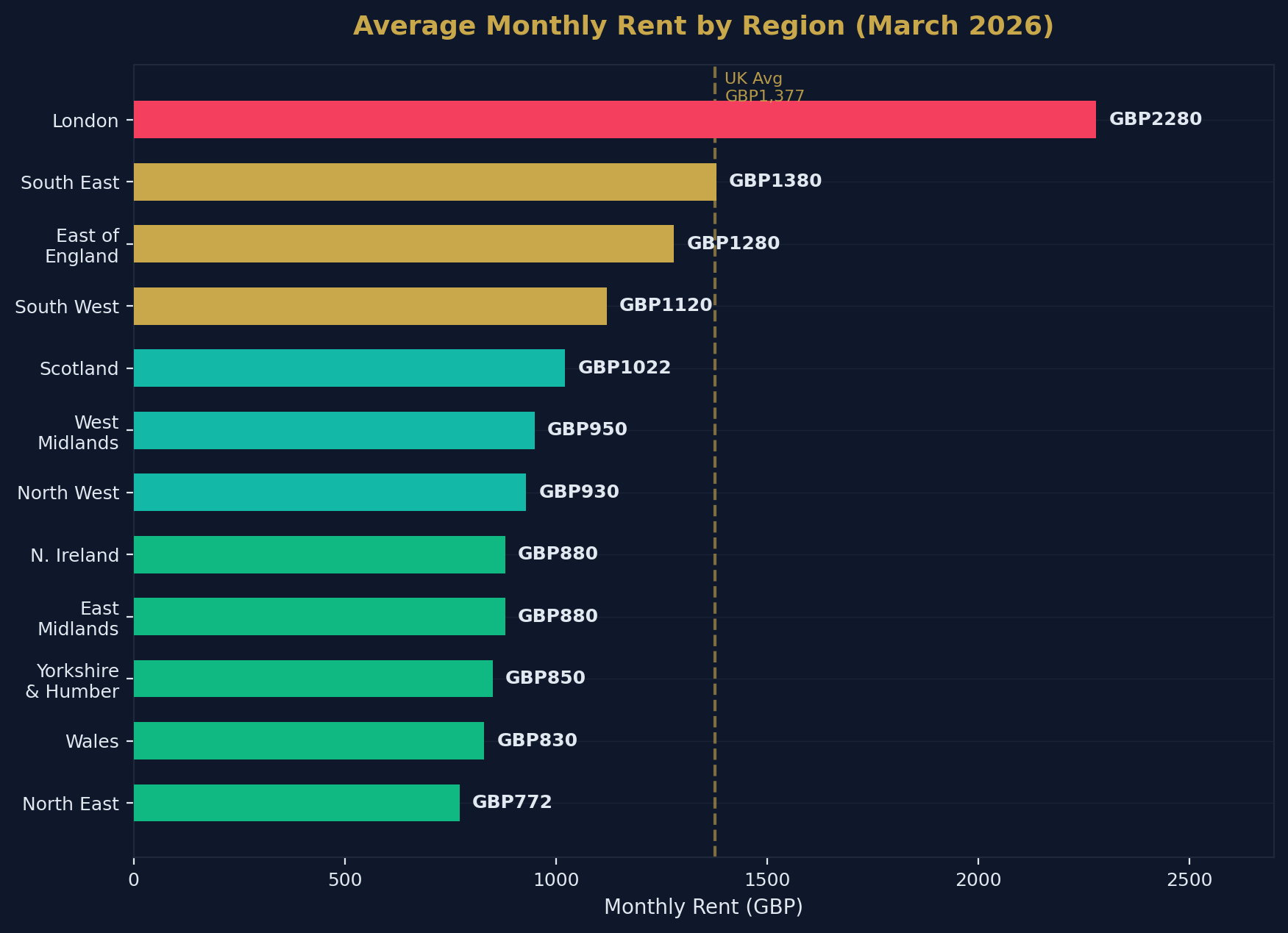

Average Rent by Region

ONS Private Rental Index (March 2026)

| Region | Average Monthly Rent | Annual Change |

|---|---|---|

| London | £2,280 | +1.7% |

| South East | £1,380 | +2.8% |

| East of England | £1,280 | +3.2% |

| South West | £1,120 | +3.8% |

| West Midlands | £950 | +4.5% |

| East Midlands | £880 | +4.8% |

| North West | £930 | +4.2% |

| Yorkshire & Humber | £850 | +5.2% |

| North East | £772 | +6.5% |

| Wales | £830 | +4.8% |

| <a href="/post/invest-in-scotland-property" style="color:#c9a84c;text-decoration:underline;font-weight:500">Scotland | £1,022 | +2.1% |

| Northern Ireland | £880 | +5.0% |

| UK Average | £1,377 | +3.4% |

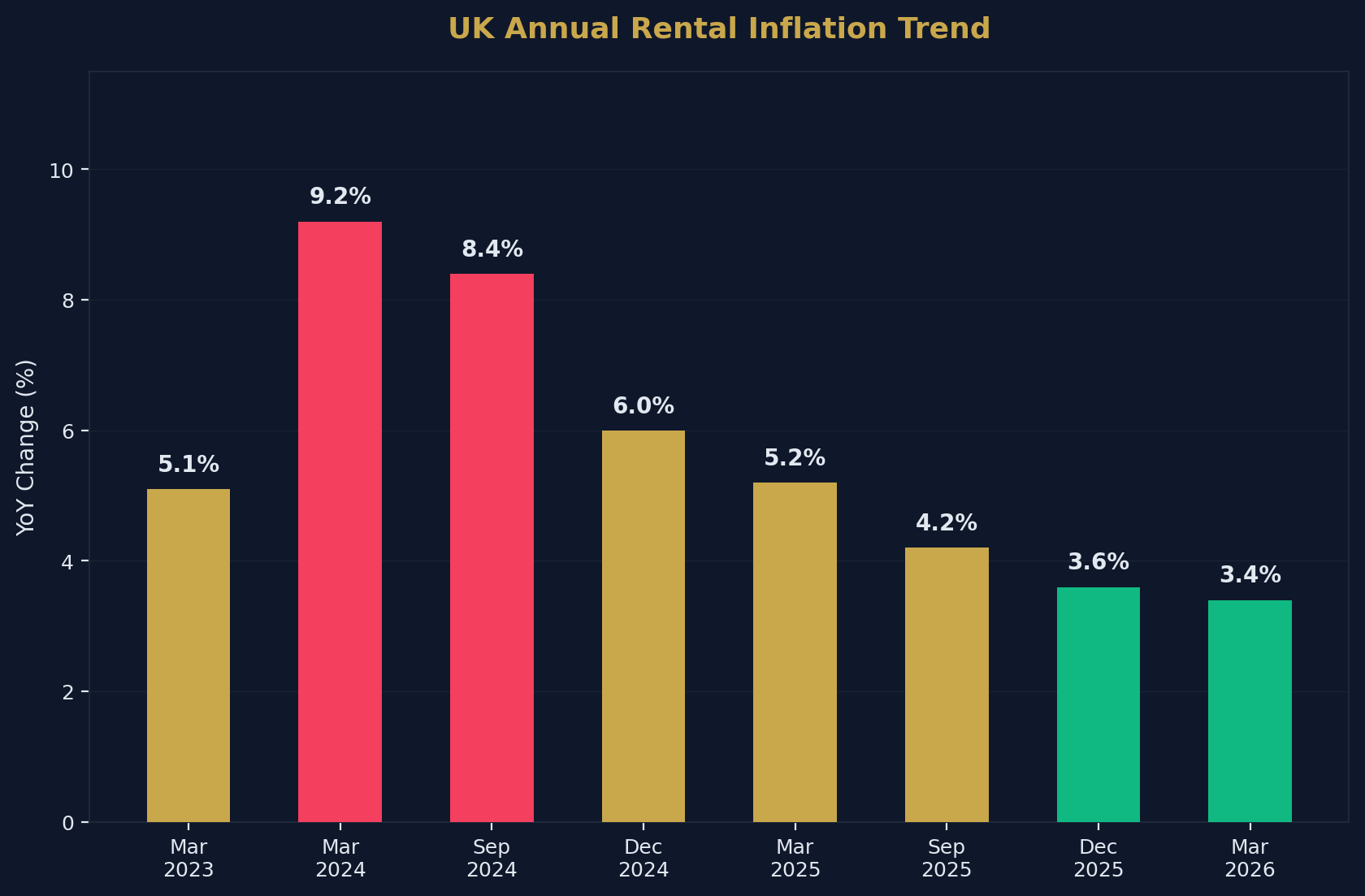

Rental Inflation: The Deceleration Story

Annual rent inflation has fallen sharply from its peak:

| Period | Annual Rent Inflation |

|---|---|

| March 2023 | 5.1% |

| March 2024 | 9.2% |

| September 2024 | 8.4% |

| December 2024 | 6.0% |

| March 2025 | 5.2% |

| September 2025 | 4.2% |

| December 2025 | 3.6% |

| March 2026 | 3.4% |

The deceleration is driven by three factors:

- Affordability ceiling: Tenants in many areas simply cannot absorb further increases

- Reduced net migration: Lower inbound migration has eased demand pressure

- Improved supply: Modest increase in available listings (3–11% YoY)

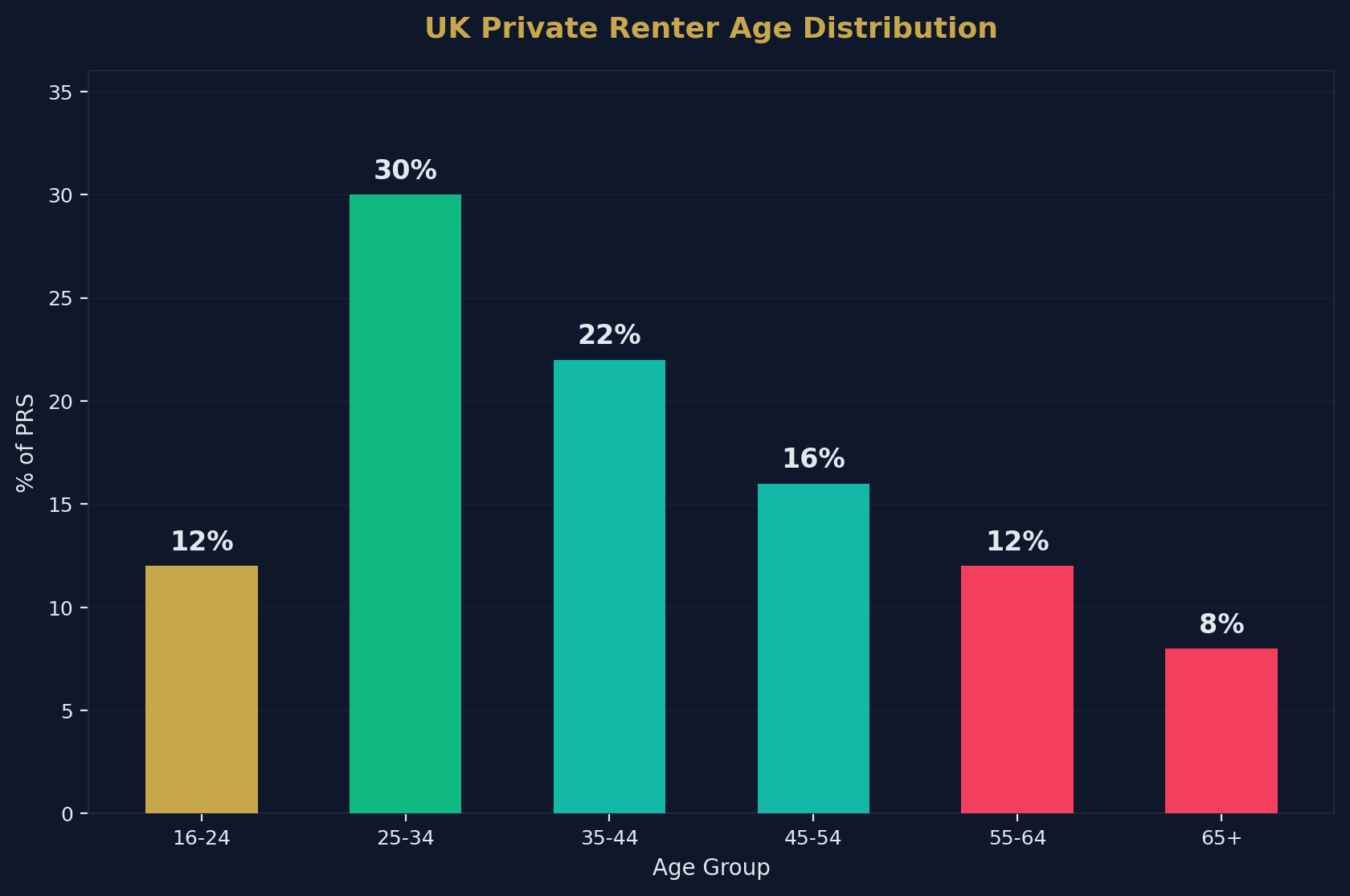

Tenant Demographics

Who Rents in the UK?

| Age Group | Share of PRS | Trend |

|---|---|---|

| 16–24 | ~12% | Declining share |

| 25–34 | ~30% | Largest group (stable) |

| 35–44 | ~22% | Growing |

| 45–54 | ~16% | Growing |

| 55–64 | ~12% | Fastest growth |

| 65+ | ~8% | Fastest growth |

The Ageing of the PRS

The most significant demographic shift is the rapid growth of older renters:

- 1 in 5 private renters is now aged 55+

- The over-55 cohort has grown faster than any other age group over the past decade

- Many older renters are former homeowners who have divorced, downsized, or experienced financial difficulty

- This group is more likely to be long-term renters with tenancies exceeding 5 years

This trend has profound implications for the sector: older renters need more stable, accessible, long-term housing — yet the regulatory framework and <a href="/post/uk-buy-to-let-statistics-2026" style="color:#c9a84c;text-decoration:underline;font-weight:500">landlord behaviour still primarily cater to younger, more transient tenants.

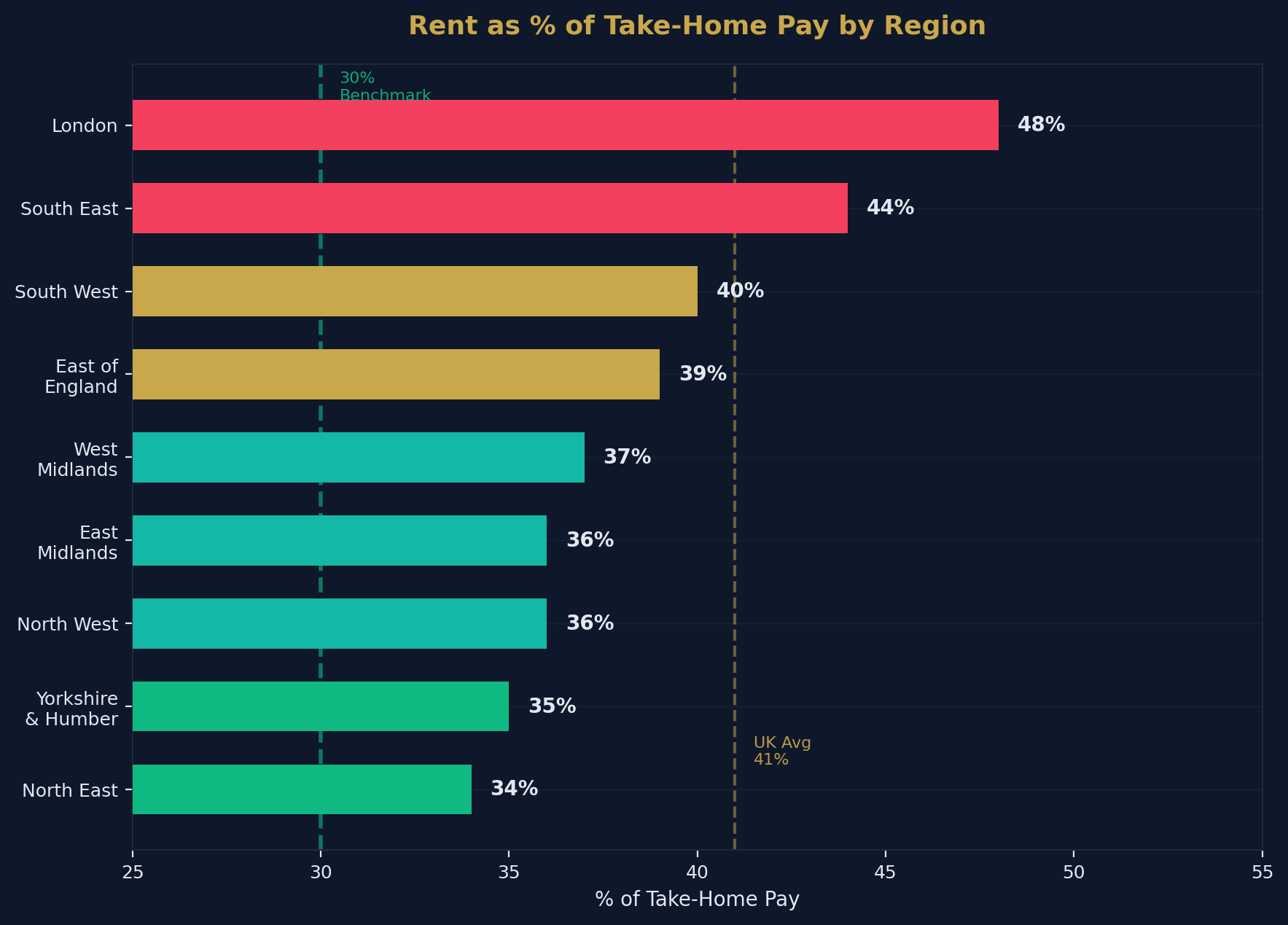

Rental Affordability

Rent-to-Income Ratio by Region

| Region | Rent as % of Take-Home Pay |

|---|---|

| London | 48% |

| South East | 44% |

| South West | 40% |

| East of England | 39% |

| West Midlands | 37% |

| East Midlands | 36% |

| North West | 36% |

| Yorkshire & Humber | 35% |

| North East | 34% |

| UK Average | 41% |

The 30% Threshold

The widely accepted affordability benchmark is that housing costs should not exceed 30% of household income. By this measure:

- Every UK region now exceeds the 30% threshold for average renters

- London exceeds it by 18 percentage points (48%)

- The lowest-income renters spend 50–63% of their income on rent

- This creates a squeeze on food, transport, savings, and mental health

Impact on Saving

For a renter in London earning £35,000 (take-home ~£2,400/month):

- Rent (average room): £1,150/month (48%)

- Bills & council tax: £250/month

- Transport: £200/month

- Food: £300/month

- Remaining for savings: £500/month — making a first-time buyer deposit of £120,000 require 20 years of saving

Supply and Demand Balance

Available Rental Stock

| Metric | 2019 (Pre-COVID) | 2022 (Peak Crisis) | Early 2026 |

|---|---|---|---|

| Available listings (index) | 100 | 55 | 67–77 |

| Enquiries per property | 2.5 | 8–12 | 4.8 |

| Average days to let | 25 | 14 | 20 |

| Listings requiring price cuts | 10% | 3% | 26% |

The Supply Gap

Despite modest improvement, rental supply remains 23–33% below pre-pandemic levels. The causes are structural:

- Landlord exits: An estimated 220,000 households will leave the PRS by end of 2026

- Undersupply of new homes: Only ~220,000 net additions vs 300,000 target

- Regulatory deterrence: New regulations discouraging new entrants

- Stamp duty surcharge: 5% surcharge on BTL purchases raises entry barriers

The professional investors absorbing this exiting stock increasingly rely on property sourcing tools to surface off-market opportunities at scale.

Build-to-Rent (BTR) Sector

BTR Market Overview

| Metric | Figure |

|---|---|

| Total BTR investment (2025) | £5.3 billion |

| Projected BTR investment (2026) | £5.7 billion |

| Average BTR occupancy rate | ~97% |

| BTR pipeline (completed + under construction) | ~100,000+ units |

| BTR share of total PRS | ~2% |

Why BTR Matters

Build-to-Rent is the fastest-growing segment of the PRS. While still representing only ~2% of total stock, it offers:

- Professional management: Higher service standards, dedicated on-site teams

- Long-term security: Designed for long tenancies, pet-friendly policies

- Amenities: Gyms, co-working spaces, communal gardens

- Institutional backing: Pension funds and REITs providing stable, long-term investment

The BTR sector is filling the gap left by departing amateur landlords — but at a premium price point that limits accessibility for lower-income tenants.

The Renters' Rights Act

Key Provisions (Effective 1 May 2026)

| Provision | Impact |

|---|---|

| Section 21 abolition | No more "no-fault" evictions |

| All tenancies become periodic | No fixed-term contracts; tenants can leave with 2 months' notice |

| Pet rights | Tenants can request pets; landlords cannot unreasonably refuse |

| Rent increases | Limited to once per year via market rent assessment |

| Decent Homes Standard | Extended to private rented sector |

| Private rented sector ombudsman | Mandatory landlord registration |

Market Impact Assessment

| Effect | Short-Term | Medium-Term |

|---|---|---|

| Tenant security | Significantly improved | Structural improvement |

| Landlord exits | Accelerated (uncertainty) | Stabilised (adaptation) |

| Rent levels | Potential upward pressure | Market-determined |

| Supply | Minor contraction risk | Recovery as clarity improves |

| Professionalisation | Accelerated | Industry standard |

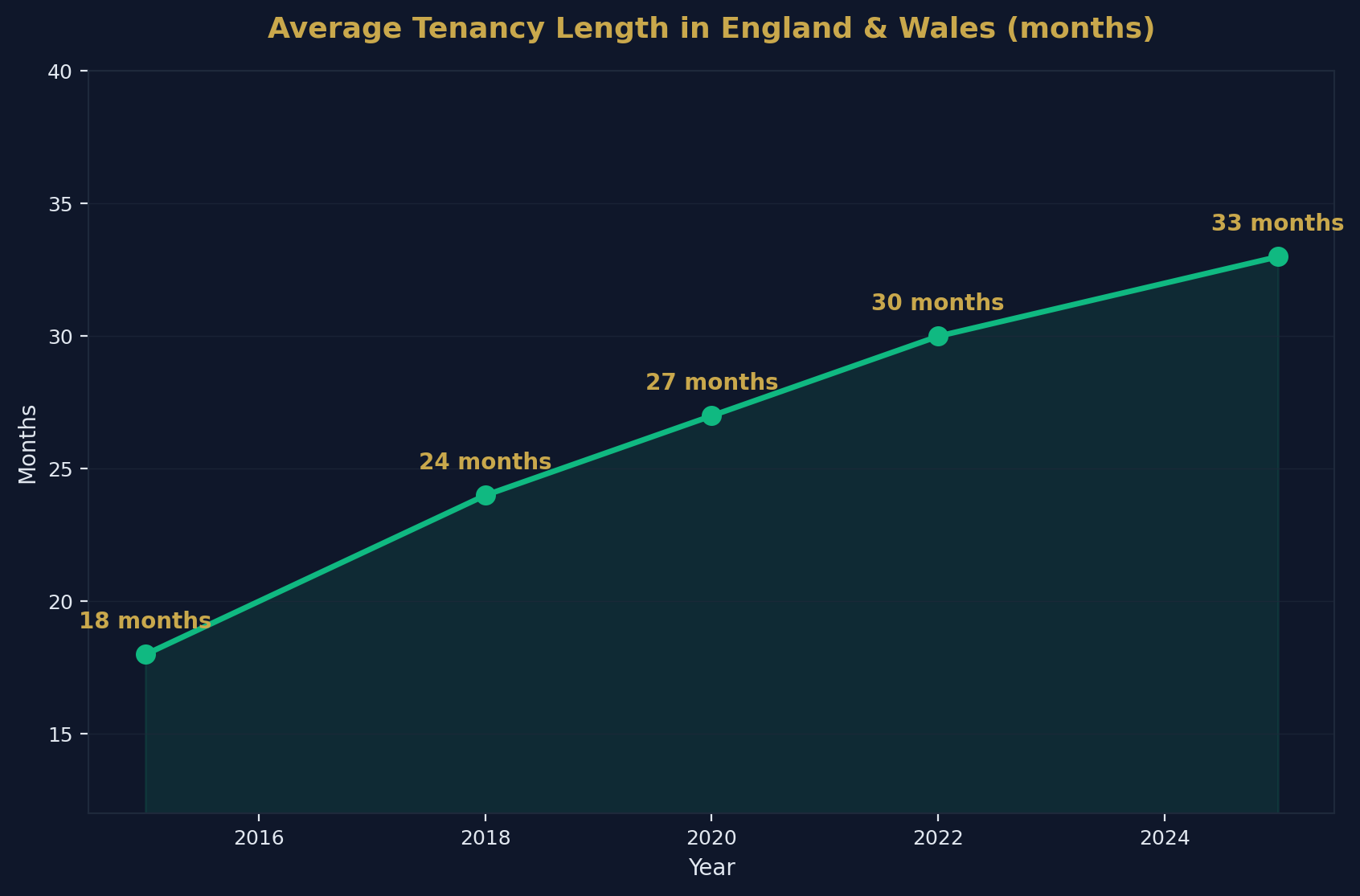

Tenancy Length Trends

Average Tenancy Duration

| Period | Average Tenancy Length |

|---|---|

| 2015 | ~18 months |

| 2018 | ~24 months |

| 2020 | ~27 months |

| 2022 | ~30 months |

| 2025 | ~33 months (1,000+ days) |

Tenancy lengths have increased steadily, driven by:

- Cost of moving: High rents make relocation expensive

- Competition fear: Tenants worry about finding suitable alternatives

- Rising deposits: New deposits require significant upfront cash

- Regulatory changes: The shift to periodic tenancies encourages stability

Methodology and Data Sources

| Source | Data Type | Coverage |

|---|---|---|

| ONS PIPR | Rents, rental inflation | UK nations & regions |

| English Housing Survey | Tenure, demographics, affordability | England |

| Zoopla Rental Market Report | Supply, demand, yields | UK cities & postcodes |

| Rightmove | Listings, time to let | UK |

| Savills | Forecasts, BTR data | UK |

| DLUHC | Housing policy, regulation | England |

How to Cite This Page

UK Rental Market Statistics 2026. Shaded Canvas. Published April 2026, updated quarterly. Available at: https://blog.shadedcanvas.co.uk/post/uk-rental-market-statistics-2026

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →