The UK buy-to-let sector is in the middle of its most significant structural transformation since Section 24 was announced in 2015. This page consolidates every critical BTL statistic for 2026 — from mortgage lending volumes and landlord demographics to limited company trends, portfolio sizes, regulatory compliance costs, and the real numbers behind the "landlord exodus" narrative.

Whether you are a landlord benchmarking your portfolio, a mortgage broker advising investors, or a researcher analysing the private rented sector, this is the definitive reference.

Last Updated: April 2026 | Next Update: July 2026

Key Buy-to-Let Statistics at a Glance

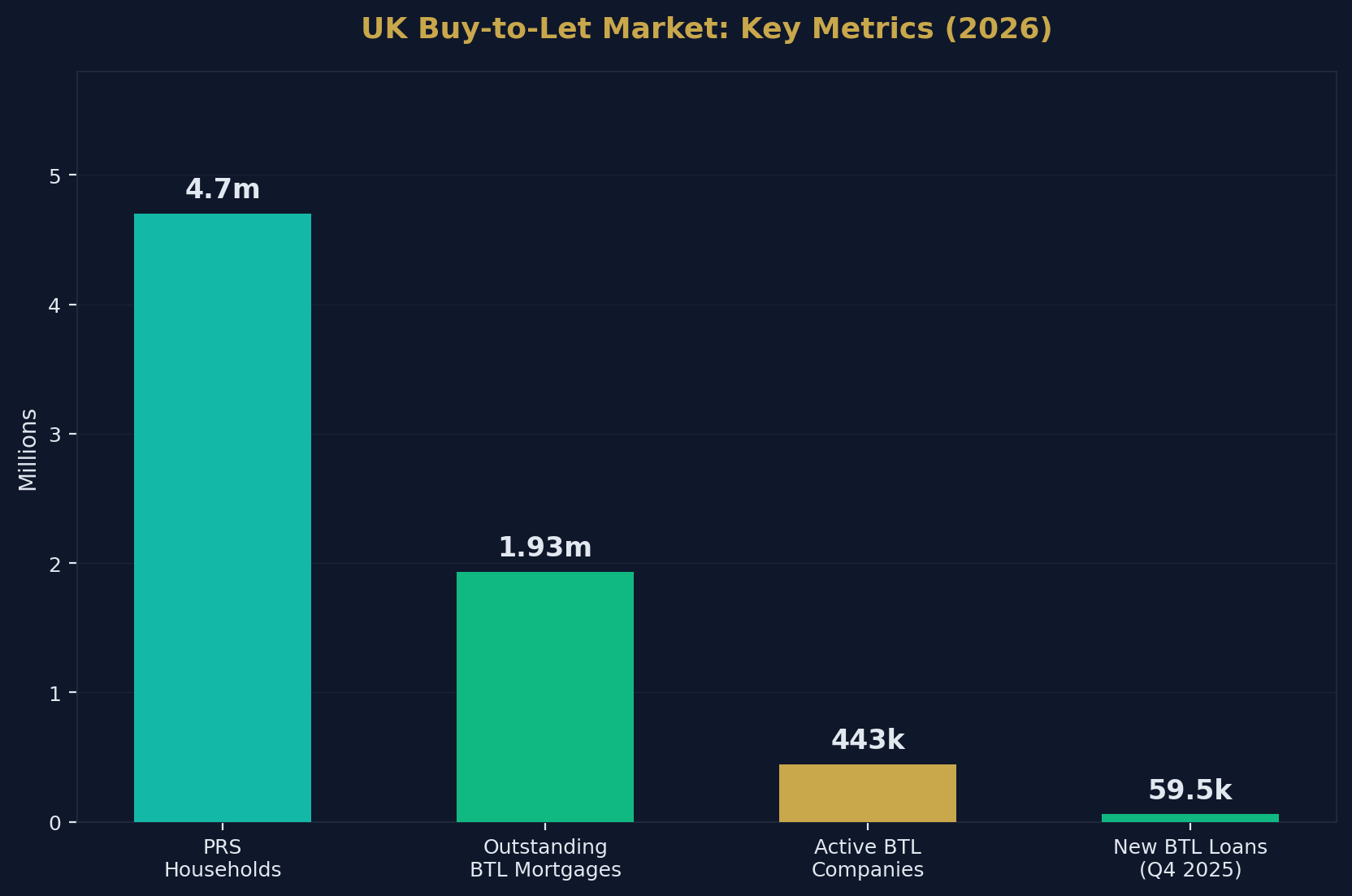

- There are approximately 4.7 million privately rented households in the UK (~19% of all households).

- The average UK monthly private rent is £1,374 (ONS, February 2026).

- Annual rent inflation has cooled to 3.4% — the lowest rate since March 2022.

- There are 1.46 million fixed-rate BTL mortgages outstanding (+2% YoY).

- There are 466,000 variable-rate BTL mortgages outstanding (-9.8% YoY).

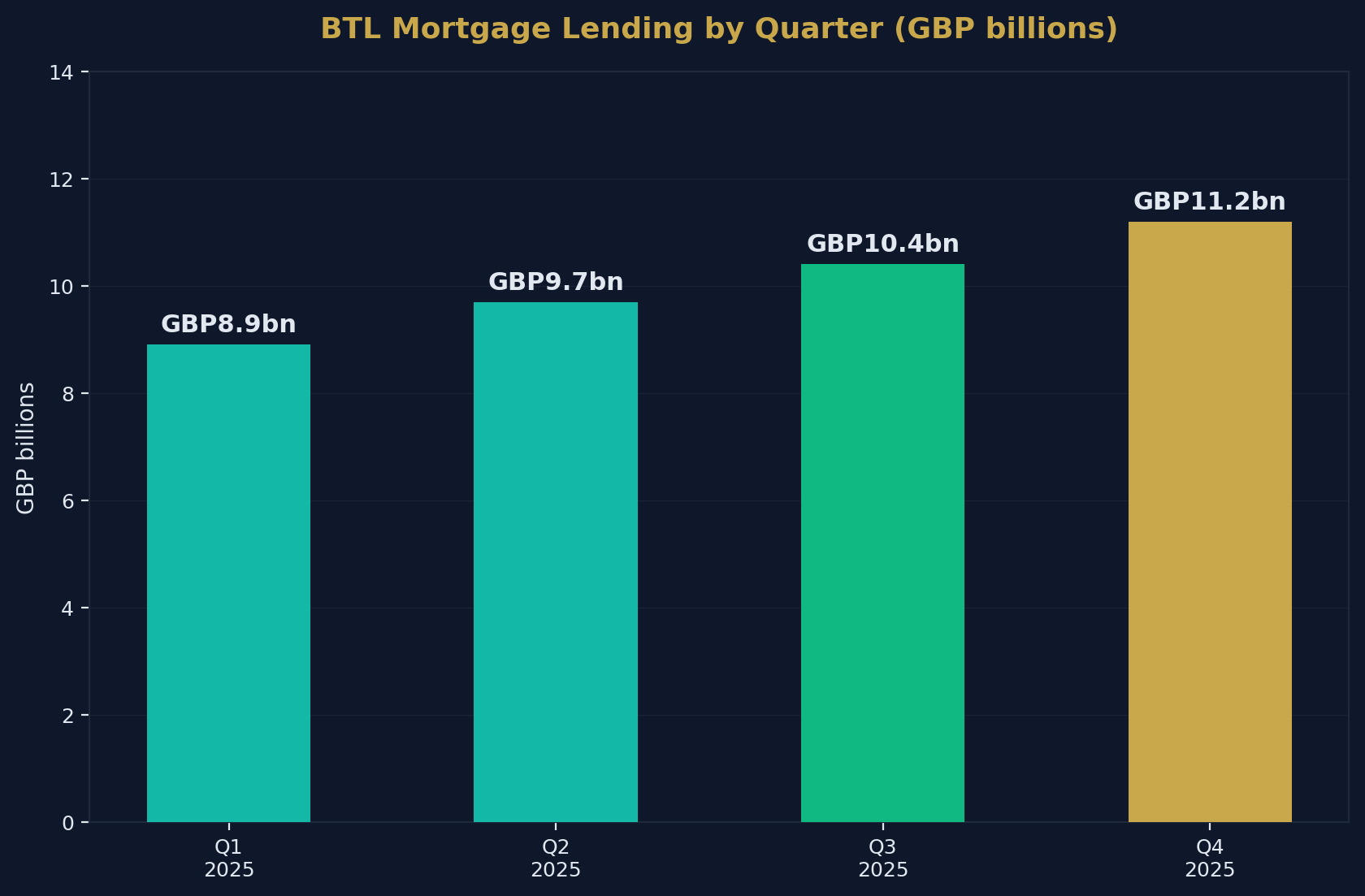

- In Q4 2025, 59,489 new BTL loans were advanced totalling £11.2 billion (+21.3% by value).

- The average BTL 2-year fixed rate (75% LTV) is approximately 3.73% (March 2026).

- The average interest cover ratio (ICR) for UK BTL is 218% — up from 201% a year earlier.

- BTL arrears (>2.5%) affected only 9,520 mortgages at end of 2025.

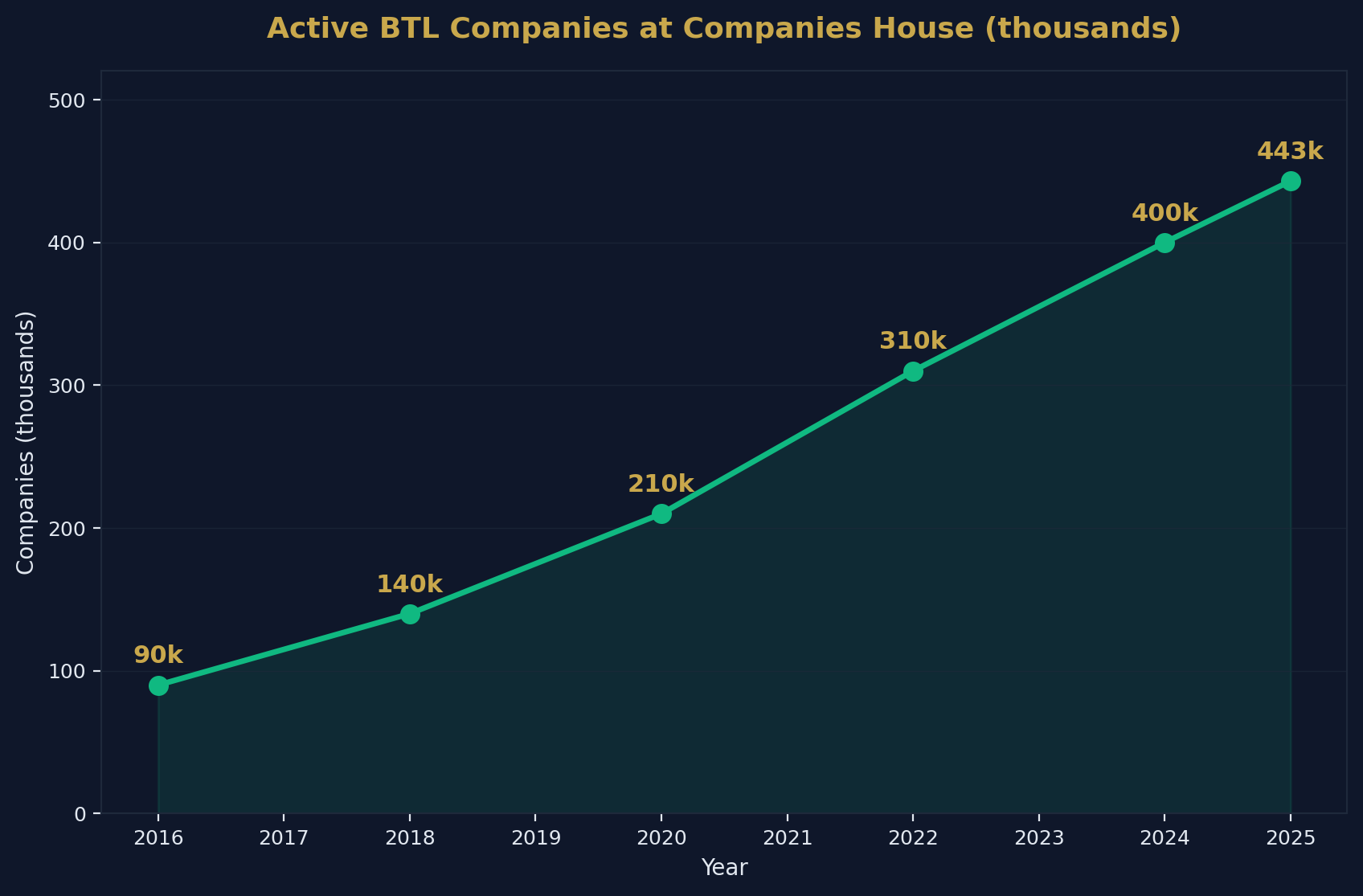

- There are 443,272 active BTL limited companies — nearly 5x the 2016 figure.

- 75–80% of all new BTL purchases are now made via limited companies.

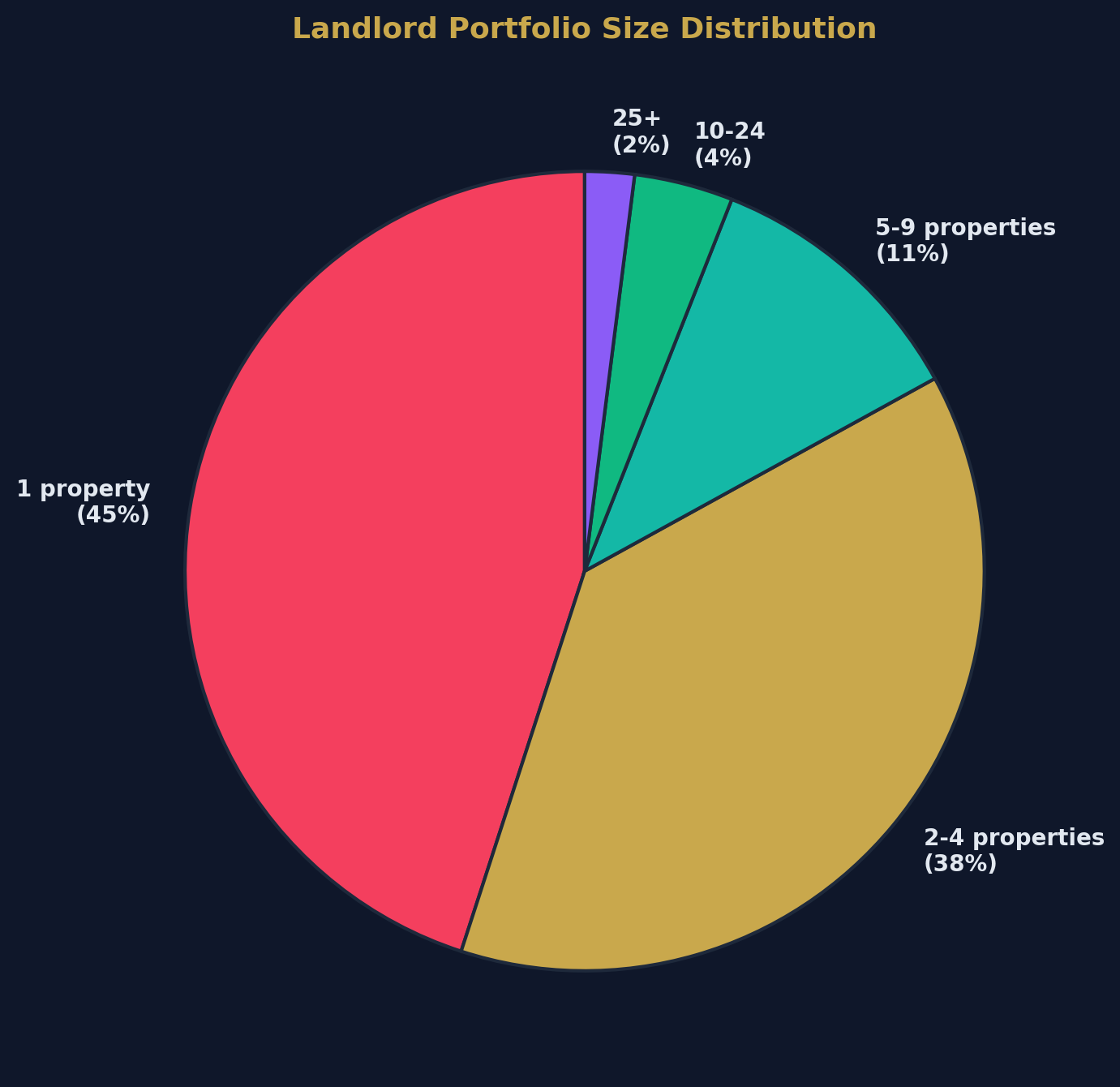

- 45% of landlords own a single rental property; 38% own 2–4 properties.

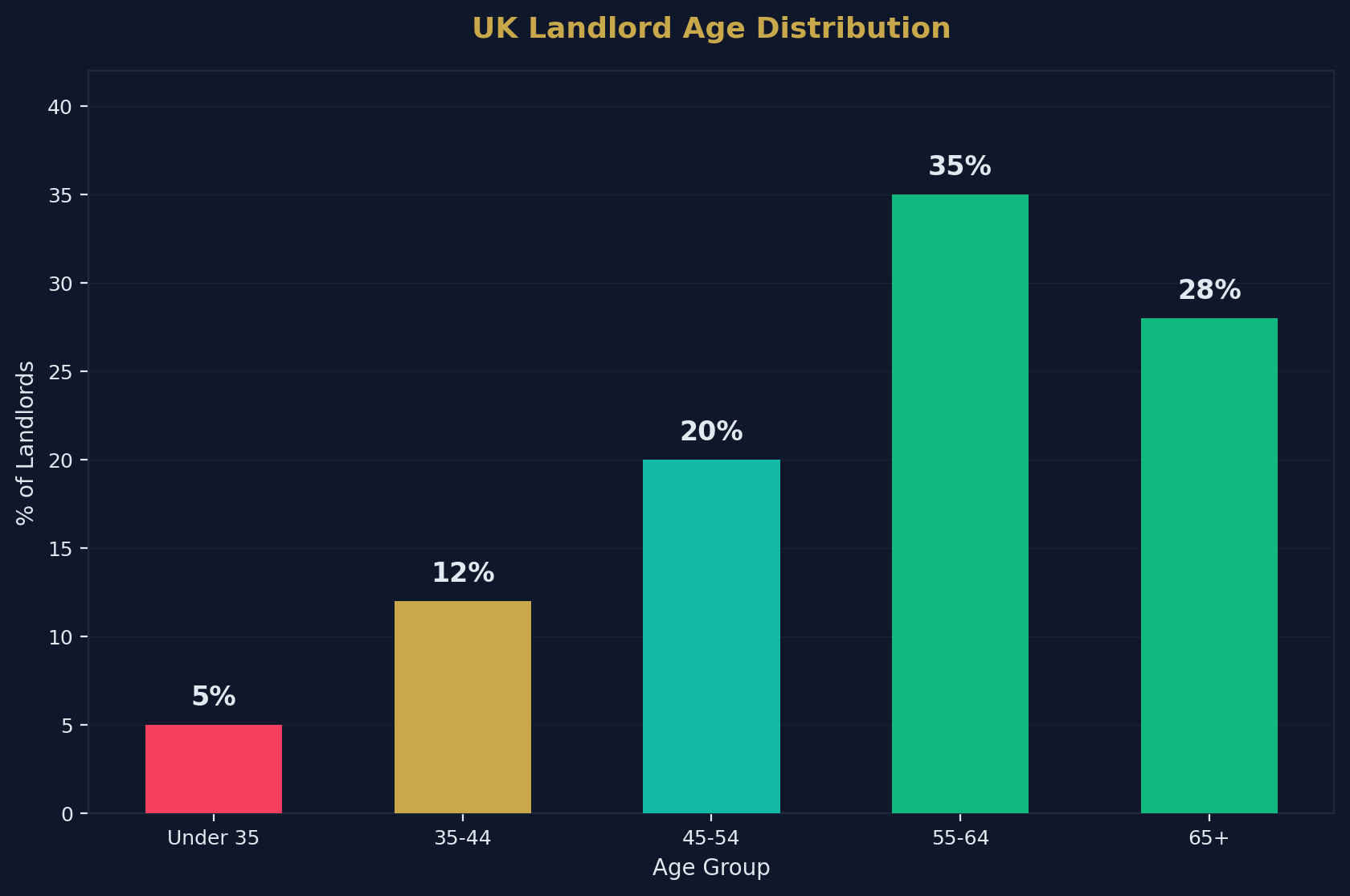

- The median landlord age is 59 years old; two-thirds are aged 55+.

- 55% of landlords are male, 44% female.

- Two-thirds of landlords plan growth activity (acquisitions, refurbs, or refinancing) in 2026.

- 39% of landlords plan to refinance in 2026 due to maturing fixed-rate deals.

- Making Tax Digital applies from April 2026 for landlords with >£50,000 gross rental income.

Source: Shaded Canvas analysis of UK Finance, ONS, HMRC, Hamptons, Companies House, and English Landlord Survey data. Last updated April 2026.

BTL Mortgage Market

Lending Volumes

| Period | New BTL Loans | Value | YoY Change (Value) |

|---|---|---|---|

| Q1 2025 | 48,200 | £8.9bn | +15% |

| Q2 2025 | 52,300 | £9.7bn | +18% |

| Q3 2025 | 55,800 | £10.4bn | +21% |

| Q4 2025 | 59,489 | £11.2bn | +21.3% |

Outstanding BTL Mortgages

| Type | Count | YoY Change |

|---|---|---|

| Fixed-rate | 1,460,000 | +2.0% |

| Variable-rate | 466,000 | -9.8% |

| Total | ~1,926,000 | — |

BTL Mortgage Rates (April 2026)

| Product | Typical Rate |

|---|---|

| 2-year fixed (75% LTV, personal) | 3.73% |

| 5-year fixed (75% LTV, personal) | 4.0–4.5% |

| 5-year fixed (portfolio landlord) | 4.5–5.5% |

| Variable/tracker | 4.0–5.0% |

| Bridging finance | 0.55–0.95%/month |

Portfolio Health

| Metric | Figure |

|---|---|

| Average ICR | 218% |

| ICR 12 months ago | 201% |

| Arrears (>2.5%) | 9,520 mortgages |

| Arrears rate | ~0.5% |

The improving ICR (218% vs 201%) indicates that landlord cash flow is strengthening as rents rise and some mortgage rates stabilise. The extremely low arrears rate (0.5%) contradicts the narrative of widespread landlord distress.

Landlord Demographics

Who Are UK Landlords?

| Demographic | Data |

|---|---|

| Median age | 59 years |

| Aged 55+ | ~65–75% |

| Aged under 40 | <10% |

| Male | 55% |

| Female | 44% |

| Retired | >33% |

| Full-time landlord | ~15% |

The Ageing Landlord Problem

The concentration of landlords in older age groups creates a medium-term succession risk for the sector:

- As landlords retire and sell, significant stock enters the market simultaneously

- Younger investors face higher barriers to entry (higher stamp duty, stricter lending, larger deposits)

- The gap is being filled by corporate and institutional investors rather than individual newcomers

Portfolio Size Distribution

How Many Properties Do Landlords Own?

| Portfolio Size | % of Landlords | Estimated Landlords |

|---|---|---|

| 1 property | 45% | ~990,000 |

| 2–4 properties | 38% | ~836,000 |

| 5–9 properties | 11% | ~242,000 |

| 10–24 properties | 4% | ~88,000 |

| 25+ properties | 2% | ~44,000 |

| Total | 100% | ~2,200,000 |

The Consolidation Trend

While single-property landlords dominate by number, the market is consolidating:

- Smaller landlords (1–4 properties) are more likely to exit

- Portfolio landlords (5+) are expanding, absorbing exiting stock

- Limited company structures make scaling portfolios more tax-efficient

- Professional property management enables larger portfolios

A growing share of these expanding portfolio landlords now buy through property sourcing companies rather than sourcing stock themselves.

The Limited Company Revolution

BTL Company Registrations

| Year | Active BTL Companies | New Companies (Annual) |

|---|---|---|

| 2016 | ~90,000 | — |

| 2018 | ~140,000 | ~25,000 |

| 2020 | ~210,000 | ~35,000 |

| 2022 | ~310,000 | ~50,000 |

| 2024 | ~400,000 | ~45,000 |

| 2025 | 443,272 | ~43,000 |

| Jan 2026 | — | 5,922 (monthly, +11% YoY) |

Why Limited Companies Dominate New Purchases

| Factor | Personal Landlord | Limited Company |

|---|---|---|

| Mortgage interest deduction | 20% basic rate tax credit only | Full deduction as business expense |

| Tax rate on profits | 20–45% income tax | 25% corporation tax |

| Retained earnings | Taxed as income when drawn | Can accumulate tax-free in company |

| Capital growth tax | 18–24% CGT | 25% corp tax + extraction tax |

| Inheritance planning | Direct estate liability | Shares can be transferred |

For higher-rate taxpayers, the limited company structure can improve after-tax returns by 15–30% compared to personal ownership — making it the rational default for any new acquisition.

The "Landlord Exodus" — Fact vs Fiction

What the Data Actually Shows

The media narrative of a "landlord exodus" is partially true but significantly oversimplified:

| Claim | Reality |

|---|---|

| "Landlords are leaving in droves" | PRS is contracting — but slowly (220,000 households over 2+ years, ~4.5% of total) |

| "BTL is dead" | BTL lending is UP 21% YoY; 59,489 new loans in Q4 2025 alone |

| "No one is buying BTL anymore" | 75–80% of new purchases via Ltd companies — structure changed, not demand |

| "Yields make it unviable" | Average ICR at 218%; most portfolios are profitable |

| "All landlords are selling" | Two-thirds plan growth activity in 2026 |

Who Is Actually Leaving

- Single-property accidental landlords who inherited or kept a property after moving

- Higher-rate personal taxpayers who refuse to restructure into limited companies

- Older landlords reaching retirement without succession plans

- Landlords with low-EPC properties who cannot justify upgrade costs

Who Is Entering/Expanding

- Limited company operators making tax-efficient acquisitions

- Portfolio landlords (5+ properties) absorbing exiting stock at discount

- Institutional investors via Build-to-Rent developments

- Professional deal packagers sourcing discounted stock for investor clients

Regulatory Timeline

Key Regulations Affecting BTL (2026–2030)

| Date | Regulation | Impact |

|---|---|---|

| April 2026 | Making Tax Digital (>£50k income) | Quarterly digital reporting required |

| April 2027 | MTD extended (>£30k income) | More landlords brought into scope |

| 2028 (est.) | Renters' Rights Act full implementation | End of Section 21; new compliance requirements |

| 2030 (est.) | EPC C minimum for all lettings | £5,000–£15,000 per property upgrade |

| Ongoing | Selective licensing expansion | £500–£800 per property per council |

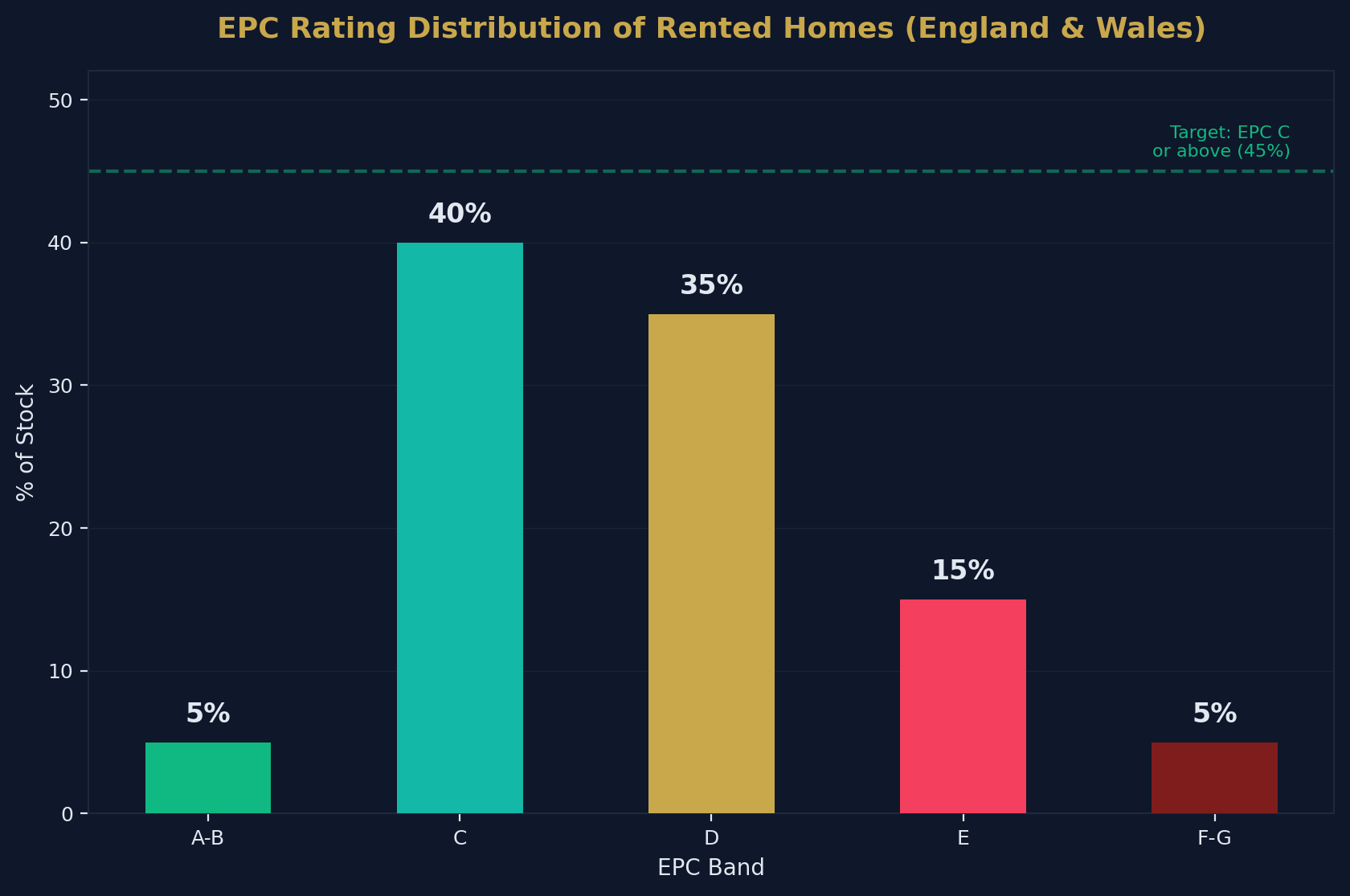

EPC Compliance

| EPC Band | % of Rented Stock | Status |

|---|---|---|

| A–B | ~5% | Exceeds requirements |

| C | ~40% | Meets expected 2030 standard |

| D | ~35% | Upgrade needed by 2030 |

| E | ~15% | Current minimum — upgrade needed |

| F–G | ~5% | Non-compliant (unless exempt) |

Approximately 55% of rented homes currently hold an EPC rating of D or below — representing a massive upgrade requirement if the EPC C target proceeds as planned.

Investment Returns: The Real Numbers

Average BTL Returns by Strategy

| Strategy | Gross Yield | Typical Net Yield | Capital Growth | Total Return |

|---|---|---|---|---|

| Single-let (North) | 6–8% | 3–4% | 2–4% | 5–8% |

| Single-let (South) | 3.5–5% | 1–2% | 3–5% | 4–7% |

| HMO (optimised) | 10–15% | 6–9% | 2–4% | 8–13% |

| Serviced accommodation | 8–15% | 4–8% | 2–4% | 6–12% |

| New-build flat | 4–6% | 1–3% | 3–5% | 4–8% |

10-Year BTL Investment Case

For a £200,000 property purchased via limited company with 75% LTV mortgage at 4.5%:

| Metric | Year 1 | Year 5 | Year 10 |

|---|---|---|---|

| Property value | £200,000 | £240,000 | £310,000 |

| Equity | £50,000 | £110,000 | £190,000 |

| Annual rent | £12,000 | £13,400 | £15,600 |

| Mortgage balance | £150,000 | £138,000 | £118,000 |

| Total return on cash invested | — | 120% | 280% |

Assumptions: 4% annual price growth, 2.5% annual rent growth, interest-only mortgage

Methodology and Data Sources

| Source | Data Type | Coverage |

|---|---|---|

| UK Finance | BTL lending, arrears, ICR | UK |

| ONS | Rents, private rental market | UK |

| Hamptons | Ltd company data, landlord trends | England & Wales |

| Companies House | BTL company registrations | UK |

| English Landlord Survey | Demographics, portfolio size | England |

| HMRC | Tax receipts, MTD | UK |

| Savills | Forecasts | UK |

How to Cite This Page

UK Buy-to-Let Statistics 2026. Shaded Canvas. Published April 2026, updated quarterly. Available at: https://blog.shadedcanvas.co.uk/post/uk-buy-to-let-statistics-2026

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →