When considering buying property for investment in the UK, many investors are drawn by the dual prospects of monthly rental income and long-term capital appreciation. However, the landscape of UK property investment is shifting. With fluctuating interest rates, stringent tax regulations, and evolving tenant rights, succeeding requires a data-driven, realistic approach.

This comprehensive guide breaks down exactly how to invest in property in the UK in the current climate. We will explore regional yields, financial models, tax implications, and the practical realities of being a landlord, leaving behind the "get rich quick" fluff.

Executive Summary

Investing in property in the UK remains a cornerstone of wealth generation, but the strategies that worked a decade ago are no longer guaranteed to yield high returns. The Office for Budget Responsibility (OBR) forecasts an average house price increase from £269,000 in early 2026 to £315,000 by 2030, suggesting modest, steady capital growth over explosive short-term gains.

In 2026, successful property investment hinges on location selection and structural optimisation. While traditional single-let properties provide steady income, strategies like Houses in Multiple Occupation (HMOs) can deliver yields exceeding 9% in targeted Northern cities like Glasgow and Belfast. Conversely, investors must navigate significant headwinds, including a 5% Stamp Duty surcharge on additional properties and increased scrutiny surrounding tenant evictions and property standards.

If you find yourself asking, "how do I invest in property sustainably?", the key is rigorous financial planning. This guide provides the complete framework for properties to invest in, mitigating risks, and structuring your portfolio for maximum net yield.

What is Investing in Property?

At its core, what is investing in property? It is the strategic purchase of real estate with the primary goal of generating a return on investment (ROI). This return manifests in two primary ways:

- Rental Yield: The monthly or annual income generated by tenants paying rent, expressed as a percentage of the property's value.

- Capital Appreciation: The increase in the property's market value over time, realized upon refinancing or selling the asset.

Unlike passive investments such as index funds, physical real estate is highly illiquid and requires active management. High agent fees, maintenance liabilities, and legal responsibilities (such as gas safety certificates and Electrical Installation Condition Reports) mean that net yields are often substantially lower than gross figures.

Core Property Investment Strategies

When asking how to invest property effectively, you must first determine the strategy that aligns with your capital availability, risk tolerance, and time commitment.

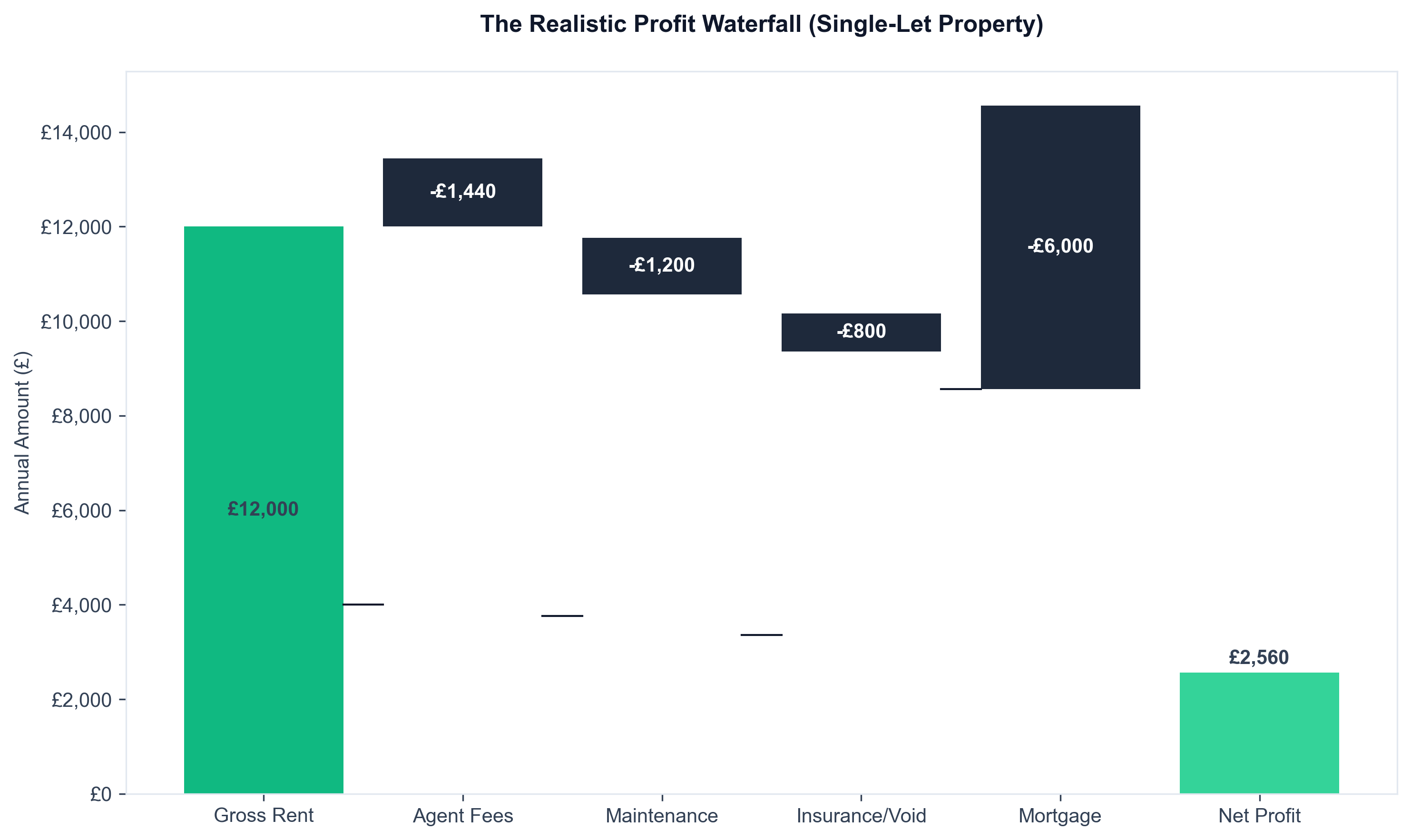

1. Single-Let Residential Buy-to-Let

The most traditional path to buying property for investment is the single-let strategy. You purchase a standard residential home or apartment and let it to a single family or professional couple.

- Pros: Generally lower maintenance, longer tenancy durations, easier to finance with standard Buy-to-Let (BTL) mortgages.

- Cons: Lower gross yields (typically 4-6%), higher risk of vacancy severely impacting cash flow (if the property is empty, income is zero).

2. Houses in Multiple Occupation (HMOs)

HMOs involve renting a property out on a per-room basis to multiple unrelated tenants who share communal facilities like kitchens and bathrooms.

- Pros: Significantly higher gross yields, often reaching 8-10% or more. Void periods have less impact since one vacant room does not stop the income from the others.

- Cons: Higher initial setup costs due to fire safety regulations (fire doors, complex alarm systems). Higher turnover of tenants, increased wear and tear, and more stringent licensing requirements from local councils.

3. Buy-Refurbish-Refinance (BRR)

The BRR strategy is a powerful method for those wondering how do you invest in property to rapidly build a portfolio. You purchase a dilapidated property below market value, force appreciation through structural or cosmetic refurbishment, and then refinance the property at its new, higher valuation to extract the initial capital.

- Pros: Allows the recycling of cash to buy multiple assets.

- Cons: Highly exposed to valuation risks. If the surveyor down-values the property post-refurbishment, your capital remains trapped. Refurbishment projects frequently exceed budget and timeline estimates.

4. Holiday Lets and Short-Term Rentals

Holiday lets involve renting out property for short durations, capitalising on tourism or corporate travel using platforms like Airbnb.

- Pros: Can generate substantially higher revenue during peak seasons. Enjoys favourable tax treatment under Furnished Holiday Let (FHL) rules (though these rules are subject to changing legislative scrutiny).

- Cons: Highly seasonal income, intensive management required for cleaning and guest communication, and increasing regulatory pushback from local authorities restricting short-term rentals.

| Strategy | Average Expected Gross Yield | Capital Required | Management Intensity | Risk Profile |

|---|---|---|---|---|

| Single-Let | 4% - 6% | Moderate (£40k - £80k) | Low to Medium | Low |

| HMO | 7% - 10%+ | High (£60k - £120k) | High | Medium to High |

| BRR | 6% - 8% (Post-Refurb) | High (£80k+) | Very High | High |

| Holiday Let | 8% - 12% | High (£60k+) | Very High | Medium |

Regional and Market Analysis

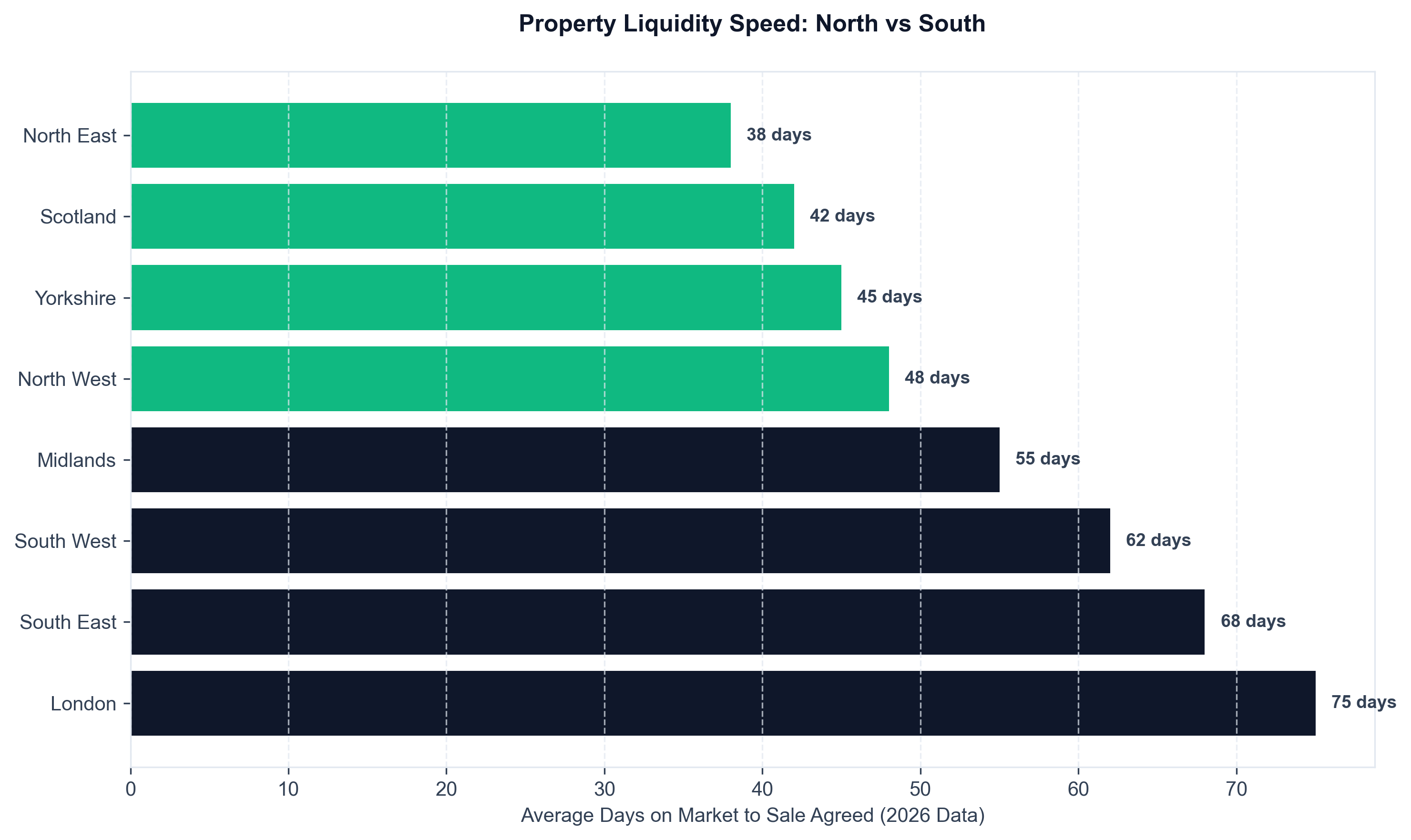

When executing a property investment how to strategy, location is the single largest determinant of success. The UK property market is highly regionalised, with a stark division in performance between London/the South East and Northern/Scottish cities.

High Yield Markets: The North and Scotland

Current data highlights that Northern cities dominate the high-yield landscape. According to late 2025 and early 2026 reports, Glasgow and Belfast frequently share the top spot for investable cities, delivering average gross yields of around 9.3%.

Other powerful performers include the broader North West region, specifically Manchester and Liverpool, which consistently show strong tenant demand driven by retaining university graduates and expanding corporate hubs. The Yorkshire and Humber region also posts robust HMO rental yields averaging over 8.6%.

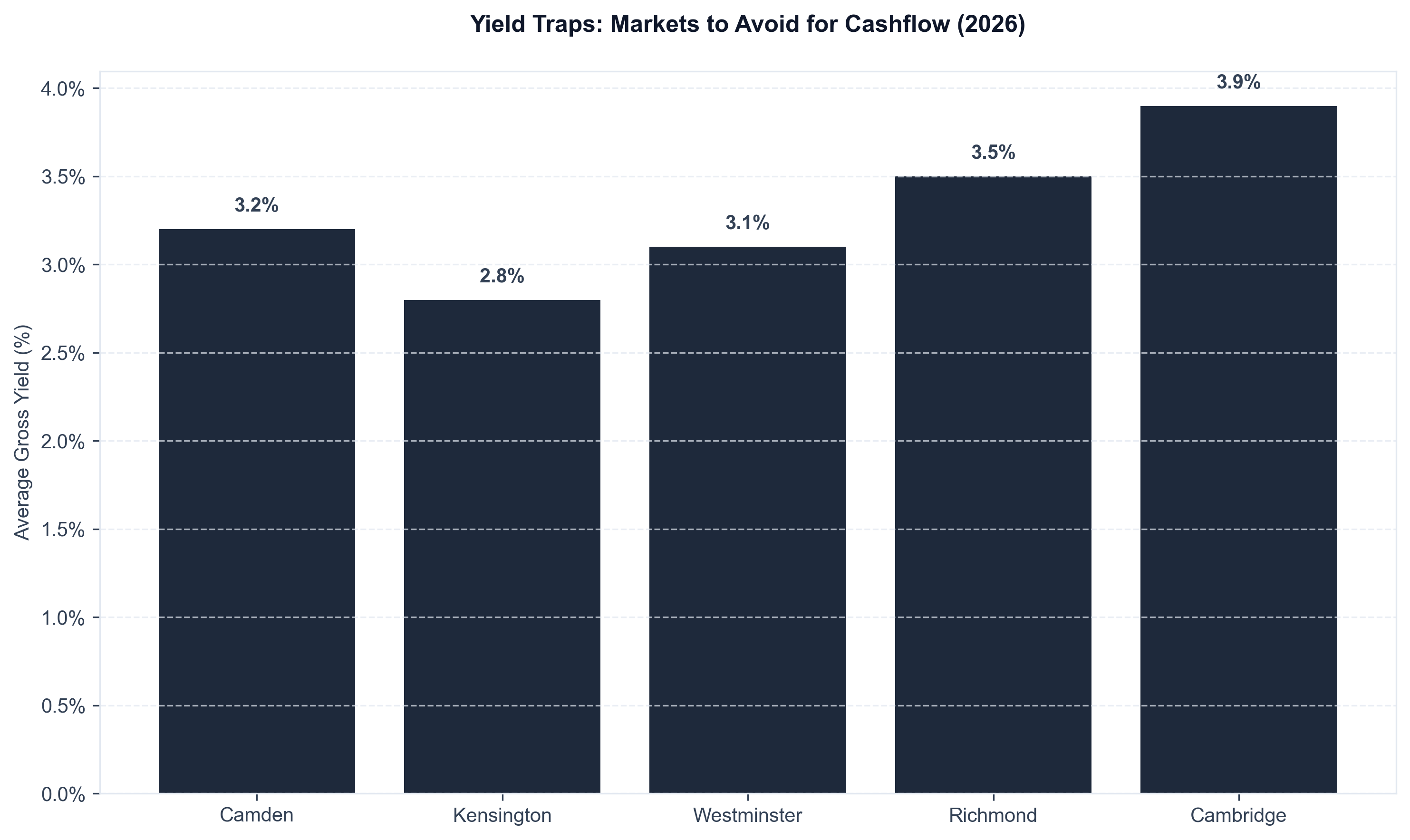

Capital Growth vs Yield: The London Dilemma

London remains a global financial hub, but for regular investors, gross yields in the capital are notoriously compressed, often hovering around the 4% to 5% mark (and sometimes lower in prime central areas).

While historic capital growth in London has been unparalleled, the high entry price points (often requiring £100,000+ just for a deposit and stamp duty) and punishing tax implications make it a difficult market for new investors seeking cash flow.

Financial Deep-Dive: Costs and Financing

Understanding how to do property investment requires a forensic examination of the numbers. Many amateur investors calculate yields using simply rent against purchase price, ignoring the multitude of operational and frictional costs.

Securing Buy-to-Let Finance

Most investors leverage their capital using interest-only Buy-to-Let (BTL) mortgages. This maximises return on capital employed (ROCE) and improves monthly cash flow compared to capital repayment loans.

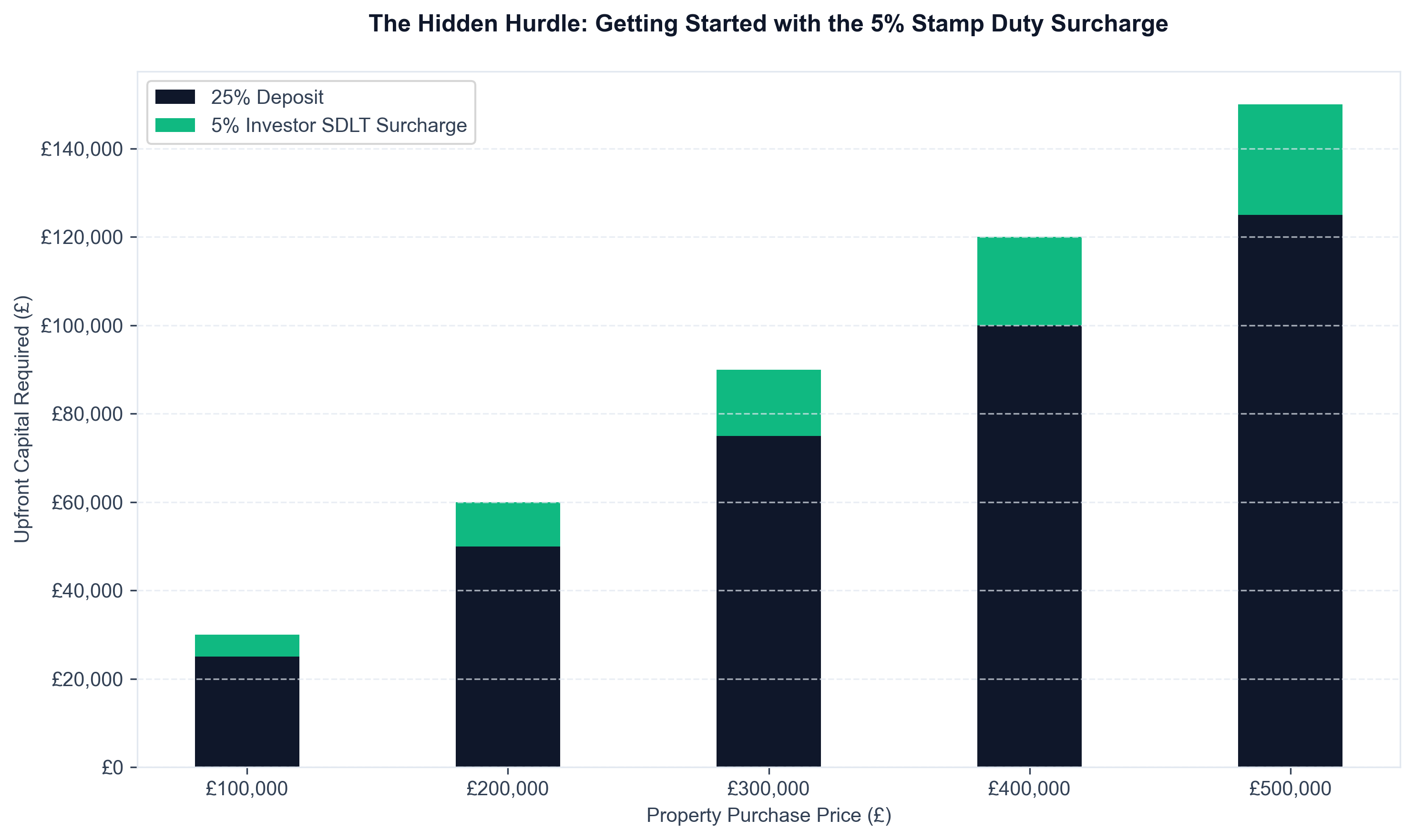

- Deposits: A minimum deposit of 25% is standard, though accessing the best interest rates often requires 30% or 40% equity.

- Affordability: Lenders use Interest Coverage Ratios (ICR) to assess viability. The anticipated rental income must usually cover 125% to 145% of the mortgage interest payments, stress-tested at a higher interest rate (often 5.5% or more).

- Personal Income: Many tier-one lenders require the applicant to have a minimum external earned income of £25,000 per annum.

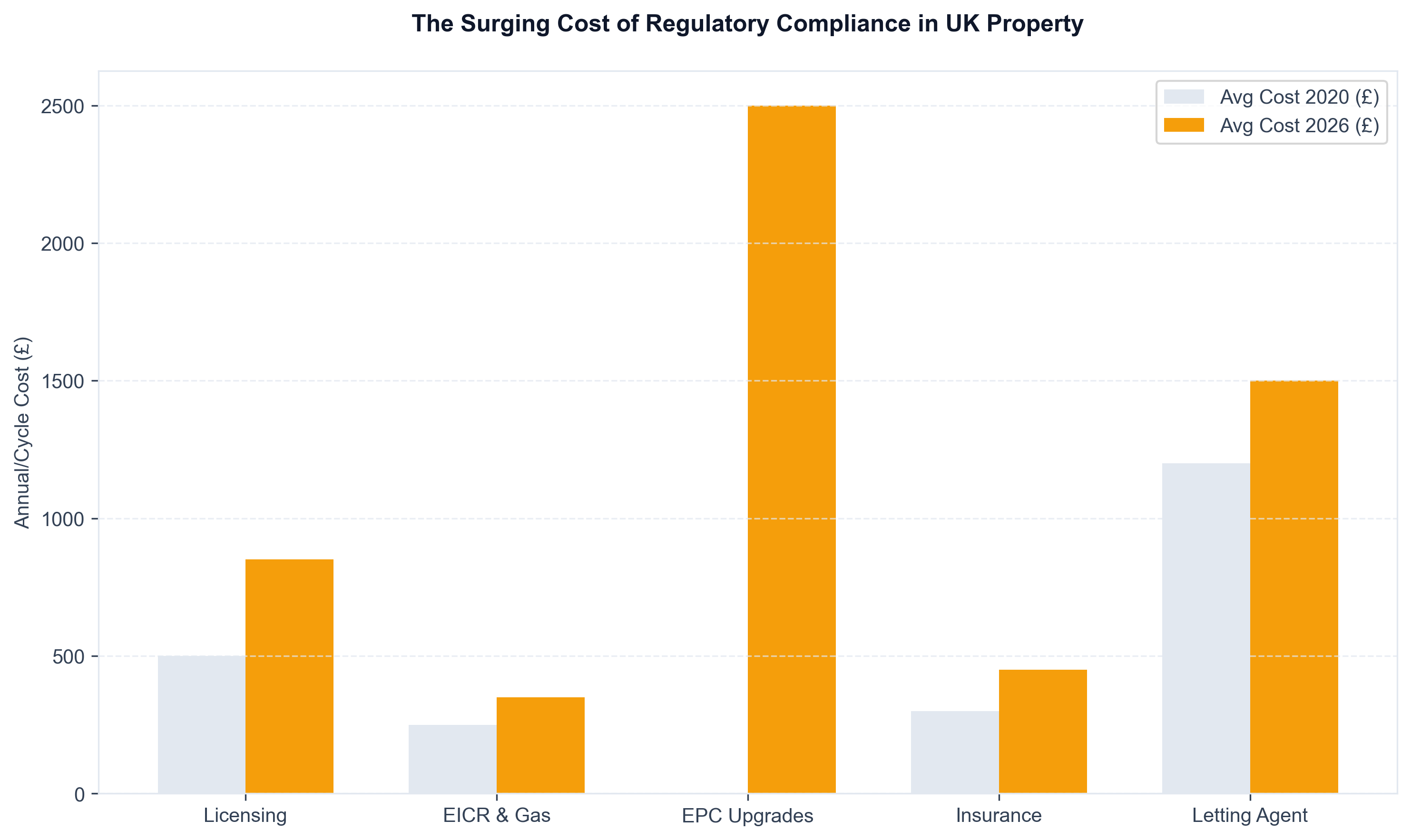

Frictional Costs of Acquisition

When buying property for investment in the UK, the upfront costs are significant:

- Stamp Duty Land Tax (SDLT): Investors purchasing an additional dwelling face a punitive 5% surcharge on top of standard residential SDLT rates. Furthermore, non-UK residents are hit with an additional 2% surcharge, effectively killing profit margins for unprepared foreign buyers.

- Conveyancing and Surveys: Expect to pay between £1,500 and £3,000 for legal fees, local searches, and a comprehensive RICS structural survey.

- Broker and Lender Fees: Mortgage arrangement fees often range from 1% to 2% of the loan amount, which can sometimes be added to the mortgage balance.

Ongoing Operational Expenses

Net yield is the only figure that truly matters. When calculating ROI, you must deduct:

- Letting Agent Fees: Typically 10% to 15% plus VAT for a fully managed service.

- Maintenance Provision: A prudent investor allocates 10% of gross rent towards ongoing repairs and eventual capital expenditures (boilers, roofs).

- Insurance and Compliance: Landlord building insurance, annual gas safety checks, EICRs (every 5 years), and potential selective licensing fees from the local council.

- Void Periods: You must model your calculations assuming the property will be empty for 2-4 weeks per year.

Risk Assessment and Landlord Realities

The reality of investing in property in UK markets involves navigating significant risk. Anecdotes from social platforms like Reddit frequently highlight the harsh truths of property management.

Tenant Challenges and the Changing Legal Landscape

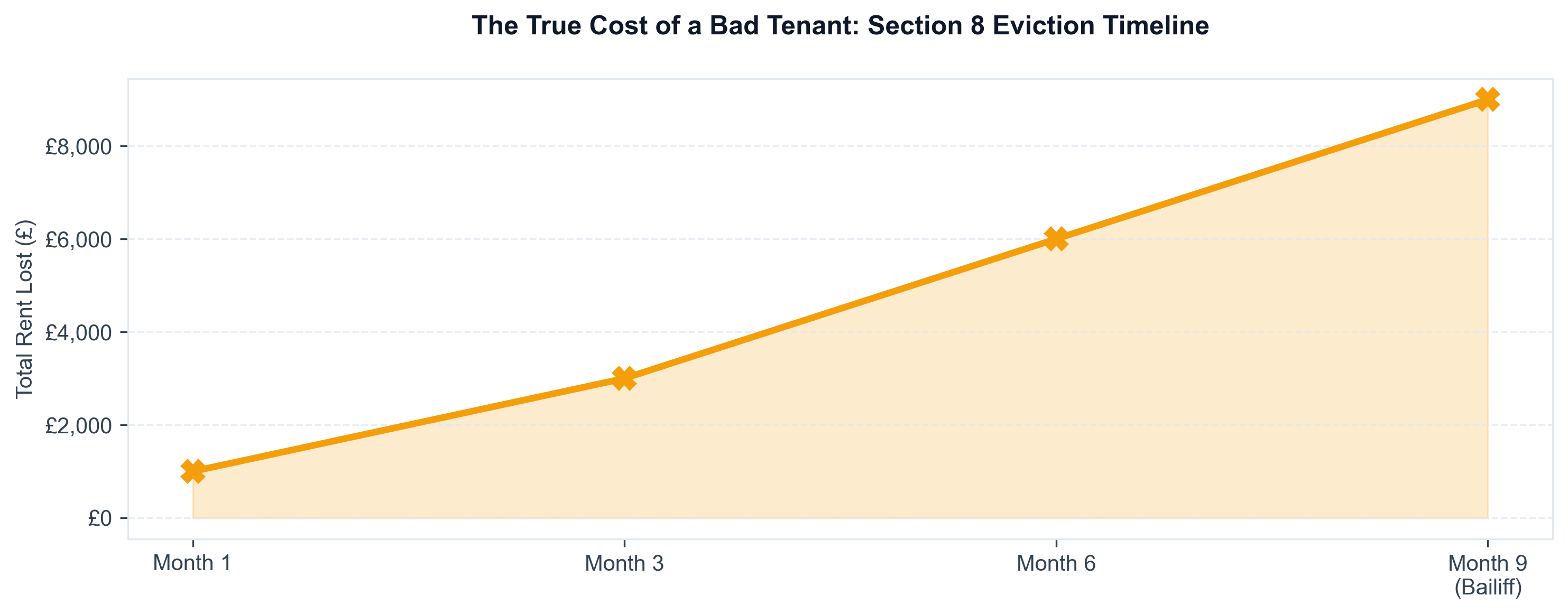

A major risk factor is tenant delinquency. Cautionary tales of non-payment of rent, severe property damage, and the arduous, months-long process of legal eviction highlight the absolute necessity of rigorous tenant referencing. Relying on specialized, competent letting agents is not just a convenience; it is a risk mitigation strategy.

Furthermore, the legal landscape is shifting aggressively in favour of tenants. Proposed legislative changes continually threaten to abolish Section 21 "no-fault" evictions, meaning landlords will need robust legal grounds to regain possession of their assets. Investors must be prepared for increased compliance burdens and the associated costs.

Market and Economic Risks

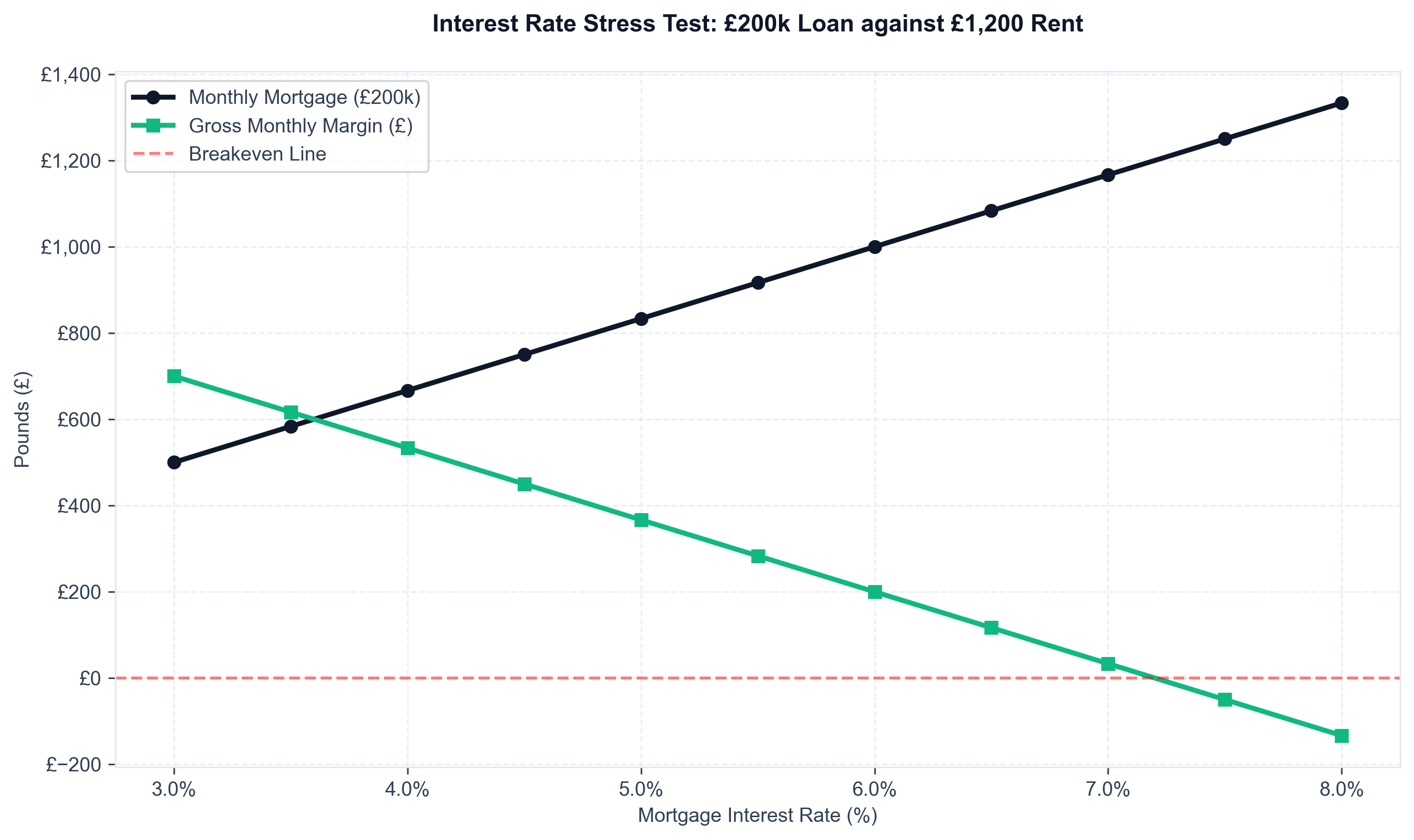

Property values can fall as well as rise. While the OBR forecasts steady growth through 2029, localized oversupply or broader economic shocks can depress both capital values and rental demand. High interest rates aggressively compress cash flow margins. If you fix your mortgage at 4% and rates rise to 6% when your term expires, a profitable investment can become a monthly liability.

Tax Implications and Structuring

Tax efficiency is crucial when determining properties to invest in. The UK tax regime for landlords has become increasingly hostile for higher-rate taxpayers holding property in their personal names.

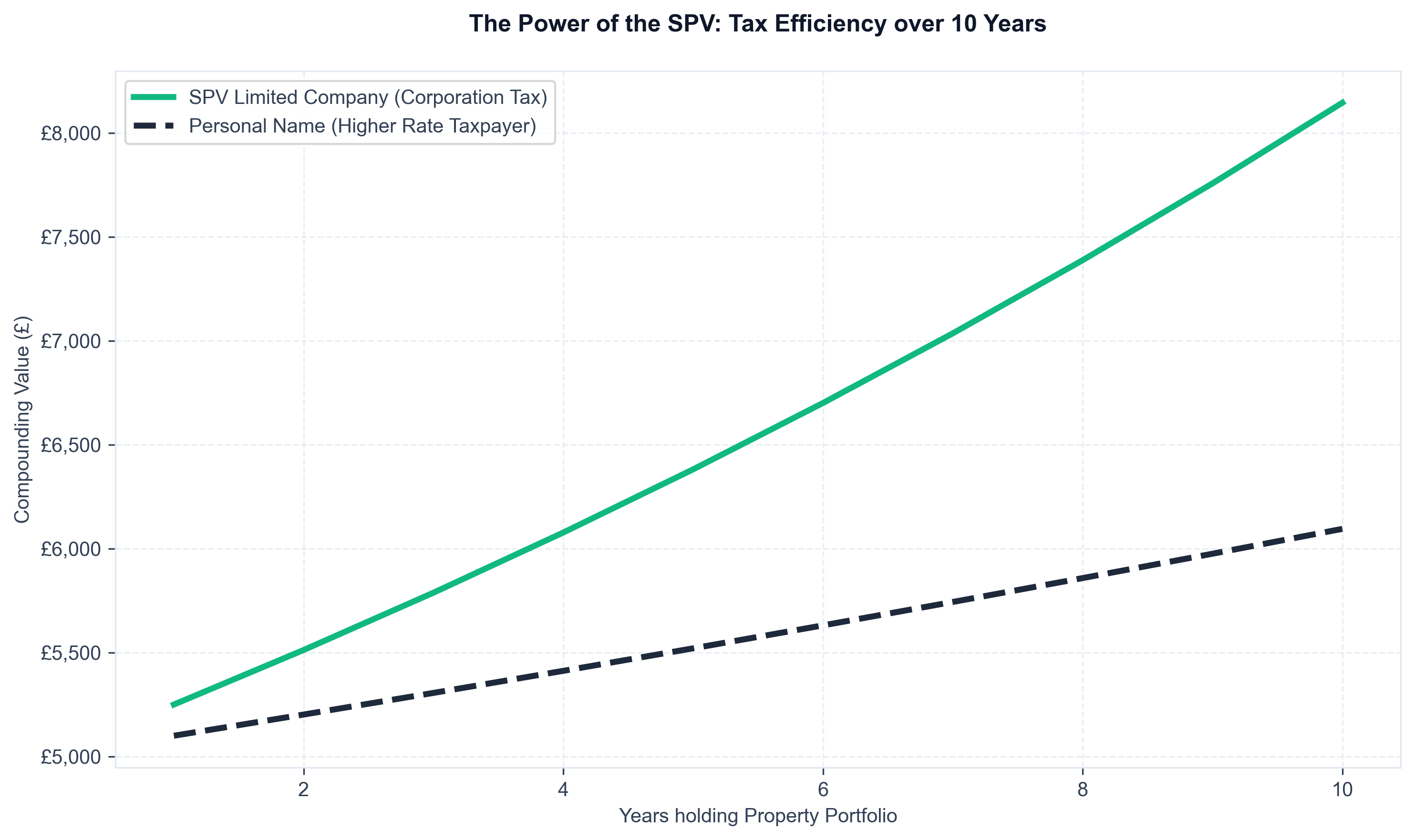

Section 24 and the Shift to Limited Companies

Under Section 24 of the Finance (No. 2) Act 2015, individual landlords can no longer deduct mortgage interest from their rental income before calculating their tax liability. Instead, they receive a basic rate (20%) tax reduction. For higher-rate or additional-rate taxpayers, this often results in paying tax on zero actual profit, or even taking a loss.

Consequently, a significant shift has occurred towards purchasing investment properties through Special Purpose Vehicles (SPVs) — dedicated limited companies. Corporate tax rates (currently ranging from 19% to 25% depending on profits) are applied to the net profit after all expenses and mortgage interest have been deducted. While extracting those profits via dividends incurs further tax, the corporate structure allows for far greater compounding of wealth within the company.

Capital Gains Tax (CGT)

When you eventually sell an investment property, the profit (sale price minus purchase price and allowable acquisition/improvement costs) is subject to Capital Gains Tax. For individuals, this is currently taxed at 18% for basic rate taxpayers and 24% for higher rate taxpayers on residential property.

Actionable Next Steps for Aspiring Investors

If you are ready to begin buying property for investment, a systematic approach is essential:

- Define Your True Strategy and Budget: Calculate exactly how much usable capital you have after accounting for the 5% SDLT surcharge and legal fees. If you have £50,000, you are looking at properties priced around £120,000 to £140,000 using a 75% LTV mortgage.

- Speak to a Broker and an Accountant: Before viewing any properties, secure an Agreement in Principle (AIP) from a specialist BTL mortgage broker. Simultaneously, consult a property tax accountant to determine if you should purchase in your personal name or via an SPV limited company.

- Target High-Yield Geographies: Focus your research on strong Northern regions (e.g., Glasgow, Liverpool, Leeds) where net yields safely exceed your mortgage interest stress tests.

- Analyze Data, Not Emotion: Use platforms like Rightmove Plus or specialized property software to analyze actual sold prices, average time-on-market, and realistic rental ceilings for specific streets. Never rely solely on an estate agent's projected yield.

- Build a Power Team: Before making an offer, assemble your team. You need a fast, communicative conveyancing solicitor, an independent RICS surveyor, and crucially, a highly reviewed local letting agent who specializes in the type of property you are purchasing.

Investing in property in the UK is no longer a passive endeavour. However, with clinical data analysis, defensive financial structuring, and a clear understanding of the risks, it remains a highly robust vehicle for long-term wealth accumulation.

Want more insights? Be sure to read the latest post from the Shaded Canvas blog or explore our deep dive into finding the best capital growth property for your next move.

📚 Related Reading

- Buy Dirt

- Buy Dirt Part 2

- Hobbies That Make Money

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →