If you are evaluating the 2026 real estate market and asking yourself, "Is off plan property investment worth it in the UK?", you are asking the wrong question.

Off-plan property is not universally "worth it" or "not worth it." It is a highly leveraged financial instrument. When executed correctly in a high-growth regeneration zone, it offers Return on Capital Employed (ROCE) metrics that completely obliterate traditional buy-to-let (BTL) or index fund returns. When executed poorly, it is a fast track to contract default, negative equity, and the permanent loss of a £50,000 deposit.

In 2026, the era of blind off-plan speculation is over. The cost of commercial debt and the scrutiny of RICS surveyors mean that you can no longer simply throw a 20% deposit at a developer and wait for unearned capital appreciation.

In this comprehensive 3,000-word audit, Shaded Canvas will dismantle the mathematics of off-plan investing. We will expose exactly when off-plan is the most lucrative asset class in the UK, when you are guaranteed to lose money, and how sophisticated investors use institutional staging to mitigate their absolute risk.

1. The Core Mechanics: What Makes Off-Plan Lucrative?

Before we dissect the risks, we must understand why institutional funds and elite retail investors continue to deploy billions into unbuilt concrete.

The fundamental allure of off-plan investing is Staging Leverage.

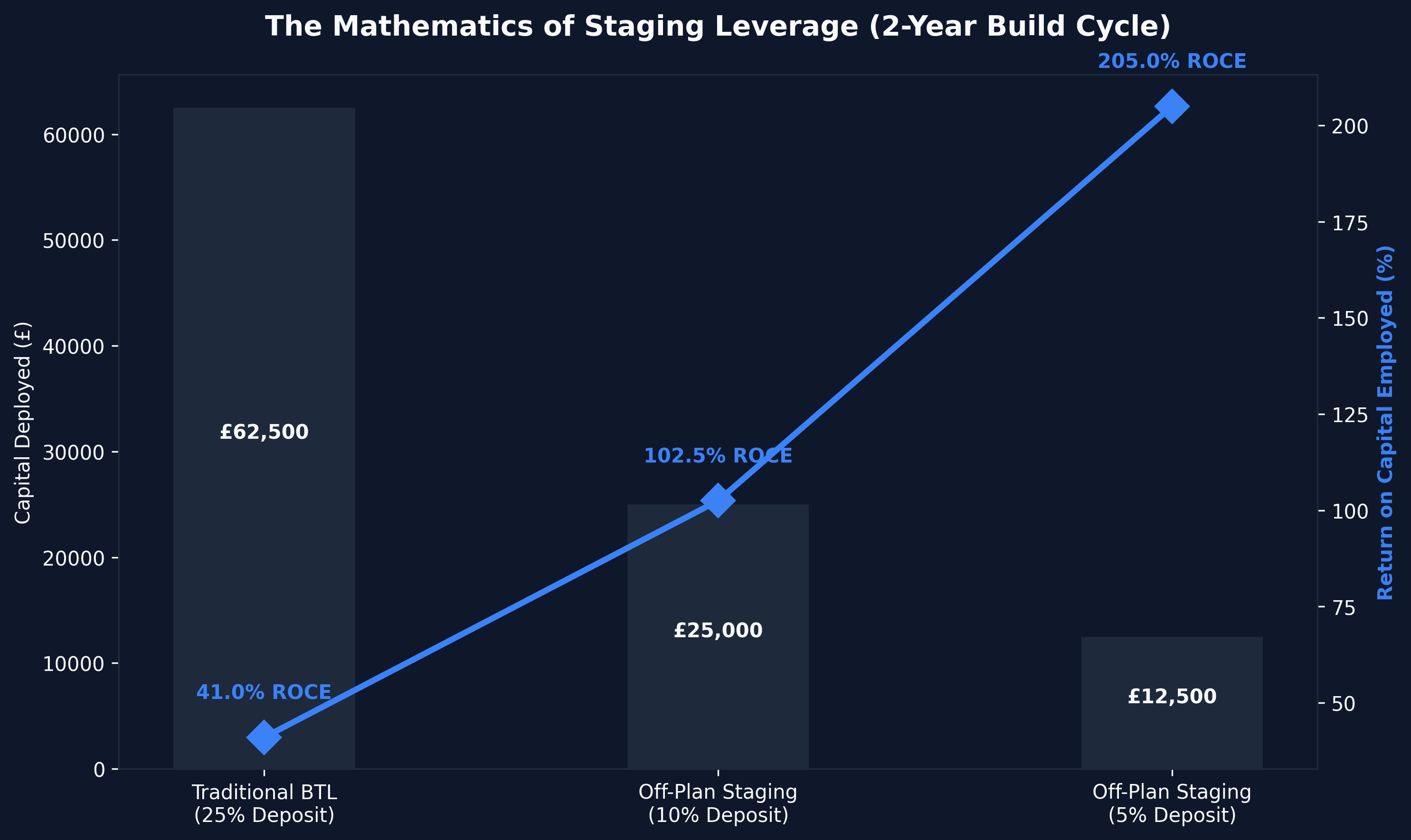

The Mathematics of Staging Leverage

When you buy a traditional Victorian terrace worth £250,000, you must deploy a 25% deposit (£62,500) and secure a mortgage within 8 weeks. Your capital is instantly locked in, and you begin paying mortgage interest immediately.

When you buy off-plan, you are buying a contract to complete a purchase 24 to 36 months in the future. Crucially, developers in 2026 frequently accept a 5% to 10% exchange deposit to legally secure the unit.

- Purchase Price: £250,000

- 10% Exchange Deposit: £25,000

- Build Cycle: 24 Months

For two years, you control a £250,000 asset having only deployed £25,000.

If the broader market (or that specific regeneration zone) inflates by 5% annually, the property will be worth £275,625 at practical completion. That £25,625 in equity growth belongs entirely to you. You generated a 102.5% Return on your Deployed Capital before the building was even finished, without ever paying a penny of mortgage interest or dealing with a tenant.

This is the power of the best new build property investment strategies, and it is the single reason off-plan continues to dominate investor portfolios.

2. The Zero-CapEx Decade

The second reason off-plan is highly sought after is the elimination of Capital Expenditure (CapEx).

If you read our guide on how to invest in property uk, you will know that the "gross yield" advertised by traditional estate agents is a fiction. A 30-year-old property yielding 6% gross will easily consume 1.5% to 2% of its value every year in structural maintenance, boiler replacements, and void periods while repairs are undertaken.

New builds are insulated by the NHBC 10-year warranty (or equivalent, like Premier Guarantee), alongside a 2-year developer defect period.

If the roof leaks in Year 3, you do not pay the £8,000 repair bill from your rental profits; the warranty provider pays it. Therefore, an off-plan property yielding 5.5% gross often delivers a higher True Net Yield than a Victorian terrace yielding 7% gross, simply because the maintenance budget is algorithmically reduced to zero for the first decade.

3. The Ultimate Threat: The Valuation Gap

If off-plan offers 100%+ ROCE and zero CapEx, why do retail investors lose money?

The answer is the Valuation Gap. This is the single metric that determines whether an off-plan investment is "worth it."

Developers bake a "New Build Premium" (usually 10% to 15%) into the initial purchase price to fund their marketing suites and profit margins. They assume the two-year build cycle will generate enough organic market inflation to absorb that premium.

If the market stagnates, the RICS surveyor assessing the property for your commercial mortgage at Month 23 will aggressively "down-value" the unit.

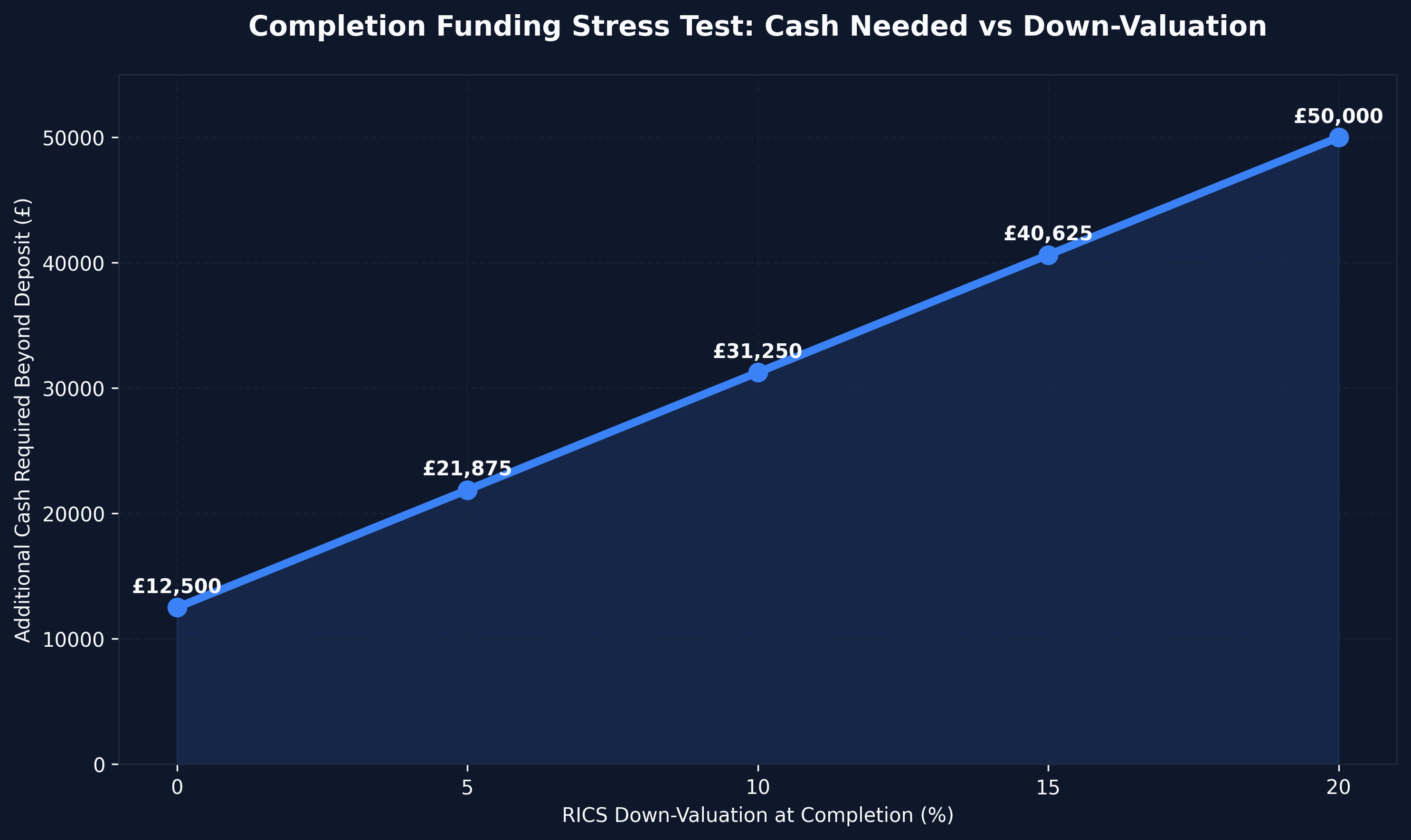

The Anatomy of a Contract Default

- Original Purchase Price: £250,000

- Deposit Paid During Build (20%): £50,000

- Balance Owed to Developer at Completion: £200,000

- RICS Valuation at Month 23: £225,000 (A 10% down-valuation)

Your buy-to-let lender will only offer a 75% LTV mortgage against the new £225,000 valuation (£168,750).

You owe the developer £200,000. The bank is only giving you £168,750. You now face a £31,250 Cash Shortfall.

You legally possess 28 days to find £31,250 in cash. If you cannot, you default on the contract. You lose your original £50,000 deposit, the developer repossesses the unit, and they may sue you for the remaining deficit.

Is Off-Plan Worth This Risk?

It is only worth it if you have stress-tested the valuation gap using tools like our off plan property investment yield calculator uk and possess the absolute liquid cash reserves necessary to plug a 10% down-valuation. If a 10% down-valuation bankrupts you, off-plan is explicitly not worth it for your current financial profile.

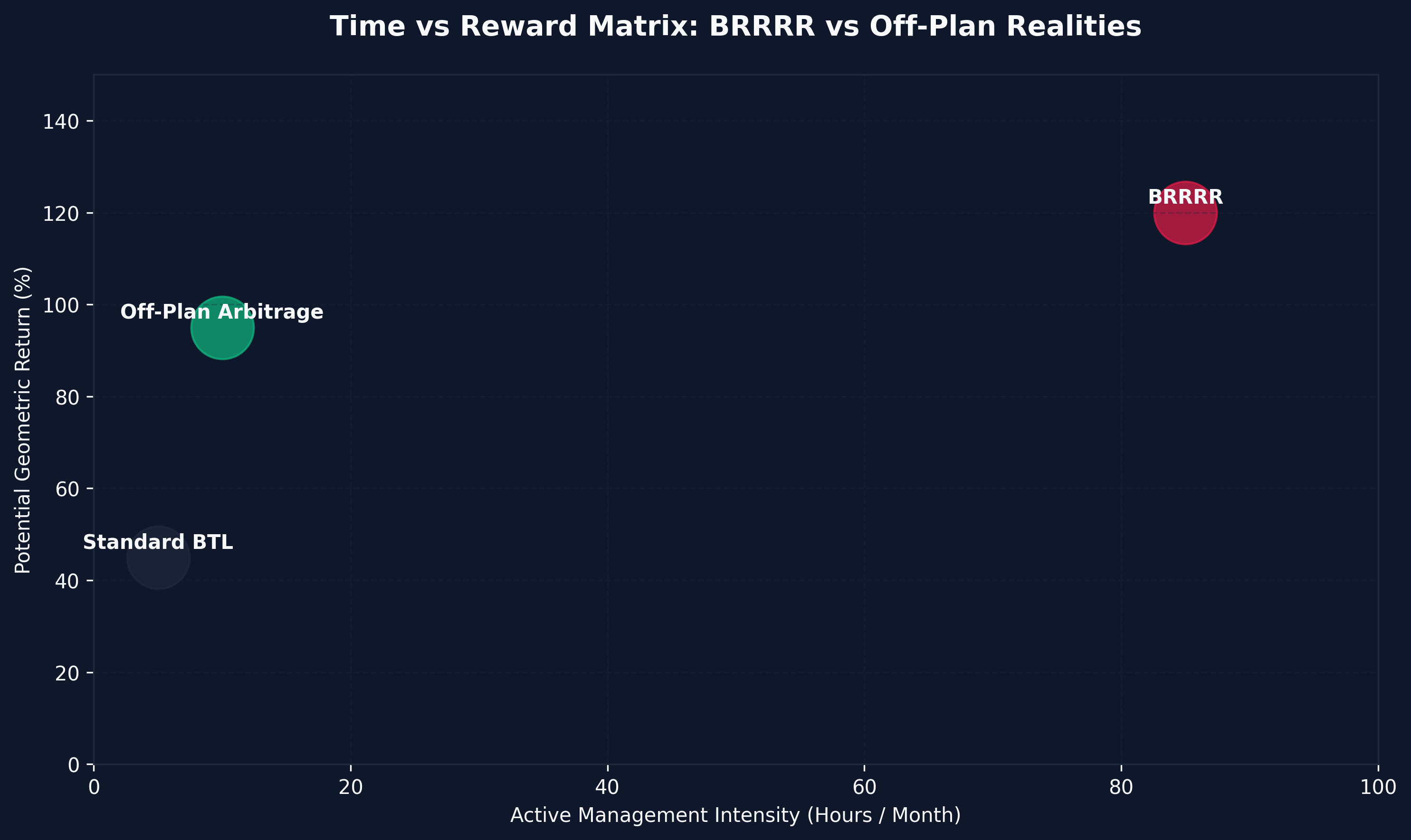

4. Off-Plan vs The BRRRR Strategy

To determine if off-plan is worth it, you must compare it against the dominant alternative for high-leverage investors: The BRRRR Strategy (Buy, Rehab, Rent, Refinance, Repeat).

For a complete breakdown of BRRRR mechanics, review our definitive guide: What is the BRRRR Method?.

The BRRRR Argument

BRRRR advocates argue that off-plan is mathematically inferior because you are paying wholesale prices (plus a developer premium) and hoping the market appreciates. With BRRRR, you buy a dilapidated property at a 30% discount, force the appreciation yourself via construction, and refinance your initial capital completely out of the deal within six months.

- BRRRR Pros: Instant equity creation; full capital recycling; no reliance on market inflation.

- BRRRR Cons: Extremely high execution risk; relies on expensive bridging finance; demands intense project management of builders; asset remains CapEx-heavy after rehab.

The Off-Plan Argument

Off-plan advocates argue that BRRRR is functionally a full-time job, whereas off-plan is a purely passive financial instrument.

- Off-Plan Pros: 100% passive; staging leverage requires less upfront cash; NHBC warranties eliminate 10 years of CapEx; EPC A/B ratings future-proof against green legislation.

- Off-Plan Cons: Total reliance on the developer not going bankrupt; total reliance on market inflation to absorb the new build premium; vulnerability to the Valuation Gap.

The Verdict: If you are a time-poor, highly-paid professional (e.g., a software engineer or surgeon) seeking passive capital deployment, off-plan is significantly more "worth it" than attempting to manage a structural roof replacement in a city three hours away. If you have infinite time but limited capital, BRRRR is the mathematically superior route.

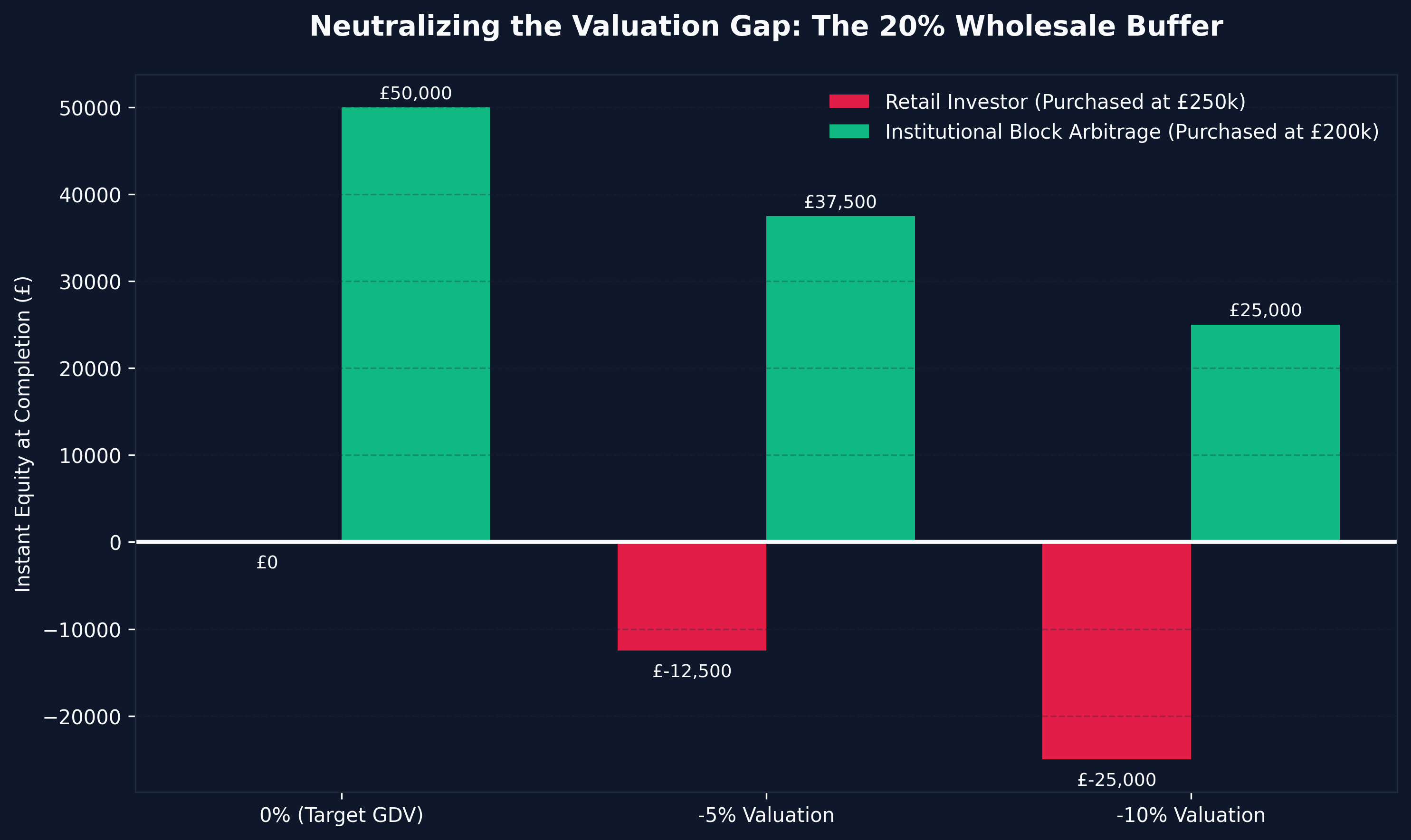

5. Mitigating the Risk: Institutional Block Arbitrage

If you want the passive, zero-CapEx benefits of off-plan without the terrifying risk of the Valuation Gap, there is one ultimate strategy: Developer Block Arbitrage.

As detailed in our how to finance new build property investment audit, developers require massive pre-sales to secure their bank funding.

Institutional funds exploit this desperation by buying 20 units in a single transaction, demanding a 20% wholesale discount off the retail price.

- Retail Price: £250,000

- Institutional Price: £200,000

If the RICS surveyor down-values the property by 10% upon completion (valuing it at £225,000), the institutional fund does not care. They bought it for £200,000. They are still sitting on £25,000 in embedded equity despite a market crash. The Valuation Gap threat has been mechanically neutralized.

How Retail Investors Can Access This

Until recently, unless you possessed £4M in cash, you could not execute block arbitrage.

In 2026, the rise of fractional property investment UK platforms has shattered this barrier. Syndicates (like the models utilized at Shaded Canvas) pool the capital of hundreds of retail investors to acquire the block at the £200,000 wholesale price.

Retail investors can deploy as little as £10,000 and receive the exact same 20% downside protection and institutional yields as a £500M hedge fund. For the vast majority of retail investors, this is the safest and most efficient way to answer "yes" to whether off-plan property is worth it.

6. The Verdict: When is Off-Plan NOT Worth It?

To provide an objective audit, we must explicitly outline when off-plan property investment is a mathematically ruinous decision in 2026.

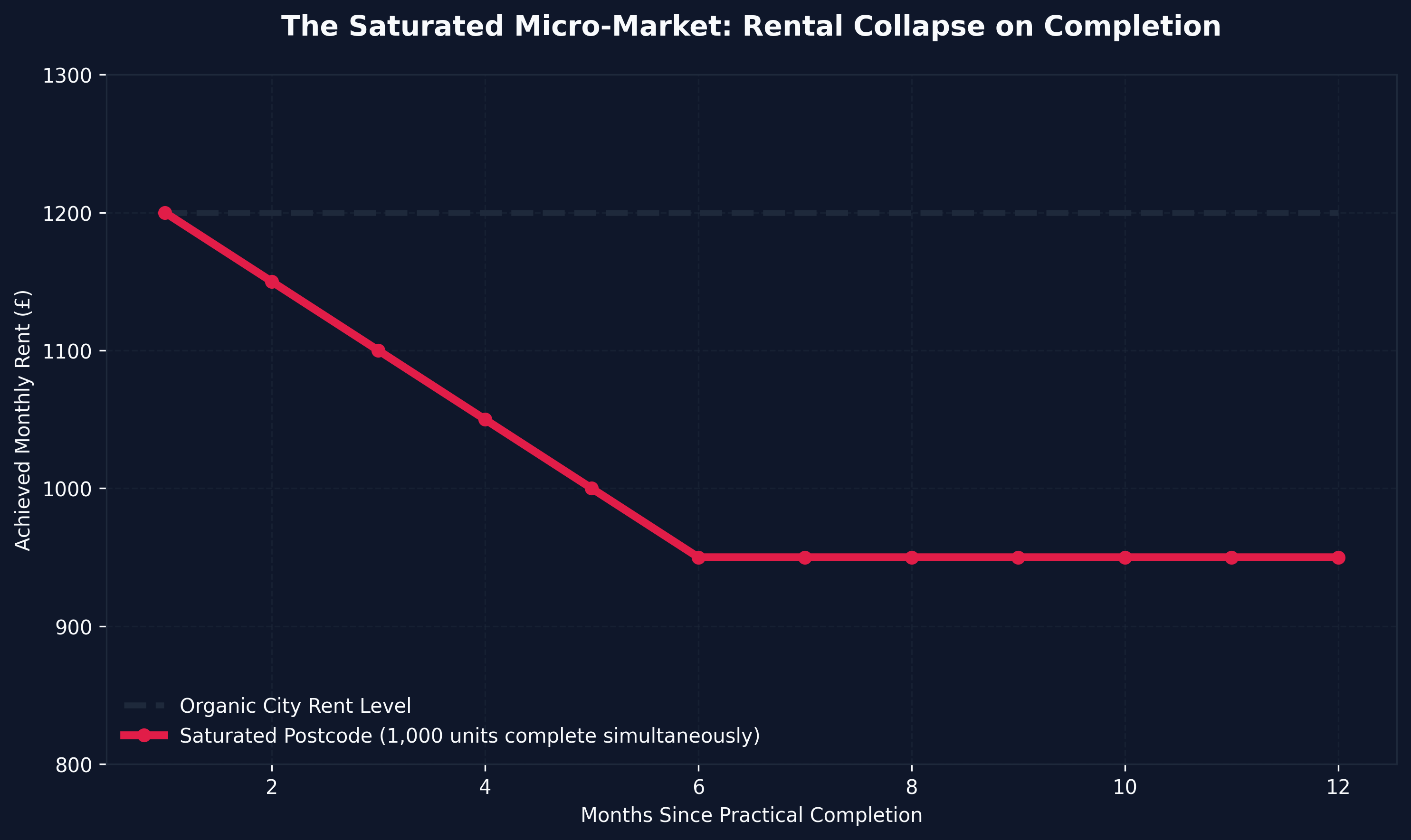

1. When buying in a totally saturated micro-market. If a developer is building a 500-unit tower, and there are three other 500-unit towers being built on the exact same street, you will face catastrophic rental void periods. Upon completion, 2,000 identically furnished 1-bed apartments will hit GoCompare and Rightmove on the exact same day. Landlords will inevitably slash rents in a race to the bottom to secure tenants, annihilating your yield.

2. When the Service Charge exceeds £2,500 annually. Luxury amenities (pools, gyms, 24/7 concierges) are yield killers. A £3,500 annual service charge acts as a massive localized tax on your net operating income. Off-plan is only worth it when you target "naked buildings"—boutique blocks with a lift and a secure entry system, keeping service charges below £1,200.

3. When you lack the liquid reserves to plug a 10% down-valuation. As explored above, if you are deploying 100% of your net worth into an off-plan deposit, you are over-leveraged. You must possess a liquid cash shock-absorber.

Summary: Is it worth it?

Yes, off-plan property investment is worth it in the UK in 2026, but only if you execute it as a sophisticated financial instrument.

If you weaponize staging leverage (putting 5% down to control 100% of the asset's growth), if you utilize the NHBC warranty to strip CapEx from your projections, and if you eliminate the new build premium by hunting institutional block discounts, off-plan generates risk-adjusted returns that BTL landlords can only dream of.

However, if you blindly buy a retail-priced unit in a saturated postcode and pray the surveyor is generous in two years' time, you are not investing; you are gambling.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →