The difference between a multi-million-pound property portfolio and a stressful, cash-draining liability is almost entirely mathematical. Novice investors purchase property based on emotional aesthetics—the color of the front door, the proximity to a nice park, or general speculation about the area "feeling up-and-coming." Professional investors ignore the bricks and mortar entirely; they purchase a series of cash flows.

In 2026, the United Kingdom property market is ruthless. With Bank of England base rates stabilizing around 5%, stringent new EPC compliance mandates, and the devastating reality of Section 24 taxation, the margin for error has been eradicated. If you do not possess a granular, commercial understanding of how to utilize a buy to let yield calculator uk, you will lose money.

This comprehensive guide systematically deconstructs the exact formulas professional fund managers use to underwrite property acquisitions. We will bridge the gap between misleading "Gross Yield" headlines and the brutal reality of "True Net Cash Flow," empowering you to analyze any UK postcode with institutional precision.

1. Defining the Core Metrics: Gross vs. Net Yield

Before we deploy complex financial modeling, we must establish the foundational vocabulary of property investment. The industry is saturated with agents and developers intentionally weaponizing these terms to misrepresent the financial viability of an asset.

What is Gross Yield?

Gross yield is the absolute most basic, unrefined metric in property investment. It represents the annualized total rental income expressed as a percentage of the total property purchase price.

The Gross Yield Formula: (Annual Rental Income / Property Purchase Price) x 100 = Gross Yield %

Example:

- You purchase a terrace house in Manchester for £150,000.

- The tenant pays £800 per month.

- Annual Rent = £9,600.

- (9,600 / 150,000) x 100 = 6.4% Gross Yield.

The Danger of Gross Yield: Gross yield is practically useless for commercial underwriting. It completely ignores the cost of debt, operational expenses, taxation, and void periods. If an off-plan developer heavily markets an apartment by screaming "8% Guaranteed Yield!", they are exclusively quoting Gross Yield to hide a catastrophic underlying cash flow position.

What is Net Yield?

Net yield is the metric that dictates your survival. It measures the true annual return on the property after all operational running costs have been aggressively deducted, but crucially, before mortgage financing costs and taxation are applied.

The Net Yield Formula: ((Annual Rental Income - Annual Operating Expenses) / Property Purchase Price) x 100 = Net Yield %

Standard UK Operating Expenses (OpEx):

- Letting Agent Management Fees: Typically 10% to 15% (+ VAT) of gross rent.

- Maintenance & Repairs Buffer: Minimum 5% to 8% of gross rent allocated to a Sinking Fund.

- Landlord Insurance: Standard building and public liability cover.

- Ground Rent & Service Charges: The absolute destroyer of leasehold apartment yields.

- Void Period Buffer: Calculating a conservative 1-month vacancy per annum (roughly 8.3%).

What is Cash-on-Cash Return (ROI)?

While Net Yield measures the performance of the overall asset, Cash-on-Cash Return measures the velocity and performance of your specific liquid capital deployed into the deal. This is the ultimate metric for leveraged buy-to-let property investors.

The Cash-on-Cash Formula: (True Annual Net Cash Flow / Total Cash Capital Deployed) x 100 = Cash-on-Cash Return %

Your Total Cash Capital Deployed includes your deposit (e.g., 25%), Stamp Duty Land Tax (SDLT) including the 5% investor surcharge, broker fees, legal conveyancing costs, and any initial day-one refurbishment capital required to make the property let-ready. Your True Annual Net Cash Flow is the final profit remaining after absolutely all expenses, including your monthly mortgage interest payment.

2. Executing a 2026 Deal Analysis: The Reality Check

Let's drag these academic formulas into the trenches of the 2026 property market. We will utilize a theoretical rental property yield calculator to strip-mine a highly standard UK property acquisition, revealing how rapidly a "good deal" can structurally collapse if the debt model is incorrect.

The Target Asset:

- Location: 2-Bedroom Apartment, Leeds City Centre.

- Tenure: Leasehold.

- Purchase Price: £220,000.

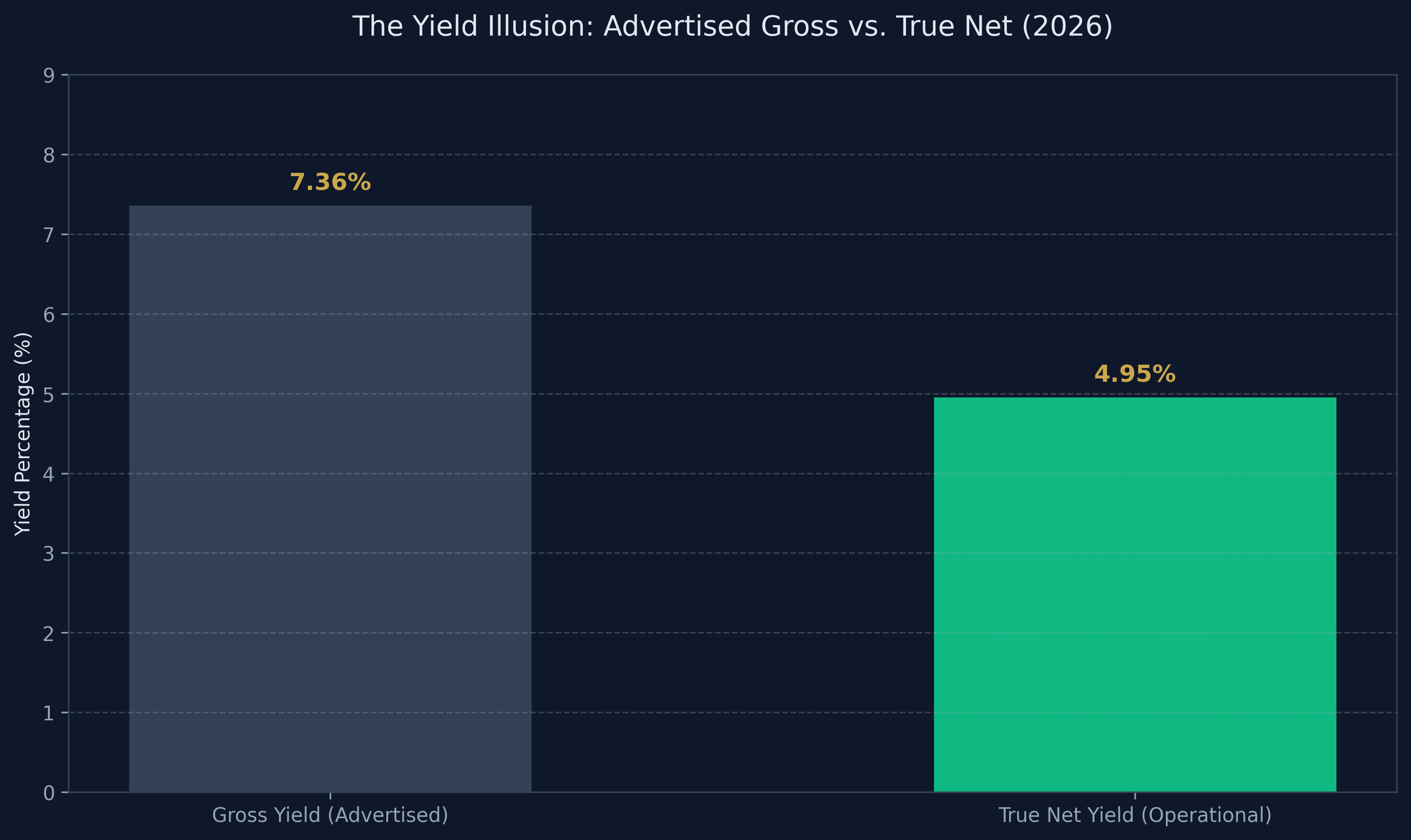

- Gross Monthly Rent: £1,350 (£16,200 annually).

- Advertised Gross Yield: 7.36% (Looks fantastic on a Rightmove listing).

Step 1: Calculating the Capital Deployment

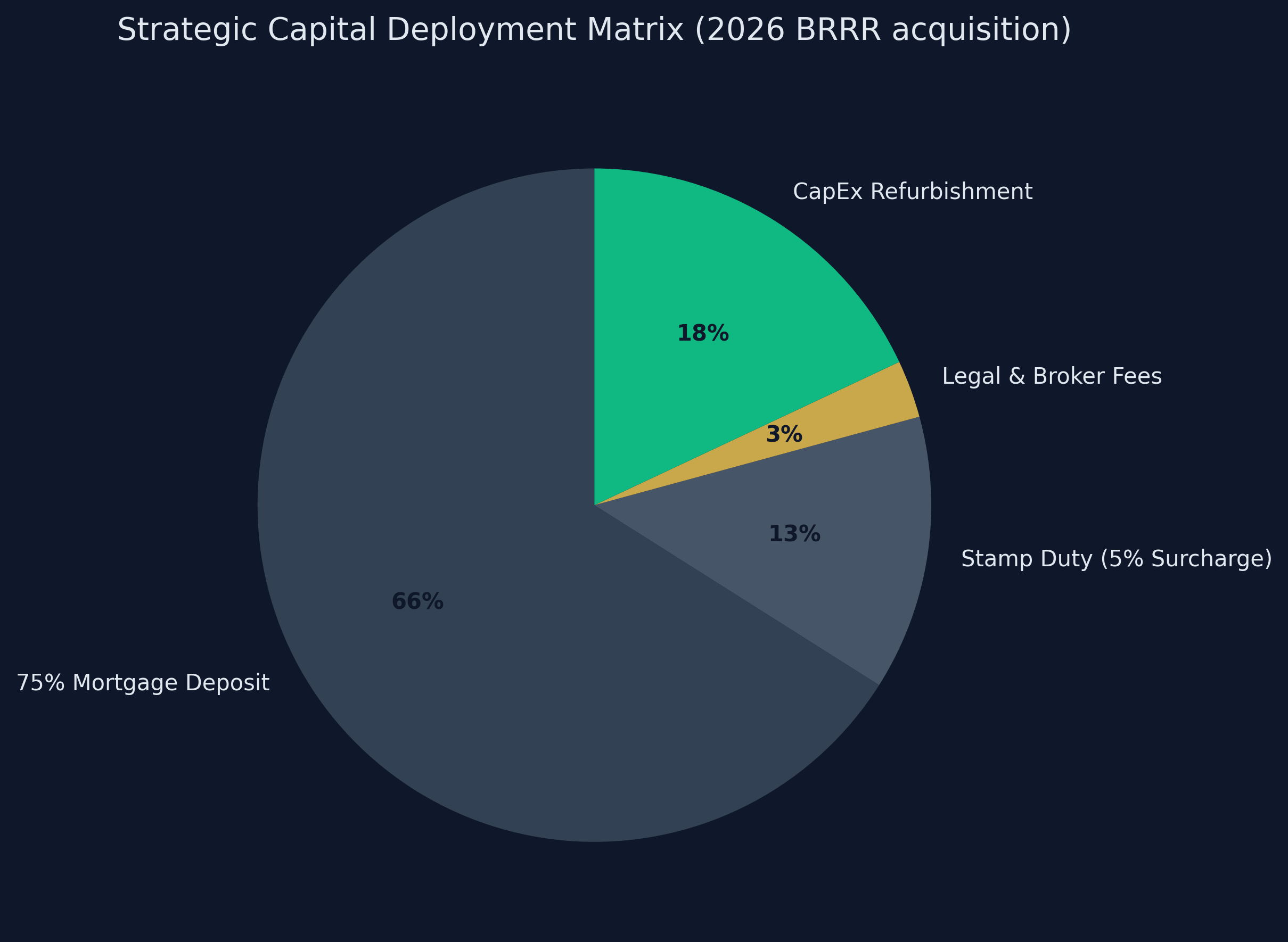

You are not paying £220,000. You are heavily leveraging the bank's capital. What is your true cash outlay?

- 75% LTV Mortgage Deposit: £55,000

- SDLT (including 5% Surcharge): £11,000

- Legal & Conveyancing: £1,800

- Mortgage Broker Fee: £500

- Lender Arrangement Fee (Added to loan): £0 upfront (£1,995 added to £165,000 debt = £166,995 total loan).

- Total Cash Deployed (Your Money): £68,300

Step 2: Stripping the Operational Expenses (OpEx)

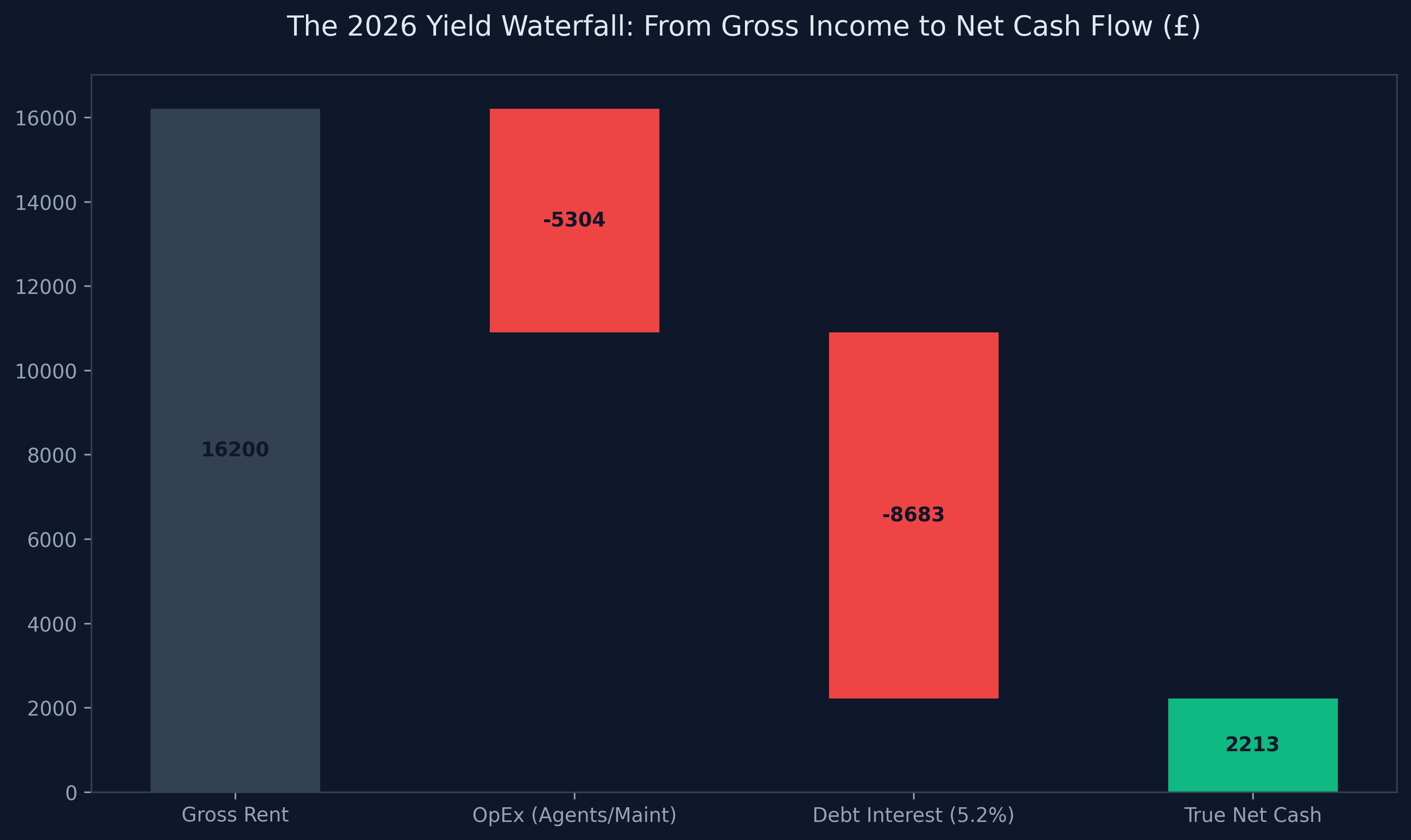

We must now brutalize that £16,200 annual gross rent with unavoidable real-world friction.

- Gross Annual Rent: £16,200

- Subtract: Agent Fee (12% inc VAT) = -£1,944

- Subtract: Service Charge & Ground Rent = -£2,200 (Catastrophic impact on leasehold).

- Subtract: Maintenance Sinking Fund (5%) = -£810

- Subtract: Insurance = -£350

- True Annual Operating Profit (NOI): £10,896

- (Notice how the "7.36% Gross Yield" is now a 4.95% Net Yield before we even pay the bank).

Step 3: Applying Exorbitant 2026 Debt Structures

You borrowed £166,995 via an Interest-Only commercial BTL mortgage secured inside your Limited Company (SPV). In 2026, a standard 5-year fixed rate sits at roughly 5.2%.

- Annual Mortgage Interest Payment: -£8,683

- (£10,896 Operating Profit minus £8,683 Debt Cost)

- Final Pre-Tax Net Cash Flow: £2,213 Annually (£184 per month).

Step 4: The Final Verdict (Cash-on-Cash ROI)

You deployed £68,300 of your hard-earned liquid cash. The asset generates £2,213 in true net cash flow per year. (£2,213 / £68,300) x 100 = 3.24% Cash-on-Cash Return.

The Commercial Conclusion: This is a terrible deal for cash flow. You are risking £68,000, taking on massive legal liabilities, and managing tenant risk—all to generate a return that is fundamentally lower than a completely risk-free, passively managed government gilt or high-yield savings account. The exorbitant Service Charge combined with 5.2% debt violently destroyed the 7.36% Gross Yield illusion.

3. The 7 Leverage Levers: How to Manipulate the Math

If standard city-center apartments are mathematically failing in 2026, how do professional investors build cash-flowing portfolios? They actively hunt specific asset classes that allow them to aggressively manipulate the variables within the buy to let yield calculator uk matrix.

There are seven specific "leverage levers" you can pull to force a fundamentally mediocre deal into a highly lucrative commercial venture.

Lever 1: The SPV Corporate Tax Shield (Section 24 Evasion)

If you executed the Leeds apartment deal described above in your personal name as a Higher-Rate (40%) taxpayer, the mathematics mutate from "terrible" to "catastrophic." Under Section 24, you cannot deduct that £8,683 mortgage payment as a business expense. You are taxed 40% on your Operating Profit (£10,896), resulting in a huge £4,358 tax bill. The government grants you a basic 20% tax credit on the mortgage interest (£1,736). Your true tax liability is £2,622. Since the property only generated £2,213 in cash, you must physically pull £409 out of your own salary every single year just to pay the taxman.

The Solution: You must acquire the asset via a Limited Company (Special Purpose Vehicle / SPV). The SPV deducts 100% of the mortgage cost before profit is calculated, exposing only the £2,213 true profit to standard UK Corporation Tax (19% to 25%). The SPV is the ultimate legal shield against the Treasury.

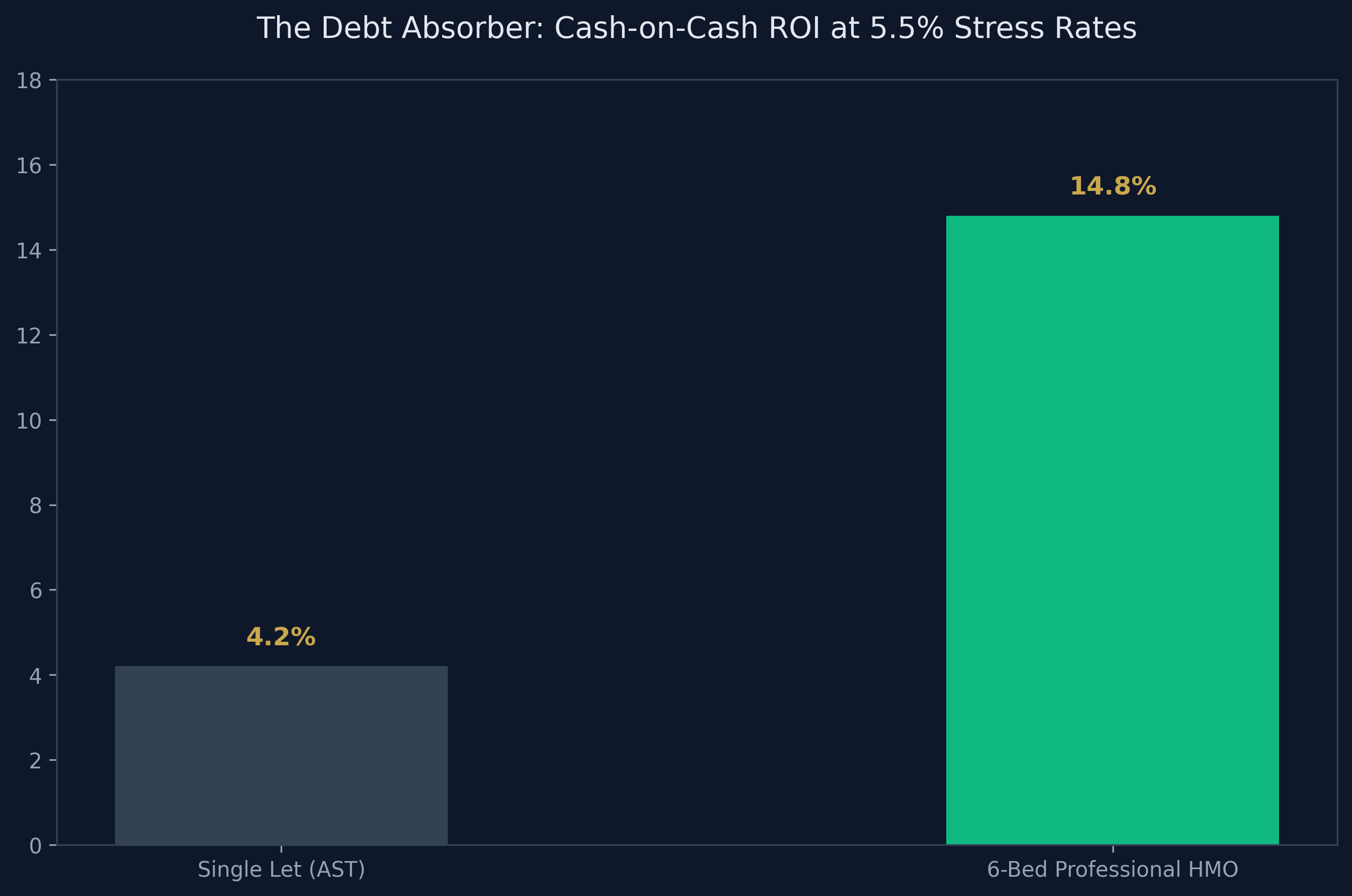

Lever 2: The HMO Revenue Multiplier

To combat 5.5% debt, you must drastically elevate your baseline Gross Rent. You cannot achieve this via standard single-family lets (ASTs) which possess a strict ceiling governed by localized wages. The solution is the House in Multiple Occupation (HMO). By acquiring a large 4-bedroom Victorian terrace, converting the reception rooms, and creating a 6-bedroom professional HMO, you decouple the rent from single-family affordability. Instead of collecting £1,200 for the whole house, you collect £650 per room. Your Gross Rent violently scales to £3,900 per month. Even after factoring in the colossal operational expenses (the landlord pays council tax, commercial broadband, and all soaring utility bills), the sheer volume of top-line revenue easily absorbs high interest rates, frequently pushing Cash-on-Cash Returns above 15%.

Lever 3: The Serviced Accommodation Arbitrage

Similar to the HMO, Serviced Accommodation (SA) or "Airbnb" strategies arbitrarily detach traditional rental ceilings. By targeting tourism bottlenecks, major hospital trust zones (for traveling locum doctors), or massive infrastructure projects (for commercial contractors), astute investors convert standard £1,000 pcm apartments into £3,500 pcm hospitality assets. The mathematical warning: this lever requires extreme operational hyper-vigilance. The management fees, constant professional cleaning overheads, and 18% Booking.com platform commissions drastically compress the gap between Gross Revenue and Net Profit.

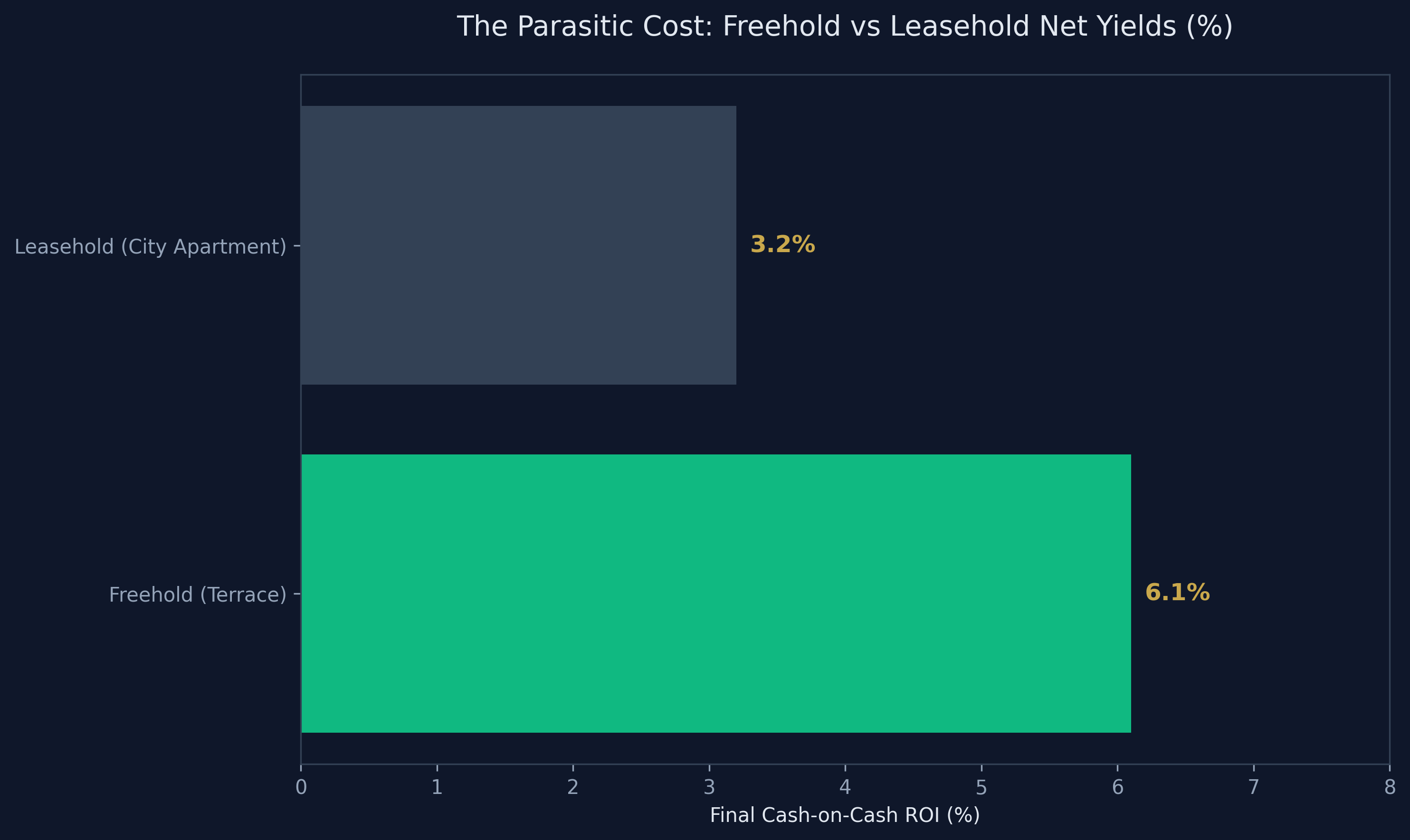

Lever 4: The Freehold Advantage (Eradicating the Parasite)

In our Leeds case study, the £2,200 annual Service Charge and Ground Rent effectively functioned as a secondary, highly punitive taxation system deployed by a private freeholder. It actively destroyed the net yield. Professional investors drastically prefer acquiring Freehold houses (terraces, semi-detached) over Leasehold flats. While a Victorian terrace may require more immediate CapEx for roof repairs, the investor retains absolute, dictatorial control over when and how that capital is deployed. There is no parasitic management company aggressively inflating their fee by 8% aligned with the Retail Price Index (RPI) every January.

Lever 5: Forcing Deep Equity via the BRRR Strategy

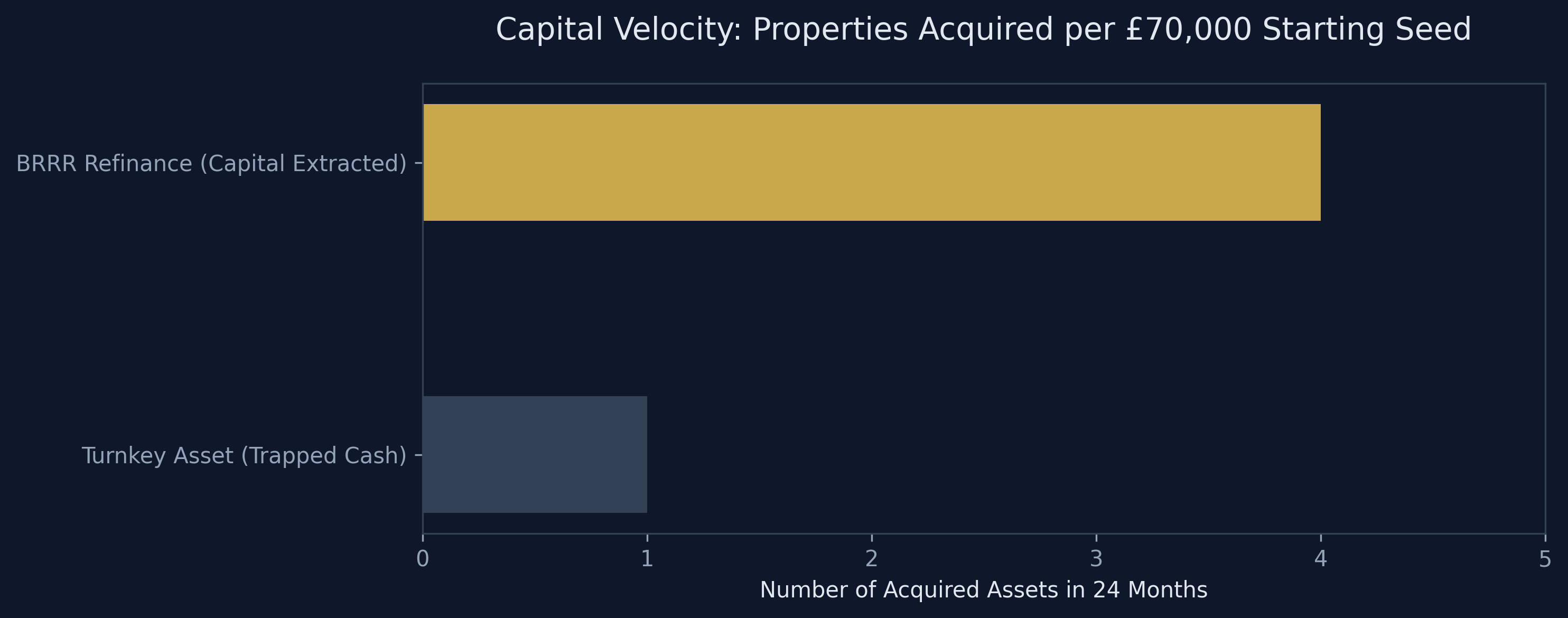

The ultimate method of maximizing Cash-on-Cash ROI is to structurally reduce the denominator in the equation: the "Total Cash Deployed." If you simply buy a turnkey property, your £50,000 deposit is trapped in the asset for a decade, waiting for organic macroeconomic inflation. By executing a BRRR strategy (Buy, Refurbish, Refinance, Rent), you hunt heavily distressed, un-mortgageable assets (e.g., properties lacking a functioning kitchen or bathroom). You acquire them via cash or expensive short-term Bridging Finance at a massive discount to True Market Value. You aggressively deploy £20,000 in heavy refurbishment, forcibly inflating the asset's value. Six months later, you refinance the asset at a standard 75% LTV against the new, higher valuation, extracting 80% to 100% of your initial capital out of the deal. You reuse that exact same chunk of capital to buy property number two. It is the holy grail of high-velocity capital scaling.

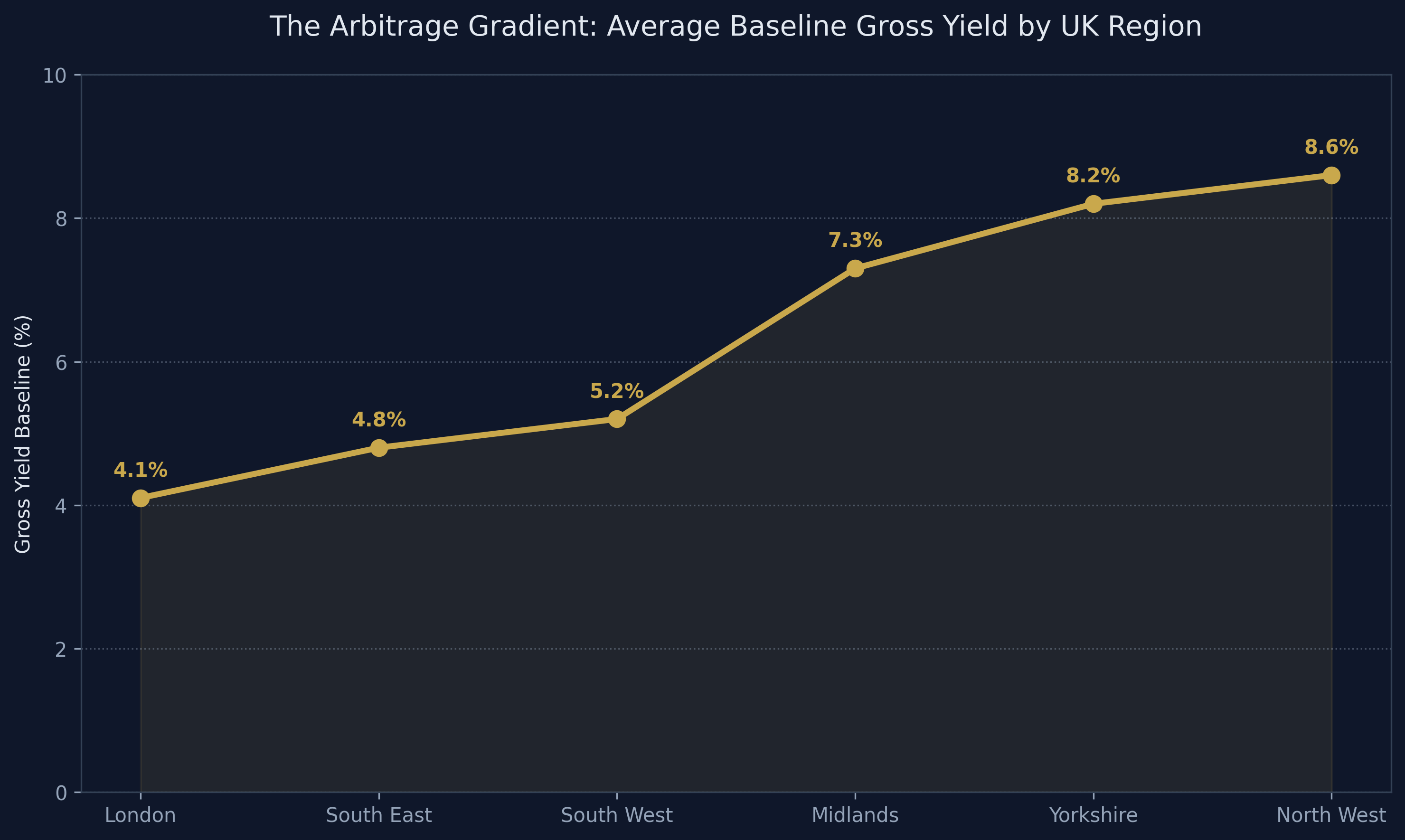

Lever 6: The Northern Powerhouse Yield Differential

Yield mathematics are geographically dictatorial. Capital values in the South East and London have hyper-inflated totally out of alignment with median localized salaries, violently compressing yields. An £800,000 semi-detached house in Surrey cannot physically rent for the £4,500 required to generate a 6.5% yield; local incomes do not support it. Conversely, the "Northern Powerhouse" arc (Liverpool, Manchester, Leeds, Sheffield, Newcastle) presents severe structural imbalances. Property acquisition costs remain historically suppressed, while massive inward migration of young professionals and corporate relocations (e.g., the BBC to Salford) continuously push rents higher. If you require aggressive yield to survive 5% mortgage rates, you must physically deploy your capital north of standard commuter belts.

Lever 7: Interest-Only Debt Structuring

Why do amateur landlords fail? Because they attempt to utilize 25-year Capital Repayment mortgages on commercial BTL assets. A repayment mortgage brutally destroys liquid cash flow. Yes, you are technically building equity, but you are rendering the asset highly vulnerable to minor fiscal shocks (like a void month or a broken boiler). Professional landlords exclusively utilize Interest-Only debt structures. They rely entirely on localized inflation and long-term asset appreciation (historically averaging 4% to 6% per annum over 20-year cycles in the UK) to invisibly "pay down" the real-world value of the loan. The liquid cash they preserve each month is aggressively diverted into their central Sinking Fund to ensure total corporate survival during a crisis.

4. The Hidden Variable: Inflation Arbitrage

A standard buy to let yield calculator uk is fundamentally two-dimensional; it provides a static snapshot of Year 1. It completely fails to calculate the most lucrative aspect of leveraged property acquisition: Inflation Arbitrage.

When you secure a £150,000 mortgage against an asset, the numeric value of that debt is fixed. However, if the broader UK economy suffers 4% localized inflation, the true purchasing-power weight of that £150,000 debt is slowly being eroded, year after year. Simultaneously, massive governmental money-printing and structural supply deficits cause the underlying physical asset (the bricks and mortar) to hyper-inflate.

Over a 15-year cycle, the tenant has covered 100% of your interest payments. Macroeconomic inflation has effectively paid off a third of the true burden of the principal debt. Meanwhile, your initial £50,000 deposit has leveraged an asset that has artificially doubled in nominal value. This is why highly leveraged property investments historically created more UK millionaires than any other asset class. It is the systemic, legalized transfer of wealth from those holding fiat currency to those holding scarce physical assets backed by massive institutional debt.

Conclusion: Engineering Your Portfolio for 2026

The era of blind speculation is over. If you attempt to acquire UK property in 2026 without possessing absolute, dictatorial control over a comprehensive buy to let yield calculator uk, the systemic fiscal friction (Section 24, 5.5% debt, incoming EPC mandates) will violently rip your capital apart.

However, for the analytical investor willing to pivot into hyper-professionalized corporate SPV structures, the current market represents a historically unique buying opportunity. As amateur, highly-taxed landlords panic and dump their portfolios onto the secondary market, structurally sound, high-yielding assets are currently available below True Market Value.

Execute the mathematics. Ignore the emotional noise. Stress-test the debt at 7%. Build an unshakeable 10% Sinking Fund. Do not invest for the aesthetic of the neighborhood; invest exclusively for the ruthless efficiency of the net yield.

Advanced Yield Diagnostics: The 2026 FAQ

Navigating the granular intricacies of a modern UK property acquisition requires specialized insight. To definitively master the buy to let yield calculator uk, we aggressively analyze the most common mathematical friction points encountered by active 2026 investors below.

Why Do Bank Stress Tests Keep Failing My Applications?

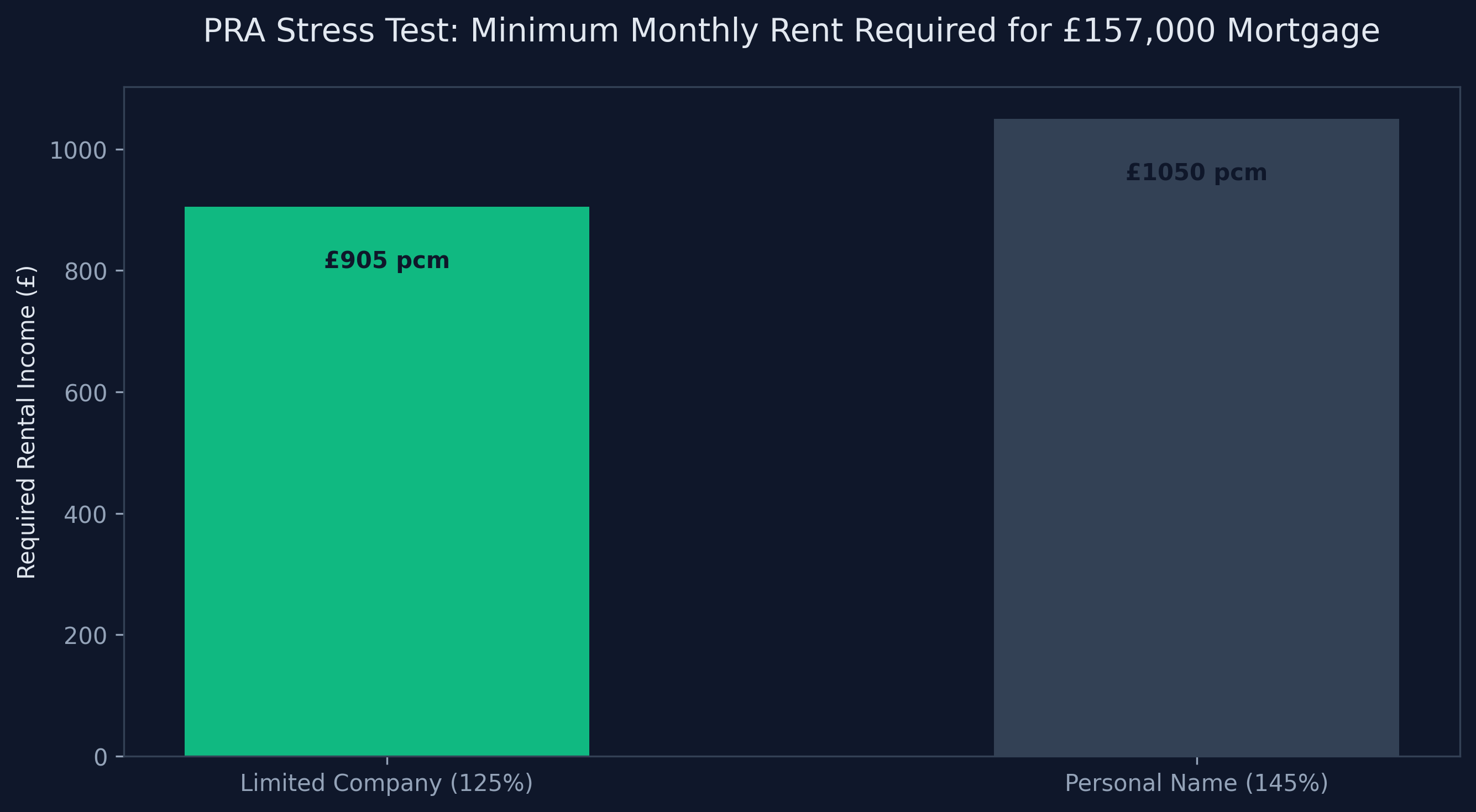

In 2026, securing the debt is significantly harder than finding the property. The Prudential Regulation Authority (PRA) forces all UK mortgage lenders to aggressively "stress test" your potential acquisition to prevent cascading defaults if base rates spike further. Lenders no longer look at the actual 5% pay rate of your mortgage. They apply a hyper-conservative localized Interest Coverage Ratio (ICR).

- The Personal Name ICR: If you buy in your own name as a higher-rate taxpayer, the bank typically demands the Gross Rent covers 145% of a theoretical 5.5% (or higher) stress rate applied against your debt.

- The SPV ICR: Because Limited Companies do not suffer Section 24 taxation, banks typically apply a vastly lower, highly favorable ICR of 125% against the stress rate.

If your property generates a 5% baseline gross yield, it fundamentally cannot mathematically pass a 145% at 5.5% stress test in the South of England. You will be ruthlessly declined. The only solutions are to inject a massive 40% deposit to lower the debt burden, perfectly pivot into an SPV structure, or hunt structurally higher 8% yields in the Northern Powerhouse regeneration zones.

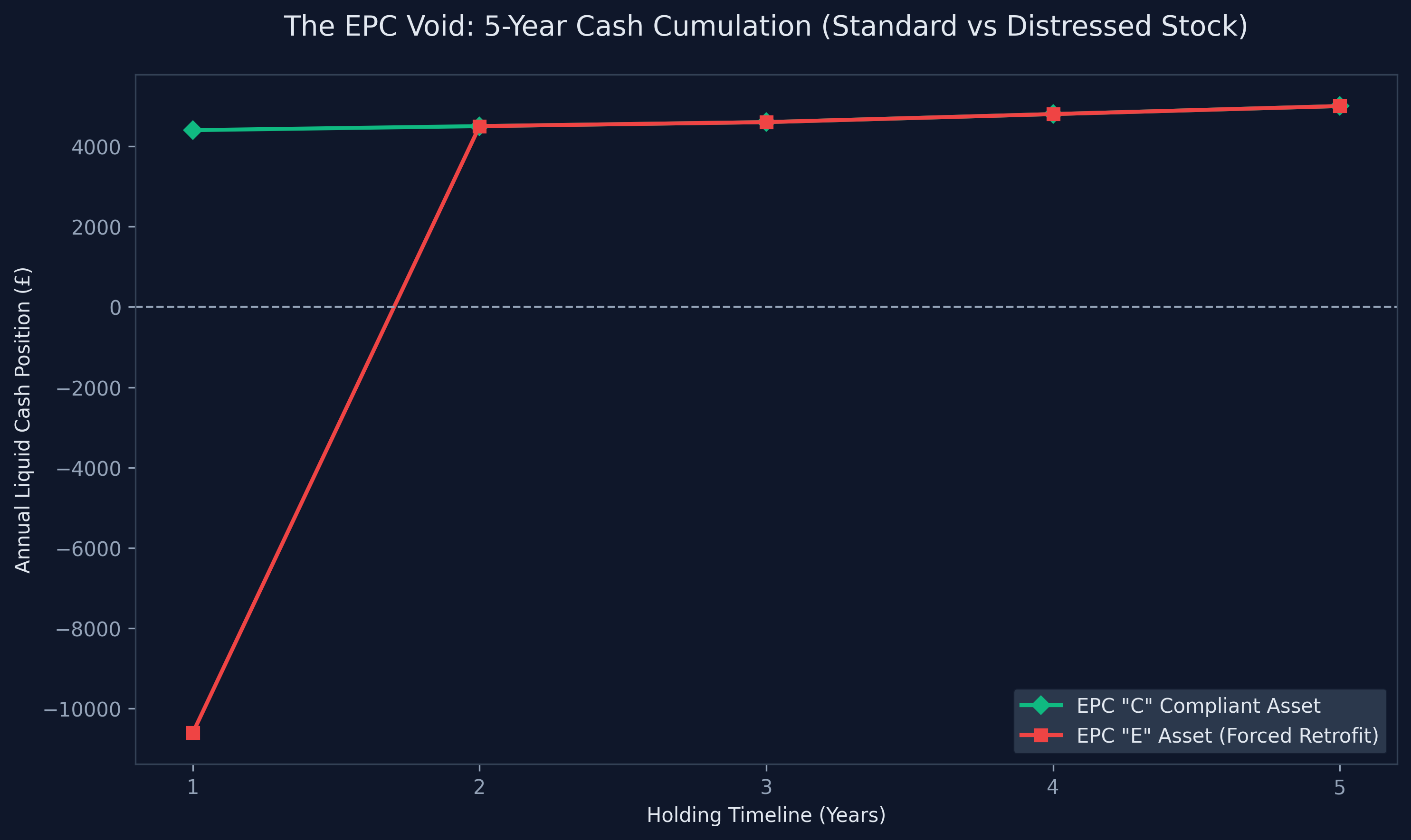

Does EPC Compliance Actually Destroy Net Yield?

The impending Minimum Energy Efficiency Standards (MEES) driving standard rental stock toward a mandatory 'C' rating is the hidden iceberg waiting to annihilate novice investors. A standard buy to let yield calculator assumes static CapEx. It does not account for a forced £12,000 retrofitting mandate. If you acquire an 'E' rated Victorian terrace, you must instantly deduct the cost of solid wall insulation, an A-rated boiler, and triple glazing from your theoretical Year 1 profits. This heavily front-loaded capital expenditure violently destroys the velocity of your capital, heavily artificially depressing the Cash-on-Cash Return for the first 36 months of ownership. Conversely, utilizing a specialized 'Green Mortgage' to acquire localized 'A' or 'B' rated new-builds can provide highly favorable, discounted interest rates, structurally boosting your net yield directly via ESG compliance rewards.

Is the Yield from Student "Pods" Fake?

Purpose-Built Student Accommodation (PBSA) is specifically engineered to target novice, overseas, or "armchair" investors. Developers heavily aggressively market "Guaranteed 8% Net Yields for 5 Years" alongside slick, off-plan CGI brochures. The mathematics are almost always structurally flawed.

- The Premium Pricing: You are drastically overpaying for the asset. A 15-square-meter "pod" might cost £80,000, representing a massive £5,300 per square meter valuation, completely detached from the localized residential market comparables.

- The Liquidity Trap: The "guaranteed yield" is simply the developer utilizing the exorbitant premium you fundamentally overpaid to gradually refund you your own money over 60 months. Once the guarantee expires, the central management company aggressively jacks up their service charges. When you attempt to sell the pod, you discover the terrifying reality: standard mortgage lenders refuse to finance localized micro-apartments under 30 square meters. Your only exit strategy is finding a clueless cash buyer, often forcing you to liquidate the asset at a catastrophic 30% to 40% capital loss.

How Does Inflation Impact My Sinking Fund?

A strictly rigid 5% maintenance deduction is a mathematical baseline, but it is deeply vulnerable to highly localized inflation. Because of Brexit-related supply chain friction and severe national labor shortages for skilled tradesmen, the physical cost of localized property refurbishment (plumbers, electricians, raw materials) has inflated drastically faster than the Consumer Price Index (CPI). A roof replacement that cost £3,500 in 2019 might demand £6,500 in 2026. If you simply allocate £70 a month to your Sinking Fund, you are structurally undercapitalized against real-world inflation. Elite portfolio builders actively adjust their CapEx reserves dynamically, pushing their maintenance buffer toward 8% to 10% during periods of heavy materials inflation to guarantee corporate survival during severe shock events.

Is Capital Growth Dead in the UK?

If interest rates remain structurally elevated near 5%, massive, sweeping national capital appreciation will be severely suppressed compared to the hyper-growth seen between 2010 and 2022. However, localized capital growth is far from dead. It has simply transitioned from a macro phenomenon into a highly targeted micro-phenomenon. Investors must stop relying on the general tide and start hunting localized alpha:

- Regeneration Arbitrage: Identifying localized towns slated for massive, government-backed infrastructure injections (new rail links, massive commercial warehouse deployments) before the broader retail market catches on.

- Forced Appreciation: Relying entirely on the BRRR methodology. If the market refuses to organically appreciate your asset, you must physically force value into the bricks via aggressive, highly optimized capital expenditure and structural extensions.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →