For over two decades, the great British public possessed an unwavering belief that "safe as houses" was not just a proverb, but a guaranteed macroeconomic law. Becoming a landlord was the ultimate pathway to passive income and generational wealth. However, the modern real estate landscape has been violently reshaped. With soaring interest rates, oppressive new tax legislation, and stringent regulatory compliance, the casual dinner-party question has morphed into a deadly serious financial calculation: Is buy to let property worth it in the UK in 2026?

The short answer is yes—but only if you execute it as a highly systematized, numbers-first commercial business. The era of the "amateur landlord" is dead, purged by compressed margins and the lethal impact of Section 24.

If you are considering deploying tens of thousands of pounds into UK bricks and mortar, you must discard outdated advice from 2018. This comprehensive guide aggressively breaks down the exact margins, operational costs, tax structures, and asset classes that define a successful, cash-flowing property portfolio in the current market environment.

1. The Death of the Amateur Landlord: Why the Market Shifted

To accurately evaluate if buy-to-let property remains a viable investment vehicle, we must first analyze the precise systemic shocks that caused hundreds of thousands of casual investors to flee the private rented sector (PRS) over the last three years.

The Eradication of Cheap Debt

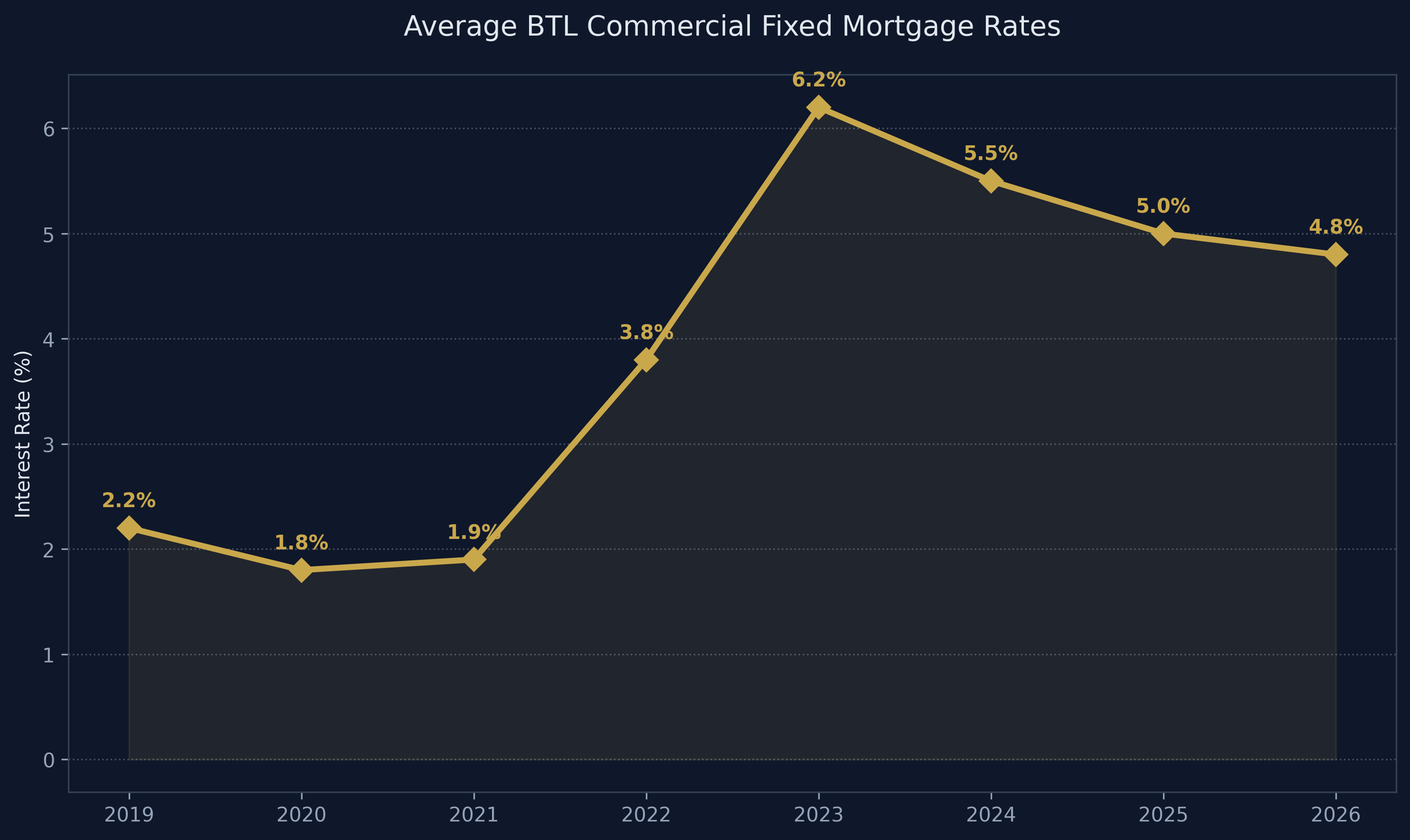

Between 2010 and 2021, the Bank of England base rate sat at historic lows, often hovering near 0.1%. Landlords could secure 5-year fixed-rate BTL mortgages for under 2.0%. In that paradigm, you could acquire a fundamentally mediocre property, operate it inefficiently, and still generate positive monthly cash flow via pure capital leverage.

In 2026, the base rate has stabilized at a structurally higher plateau. The new normal for commercial BTL borrowing sits squarely between 4.5% and 5.5%. This shift represents a massive increase in the direct cost of capital, violently compressing the gap between gross rent received and the net profit retained.

The Lethal Reality of Section 24

Perhaps the most destructive government intervention into the property sector was Section 24 of the Finance (No. 2) Act. This catastrophic legislation systematically removed the ability for private landlords (acting in their own name) who sit in the higher or additional-rate tax brackets to deduct their mortgage interest payments as an operational business expense.

Instead of paying tax on actual profit, these investors are now effectively taxed on their gross revenue and receive only a flat 20% basic-rate tax credit. For thousands of highly leveraged private landlords, this accounting shift turned incredibly profitable portfolios actively cash-negative, forcing immediate liquidations.

The Regulatory Burden: EPCs and Compliance

The UK government is rapidly driving toward Net Zero, heavily weaponizing the property market to achieve its goals. By 2030, standard rental properties are mandated to reach an Energy Performance Certificate (EPC) baseline rating of 'C'.

Acquiring a traditional, un-refurbished Victorian terrace in 2026 means inheriting an arbitrary £10,000 to £15,000 liability. You must immediately inject heavy capital expenditure (CapEx)—external wall insulation, A-rated boilers, and double glazing—simply to possess the legal right to rent the asset.

2. Why Institutional Capital is Still Buying UK Bricks

If the operational landscape is so unforgiving, why are global hedge funds, massive institutional build-to-rent (BTR) corporations, and elite portfolio builders aggressively sweeping up UK residential stock? Because they recognize a fundamental demographic truth that supersedes taxation.

The Ultimate Supply and Demand Imbalance

The United Kingdom suffers from a chronic, generational failure to construct sufficient housing. Decades of restrictive planning permissions (the Town and Country Planning Act), localized NIMBYism, and broken developer pipelines mean the UK physically cannot build the 300,000 homes a year required just to keep pace with localized demographic expansion and net migration.

This structural scarcity creates the ultimate safety net for the property investor. As amateur landlords exit the market, the available pool of Private Rented Sector (PRS) stock shrinks even further, directly colliding with expanding tenant demand. The unavoidable macroeconomic result? Relentless, aggressive upward pressure on rental values. Void periods in strong demographic hubs (like Manchester, Leeds, and Birmingham) have dropped to near zero. Tenants are bidding aggressively above listing price simply to secure accommodation.

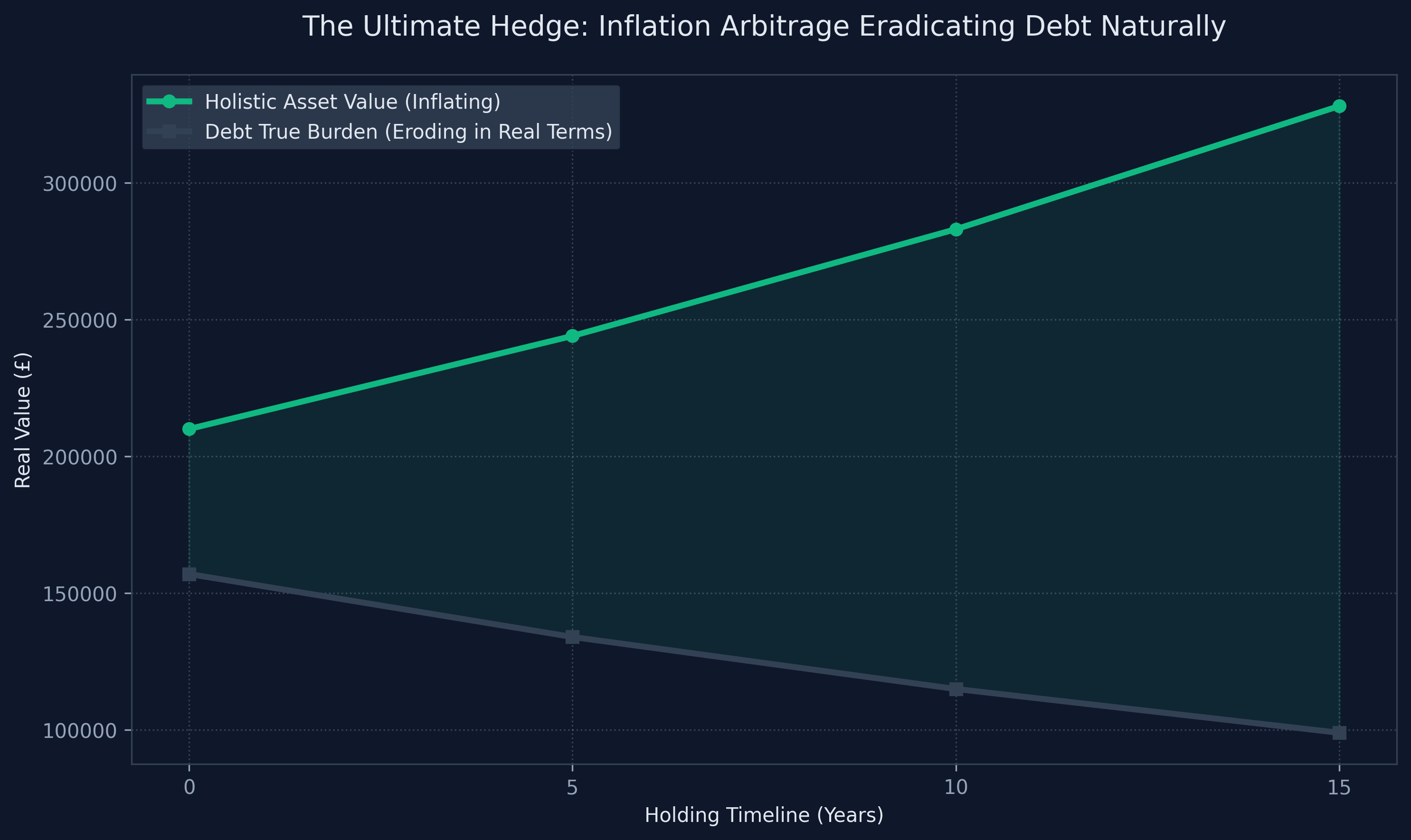

Sovereign Debt and Inflation Arbitrage

Professional investors do not just invest in property for the yield; they invest to trigger inflation arbitrage against massive debt structures.

If you take out a £200,000 interest-only mortgage to acquire an asset, that debt is fixed nominally. If UK inflation runs at an annualized 3%, the true purchasing-power weight of that £200,000 debt is slowly being eradicated by the economy itself. Meanwhile, your underlying physical asset (the bricks and mortar) heavily inflates alongside the broader money supply. Over a 15-year cycle, you are essentially utilizing the bank's capital to capture asset inflation while the economy organically pays down the true burden of the loan. This makes buy to let property one of the greatest wealth protection mechanisms legally available.

3. The 2026 Mathematics: Running a Live Deal Analysis

Let's drag the theoretical debate into the real world. We will run a standard 2026 acquisition through a targeted rental property yield calculator to determine if the holistic return on investment (ROI) justifies the risk.

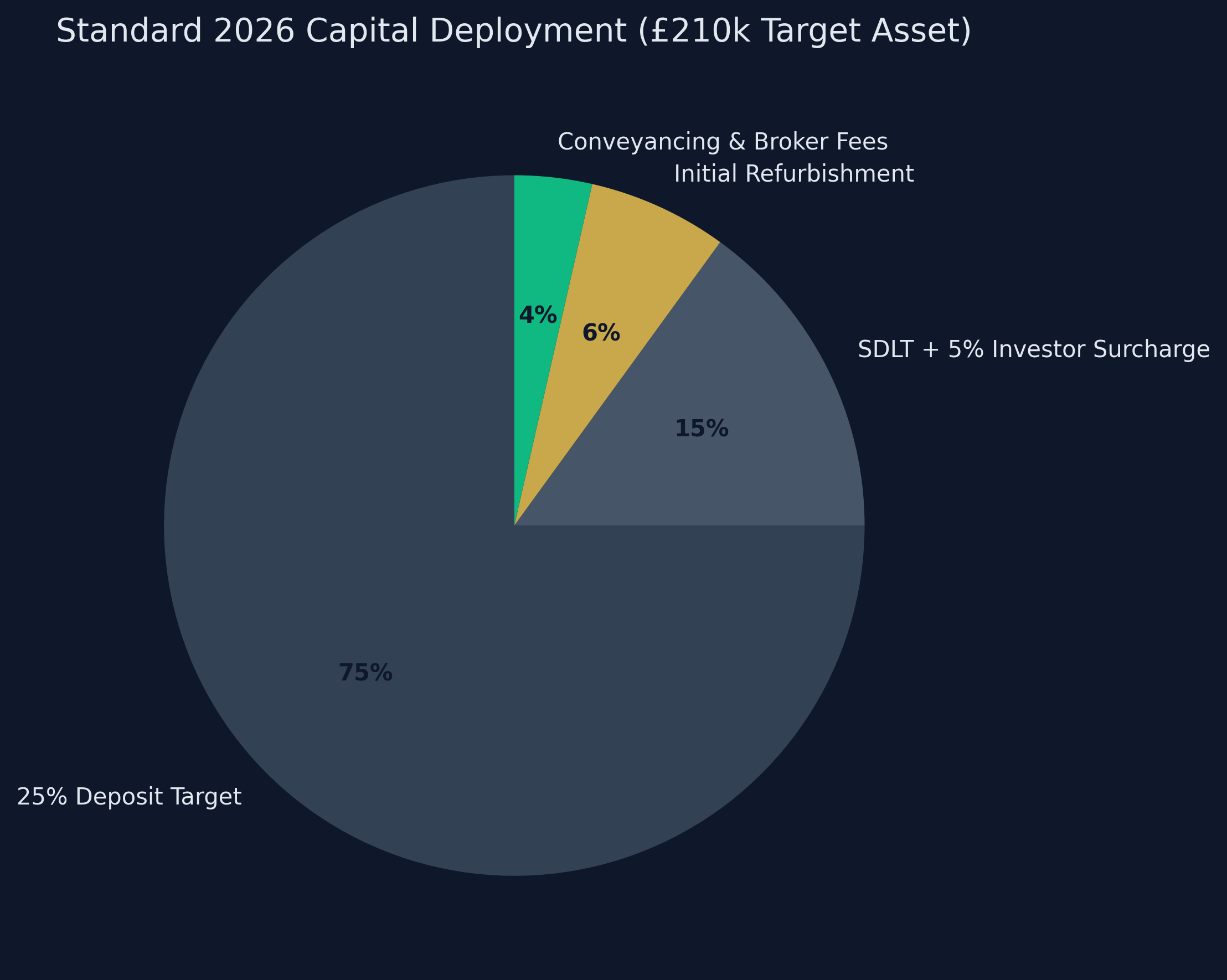

The Strategy: A standard 3-bedroom semi-detached Single Let. The Location: The West Midlands (Birmingham Commuter Belt). The Purchase Price: £210,000.

The Total Capital Deployed (Your Cash Outlay):

- 75% LTV Mortgage Deposit: £52,500

- Stamp Duty (SDLT + 5% Investor Surcharge): £10,500

- Legal, Broker, and Valuation Fees: £2,500

- Initial Cosmetic Refurbishment (Paint, Carpets): £4,500

- Total Initial Cash Deployed: £70,000

The Operational Model (Annual Cash Flow):

- Gross Rent: £1,300 per month (£15,600 annually)

- Target Gross Yield: 7.4%

- Subtract: 5.0% Mortgage Interest on £157,500 Debt = -£7,875

- Subtract: 10% Agent Management Fee (+ VAT) = -£1,872

- Subtract: Maintenance / Void Buffer (7%) = -£1,092

- Subtract: Landlord Insurance = -£350

- True Net Profit: £4,411 annually (£367 per month)

Calculating the True ROI

You deployed £70,000 in hard cash. You receive £4,411 in true, post-expense net profit every single year. Your Cash-on-Cash Return (ROI) is mathematically 6.3%.

Crucially, an aggressive 6.3% cash return is achieved without factoring in a single penny of capital growth.

If the property appreciates at a highly conservative UK historical average of 4% annually, that £210,000 asset generates £8,400 in hidden, untaxed equity growth in Year 1. Combine that invisible equity extraction with your £4,411 liquid cash flow, and your holistic return on your £70,000 deployed cash exceeds 18% in the first 12 months. Is buy to let property worth it uk? When the underlying mathematics are properly optimized and respected, it remains unbeatably lucrative.

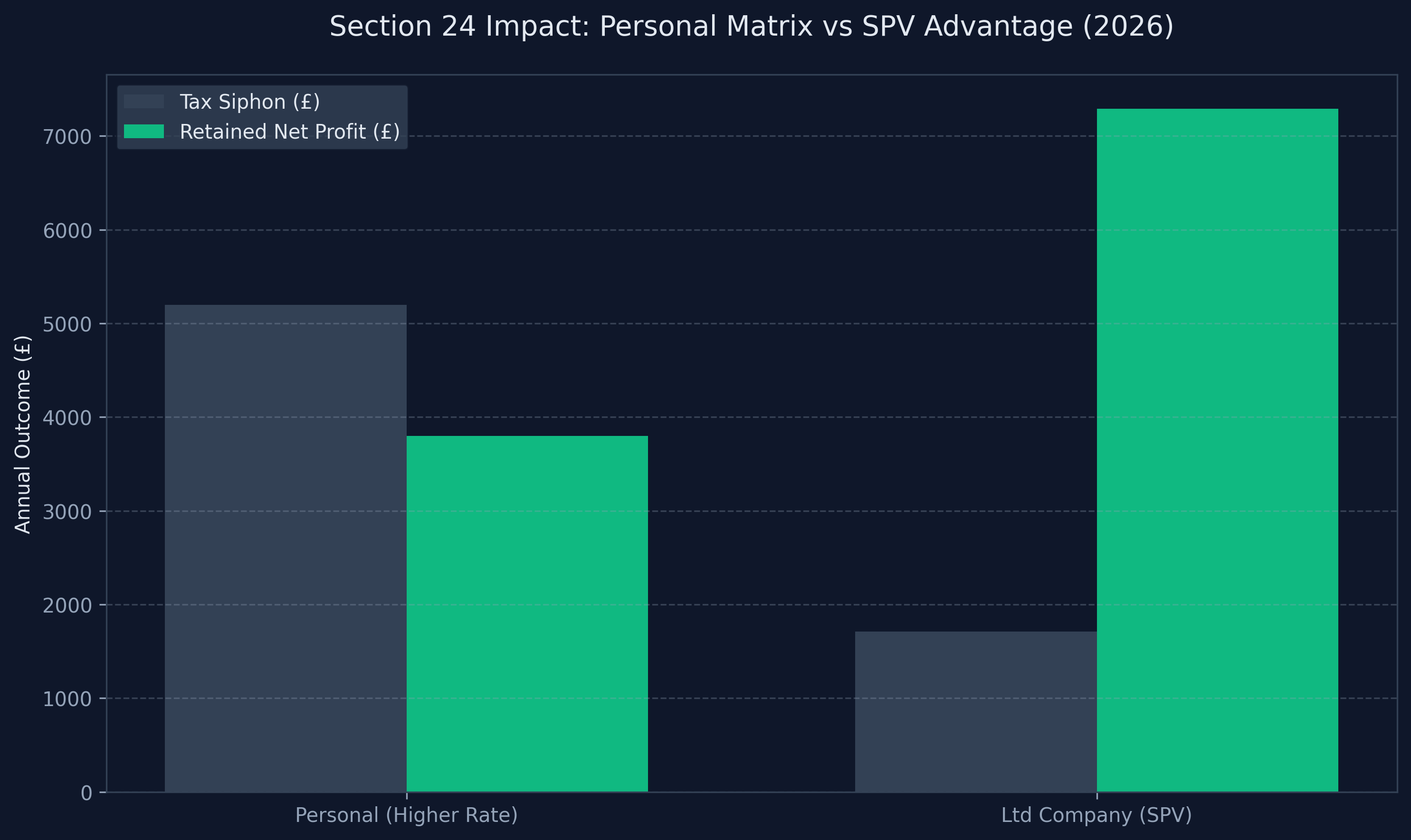

4. The Antidote to Taxation: The SPV Limited Company

If you are buying property in your personal name in 2026, you are fundamentally executing a flawed business plan. The total paradigm shift in modern property investment is the aggressive movement toward corporatization via Special Purpose Vehicles (SPVs).

An SPV is simply a standard UK Limited Company created for the singular, dedicated purpose of holding and managing real property. Currently, over 80% of all new commercial buy-to-let mortgage applications in the UK are processed through Limited Company structures.

Why You Must Invest Through an SPV:

- Evading Section 24: Because an SPV is a legally registered trading entity, HMRC recognizes it as a genuine business. This allows the SPV to deduct 100% of its mortgage interest payments against its gross rental income before any profit is declared. This instantly rescues properties that would be cash-negative in a personal name and makes them highly profitable again.

- Corporation Tax Limits: A higher-rate taxpayer loses 40% to 45% of their personal rental income to the state. An SPV pays standard UK Corporation Tax on its profits—which peaks at 25% but frequently sits at 19% for smaller, expanding portfolios. That massive tax gap is retained directly within your business.

- The Reinvestment Snowball: The greatest advantage of the SPV is operating it as an isolated wealth vault. If you leave your rental profits inside the company rather than drawing them as personal dividends, you do not pay personal income tax. You can leverage that retained profit heavily, allowing you to build your deposit for property number two, three, and four at a vastly accelerated rate.

- Generational Structuring: Transferring a £2M property portfolio to your children triggered massive Inheritance Tax (IHT) liabilities historically. Moving shares within a Limited Company via smart trust planning and directorship allocations allows for a significantly smoother, hyper-tax-efficient transfer of generational wealth.

5. Identifying the Winning Asset Classes in 2026

When investors ask "is buy to let property worth it uk," the secondary, arguably more important question must be: What exactly should I buy? The answer relies entirely on understanding regional arbitrage and distinct asset strategies.

The Foundational Single-Let (The North and Midlands)

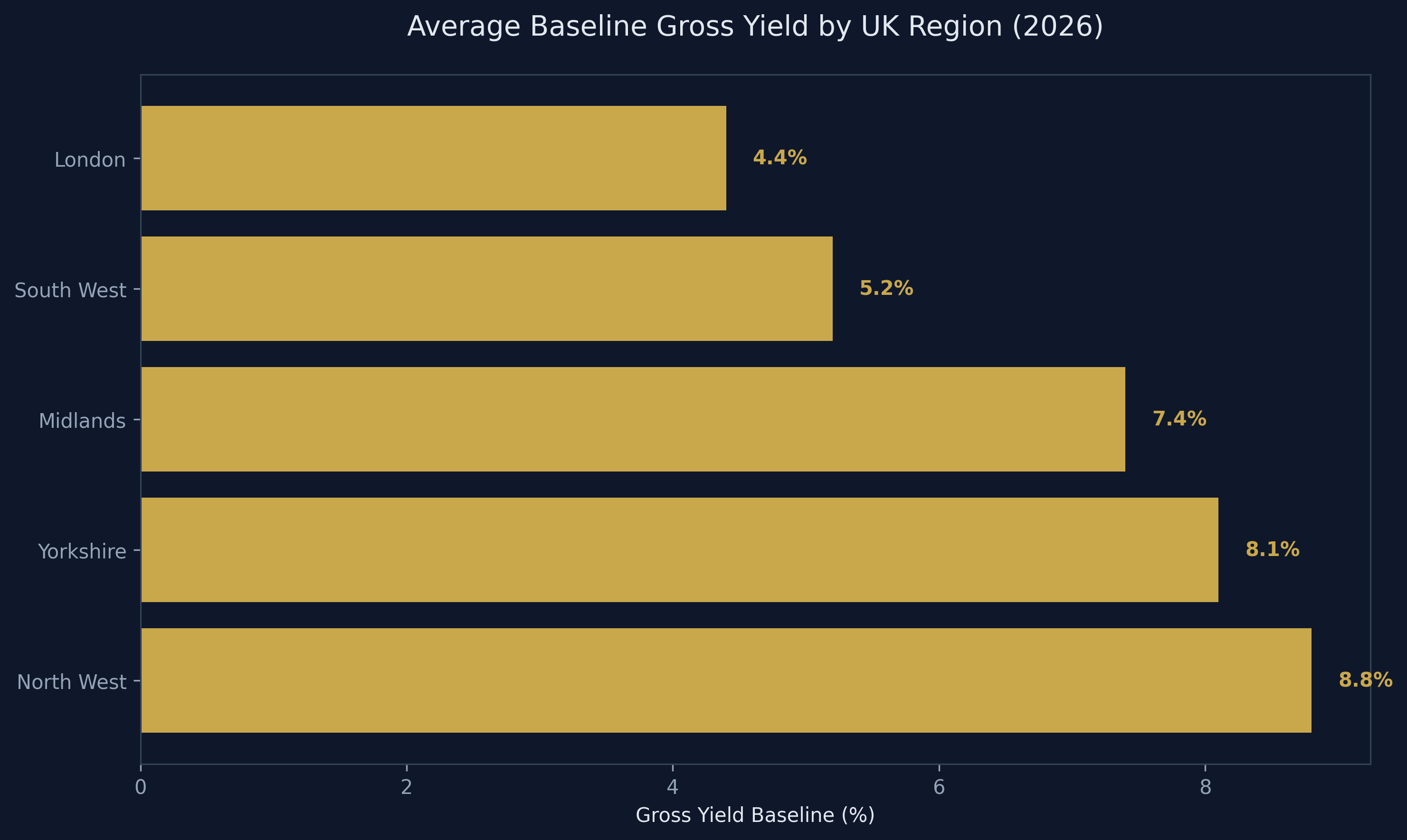

The mathematical example provided earlier relies on a traditional Single-Let property located outside of London. The Northern Powerhouse regeneration zones (Manchester, Liverpool, Leeds) and the West Midlands offer the holy grail of property investment: low entry-price barriers directly coupled with structurally robust rental demand. Acquiring 3-bedroom, ex-local authority semi-detached housing in these zones represents the lowest-risk methodology for establishing a reliable 6% to 8% gross yield portfolio with zero void periods.

Houses in Multiple Occupation (HMOs)

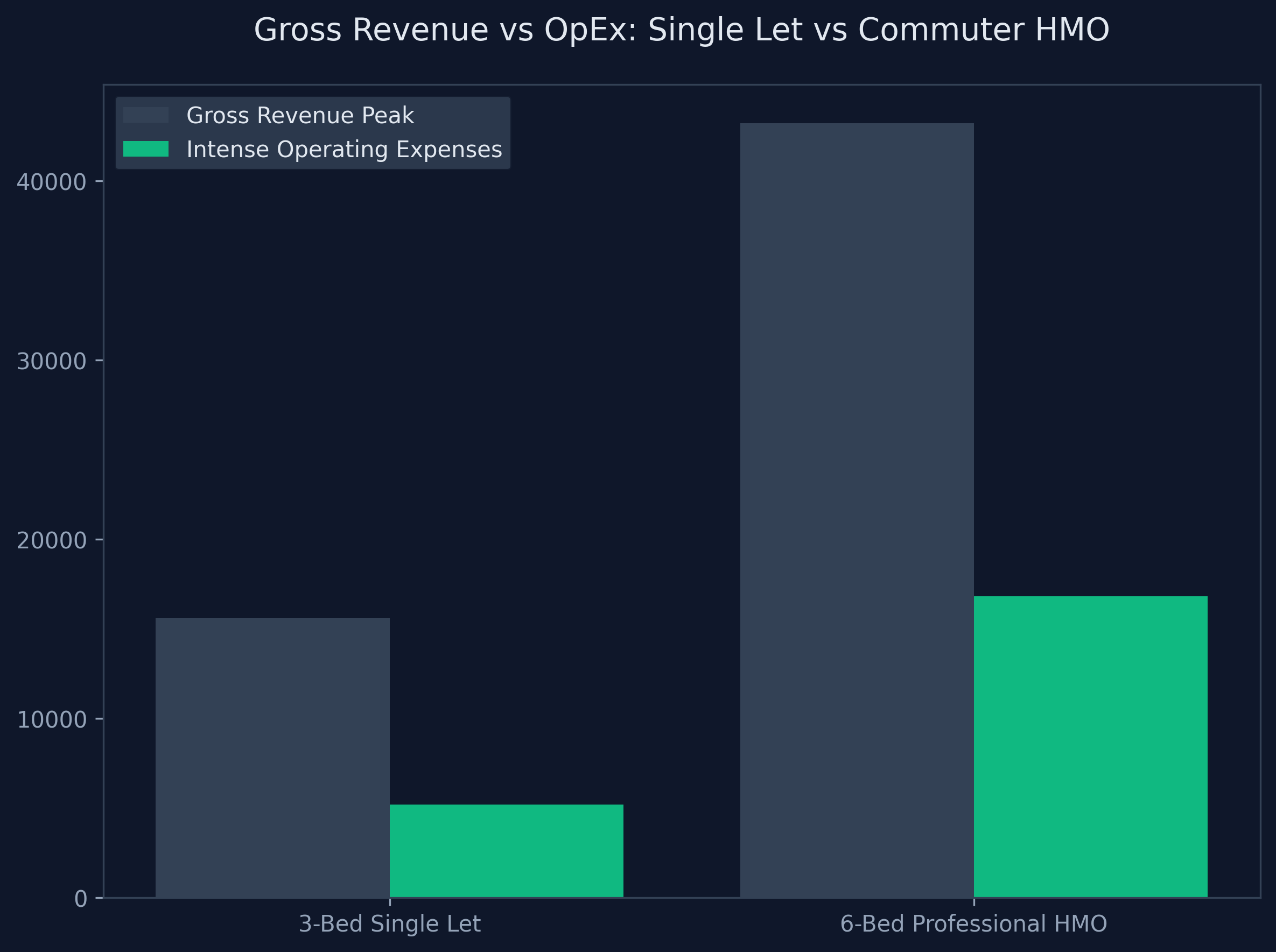

If you require aggressive, accelerated cash flow to replace your primary income, you must transition from standard residential letting into quasi-commercial hospitality: the HMO. By acquiring a large property and renting out individual bedrooms (typically 4 to 6 units per house) to young professionals or students, you aggressively monetize the asset's physical footprint, frequently driving gross yields beyond 10% to 14%.

The Catch: Operating an HMO requires heavy, brutal operational expenditure (OpEx). The landlord is legally mandated to cover all utilities (gas, electricity, water, ultra-fast broadband), council tax, commercial fire safety compliance, and stringent local authority licensing. It transforms passive investing into active management.

The Serviced Accommodation (Short-Term Let) Pivot

The Airbnb revolution has fundamentally altered the yield matrix. Clever investors are taking standard apartments in city centers, tourism hotspots, or adjacent to major hospitals, and renting them on a nightly basis to contractors, traveling nurses, and weekend tourists. An apartment that generates £1,000 per month on an Assured Shorthold Tenancy (AST) might generate £3,000 per month on the short-term market.

Like the HMO, this model forces catastrophic operational expenses onto the landlord—constant professional cleaning fees, linen services, massive utility burn, and hefty platform commissions (15% to 20%). The model is highly lucrative but deeply vulnerable to sudden localized regulatory crackdowns (such as aggressive 90-day London caps).

6. The Fatal Mistakes: How to Destroy Your Yield

If the data proves that buy-to-let remains profitable, why do so many landlords fail and exit the industry? Because they execute terrible deals rooted in emotional speculation rather than cold mathematics.

Fatal Error 1: Buying in Central London. Yield requires a localized imbalance between the capital asset price and the rental income. In London, global capital has hyper-inflated property values far beyond what localized wages can support in rent. Buying a £600,000 flat in Zone 2 that generates £2,200 a month will result in a gross yield of roughly 4.4%. Once you factor in a 5% mortgage, service charges, and management fees, you are actively losing hundreds of pounds every month. Investing in London is a pure wealth preservation speculation play; it is terrible for building cash flow.

Fatal Error 2: Ignoring Ground Rent and Service Charges. Investors frequently purchase beautiful new-build leasehold apartments, dazzled by the projected gross rent, entirely forgetting the freeholder. Major city center apartments often carry £2,000 to £4,000 annual service charges that inflate heavily with the Retail Price Index (RPI). You must violently deduct these fixed costs from your gross rent before running your yield calculations. A brilliant 7% gross yield can instantly become a sub-3% net yield once the management company issues its invoice.

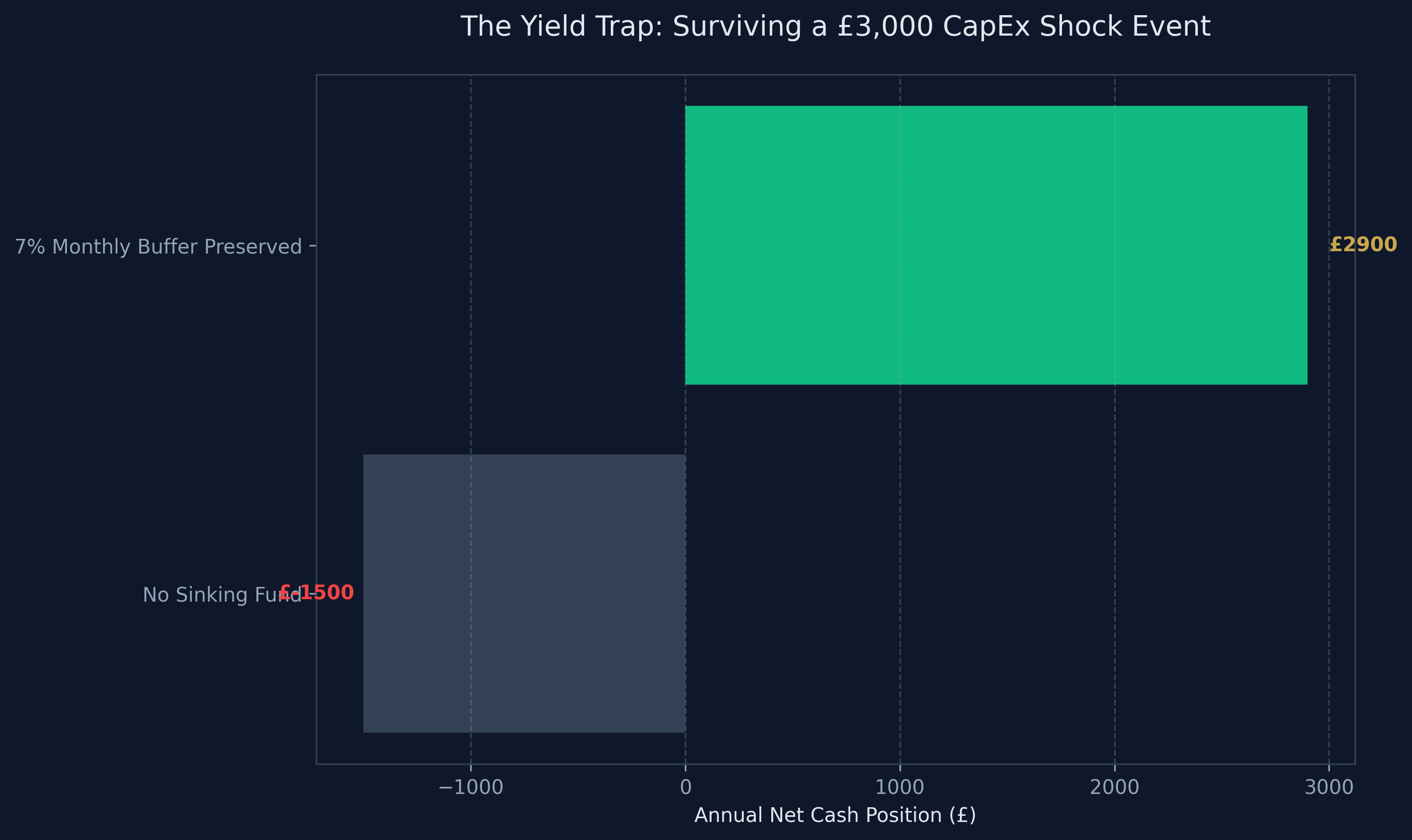

Fatal Error 3: Failing to Build a Sinking Fund. The spreadsheet isn't reality. A newly refurbished property will suffer damage. You must mathematically bake a 5% to 8% monthly maintenance deduction into your model from day one. Do not treat 100% of your net cash flow as disposable income. When the boiler dies in December, costing £2,500 to replace, a landlord without a sinking fund is forced into expensive credit card debt, instantly destroying a year of hard-earned yield.

The Final Verdict on 2026 Buy-to-Let

Is buy to let property worth it in the UK? Without a moment's hesitation: Yes.

Property remains the single most legally weaponized, highly leveraged asset class available to the UK retail investor. It provides a unique combination of aggressive monthly cash flow, invisible inflation arbitrage, and deep generational wealth preservation.

However, the barrier to entry has structurally increased. The market relies entirely on ruthless mathematical optimization. If you are willing to operate as a hybridized commercial entity—leveraging SPV structures to shield your revenue, hunting distressed midlands assets for immediate equity capture, modeling rigid 75% LTV debt tranches, and demanding minimum 7.5% gross yields—then 2026 represents arguably the greatest buyer's market of the current decade.

Execute the math, remove the emotion, and buy the brick.

Essential Property Deal Analysis: Deep Dive FAQ

Navigating the granular intricacies of a modern UK property acquisition requires specialized insight. To definitively assess "is buy to let property worth it uk," we aggressively analyze the most common friction points encountered by active 2026 investors below.

Do I Have to Pay the 5% Stamp Duty Surcharge?

For the overwhelming majority of standard residential buy-to-let acquisitions, yes, the 3% (recently increased to 5% by emergency budget actions) Additional Properties surcharge is a brutal, unavoidable reality. It applies to the entire purchase price and completely removes the standard nil-rate band utilized by owner-occupiers. If an investor attempts to use a standard stamp duty buy to let calculator, they will quickly discover that sophisticated corporate structuring (like an SPV) does not offer a bypass to this domestic levy.

The only viable methods of eradicating the surcharge are structurally pivoting into distinct asset classes:

- True Commercial Real Estate: Purchasing retail units, industrial warehouses, or office spacing relies on commercial SDLT scaling, ignoring residential surcharges.

- Mixed-Use Properties: Acquiring a property encompassing both commercial and residential elements (e.g., a high-street shop with two flats directly above it). The entire transaction is taxed at the drastically more favorable commercial SDLT rate.

- The Rule of Six: If an investor rapidly acquires an entire block of flats containing six or more independent localized residential units in a single bulk transaction, HMRC legally reclassifies the acquisition as a commercial transaction, eradicating the residential surcharge completely.

Why is the BRRR Model So Difficult in 2026?

The BRRR (Buy, Refurbish, Refinance, Rent) methodology relies entirely on the velocity of capital. The faster you can force value into an asset and extract your initial cash via a revaluation mortgage, the higher your holistic ROI. In 2026, the BRRR model faces severe systemic friction:

- The Valuation Gap: High-street valuers have become incredibly conservative. You might inject £25,000 of heavy capital expenditure into an asset, only for the bank's surveyor to 'down-value' your projected End Value by £15,000, actively trapping a massive tranche of your liquid cash inside the deal permanently.

- The Six-Month Rule: Almost all major UK lenders strictly enforce the 'Six Month CML Rule'. They will arbitrarily decline any application to refinance an asset if you currently have owned it for less than 180 days. This brutally destroys capital velocity, forcing investors to sit on expensive bridging finance (costing ~1% per month) while waiting for the arbitrary clock to run out.

- Material and Labor Inflation: The cost of raw materials and skilled tradesmen has skyrocketed, destroying the tight margins BRRR investors previously relied upon.

Are Interest-Only Mortgages Dangerous?

For standard owner-occupiers, an interest-only mortgage is a high-risk gamble. For professional buy-to-let investors, it is an absolute mathematical necessity. Utilizing a repayment mortgage brutally destroys your monthly cash flow, significantly lowering your holistic Net Yield. Yes, you are slowly paying down the capital base of the loan, but you are trapping your profits in an illiquid asset. An interest-only mortgage maximizes your monthly liquid cash flow. Professional investors retain this cash flow to aggressively build a deposit for their next localized acquisition. They rely on localized inflation and long-term 15-year macroeconomic capital appreciation to effectively 'pay down' the real-world value of the debt, rather than physical cash repayments.

Should I Self-Manage or Use a Letting Agent?

The decision to self-manage property hinges entirely on how you value your own theoretical hourly rate. A standard UK letting agent charges 10% to 15% (+ VAT) of the gross monthly rent to fully manage an asset. For a property generating £1,200 pcm, that represents roughly £1,700 to £2,500 of annual lost yield.

However, self-management transforms a passive investment into a highly active second job. If a boiler explodes at 2 AM on a Sunday in January, the tenant calls you. If the tenant abruptly stops paying rent, you are legally responsible for navigating the deeply complex, six-month-long Section 21 / Section 8 eviction court procedures. If your primary career generates £50+ per hour, attempting to save £150 a month by self-managing an asset is a catastrophic misallocation of your time. Outsource the friction; retain the macro-strategy.

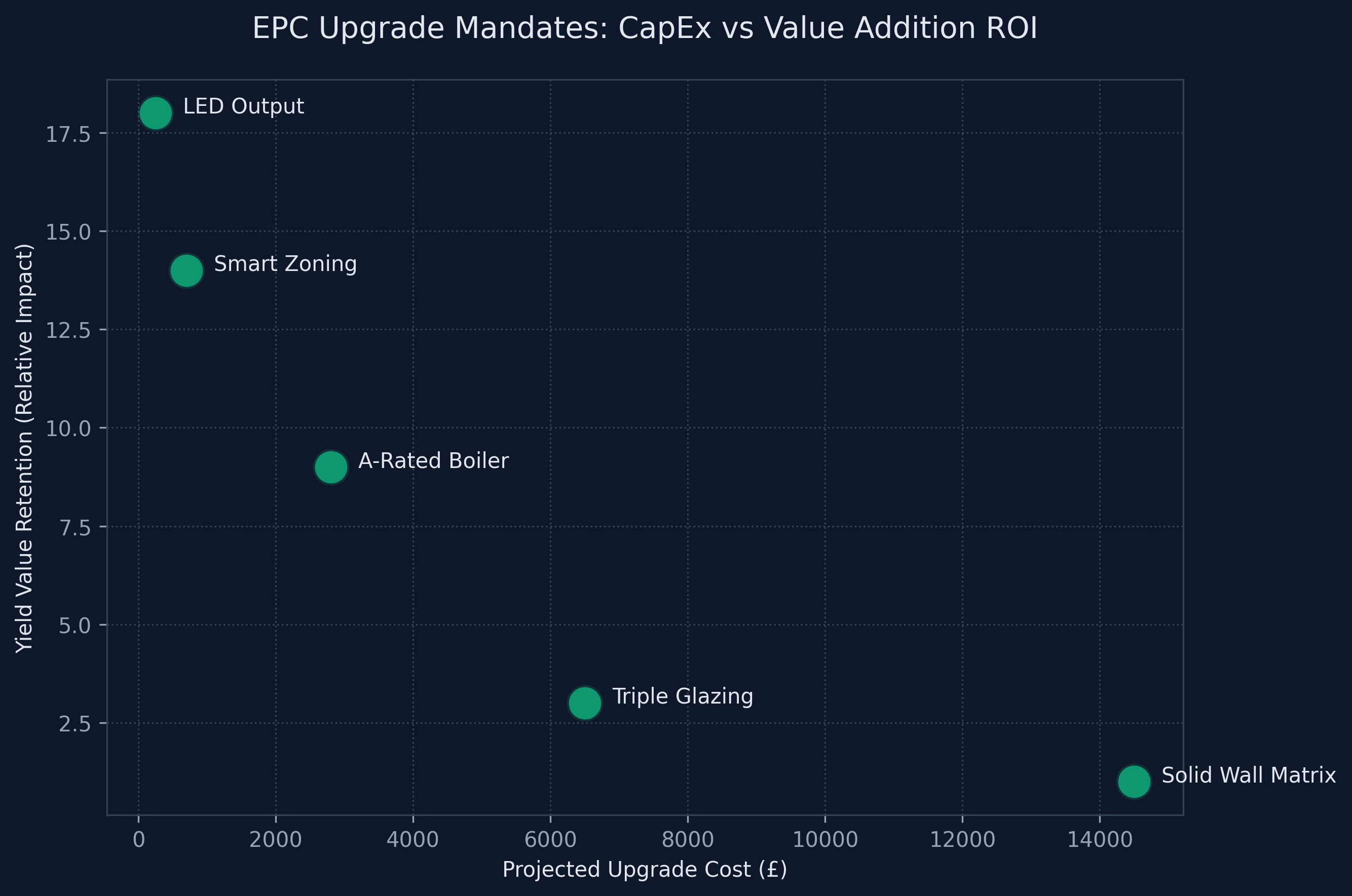

Does EPC Rating Actually Alter Capital Valuations?

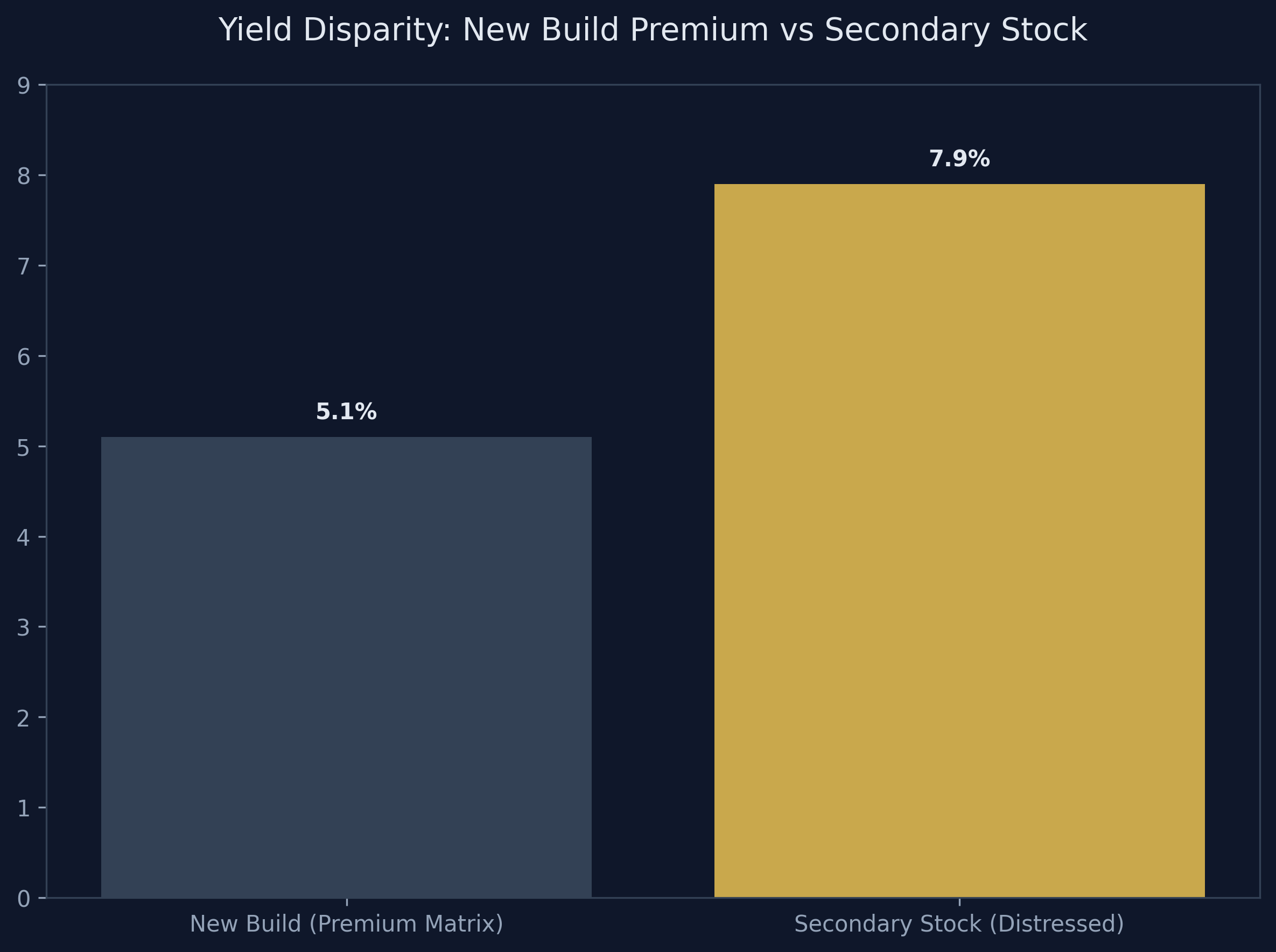

Absolutely, and the market penalty for non-compliance is only intensifying. Under impending government mandates driving the Minimum Energy Efficiency Standards (MEES) toward a definitive 'C' rating, an asset languishing at an 'E' or 'F' is effectively distressed stock. Savvy corporate investors explicitly hunt these inefficient properties, utilizing the horrifying prospect of a £15,000 retrofitting bill to aggressively negotiate the vendor down 15% below True Market Value.

Conversely, acquiring a structurally efficient 'B' or 'A' rated passive income property grants the landlord access to specialized 'Green Mortgage' products. These commercial lenders offer preferential, heavily discounted interest rates as an ESG compliance reward, significantly expanding your localized cash flow simply because the asset is environmentally optimized.

What is the "Yield Trap" on Cheap Properties?

When aggressively screening UK property portals utilizing a yield calculator, novice investors frequently spot £60,000 terraced houses generating £550 pcm in rent, yielding a massive 11% Gross Return.

This is the classic Yield Trap. Extremely cheap housing stock is fundamentally located in areas suffering high localized unemployment, systemic structural deprivation, and crumbling heavy industry. The mathematical reality of the Yield Trap is catastrophic:

- Devastating Void Periods: Tenant turnover is incredibly high, and tenant fiscal stability is incredibly low. You might face 3 months of consecutive voids per year.

- Disproportionate CapEx: A £4,000 new roof costs the exact same physical price whether the house is worth £60,000 or £600,000. On a £60,000 asset, that single repair violently annihilates 18 months of net profit.

- Negative Capital Growth: You are buying an asset in a structurally failing demographic hub. The capital value will stagnate or actively decay over a 10-year term, destroying your holistic ROI.

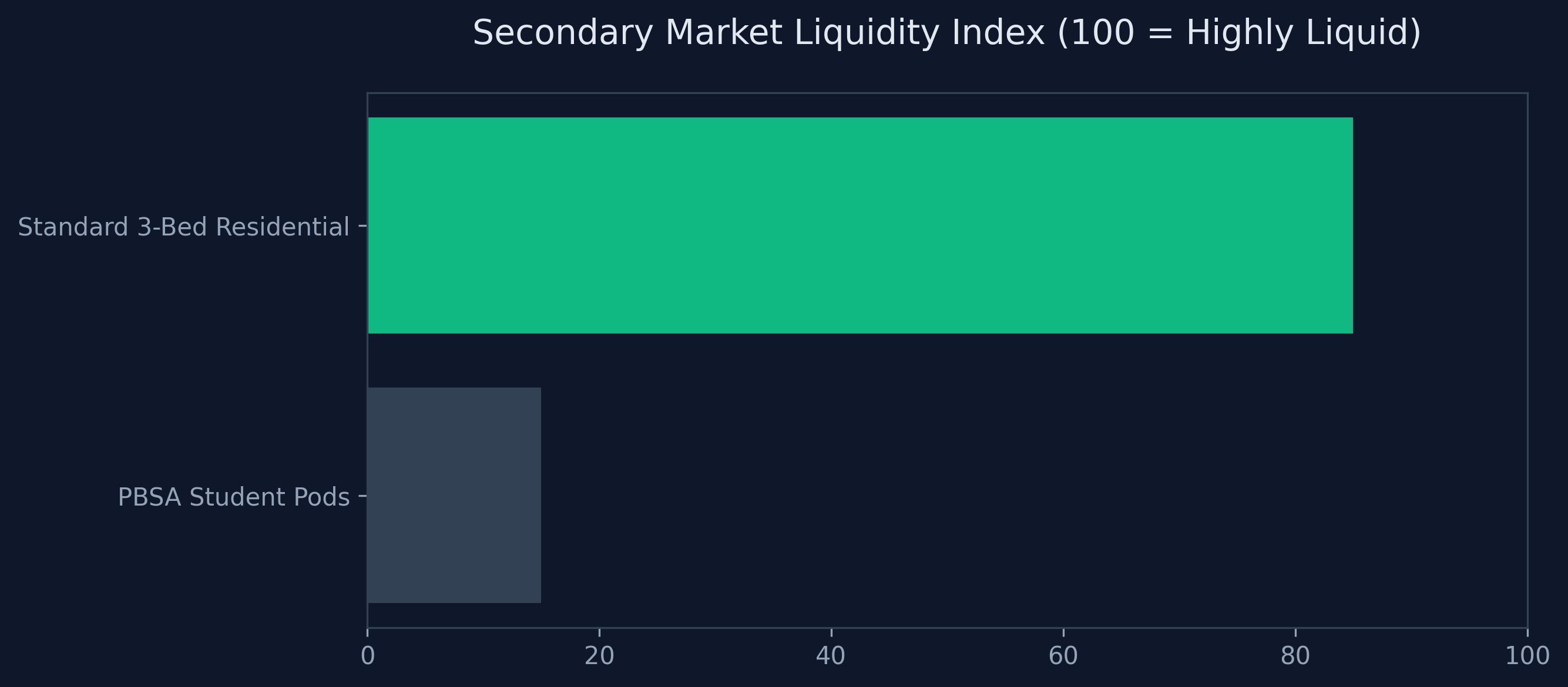

Should I Invest in Student Accommodation (PBSA)?

Purpose-Built Student Accommodation (PBSA)—often sold as 'pods' or localized micro-apartments in major university cities—is fiercely marketed by developers as offering 'Guaranteed 8% Net Yields for 5 Years'.

Professional investors avoid PBSA violently for one critical reason: Total lack of secondary market liquidity. Standard residential properties can be sold to other landlords, first-time buyers, downgrading retirees, or expanding families. A PBSA 'pod' can only be sold to another investor at an extreme discount. You do not own the land; you own a highly restrictive leasehold slice of a commercial hotel. When the developer’s 'guaranteed yield' period expires, you are at the absolute mercy of the centralized management company's aggressive fee structures, trapping your capital in an illiquid asset that banks refuse to mortgage.

Final Strategy: Building the 2026 Portfolio

An investor constantly asking "is buy to let property worth it uk" is looking for reassurance that the easy days will return. They won't. The absolute blueprint for 2026 is hyper-professionalization. You must decouple your emotions from the physical brick, incorporate your portfolio via a Limited Company SPV to violently suppress your tax liability, and pivot away from high-value Southern commuting belts to chase structurally strong yields in the Northern regeneration corridors. Lock down reliable 5-year fixed debt, aggressively build a 10% cash sinking fund, and trust the mathematics over the newspaper headlines.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →