If you are systematically hunting for the highest gross yield property in the UK, buying at retail price on Rightmove is mathematical suicide. The 2026 macro-environment is choked with highly inflated asking prices, elevated base interest rates, and an army of amateur investors inflating the open market.

To protect your capital and inject instant, Day-1 equity into your portfolio, you must execute the best finding below market value (BMV) acquisition strategies. But true BMV is not passively handed to you by an estate agent. It is aggressively engineered.

Finding properties significantly under their core valuation requires an institutional-grade sourcing pipeline. You must intercept distressed, unencumbered, or structurally problematic assets before they ever hit the open market. This 3,000-word tactical manual decodes the exact Direct-to-Vendor pipelines, PropTech data-scraping algorithms, and auction frameworks utilized by elite sourcing syndicates in 2026.

What Actually Constitutes "Below Market Value" (BMV)?

Before we deploy capital into marketing or data acquisition, we must definitively kill the biggest myth in property investment: A cheap property is not a Below Market Value property.

If a 3-bedroom semi-detached house in a brutalized postcode with extreme crime rates and failing schools is listed at £65,000 while the national average is £285,000, that property is not BMV. It is simply cheap, accurately reflecting the localized lack of demand. It will yield poorly, suffer extreme void periods, and experience zero capital growth.

The True Definition of BMV

A property is truly Below Market Value when it is acquired for a price functionally lower than its exact, true open market valuation (if placed on the open market in pristine condition with a standard 12-week marketing window).

True BMV is entirely derived from Vendor Distress. The property itself is fine (or has curable architectural distress, ideal for the BRRRR Strategy); it is the human owner who is in distress.

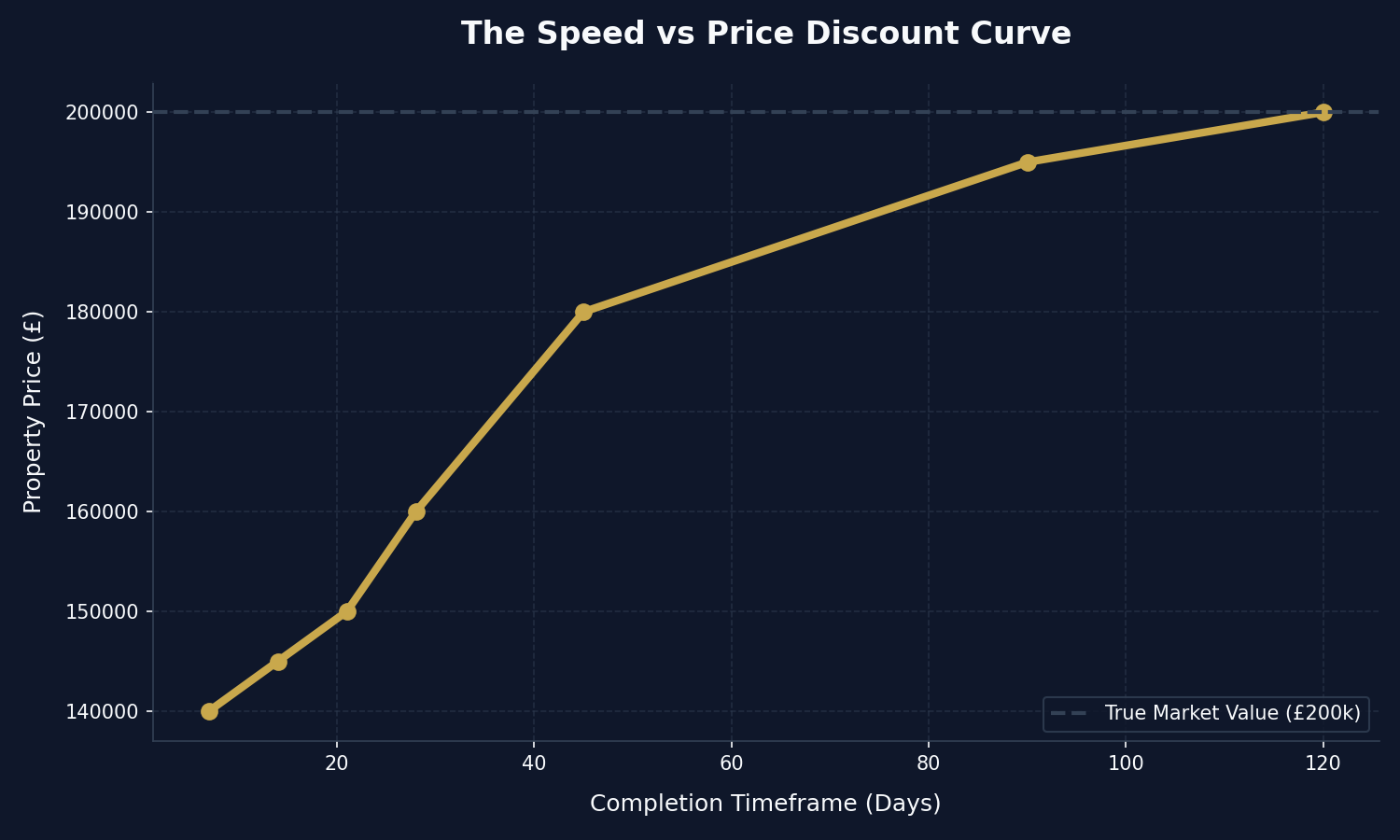

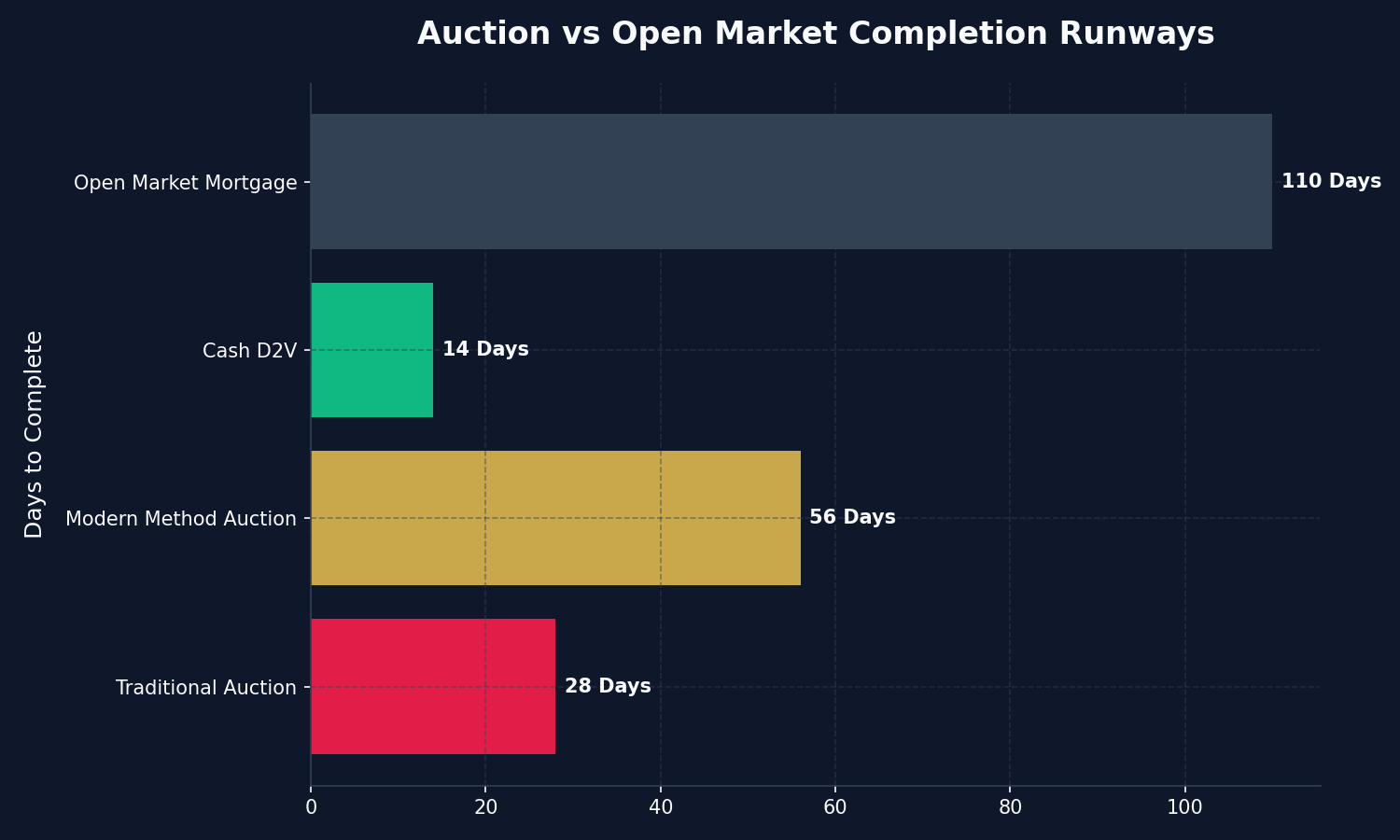

We are trading Speed and Certainty for Price. The vendor is willing to surrender £30,000 in equity because you can complete the purchase in 14 days using bridging finance, rescuing them from imminent bank repossession, a collapsing chain, or severe liquid capital starvation.

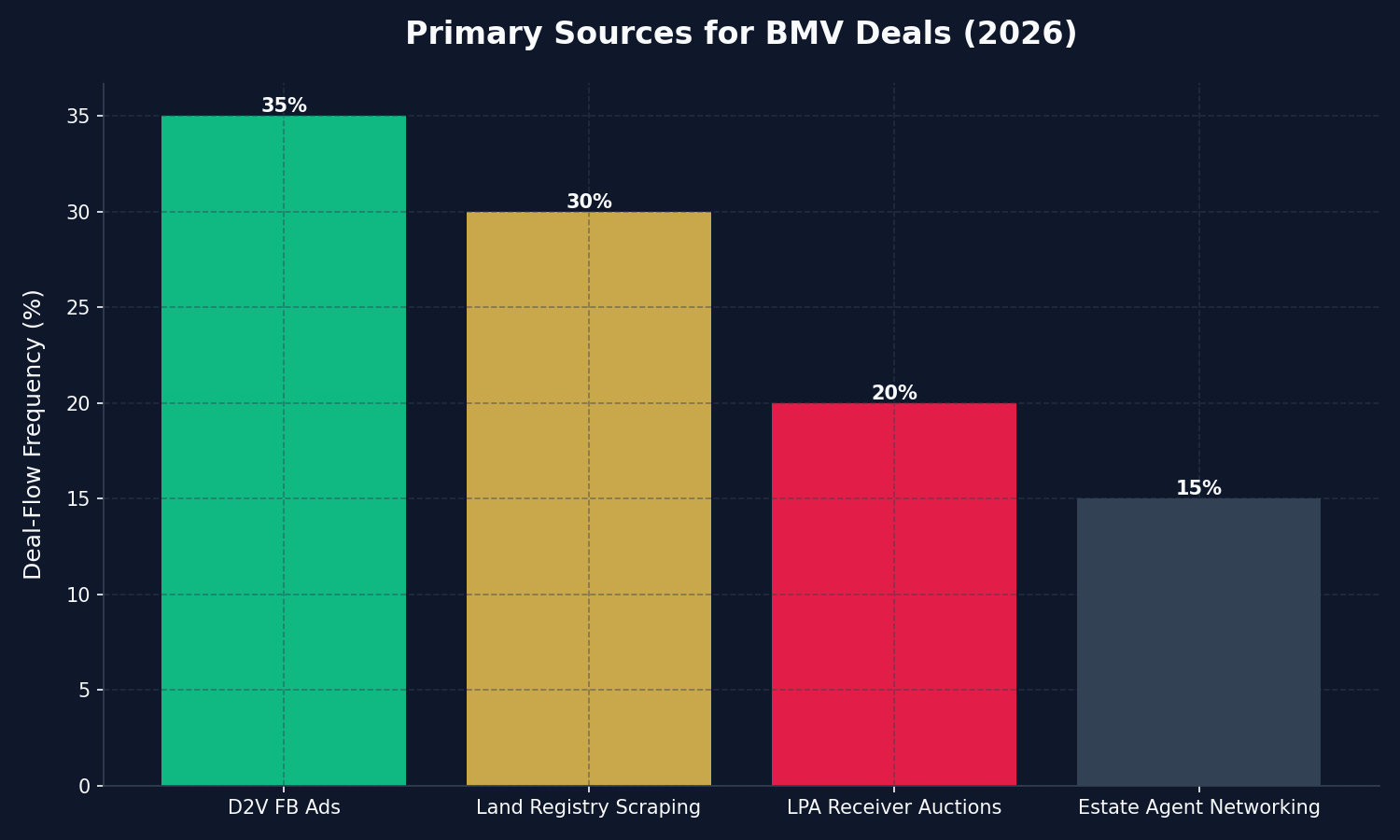

Strategy 1: Direct-to-Vendor (D2V) Marketing

The absolute best way of finding below market value property is to build your own proprietary deal-flow pipeline. You must intercept the vendor long before they contact a high-street estate agent.

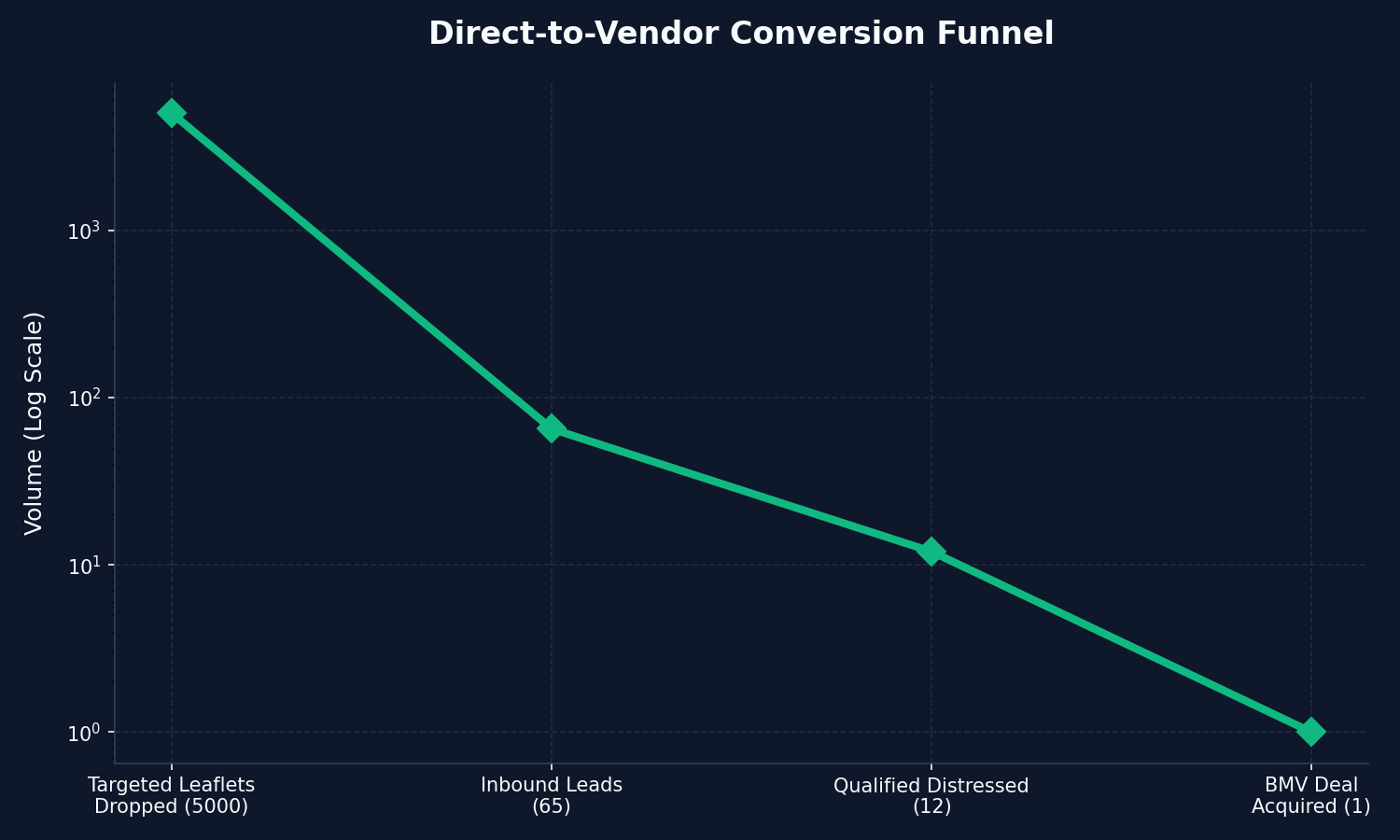

Physical Leaflet Dropping campaigns

While it sounds archaic in 2026, physical leaflet dropping remains devastatingly effective if executed with algorithmic precision. However, you cannot randomly drop 10,000 leaflets across a city. The ROI is negative.

You must utilize demographic cluster plotting. Target areas with high concentrations of properties built between 1950 and 1980 (which often require modernization and are currently occupied by elderly owners facing downsizing) or dense concentrations of basic, unrefurbished Houses in Multiple Occupation (HMOs) operated by tired, aging landlords facing brutal Renters' Rights Act compliance costs.

Your leaflet copy must be brutally direct, addressing their exact pain point:

"Tired of Section 24 Taxes and new EPC Regulations? I am a local cash buyer. I will buy your property in 21 days. No agent fees. No viewings. Guaranteed completion."

Targeted Social Media Lead Generation

Facebook and Instagram Lead Generation ads offer surgical precision for hunting distressed landlords.

By leveraging the Facebook Pixel, you can target local demographics who exhibit behaviors correlated with landlord exhaustion: searching for "how to evict a tenant in 2026", "capital gains tax calculator", or "EPC rating upgrades costs."

We run automated campaigns offering a free "2026 Landlord Exit Strategy Guide". Once they download the guide, they enter an automated email sequence that systematically positions us as the cash-ready savior for their depreciating, problematic portfolio.

Strategy 2: Modern PropTech Data Scraping (The Unencumbered Pipeline)

Relying on organic D2V leads is slow. The elite 2026 strategy for finding below market value property relies on aggressive data analytics, primarily scraping Land Registry and Title Deed APIs.

The "Absentee Landlord" Protocol

To secure a BMV deal, you need an owner who has immense equity (so they have the mathematical cushion to offer a discount) and zero emotional attachment to the asset.

Using advanced PropTech mapping tools (like PropertyData or Nimbus Maps), you can scrape the UK Land Registry to filter for:

- Unencumbered Properties: Homes purchased prior to 2005 (meaning the 25-year mortgage is fully paid off) or bought outright for cash.

- Absentee Owners: The registered Title Deed ownership address is different from the physical property address (proving it is a rental or second home).

- Distance Factor: The owner lives more than 100 miles away from the asset.

When a landlord lives 150 miles away, has zero mortgage debt, and receives an emergency call that the boiler has exploded causing £5,000 in water damage, they frequently decide they have had enough. Because they have 100% equity, they will gladly sell a £200,000 property for £160,000 just to instantly cleanly sever the headache. Writing highly targeted, bespoke direct mail letters to these specific Title Deed addresses is the highest converting BMV acquisition channel available to professional property syndicates.

Strategy 3: The Distressed Auction and Receivership Market

When D2V marketing fails, we turn to the brutal efficiency of the auction room. Property auctions are fundamentally designed to achieve speed, often forcibly exchanging contracts at heavily reduced BMV prices.

The Traditional Auction Gauntlet

In a traditional auction, when the hammer falls, you have legally exchanged contracts. You must instantly pay a 10% non-refundable deposit and you have precisely 28 days to complete the final 90% balance.

If you fail to complete on day 28, you lose your 10% deposit, and the vendor can sue you for the mathematical difference if they are forced to sell the property to someone else for less.

This insane velocity terrifies amateur retail buyers. Traditional BTL mortgage lenders simply cannot underwrite, value, and approve a mortgage in 28 days. Therefore, the buyer pool is artificially restricted to extreme cash-rich investors or those utilizing aggressive Bridging Finance. Because 90% of the market cannot compete, the hammer frequently falls at 15% to 25% Below Market Value.

Identifying Fixed Charge Receivership Sales (LPA)

The holy grail within the auction catalogue is identifying the LPA (Law of Property Act) Receiver.

When a heavily leveraged landlord mathematically defaults on their commercial mortgage, the bank appoints an LPA receiver. The receiver’s sole legal directive is to liquidate the asset instantly to recover the bank's core debt. They have zero emotional attachment. They do not care if the property was worth £500,000 last year; if the bank is owed £350,000, the receiver will set a reserve price of £360,000 and happily slam the hammer down. Scanning auction legal packs daily for "LPA Receiver" declarations is a guaranteed path to uncovering severe institutional distress.

Strategy 4: Architecturally Distressed Property (The "Ugly" Asset)

Sometimes the human isn't distressed, the brickwork is. Buying structurally compromised assets at a brutal discount and curing the defect is the cornerstone of Property Flipping.

Sub-Standard EPC Regulations

In 2026, the legislative net zero push has weaponized the EPC (Energy Performance Certificate) rating system. It is functionally illegal to rent out a property with an EPC rating of 'E' or below without severe exemptions.

Thousands of elderly "accidental landlords" possess vast, uninsulated Victorian terraced housing stock that holds an 'E' rating. Refitting these properties with solid wall insulation, air-source heat pumps, and double glazing can cost £15,000 to £25,000. These landlords refuse to spend the capital and simply want to exit.

By aggressively targeting properties listed specifically with low EPC ratings, investors can aggressively negotiate BMV discounts, absorb the asset, execute a rapid green retrofit, and instantly unlock massive capital appreciation via Green Refinance products.

Strategy 5: Curating Estate Agent Relationships (The Off-Market Desk)

Despite the power of PropTech and direct marketing, highly lucrative BMV deals still flow through traditional high-street estate agents—they just never reach Rightmove.

The "Bottom Drawer" Deals

When an estate agent receives an instruction from a highly distressed vendor (e.g., someone going through a hostile divorce needing a 10-day completion), the agent does not want to waste time paying Rightmove listing fees, photographing the property, and dealing with 40 time-wasting residential buyers requiring 12 weeks of mortgage underwriting.

The agent opens their proverbial "bottom drawer" and immediately calls the three cash-ready, professional investors they know can complete instantly without friction.

To secure your position on that shortlist, you must physically canvas local agents weekly. Provide them with "Proof of Funds" directly from your commercial bridging lender. Assure them that you will retain them to re-sell the property after you calculate the flip margins and execute the refurbishment. If they realize they can double-dip the commission (earning once when you buy, and once when you sell), they will consistently feed you severe BMV deals.

The Risks of BMV Acquisition

Sourcing off-market BMV is highly lucrative, but it is a predatory landscape fraught with intense margin traps.

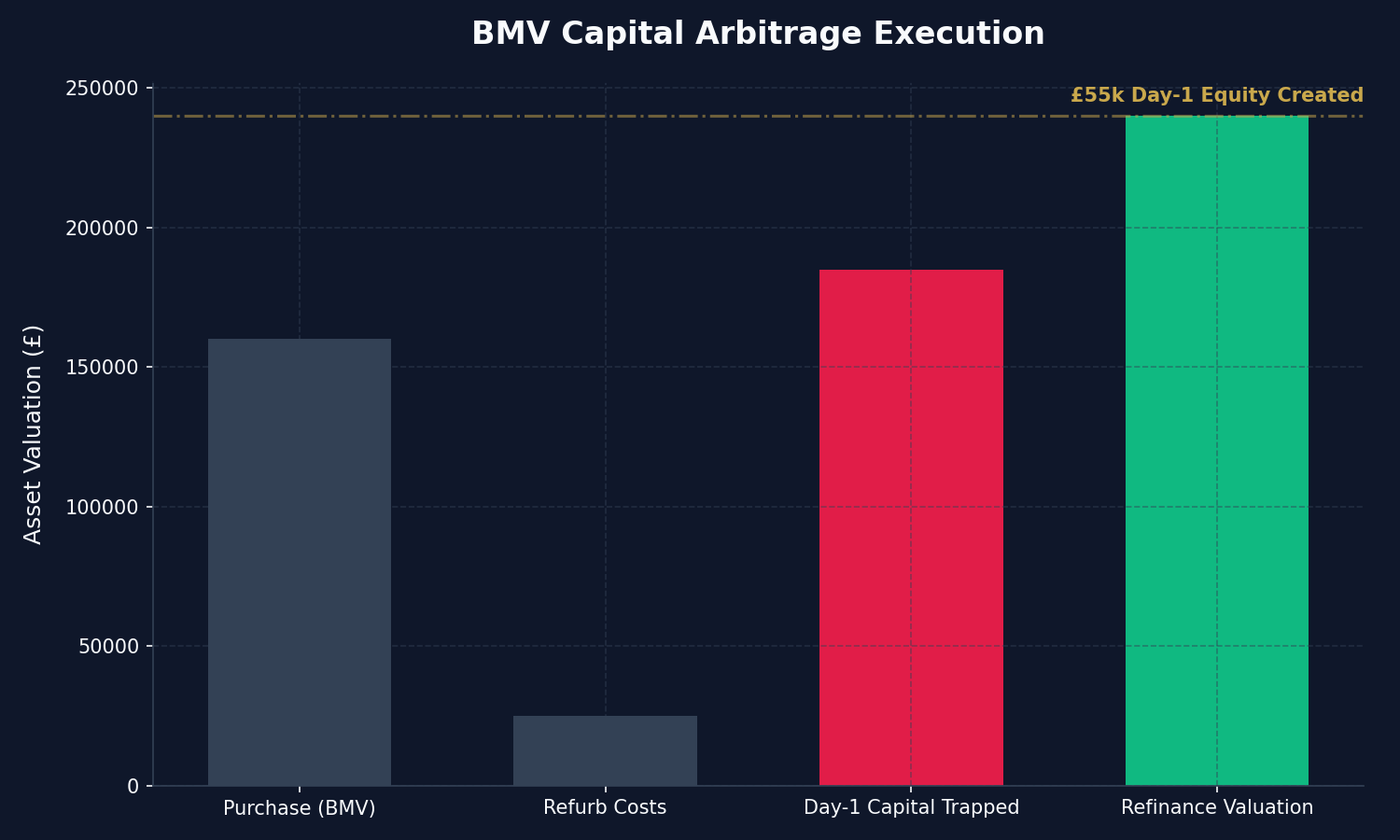

The "Down-Valuation" Threat

If you secure a BMV deal directly from a vendor at £150,000 (true market value £200,000), you intend to use bridging finance to acquire it, and then instantly refinance onto a BTL mortgage at the £200k valuation to pull all your capital out.

However, commercial surveyors in 2026 are ruthlessly defensive. If they see you bought the property 6 months ago for £150,000, and you haven't fundamentally altered the square footage (only adding a lick of paint), they will likely physically "down-value" the refinance back to £150,000 to protect the bank's exposure.

This completely traps your capital in the deal. To successfully unlock the Day-1 BMV equity, you must definitively force appreciation through heavy, structural Permitted Development (PD) rights, changing the fundamental layout of the asset so the surveyor cannot rely on your purchase price as a baseline.

Execution Summary: How to Find BMV Today

To successfully execute the best finding below market value strategies in 2026, you must completely abandon Rightmove and transition your operation into a data-driven acquisition company.

Your daily operating procedure must involve:

- Running automated FB Ads targeting severe landlord pain points (Section 24, EPCs).

- Scraping Land Registry data to identify long-distance, unencumbered landlords.

- Scanning specific auction legal packs for LPA Receiver sales.

- Cultivating deep, incentivized relationships with local estate agency directors.

If you can combine absolute data precision with the deployment speed of commercial bridging finance facilities, the extraction of Day-1 BMV equity is mathematically inevitable.

Ready to deploy? Once you lock in a severely distressed BMV asset, immediately utilize our Property Flipping Yield Calculator to map your exact refurbishment costs, bridging rollover margins, and exit ROI metrics.

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →