Stamp duty is the most visible transaction tax in UK property — and the most politically contentious. This page consolidates every critical stamp duty statistic for 2026, covering current SDLT rates in England and Northern Ireland, LBTT rates in Scotland, LTT rates in Wales, HMRC revenue data, transaction volumes, and the impact of the April 2025 threshold changes on buyers and investors.

Whether you are calculating your own stamp duty bill, advising clients on transaction costs, or analysing fiscal policy, this is the definitive reference.

Last Updated: April 2026 | Next Update: July 2026

Key Stamp Duty Statistics at a Glance

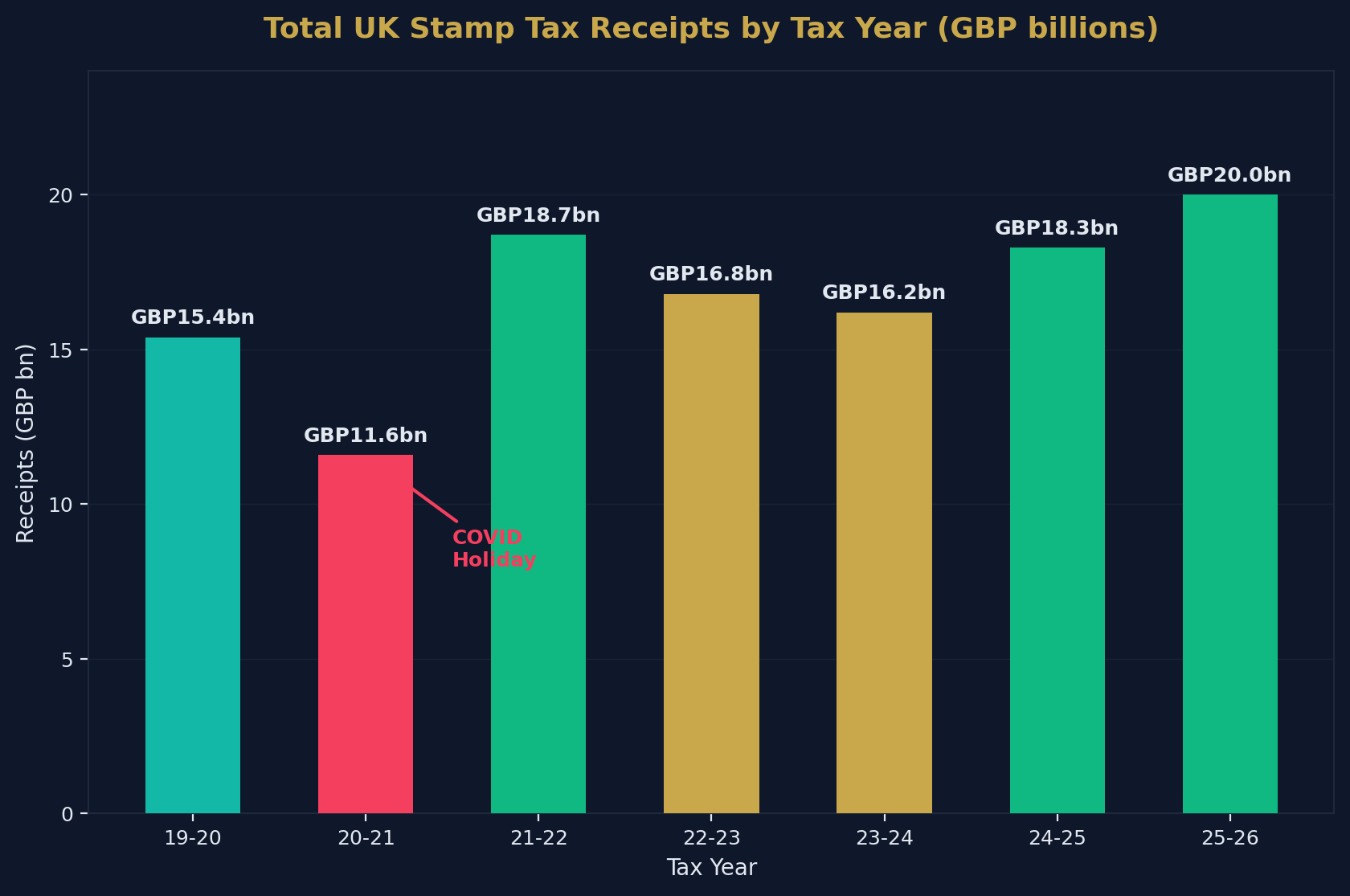

- Total stamp taxes receipts for 2025-26: £20.0 billion (+£1.7bn on prior year).

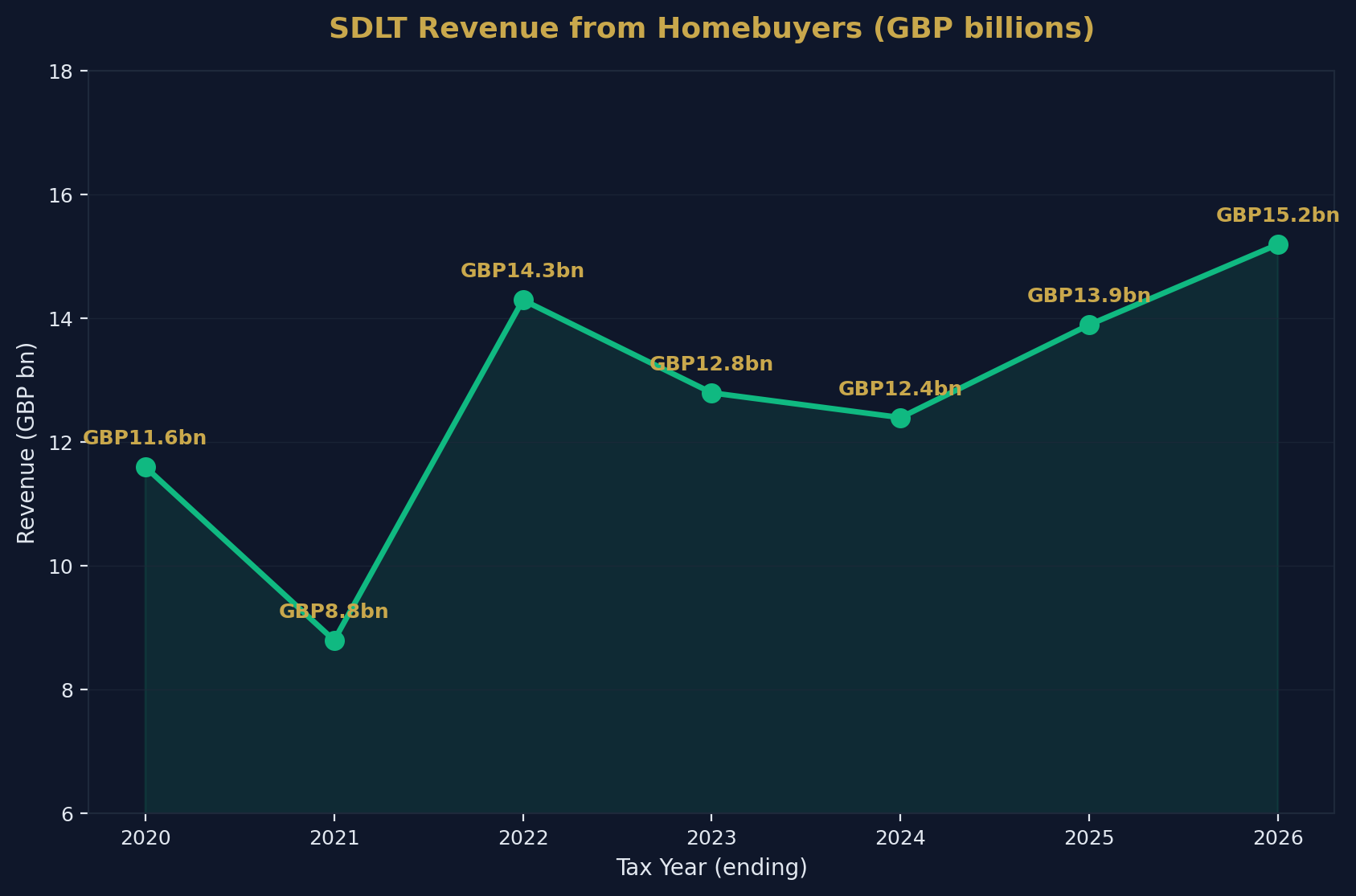

- Total SDLT receipts from homebuyers: £15.2 billion (+9.2% year-on-year).

- HMRC recorded 102,410 residential transactions in February 2026.

- The standard SDLT nil-rate threshold is £125,000 (since April 2025).

- The first-time buyer nil-rate threshold is £300,000.

- The additional property surcharge is 5% (increased from 3% in October 2024).

- The non-resident surcharge is 2% on top of all applicable rates.

- An average-priced home in England (£290,000) now attracts £5,800 in SDLT — up from £3,300 before April 2025.

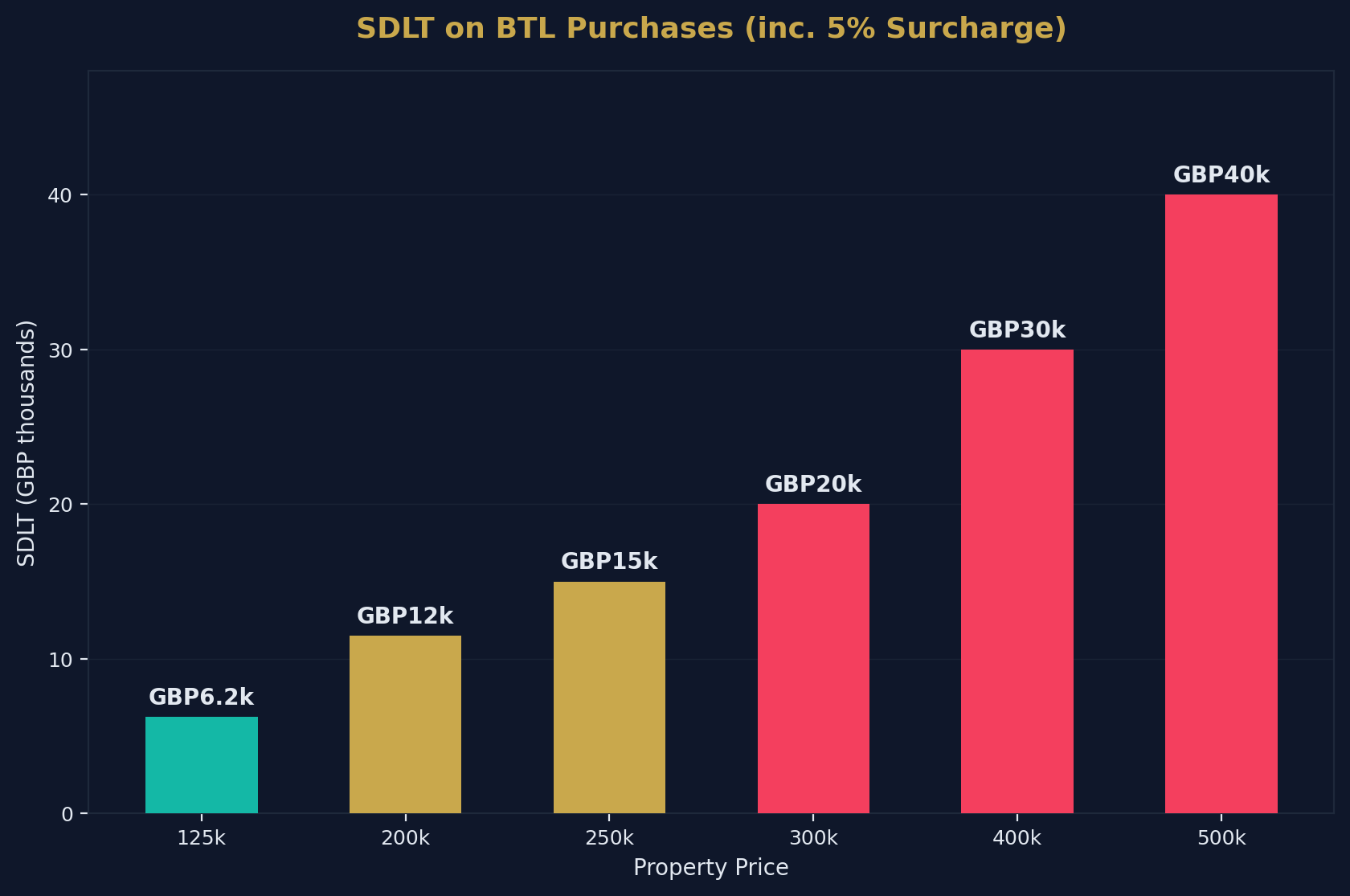

- A buy-to-let purchase at £250,000 attracts £15,000 in SDLT (including the 5% surcharge).

- Scotland's LBTT Additional Dwelling Supplement is 8% — the highest surcharge in the UK.

- Wales has a £225,000 nil-rate threshold — the most generous in the UK.

- The Q1 2025 SDLT deadline rush drove a 62% surge in first-time buyer completions.

- SDLT represents approximately 5–8% of total HMRC tax receipts annually.

Source: Shaded Canvas analysis of HMRC, Revenue Scotland, Welsh Revenue Authority, and ONS data. Last updated April 2026.

Current SDLT Rates: England and Northern Ireland

Standard Residential Rates (April 2026)

| Purchase Price Band | SDLT Rate |

|---|---|

| Up to £125,000 | 0% |

| £125,001 – £250,000 | 2% |

| £250,001 – £925,000 | 5% |

| £925,001 – £1,500,000 | 10% |

| Above £1,500,000 | 12% |

First-Time Buyer Rates

| Purchase Price Band | SDLT Rate |

|---|---|

| Up to £300,000 | 0% |

| £300,001 – £500,000 | 5% |

| Above £500,000 | Standard rates apply (no relief) |

Additional Property Surcharge (BTL / Second Homes)

From October 2024, the surcharge on additional residential properties increased from 3% to 5%. This applies on top of the standard rates across all bands.

Non-Resident Surcharge

Non-UK residents pay an additional 2% surcharge on top of all applicable rates (including the additional property surcharge if applicable).

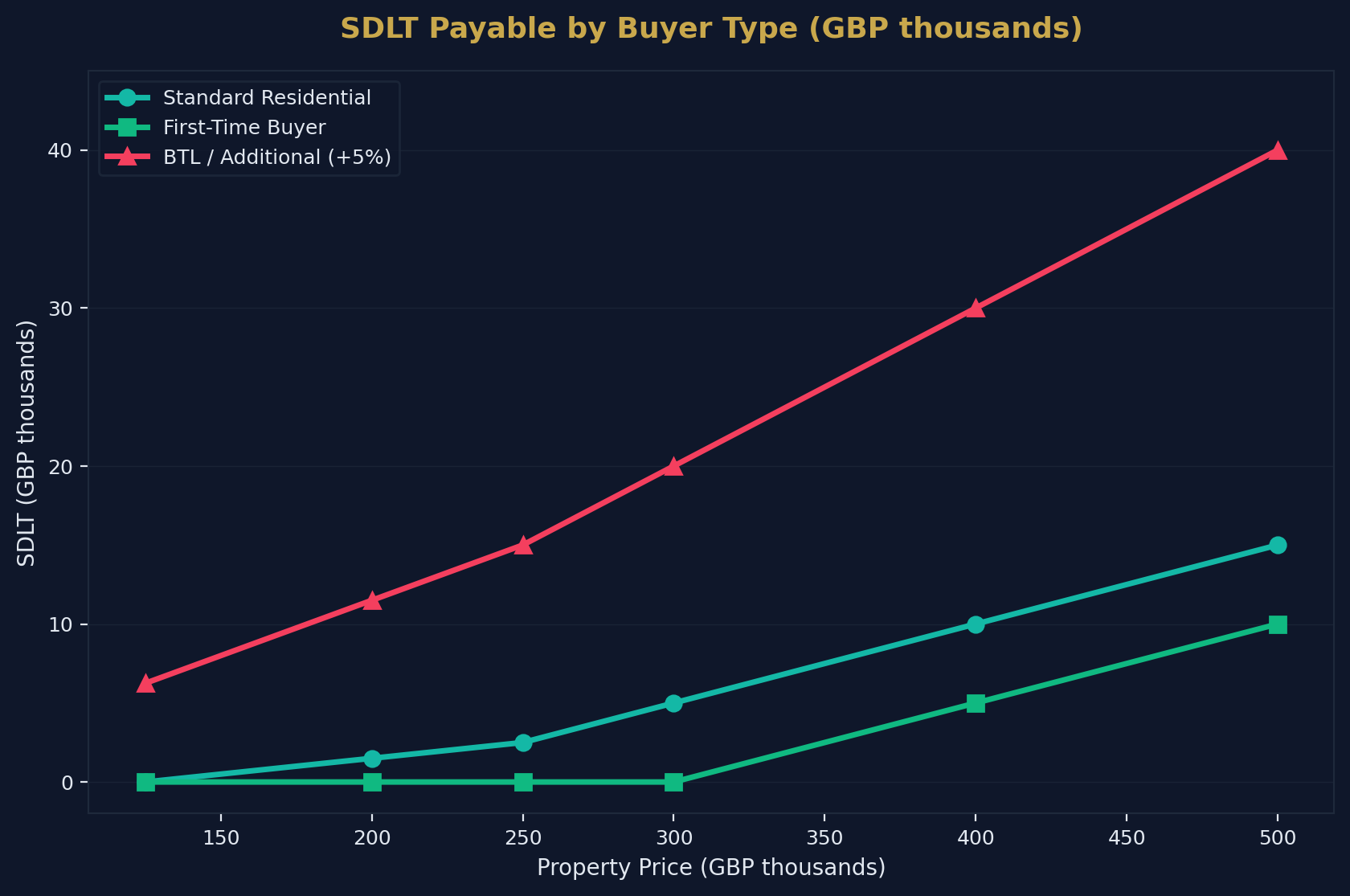

SDLT Calculation Examples

Main Residence Purchases

| Property Price | SDLT Payable | Effective Rate |

|---|---|---|

| £125,000 | £0 | 0% |

| £200,000 | £1,500 | 0.75% |

| £250,000 | £2,500 | 1.0% |

| £300,000 | £5,000 | 1.67% |

| £400,000 | £10,000 | 2.5% |

| £500,000 | £15,000 | 3.0% |

| £750,000 | £27,500 | 3.67% |

| £1,000,000 | £43,750 | 4.38% |

Buy-to-Let / Additional Property Purchases (inc. 5% surcharge)

| Property Price | SDLT Payable | Effective Rate |

|---|---|---|

| £125,000 | £6,250 | 5.0% |

| £200,000 | £11,500 | 5.75% |

| £250,000 | £15,000 | 6.0% |

| £300,000 | £20,000 | 6.67% |

| £400,000 | £30,000 | 7.5% |

| £500,000 | £40,000 | 8.0% |

First-Time Buyer Purchases

| Property Price | SDLT Payable | Saving vs Standard |

|---|---|---|

| £250,000 | £0 | £2,500 saved |

| £300,000 | £0 | £5,000 saved |

| £350,000 | £2,500 | £5,000 saved |

| £400,000 | £5,000 | £5,000 saved |

| £425,000 | £6,250 | £5,000 saved |

| £500,000 | £10,000 | £5,000 saved |

What Changed in April 2025

The temporary SDLT thresholds introduced in September 2022 ended on 31 March 2025. This was the most significant stamp duty change since the pandemic holiday.

Before vs After: Key Threshold Changes

| Threshold | Before (Sep 2022–Mar 2025) | After (Apr 2025 onwards) | Impact |

|---|---|---|---|

| Standard nil-rate | £250,000 | £125,000 | +£2,500 on average-priced home |

| FTB nil-rate | £425,000 | £300,000 | +£6,250 for FTBs at old threshold |

| FTB max purchase | £625,000 | £500,000 | More FTBs lose relief entirely |

| Additional property surcharge | 3% | 5% (from Oct 2024) | +£5,000 on £250k BTL purchase |

Impact on Buyers

The combined effect of these changes:

- Average homebuyer: An average-priced home in England (£290,000) now costs £5,800 in SDLT vs £3,300 before — a £2,500 increase

- First-time buyers in <a href="/post/foreign-investment-in-london-real-estate" style="color:#c9a84c;text-decoration:underline;font-weight:500">London/SE: Average FTB property at £400,000 now costs £5,000 in SDLT vs £0 before — a £5,000 increase

- BTL investors: A £250,000 investment property now costs £15,000 in SDLT vs £10,000 — a £5,000 increase

HMRC Revenue and Transaction Data

SDLT Revenue Trend

| Tax Year | Total Stamp Taxes Receipts | SDLT from Homebuyers | Change |

|---|---|---|---|

| 2019-20 | £15.4 billion | £11.6 billion | — |

| 2020-21 | £11.6 billion | £8.8 billion | -24% (COVID holiday) |

| 2021-22 | £18.7 billion | £14.3 billion | +63% (holiday unwinding) |

| 2022-23 | £16.8 billion | £12.8 billion | -10% |

| 2023-24 | £16.2 billion | £12.4 billion | -3% |

| 2024-25 | £18.3 billion | £13.9 billion | +12% |

| 2025-26 | £20.0 billion | £15.2 billion | +9.2% |

The 2025 Deadline Rush

The March 2025 deadline created one of the largest transaction surges in UK property history:

- Q1 2025: First-time buyer completions surged 62% year-on-year

- March 2025: Transaction volumes peaked as buyers and sellers rushed to exchange before the April threshold reduction

- Q2 2025: Transactions dipped sharply as the market absorbed the post-deadline hangover

- H2 2025: Gradual normalisation, with volumes recovering by Q4

This pattern mirrors previous stamp duty deadline rushes (2021 holiday, 2016 BTL surcharge introduction) — each creating a temporary spike followed by a proportional dip.

Scotland: Land and Buildings Transaction Tax (LBTT)

Scotland operates a separate property transaction tax system administered by Revenue Scotland.

LBTT Residential Rates (2026-27)

| Property Price Band | LBTT Rate |

|---|---|

| Up to £145,000 | 0% |

| £145,001 – £250,000 | 2% |

| £250,001 – £325,000 | 5% |

| £325,001 – £750,000 | 10% |

| Above £750,000 | 12% |

- First-time buyer relief: Nil-rate band extended to £175,000

- Additional Dwelling Supplement (ADS): 8% — the highest surcharge in the UK

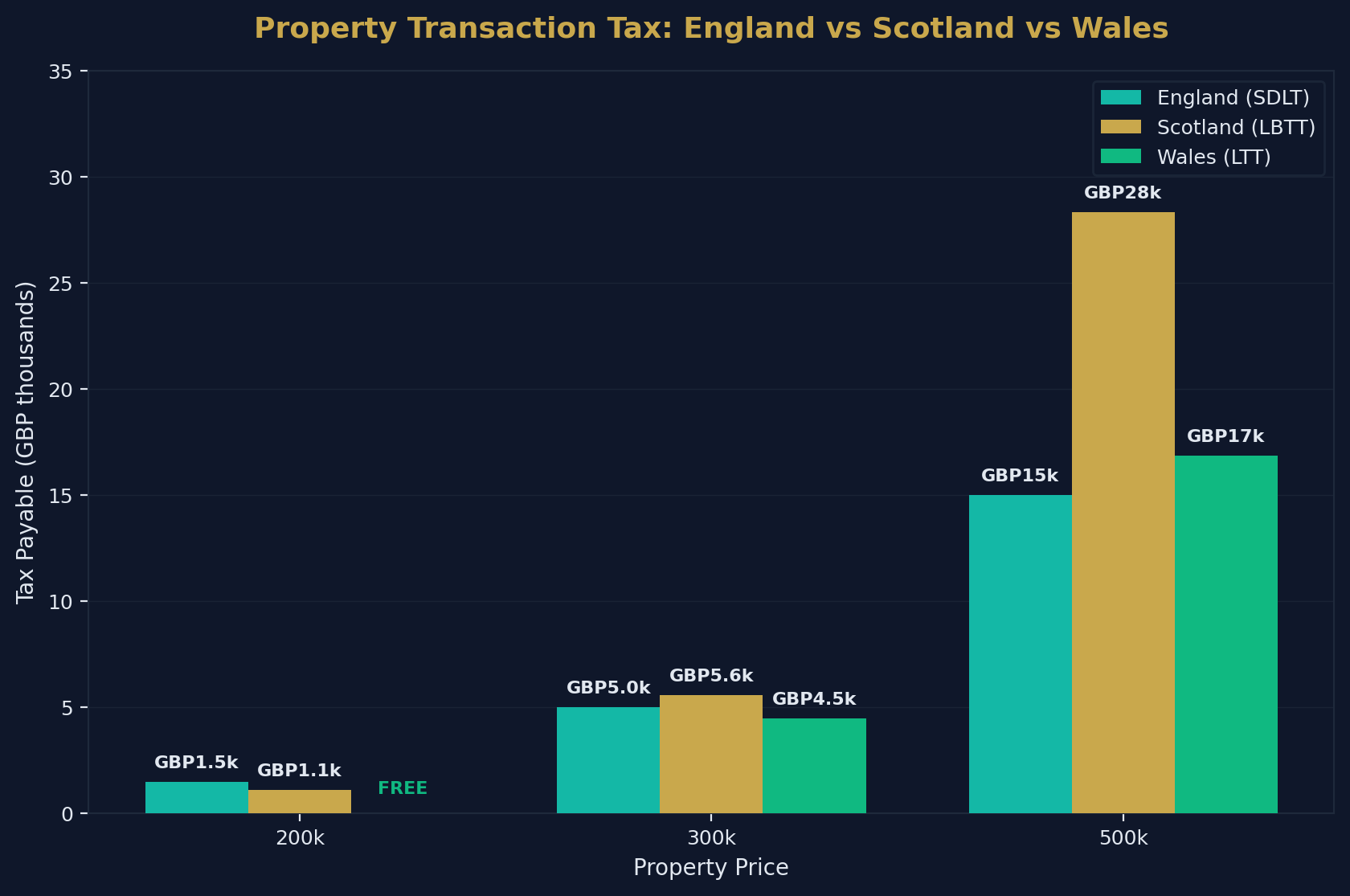

LBTT vs SDLT Comparison

| Property Price | SDLT (England) | LBTT (Scotland) | Difference |

|---|---|---|---|

| £200,000 | £1,500 | £1,100 | Scotland £400 cheaper |

| £300,000 | £5,000 | £5,600 | England £600 cheaper |

| £500,000 | £15,000 | £28,350 | England £13,350 cheaper |

At lower price points (below ~£250,000), Scotland is slightly cheaper. Above that threshold, LBTT becomes significantly more expensive than SDLT — particularly at higher values.

Wales: Land Transaction Tax (LTT)

Wales operates its own property transaction tax administered by the Welsh Revenue Authority.

LTT Residential Rates (2026-27)

| Property Price Band | LTT Rate |

|---|---|

| Up to £225,000 | 0% |

| £225,001 – £400,000 | 6% |

| £400,001 – £750,000 | 7.5% |

| £750,001 – £1,500,000 | 10% |

| Above £1,500,000 | 12% |

Key Differences

- Highest nil-rate threshold: Wales's £225,000 nil-rate band is the most generous in the UK (vs £125,000 in England and £145,000 in Scotland)

- No first-time buyer relief: Unlike England and Scotland, Wales does not offer specific FTB relief

- Steeper rates above threshold: The jump from 0% to 6% at £225,001 is the steepest initial rate increase of any UK nation

SDLT Impact on Investment Returns

For property investors, SDLT is a significant upfront cost that directly reduces returns. Here's how it impacts rental yield:

SDLT as a Percentage of Total Investment Cost

| Property Price | SDLT (inc. 5% surcharge) | Total Cost | SDLT as % of Total |

|---|---|---|---|

| £100,000 | £5,000 | £105,000 | 4.8% |

| £150,000 | £8,500 | £158,500 | 5.4% |

| £200,000 | £11,500 | £211,500 | 5.4% |

| £250,000 | £15,000 | £265,000 | 5.7% |

| £300,000 | £20,000 | £320,000 | 6.3% |

| £500,000 | £40,000 | £540,000 | 7.4% |

Impact on Effective Yield

If a property costs £200,000 and generates £12,000/year rent (6% gross yield), the effective first-year yield including SDLT drops to:

- Without SDLT: £12,000 / £200,000 = 6.0%

- With SDLT (main residence): £12,000 / £201,500 = 5.96% (minimal impact)

- With SDLT (BTL, 5% surcharge): £12,000 / £211,500 = 5.67% (0.33% yield reduction)

Over a 10-year hold period, the SDLT cost amortises to approximately 0.5–0.7% per year — meaningful but not deal-breaking for well-selected investments with strong capital growth potential. For sourced deals, the fee terms set out in a property sourcing agreement sit alongside SDLT in any realistic model of total acquisition costs.

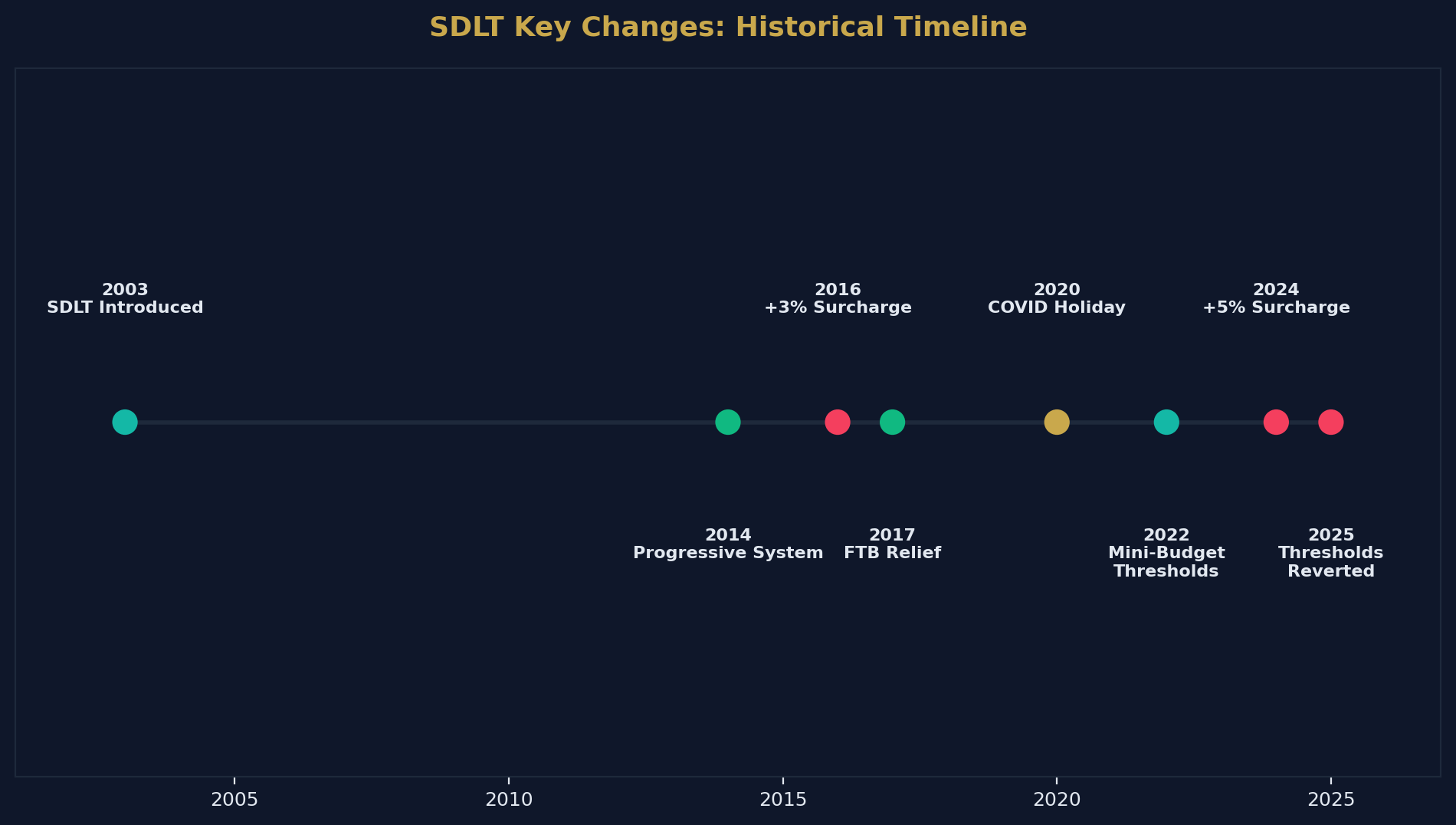

Historical SDLT Timeline

| Year | Key Change |

|---|---|

| 2003 | SDLT replaced stamp duty (slab system) |

| 2014 | Reform: progressive/tiered system introduced (Autumn Statement) |

| 2016 | 3% additional property surcharge introduced |

| 2017 | First-time buyer relief introduced (£300k nil-rate) |

| 2020 | COVID stamp duty holiday (nil-rate raised to £500k) |

| 2021 | Holiday extended then tapered (Sept 2021 end) |

| 2022 | Mini-budget: nil-rate raised to £250k, FTB to £425k |

| 2024 | Additional property surcharge increased to 5% (Oct 2024) |

| 2025 | Temporary thresholds end: nil-rate reverts to £125k, FTB to £300k (April 2025) |

Methodology and Data Sources

| Source | Data Type | Coverage |

|---|---|---|

| HMRC | SDLT receipts, transaction volumes | England & NI |

| Revenue Scotland | LBTT receipts and rates | Scotland |

| Welsh Revenue Authority | LTT receipts and rates | Wales |

| ONS | House price data, affordability | UK |

| GOV.UK | Rate tables, policy documents | UK |

How to Cite This Page

UK Stamp Duty Statistics 2026. Shaded Canvas. Published April 2026, updated quarterly. Available at: https://blog.shadedcanvas.co.uk/post/uk-stamp-duty-statistics-2026

Stop being a landlord. Start being an investor.

Shaded Canvas introduces serious capital to vetted UK property opportunities — targeting 12–16% net returns.

Start Investing →